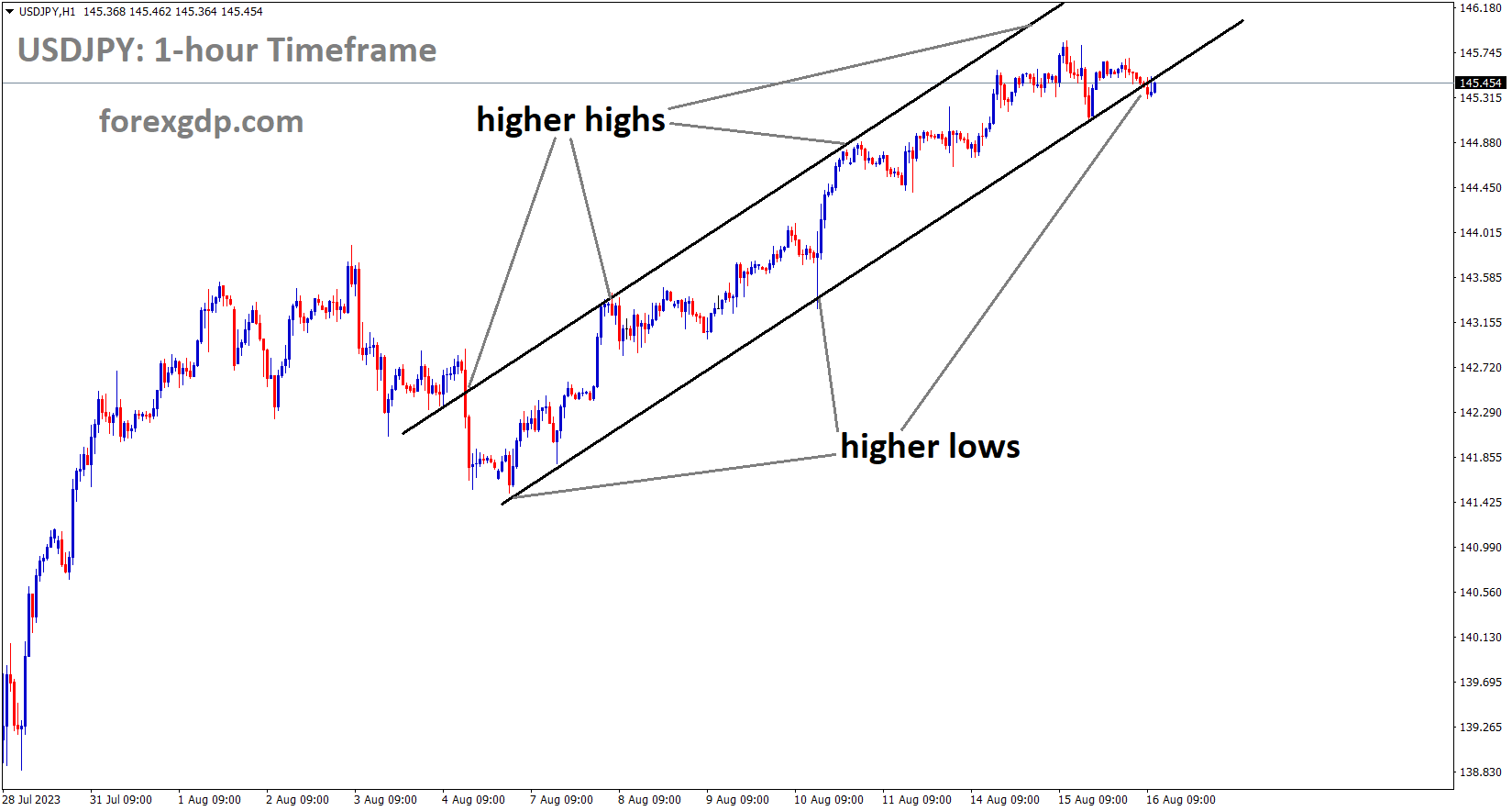

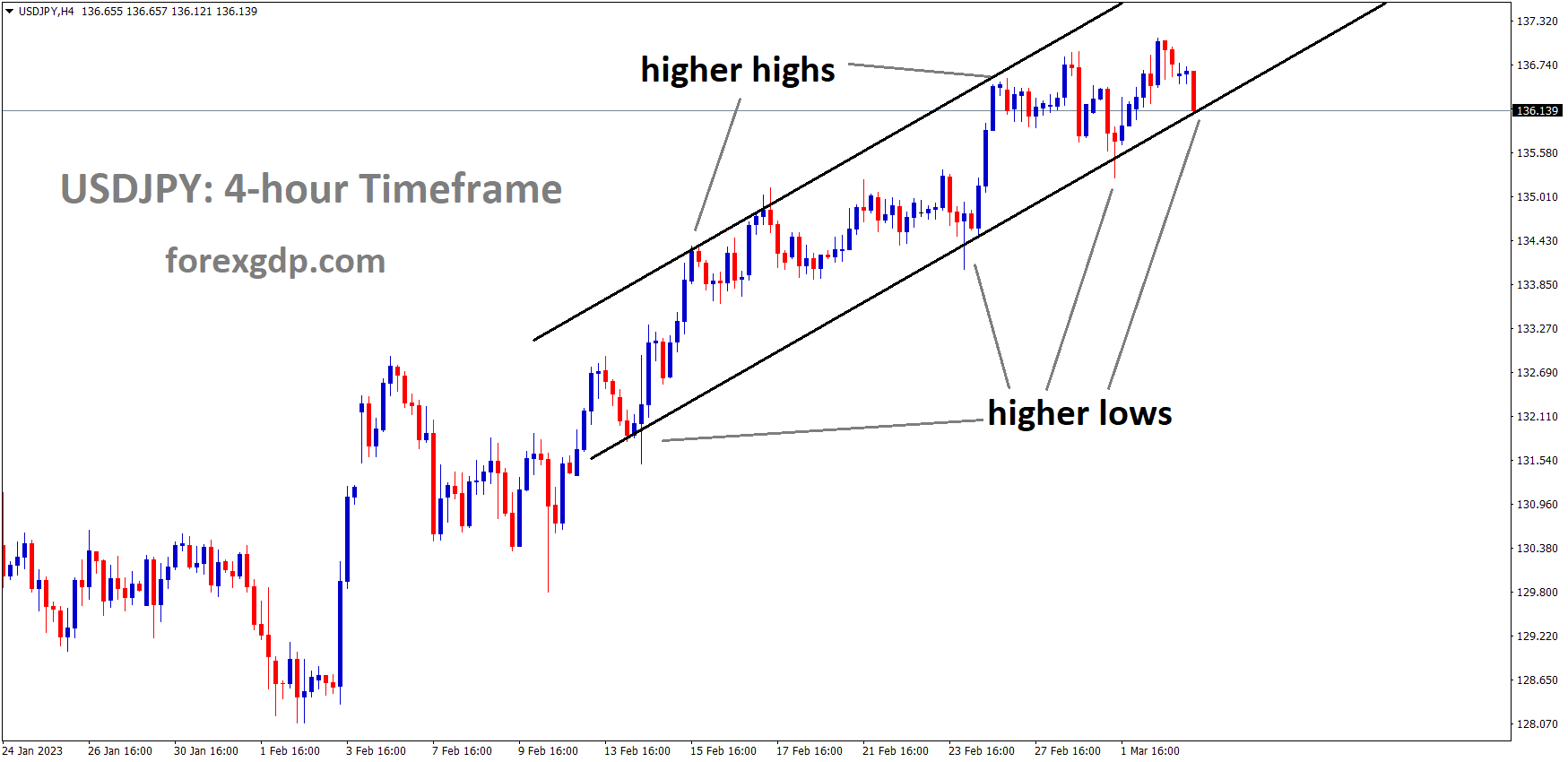

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

While many people believe the Bank of Japan is buying ETFs so they can turn a profit, Japanese Finance Minister Shunichi Suzuki has stated that this is not the case.

Despite the fact that the Bank of Japan has a plan in place for when these ETFs can be sold, energy and food prices have increased, and the Japanese government has allocated additional funds to address this problem. We are keeping a close eye on the spiralling expense of living caused by rising energy and food prices.

Japanese Finance Minister Shunichi Suzuki said in a statement following the release of the country’s Consumer Price Index (CPI) data that the government will accelerate the implementation of extra budgetary steps to deal with rising energy and food prices.

The BoJ’s purchases of ETFs are part of the BoJ’s easing strategy. Don’t believe that the BoJ’s ETF acquisitions are having a negative impact on individual asset formation. It is up to the Bank of Japan to determine how to dispose of its ETF holding. The Bank of Japan is expected to implement appropriate policy. Energy and food price increases are being closely monitored, as is the effect on people’s livelihoods.

GOLD Analysis

XAUUSD Gold price has broken the Descending channel in Upside.

old prices have consistently benefited from rising inflation rates around the globe. This scenario demonstrates that consumers are willing to pay more for goods even with higher borrowing costs and interest rates.

FED rate hikes of 50 basis points are expected at the next meeting due to higher inflation data, which will be good for US Treasury yields and US Dollar strength.

When the condition of a higher interest rate persists, the returns on non-yielding assets fall, and selling pressure on gold rises in the future weeks.

The latest consumer price index data has boosted gold and silver values because it highlights the world’s high inflation rates. Consumers will have less disposable income as a result of higher prices for products and services. While major central banks are still dedicated to reining in inflation, they plan to do so by raising interest rates, which is bad news for investments that don’t generate income.

Sticky inflation has increased expectations that interest rates will stay high for a longer period of time, despite the fact that the Federal Reserve, the European Central Bank, and the Bank of England are all committed to bringing inflation back to the 2% target. After a year of aggressive rate hikes and monetary tightening, policymakers have more evidence to support raising rates even further. Rising yields and the strength of the Dollar are being supported by the greater likelihood of a 50-basis point rate hike at the next FOMC meeting.

Gold and silver are safe-haven commodities, but they are negatively affected by rising rates because they do not produce additional income. Despite a decrease of 5.43 percent in February, rising living expenses will likely prevent any further declines.

SILVER Analysis

XAGUSD Silver Price is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

Members of the US Federal Reserve have repeatedly suggested that interest rates in FED Goal will be raised at a faster clip this summer.

The United States has published a mixed bag of domestic statistics this week, and next week FED Chairman Powell will testify before the Senate Banking Committee about releasing a semiannual monetary policy report.

Overnight, the US Dollar rose again in response to hawkish remarks from Susan Collins, president of the Boston Fed, emphasising the need to raise interest rates and the data-dependent nature of the rate hikes. Raphael Bostic from the Atlanta Fed dampened the jubilation by predicting that interest rates may crest in the upcoming summer, which was bolstered by better-than-anticipated jobless claims. However, he did state that gradual rate increases were the best course of action. Christopher Waller, the governor of the Federal Reserve, also spoke after the bell and suggested that rate increases could be more aggressive if the data warranted it.

In spite of this, overnight index swap (OIS) and futures markets are pricing in a 25 basis point increase at each of the next three Federal Open Market Committee (FOMC) meetings. Overnight, the futures market implied that the Fed’s terminal rate would be close to 5.5%. A far cry from the 4.90 percent that was predicted in January. Treasury yields maintained their march towards new highs, with the 2-year bond trading at 4.94 percent, the highest level since July 2007, and the benchmark 10-year note edging 4.0 percent.

The DXY index recouped the previous day’s losses as the New York session came to a close, but it has since weakened during the Asian session. The DXY index measures the US Dollar relative to EUR (57.6%), JPY (13.6%), GBP (11.9%), CAD (9.1%), SEK (4.2%), and CHF (3.6%). While the Federal Reserve is concerned with remaining ahead of the curve in terms of monetary policy tightening, the European Central Bank appears to be playing catch-up as inflation data there has reaccelerated. Yesterday, the Euro-wide month-over-month CPI soared to 0.8% for February, significantly higher than the 0.5% expected and -0.2% recorded in January. The year-over-year reading was 8.5% versus 8.3% predicted and 8.6% previously.

The European Central Bank (ECB) will increase the OIS market by 50 basis points at its meeting in two weeks, with the possibility of further increases of 50 basis points in the future. Yesterday, EUR/USD fell below 1.0600, but it has since recovered somewhat. Mary Daly, president of the Federal Reserve Bank of San Francisco, will speak later today, but the emphasis will be on Fed chair Jerome Powell next week. Tuesday, he will testify before the Senate Banking Committee as he presents the semi-annual Monetary Policy Report.

USDCAD Analysis

USDCAD is moving in an Ascending channel and the market has broken the higher low area of the channel.

Oil prices have risen recently due to the recovery of China’s economy, which is the world’s biggest oil importer.

Rising interest rates raise borrowing costs, reducing economic development and, as a result, oil borrowing for imported countries.

The Bank of Canada has paused its tightening strategy, resulting in a Softer CAD CPI this month.

Rate hikes only serve to keep inflation modest and the Canadian dollar strong.

The USD/CAD pair sees some selling pressure on Friday near the 1.3600 round number, and this selling pressure persists through the beginning of the European trading period. The pair is trading near 1.3575, down just over 0.10% on the day, though further losses are unlikely to be significant. The newest optimism about a strong fuel demand recovery in China, the world’s top importer, has helped keep the price of crude oil near a two-week high touched on Thursday. Consequently, this is thought to be supporting the commodity-linked Loonie, which, together with a slight decline in the value of the US Dollar, puts some downward weight on the USD/CAD exchange rate. Oil prices may be limited in their upward movement by mounting concerns that higher borrowing costs will slow global economic development and reduce demand for fuel. In addition, hawkish Fed expectations back the emergence of some USD dip purchasing and should help to limit losses for the major.

CADCHF Analysis

CADCHF is moving in the Box pattern and the market has reached the resistance area of the pattern.

Recent readings from the Consumer Price Index (CPI), Producer Price Index (PPI), and Personal Consumption Expenditures Price Index in the United States show that inflation isn’t declining as quickly as anticipated. Positive US macro statistics, such as Thursday’s Initial Jobless Claims report, also suggested a robust economy. Furthermore, many members of the Federal Open Market Committee (FOMC) have voiced their support for higher interest rate increases to bring down persistently high inflation and have indicated that they see no reason to bring down high bond yields in the United States. Rate-sensitive two-year Treasury note yields have soared to levels not seen since July 2007, while the standard 10-year US government bond yield has risen to its highest level since last November, both of which are bullish for the USD.

Bearish bets on the USD/CAD pair should be made with caution due to the recent softer Canadian CPI report published last week, which has fueled speculation that the Bank of Canada (BoC) may pause the policy-tightening cycle. Since this is the case, it will be wise to wait for significant follow-through selling before confirming that the recent upward trajectory seen over the past two weeks or so has run its course. Traders await the publication of the US ISM Services PMI later during the early North American session. However, the dynamics of the oil price should provide some real encouragement on the final day of the week.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel.

The US dollar rose to its highest level against the Swiss franc in three months, and US Federal Reserve members discussed the need for multiple rate increases in 2023 to keep inflation at or below the 2% goal.

At the G20 meetings, the United States and China resolved their tense relationship and the United States sanctioned nations that provided military aid to Russia in its conflict with Ukraine.

In the early hours of Friday, USD/CHF is trading flat around 0.9420, having retreated from the yearly peak just hours earlier. Even though the US dollar as a whole rose in value the day before, the Swiss franc rose to a three-month high against it. However, contradictory remarks from Fed officials and lacklustre US data have since challenged the bulls. The quotation may also be threatened by the cautious atmosphere preceding next month’s crucial US ISM Services PMI reading. Market participants’ hawkish stance on the Federal Reserve (Fed) was challenged by Federal Reserve Bank of Atlanta President Raphael Bostic, who suggested that the Fed might be able to halt its current tightening cycle by the middle or end of the summer. On the other hand, Susan Collins, president of the Boston Fed, said last Thursday that additional rate hikes are needed to put inflation back under control. She also said that new information will be used to decide the extent of future interest rate hikes.

According to the latest statistics out of the United States, the number of people filing for unemployment benefits fell to 190,000 in the week ending February 24 from 195,00 as predicted by the market and 192,00 the week before. In addition, Q4 Nonfarm Productivity slowed to 1.7% from 3.0% before and 2.6% market expectations, while Unit Labor Costs increased 3.6% from 1.6% before and 1.1% before. Another factor that tested public opinion was the tense relationship between the United States and China at the Group of 20 (G20) summit, where the United States was pushing for sanctions against countries with close ties to Russia and those assisting Moscow in its conflict with Ukraine. There was a risk-off attitude before the Fed’s dovish comments and talk of Sino-American trade talks, but this mood reversed afterward.

Despite these moves, Wall Street ended the day on a high note after a negative start and the S&P 500 Futures had posted slight gains as of press time. In addition, yields on 10-year US Treasury bonds hit a new peak since early November 2022, when they first broke the 4.00% barrier, while yields on 2-year bonds surged to a level not seen since 2007 (4.94%). Bond coupons have declined from their recent multi-month peak. Following this, investors in USD/CHF should focus on the US ISM Services PMI for February, which is forecast to come in at 54.5 compared to 55.2 in the previous two readings.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has broken the lower high area of the channel.

Last day, the UK Prime Minister and the EU reached an agreement on the Northern Ireland Agreement. This is good for the UK economy and has been praised by senior pro-Brexit figures for concessions to Northern Ireland.

The UK is confronting higher inflation, and the Bank of England is planning a series of rate hikes to bring it down.

Due to the strength of the US dollar on Thursday, the British pound has fallen against it. Both Kashkari and Bostic, who spoke at the Fed meeting last night, kept a hawkish slant to their advice by emphasising the importance of combating inflationary pressures and praising the strong state of the US economy and its tight labour market. What the UK’s Prime Minister and the EU agreed upon after Brexit. The trade dispute with Northern Ireland has been settled, but the most surprising aspect of this deal was the receptiveness of some prominent pro-Brexit individuals who applauded the new concessions. This is good news for the UK economy as a whole, but the money is still controlled by the central bank.

There may be some short-term relief for the pound against the USD as a result of the Brexit agreement, but the more important statistics will come from the US economy and the Federal Reserve. Recently, BoE Governor Andrew Bailey expressed ambiguous opinions in order to provide some leeway in the coming months and to avoid causing market panic. Towards the end of the day, speakers from both central banks will make public comments (details in the economic schedule), and the latest jobless claims data will provide an update on the healthy state of the American labour market.

EURAUD Analysis

EURAUD is moving in the Descending channel and the market has reached the lower low area of the channel.

Australia is China’s most important trading partner, so the country’s purchasing manager indicator recently hit a 10-year high, signalling optimism for future business.

Australia’s inflation rate was 7.4%, up from the lower level seen in the final three quarters of 2022, but the economy expanded by 0.50% over the same time period.

The RBA’s efforts to reduce inflation by raising interest rates also have an effect on the expansion of the economy.

The RBA met on March 7 to discuss interest rates; a 25 basis point increase is anticipated, with a goal rate of 4.2% by August of this year.

After yesterday’s session’s gains on buoyant Chinese economic statistics, the Australian Dollar appears to be weaker on Thursday. The official Chinese manufacturing Purchasing Managers Index hit a 10-year high, giving optimism that the world’s second-largest economy is finally regaining its vigour in the wake of the Covid Anomaly. Naturally, this boosted the Aussie dollar, as Australia is a significant business partner for China.

The Reserve Bank of Australia is widely predicted to raise interest rates again soon despite weaker-than-anticipated inflation data in Australia. As of data released on Wednesday, the domestic economy of the Australian Dollar grew by less than forecast in the final three months of 2022. While the 0.5% quarterly increase fell short of the 0.8% expected by economists, the RBA’s efforts to slow inflation are sure to trim growth, so the central bank is likely content with the avoidance of recession at this modest level of expansion.

The outlook for the Australian economy is very comparable to that of other developed economies, which should provide some support for the Australian Dollar as further rate hikes are anticipated. On March 7, the Reserve Bank of Australia (RBA) will hold a meeting at which interest rates will likely change. The futures market presently indicates a 95% probability that rates will increase by 0.25% to 3.60%. Rates are expected to reach a peak of 4.2% by August, according to the markets.

EURNZD Analysis

EURNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Adrian Orr, governor of the Reserve Bank of New Zealand, stated that excessively rapid or tardy rate increases will result in a severe economic downturn.

Rate increases or pauses cause spending and investment to collapse, which impacts foreign exchange dealers and stifles New Zealand exports.

Inflation needs to be reduced to a more manageable level. While speaking at the NZ Economics Forum at Waikato University in the wee hours of Friday morning in Asia, Reserve Bank of New Zealand (RBNZ) Governor Adrian Orr cautioned against crashing the economy prematurely and turning temporary, slower development into permanent unemployment.

In contrast to the dual mandate, a singular mandate would not be easier to implement. When you add in complications like preserving financial security and avoiding unnecessary volatility, you quickly realise that striking that delicate balance is no easy task. For instance, if the official cash rate is raised too steeply or too quickly, the economy could suffer a severe downturn, with spending and investment collapsing and the exchange rate rising sharply as foreign exchange dealers flocked to the high-yielding New Zealand dollar, thereby stifling the country’s export industry.

EURCAD Analysis

EURCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The rate of core inflation in the Eurozone in February was 5.6%, marking the third straight month of growth. Food, booze, tobacco, and energy are not included in this “core” inflation. The year-over-year rate of inflation is currently 8.5%, which is less than the 8.6% peak seen in the previous year and in line with market expectations of 8.2%.

The ECB’s persistent hints at a 50 basis point rate increase at upcoming meetings have made the Euro stronger against counter pairs.

The European Central Bank (ECB) can raise interest rates because inflation in Spain, France, the Netherlands, and Germany is still above target.

In February, the Eurozone’s core inflation rate increased for the third month in a row, reaching a new high of 5.6%. The core CPI, which excludes energy, food, booze, and tobacco, increased by 0.8%. The core number reinforces the idea that without lower energy costs, inflation will stay sticky, lending credence to the ECB’s recent hawkish rhetoric. The year-on-year inflation rate fell to 8.5 percent in February 2023, the lowest since last May, but it was still higher than market forecasts of 8.2 percent. Food, alcohol, and tobacco are anticipated to have the highest annual rate in February (15.0%, compared to 14.1% in January), followed by energy (13.7%, compared to 18.9% in January), non-energy industrial goods (6.8%, compared to 6.7% in January), and services (4.8%, compared to 4.4% in January). In terms of specific countries, France, Spain, and the Netherlands all saw increases, while German inflation remained stable.

Given the economic backdrop of the Eurozone’s various countries, the ECB’s work is difficult. The Euro has benefited from the ECB’s repricing of the hiking cycle, which is anticipated this week, with additional comments from ECB President Christine Lagarde this morning. Lagarde emphasised the importance of a 50 basis point hike this month, despite the fact that inflation is not showing indications of a sustained decline. Looking forwards to the upcoming ECB meetings and the rest of the year, inflation, particularly core inflation data, is expected to be a driving force behind the ECB’s decisions, with President Lagarde stating that the need for higher rates remains while data will be the driving force. Lagarde went on to say that the Central Bank is uncertain what the peak rate will be. Given recent data, and something I’ve been emphasising recently, the majority of inflationary pressure appears to be entrenched in the economies of many Eurozone nations, with yesterday’s German inflation report supporting this.

Don’t trade all the time, trade forex only at the confirmed trade setups.

🎁 80% NEW YEAR OFFER for forex signals. LIMITED TIME ONLY Get now: forexgdp.com/offer/