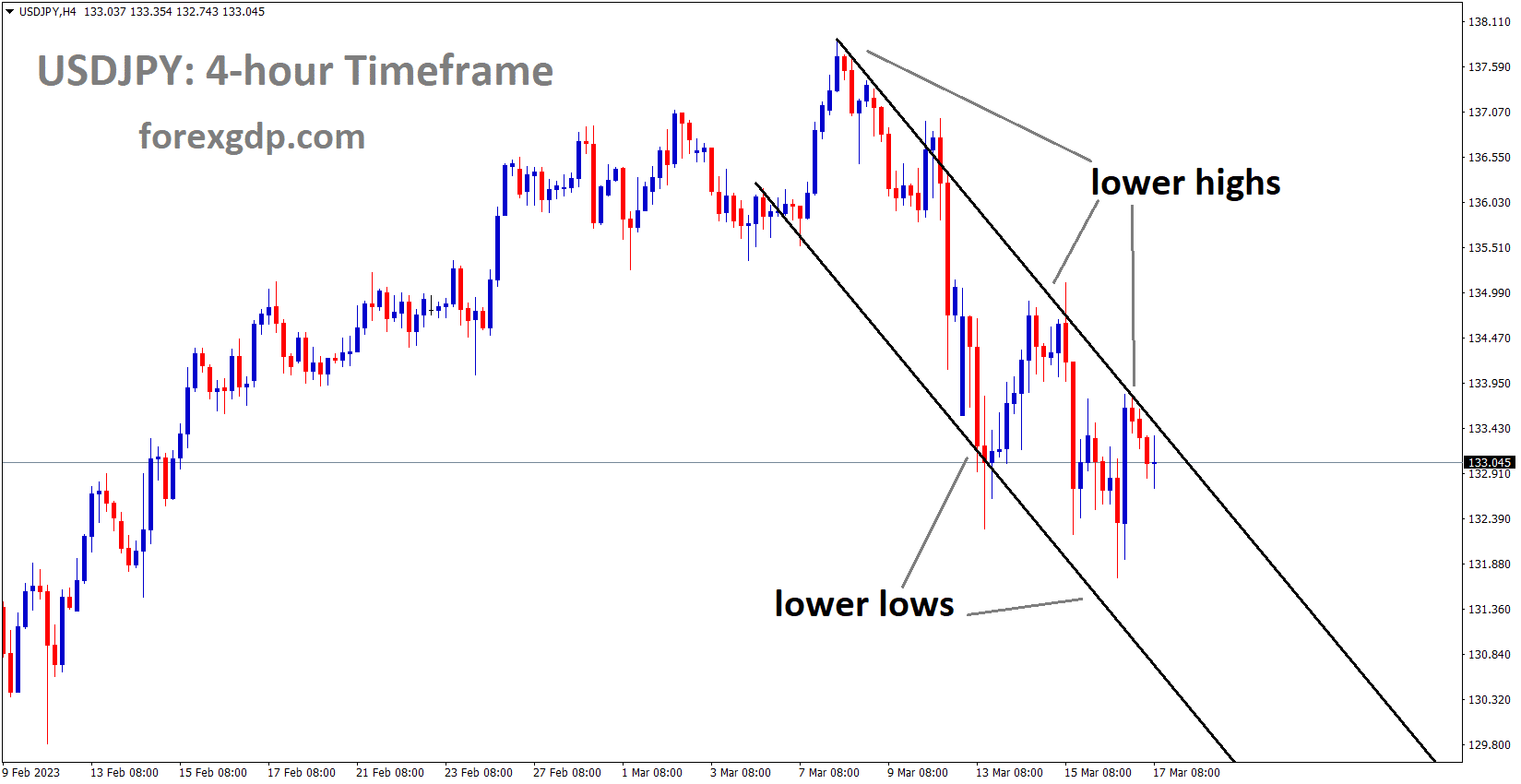

USDJPY Analysis

USDJPY is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Inflation must be addressed immediately, according to Suzuki, Japan’s finance minister, and households must raise salaries. In order to examine the financial conditions in Japan, they are in constant communication with the Bank of Japan. Goto, the minister of finance for Japan, claimed that unlike US and Swiss banks, Japanese banks are secure.

According to Japan’s Finance Minister Shunichi Suzuki, family expenses are increasing, and they must take additional steps to combat inflation. In order to respond to financial circumstances, Suzuki stated that they closely coordinate with the Bank of Japan and other central banks.

The failure of the US bank or the Credit Suisse scandal, according to Japanese Economy Minister Goto, won’t have a significant effect on the Japanese economy right now. As of Thursday’s close on the Tokyo stock exchange, the USD/JPY rate was 132.74, up to 133.40. The Thursday after Credit Suisse announced it would borrow up to $54 billion from the Swiss National Bank to support liquidity and investor trust, the currency markets were generally calmer.

USDCHF Analysis

USDCHF is moving in the Descending triangle pattern and the market has reached the horizontal support area of the pattern.

Swiss National Bank has provided Credit Suisse Bank with CHF 50 billion to guarantee its debt, and Credit Suisse will purchase CHF 3 billion of its debt as part of the bailout. The Swiss Franc’s value against Counter pairs decreased as a result of this report.

SNB prevented a 50% possibility of Credit Suisse defaulting, keeping the CHF stronger against the USD.

As markets wonder what the effects of the collapse of three US banks will be, the Swiss Franc is caught in a vortex between a banking crisis and a risk-off event. The Swiss National Bank has today helped out Credit Suisse. The troubled investment bank will receive up to CHF 50 billion in cash from them, and Credit Suisse will purchase CHF 3 billion of their own debt. Credit Suisse’s 1-year credit default swaps which cover the expense of insuring the debt of the banks, increased from 5% to 37% as of today. The share price is still significantly below CHF 2. The peak of CHF 80 reached in 2007 is now merely a distant recollection.

The Franc is frequently regarded as a safe haven in uncertain times, but currency traders are at odds with a Swiss bank at the center of the current trust crisis. Less than a week has passed since the emerging financial problems began, but the future of rates has drastically changed. The Federal Reserve’s final rate is currently around 4.85%, a significant decrease from the over 5.90% seen just last week. Despite the tight labor market and record-high inflation, Australia’s unemployment rate hit a multi-generational low today, but the futures market is now pricing in a reduction as the RBA’s next move in a few months. In each of the previous nine sessions, the bank raised rates. For the record, the unemployment percentage decreased to 3.5% in February as opposed to the predicted 3.6% and the 3.7% in January. Australian employment increased by 64.6k in the month, exceeding expectations of 50k and a prior increase of -10.9k.

Today’s GDP figures for New Zealand were lower than expected, increasing the likelihood that the island country will experience a recession. In contrast to the -0.2% forecast and 2% previous, the fourth quarter GDP was -0.6% quarter over quarter. The year-over-year reading was 2.2%, significantly less than the predicted 3.3% and prior 6.4%. Devastating cyclones and flooding that struck the nation in the first quarter of this year are expected to reduce GDP for Q1. The Kiwi fell below o.6140 but has since bounced back. Going into the North American close, Treasury rates were still falling, with the front end of the curve over 30 bp lower out to 5 years. It should come as no surprise that the MOVE index, a gauge of volatility in the Treasury market, is at its highest level since the global financial disaster in 2009.

All of this theater is taking place before today’s monetary policy decision by the European Central Bank. Bloomberg surveyed analysts who predicted a 50 bp increase, but given recent events, the interest rate market is only pricing in a 25 bp increase. The risk-off sentiment is permeating the market, turning APAC stocks into a sea of crimson. The Wall Street open may see a small uptick, according to futures. The hardest-hit sectors worldwide have been banking stocks. Crude oil fell yesterday, and it is still falling today, with the WTI futures contract trading at less than $69 per barrel and the Brent contract trading at less than $75 per barrel. With prices trading above US$ 1,900, gold has largely been able to hold onto recent advances.

GOLD Analysis

XAUUSD Gold price is moving in an Ascending triangle pattern and the market has reached the horizontal resistance area of the pattern.

Between the 11 consortium banks, First Republic Bank got USD 30 billion in deposits. Foreign institution banks like JP Morgan, Citibank, Bank of America, and Wells Fargo each gave USD 5 billion to this USD 30 billion, while Goldman Sachs and Morgan Stanley each contributed USD 2.5 billion. Less money came from other banks.

As of today, the week that concluded on March 15 saw banks borrow USD 152.85 billion from the lender of last resort, up from USD less than 5 billion the week before. This amount replaces the previous record of USD 111 billion in loans taken out during the financial crisis of 2008.

Due to the Funds arrangements provided to depositors and measures taken by the FED and US Banks to restore trust, yellow metal is now cooling.

As traders assess a hectic week that has favored the valuable metal, the price of gold has remained stable so far on Friday. The turmoil engulfing other markets has increased demand for commodities seen as safe havens, like gold. First Republic Bank received USD 30 billion in deposits overnight, according to the news. While Goldman Sachs and Morgan Stanley each contributed USD 2.5 billion, JP Morgan, Citibank, Bank of America, and Wells Fargo each contributed USD 5 billion. Less money will be contributed by other institutions. These bigger banks reportedly experienced a rise in assets as customers reduced their exposure to small and regional banks.

Additionally, the report of a significant increase in US banks using the Federal Reserve’s discount window appeared to provide some solace to the markets. Banks borrowed USD 152.85 billion from the lender of last resort in the week that concluded on March 15th, up from USD 5 billion the week before. It surpassed the previous record high, which was USD 111 billion during the world financial crisis in 2008. Additionally, almost USD 12 billion was drawn from the recently announced Bank Term Funding Program. One way in which this helps is to reassure stockholders and depositors that the banks have enough liquidity to weather the storm. On the other hand, it highlights the severity of the industry-wide confidence problem.

An rise in concern over the severity of the bank problems could be supportive of gold. If the rescue measures are sufficient to stop the tide, the market may return to concentrating on other variables that could affect the price of yellow metal. US real yields fell early in the week before rising on Friday. This may be a reflection of the belief that some calm may have been restored as a result of the liquidity measures so far revealed. If that is the case, the Fed’s aggressive downward revision in its rate hike cycle may be reversed given that inflation is still significantly above goal. In the event that higher US rates resume, the US Dollar may gain support, which could weaken gold.

USD Index Analysis

US Dollar Index is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

After banks donated USD 30 billion to consortium banks that were facing increased pressure from depositors yesterday, the US dollar recovered.

The US FED balance sheet has increased to $300 billion, which is a far cry from the financial catastrophe of 2008 and the COVID-19 era. Last day saw a rise in the US 2-year treasury, and the FED is anticipated to lower or hold interest rates in 2023 until the bank crisis is completely resolved.

On Thursday, the US Dollar outperformed its key competitors as financial market volatility continued to decline in the aftermath of Silicone Valley Bank’s collapse last week. It was reported that First Republic Bank, one of the regional lending institutions affected by the hurricane, would soon receive approximately $30 billion in rescue funding from some of the biggest banks in the country. Front-end Treasury rates increased, with the 2-year rate rising by nearly 7% in a single day.

This implies that perhaps some financial ambiguity was eliminated, allowing the Federal Reserve to possibly continue its tightening campaign to reduce inflation. The Nasdaq Composite, S&P 500, and Dow Jones all increased. The Fed’s balance sheet reportedly grew by an amazing 300 billion during this time. No, this is not quantitative easing, make no mistake. As you can see in the chart below, overall holdings increased, but the amount of securities owned in their entirety and mortgage-backed securities continued to decline, as would be expected under a quantitative tightening policy. Discount window loans blew up, rising to 152.9 billion last week. That was a greater event than the 2008 Financial Crisis or the 2020 Covid epidemic. Discount window financing mainly functions as a safety valve and a credit extension to ease liquidity pressures. It operates independently of the present medium-term rate hike/QT regime as a short-term mechanism.

USDCAD Analysis

USDCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to a global banking crisis that hit several major institutions, including those in the US and other countries, US oil fell to a multi-month low of $69 on Monday. The sharp decline in the Canadian dollar was caused by the daily decline in oil prices, which is a significant export for the Canadian economy.

FED is eagerly awaiting a judgment regarding the future course of the USDCAD Pair before raising interest rates by 25 basis points next week.

As it rises from the intraday bottom of 1.3683 to 1.3710 early on Friday morning in Europe, USDCAD consolidates weekly losses. The recent strengthening of the Loonie could be attributed to the decline in WTI crude oil, a major product for Canada. Thus, the quotation finds it difficult to explain the US Dollar’s second straight day of losses in the midst of sluggish trading on the final day of the erratic week. As risk-on sentiment in the Asian session subsides before the arrival of the European dealers, WTI crude oil loses some of its recent gains and falls back below the $69.00 mark. The conflicting headlines that suggested the market’s concerns about the global financial system may be the cause.

Crude Oil Analysis

Crude Oil has broken the box pattern in Downside.

One of the major headlines mentions Reuters’ research that suggests British companies withdrew money following the most recent banking chaos involving Silicon Valley Bank and Credit Suisse. According to Bloomberg, Hedge funds held the biggest yen-bearish positions in six months last week, a painful trade as the collapse of Silicon Valley Bank suddenly boosted demand for Japan’s currency as a haven. Along the same lines, hedge funds have rushed to secure positions using the traditional safe-haven Yen. Additionally, the sentiment is weighed down and the US Dollar is able to maintain its strength due to declining calls from hawks for the next move by the European Central Bank and uncertainty over future rate increases by the Fed.

Alternately, the moderately upbeat mood might be explained by efforts being made by lawmakers and bankers around the world to prevent a repeat of the financial crisis of 2008, as well as by statements made by rating agencies indicating that the baking industry won’t face any further difficulties. As a result of a positive finish for the Wall Street benchmarks, the S&P 500 Futures reverses the day’s early gains around 3,990 against this backdrop, while the US Treasury bond yields lose the previous day’s corrective bounce off the monthly low. In light of the upcoming Federal Open Market Committee monetary policy meeting, the US and Canadian Industrial Production for February may provide some amusement for USDCAD pair speculators. The US Michigan Consumer Sentiment Index for March and the University of Michigan’s 5-year Consumer Inflation Expectations for the same month should also be closely monitored.

EURUSD Analysis

EURUSD is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern.

In order to keep inflation rates in Europe under control, the ECB raised rates by 50 basis points yesterday. Staff think that growth will go up to 1.6% in both 2024 and 2025, and inflation will go down to 4.6% in 2023. The ECB has said that it will provide liquidity if any banking sector in Europe gets back on track. After the failure of Global banks in the US, the ECB is now more cautious about activities in the financial industry. Due to the fall of US banks, the market is now expecting the ECB to raise rates by 15 basis points in July.

In line with predictions, the European Central Bank increased interest rates by 50 basis points. Prior to the meeting, the ECB allegedly warned Ministers that certain EU banks might be exposed. According to the Central Bank, the future of monetary policy must be informed by statistics as a result of the rising level of uncertainty. Prior to the recent emergence of tensions on the financial markets, the ECB staff prepared macroeconomic forecasts. Due to a robust labor market, rising trust, and a recovery in real incomes, the staff forecasts that growth will pick up to 1.6% in 2024 and 2025. Inflation is projected to average 4.6% in 2023, which is an increase from the December forecasts and roughly half the current inflation rate. The Central Bank predicts that inflation will continue to be too high for an extended period of time.

The ECB reaffirmed that the policy toolkit is completely prepared to offer liquidity support to the Euro area financial system if necessary and added that they are closely monitoring current financial sector developments. However, the Central Bank has held off on announcing upcoming rate changes in a statement. In the immediate aftermath of the decision, market participants are factoring in possible increases of 15 bps by July. The Eurosystem does not reinvest all of the capital payments from maturing assets, so the APP portfolio is losing value at a measured and predictable rate. Up until the end of June 2023, the fall will cost an average of €15 billion per month, and its pace after that will be decided over time. The Governing Council plans to reinvest principal payments from maturing securities bought under the PEPP until at least the end of 2024. Along with its fellow Central Banks, the European Central Bank’s rate increase trajectory is becoming increasingly hazy.

Recent problems in the banking industry, particularly the Credit Suisse story, have altered market expectations and increased the likelihood that rates will be reduced in 2023. However, since the ECB is still fighting this battle, such pricing may be wrong due to the persistence of inflation. Any rate increases in the future will only be possible if the ECB is certain they won’t harm the financial industry. However, in light of today’s increase, it now seems that the Central Bank may prioritize price stability over worries about financial stability. Hopefully, today’s press conference by the ECB, the macroeconomic projections due in the next hour, and remarks by ECB President Christine Lagarde at 15:15 GMT will all shed more light on how the ECB views the rate and inflation paths moving forward. In particular as we approach Q2 2023, the EURUSD may have to wait until next week’s Federal Reserve interest rate decision to provide us with a more medium-term forecast.

GBPUSD Analysis

GBPUSD has broken the Descending channel in Upside.

The UK pound keeps rising as the UK The UK economy has benefited from the spring budget; UK Chancellor Jeremy Hunt stated that the country will escape a recession in 2023, and inflation may have decreased to 2.9% from 10.7% in the previous month. The Bank of England cannot raise interest rates if inflation slows. The Bank of England will hold its monetary policy conference the following week based on information about whether or not a rate hike is likely.

Following yesterday’s flight to quality, the financial markets are having a break in today’s early turnover. Risk assets were dumped widely and occasionally pretty indiscriminately as a result of the rollover of banking concerns from the US to Europe. Haven assets like the US dollar, US Treasury bonds, gold, and the Japanese Yen all saw strong demand. The news that the struggling banking company Credit Suisse has been given a 50 billion Swiss Franc lifeline by the Swiss National Bank to strengthen its balance sheet has helped the risk tone in the market today. Yesterday, the CDS market had Credit Swiss’ default as having a nearly 50% probability of happening at one point. As a result of the US dollar moving lower due to today’s slightly calmer market, a number of USD currencies, including cable, have been able to advance. Today’s session will end with the announcement of the ECB’s most recent monetary policy move by President Lagarde. The 50 bp increase Ms. Lagarde promised at the previous gathering must now be questioned in light of mounting financial pressure and the possibility of contagion. See the DailyFX Economic Calendar for all news releases and events that could impact the market.

The quickly changing events and market moves on Wednesday overshadowed the UK’s Spring Budget. The UK would escape a recession in 2023, according to Chancellor Hunt, and inflation would drop from 10.7% in the final quarter of 2022 to 2.9% by the end of the year. Despite remaining above the central bank’s 2% goal, this sharp decline will allow the Bank of England to scale back any additional rate increases as needed. With the FOMC rate decision on March 22 and the Bank of England’s upcoming policy meeting on March 23, next week is a significant week for cable traders. The only thing that can be assured for next week is increased volatility due to the conflicting and constantly changing market perceptions of what each central bank will do. Following yesterday’s sell-off, cable is advancing today and is trading on either side of 1.2100. The CCI indicator indicates that the pair is in overbought territory, and the short-term negative channel is still in effect. However, the 20- and 200-day moving averages have been supporting the upward movement. If the 50-dma, which is currently at 1.2137, is verified to have been broken, the pair may attempt to test Tuesday’s high of 1.2204.

NZDUSD Analysis

NZDUSD has broken the Descending channel in Upside.

Yesterday, the New Zealand Dollar recovered thanks to bank deposits obtained from major institutional institutions. Investor trust increased as a result of the Swiss National Bank saving Credit Suisse from default.

Floods that hurt the NZ economy last month prompted a decrease in NZD GDP yesterday.

NZDUSD applauds the confidence in Asian hours, which is driven by the US Dollar’s lack of vigor and a favorable risk appetite. The NZDUSD risk proxy is displaying a relief rally sparked by prompt action in the financial crisis. At the moment of writing, the pair is up about 0.68%. Along with stable US Treasury yields, the majority of Asian stock complexes are currently trading in the green. In the lack of any top-tier data from the US or New Zealand, Friday’s price movement for the NZDUSD is more likely an exploitation of the previous day. The Swiss National Bank saving Credit Suisse by giving CHF50 billion as a covered loan facility increased the risk sentiment.

Given that Credit Suisse’s financial situation deteriorated last year, and given that Deutsche Bank recently experienced a situation that was essentially similar, this is understandable. By providing a pool of liquidity reaching US$30 billion on Thursday, several significant market participants, including JPMorgan, Citibank, Bank of America, and many others, attempted to revive the First Republic Bank in the US.

In a nutshell, investors are confident that no matter what, there will be assistance from the government to smooth out any financial hiccups. Such an effort was also demonstrated during the COVID crisis, when all central banks made every effort to resurrect the economy. The market doesn’t know how many chapters on the liquidity front have yet to be disclosed, and if so, what position the central banks will take. Given that the European Central Bank did not alter its rate-hiking strategy on Thursday despite the Credit Suisse crisis. Additionally, some accounts contend that it is extremely unlikely that the Federal Reserve will make a significant adjustment at the FOMC meeting in March. The USD 250K uninsured deposit cap will not be extended to every failing bank, according to statements made previously by US Treasury Secretary Yellen. As a result, there are many issues that remain unanswered.

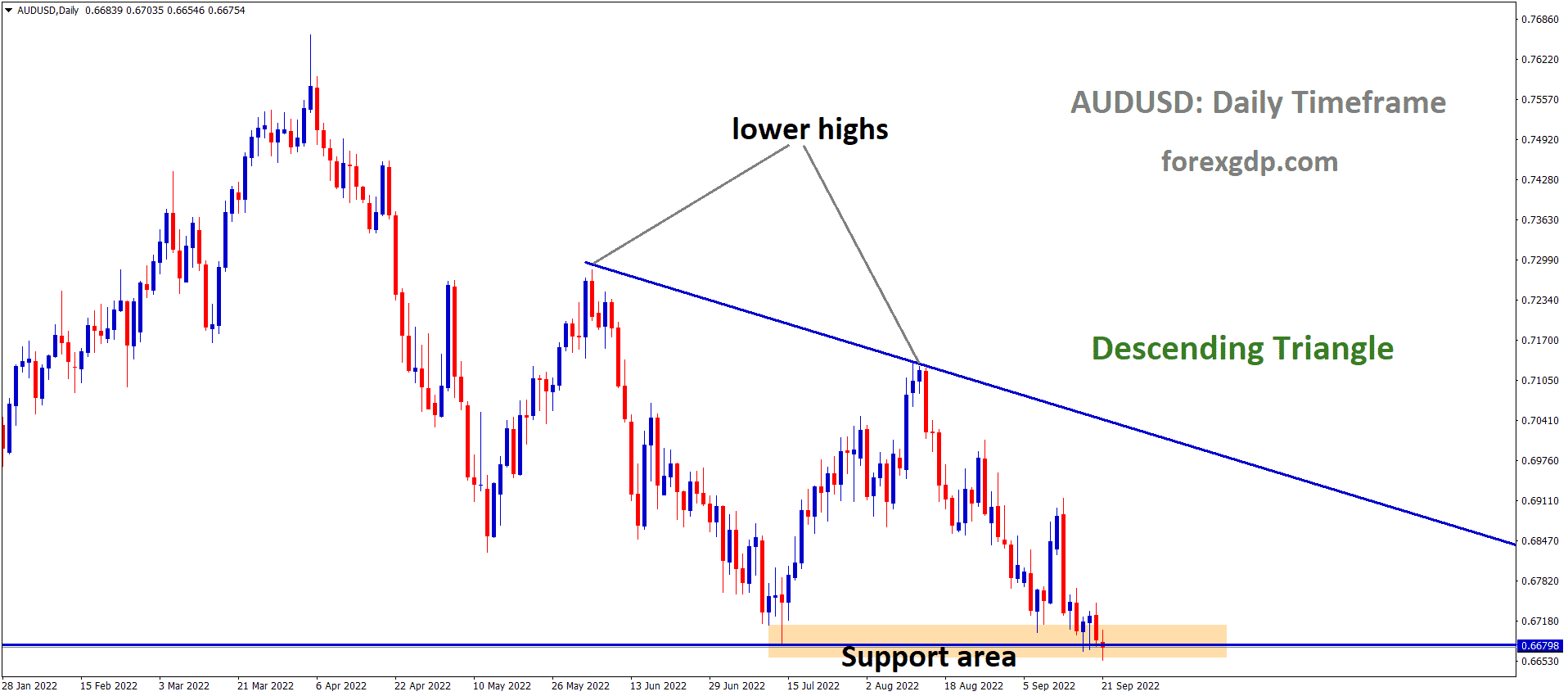

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has reached the higher high area of the channel.

Australian employment changed at a faster rate than anticipated, which gave the AUD against counter pairs a boost. After the failure of US Banks, the US Dollar plunged, which caused the AUD to recover from its lows. The Australian unemployment rate decreased from 3.7% to 3.5%, so rate hikes or cuts by the RBA may be put on hold in the future months.

Following a positive performance the day before, the AUDUSD currency pair is essentially unchanged at 0.6650 as bulls prepare for the biggest weekly gain in seven weeks leading up to the Federal Open Market Committee monetary policy conference the following week. Even though the most recent moves appear to reflect traders’ cautious mood amid a light schedule at home, it should be noted that the positive Australian data and improvement in market sentiment benefited the risk-barometer pair. Global lawmakers and banks hurried to contain the banking industry’s repercussions while favoring the market’s mood the day before. As some of the most recent market performance parallels the financial crisis of 2008, investors aren’t entirely on board and are being cautious.

However, remarks from the chairman of the Saudi National Bank, Ammar Al Khudairy, expressing the sound circumstances of Credit Suisse join the major US banks’ efforts to support the risk-on environment by assisting the California-based First Republic Bank in avoiding a liquidity crunch. Along with reports that Credit Suisse planned to borrow up to CHF50 billion from the Swiss National Bank to boost liquidity, Reuters also reported that the US institutions were less susceptible to the Credit Suisse scandal. Additionally, the sentiment was favored and the most recent run-up in the AUDUSD prices was made possible by US Treasury Secretary Janet Yellen’s assurances regarding the health of the US banking sector and the European Central Bank’s 50 bps rate increase, which was consistent with expectations. While the four-week average number decreased to 196.5K from 197.25K previously, US Weekly Initial Jobless Claims decreased to 192K for the week ended on March 10 from 205K expected and 212K prior. In addition, housing starts increased to 1.45 million in February from the previous figure of 1.321 million and analysts’ estimates of 1.31 million, and to 1.524 million in the aforementioned month from 1.34 million expected and 1.339 million in January. Additionally, the Philadelphia Fed Manufacturing Survey gauge registered a reading of -23.2 versus a consensus of -14.5 and a previous reading of -24.3.

At home, Australia’s headline Employment Change rises by 64.6K compared to the expected 48.5K and 11.5K, and the Unemployment Rate also decreased to 3.5% from the previous estimates of 3.7% and the forecasted 3.6%. Furthermore, consumer inflation expectations in Australia decreased to 5.0% for March from 5.4% market expectations and 5.1% in February. Despite the previous day’s recovery from the multi-day bottom, the 10-year and two-year Treasury bond yields for the United States are declining for the second straight week amid these plays. Furthermore, Wall Street ended the day in the black despite daily ending losses for the benchmark indices of the US Dollar of more than 1.0% each. It’s important to note that recent Fed fund futures strengthen the case for the US central bank raising interest rates by 0.25% at its monetary policy meeting next week. The concluding hints for the Fed meeting the following week are the Michigan Consumer Sentiment Index for March and the University of Michigan’s 5-year Inflation Expectation for clear directions.

Don’t trade all the time, trade forex only at the confirmed trade setups.

🎁 80% NEW YEAR OFFER for forex signals. LIMITED TIME ONLY Get now: forexgdp.com/offer/