GOLD Analysis

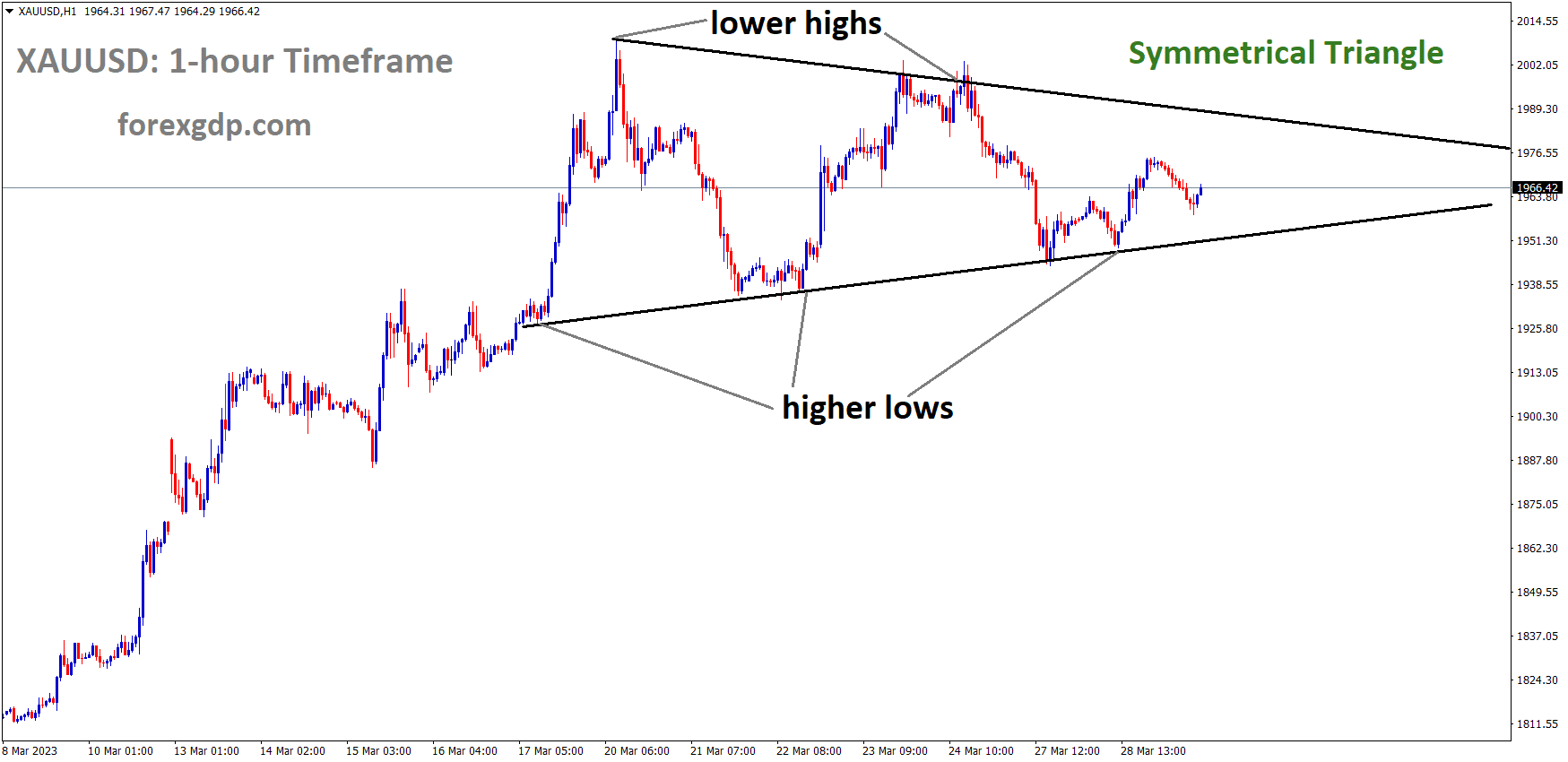

XAUUSD Gold Price is moving in the Symmetrical triangle pattern and the market has rebounded from the bottom area of the pattern.

The failure of SVB and Signature Bank in the US has led to a 7.7% increase in gold prices this month. Although yesterday’s US consumer confidence statistics exceeded expectations, the US dollar rose less quickly against other currencies.

The US economy is still experiencing market fears, and the US dollar is only declining against gold.

Over the previous 24 hours, gold values rose, rising 0.87%. As we near the end of March, XAUUSD is expected to gain 7.7% this month. If this trend continues, it will be the best showing since November. Despite a good day for the 2-year Treasury yield, the anti-fiat yellow rose. This followed upbeat US Conference Board Consumer Confidence statistics for March, despite the failure of Silicon Valley Bank and the resulting financial sector uncertainty. Fed policy forecasts have been gradually fading in markets. Despite this, the US Dollar did not fare well on Tuesday.

SILVER Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

This is most probable why gold did well. XAUUSD will be watching for important US economic statistics later this week, including the Federal Reserve’s preferred inflation gauge, PCE Core, on Friday. Stubbornly high prices would make it challenging for the Fed to manage the economy while dealing with the fallout from SVB’s collapse. This is a recipe for volatility and unpredictability. That is something that could help the US Dollar while harming gold.

USDJPY Analysis

USDJPY is moving in the Descending channel and the market has reached the lower high area of the channel.

The likelihood that the new BoJ leadership will adopt a hawkish monetary policy is diminished in the present environment.

Future Governor Ueda stated that an ultra-easy monetary policy is maintainable until inflation is brought under control and wage demands rise.

The Japanese Yen’s decline that began in the markets following the Dovish policy will continue.

In the early hours of the European trading day, the USDJPY pair is trading close to its weekly peak at 131.75. The asset is anticipated to continue moving upward towards 132,000 amid fresh concerns that the Bank of Japan will keep its ultra-loose monetary policy in place. Since a new BoJ leadership took office a few months ago, the Japanese Yen has attracted bullish wagers in the anticipation that the BoJ will abandon its decade-long expansionary policy. Expectations of a change in the policy attitude, however, have diminished because BoJ Governor Kazuo Ueda hasn’t made any hawkish comments since assuming the position of highest ranking official in the central bank.

In the meantime, ex-BoJ Governor Haruhiko Kuroda’s fervently dovish comments has fanned the flames. “It is premature to debate an exit from easy monetary policy,” ex-BoJ Kuroda said. Additionally, more time is required to achieve the price target steadily and consistently. Due to the fact that the sustained inflation goal has not yet been reached, dovish policy is necessary. In addition, the appeal of the Japanese Yen as a haven currency has diminished due to waning worries about a potential banking catastrophe in the United States. The US government is working to give investors and families confidence that their deposits are secure.

As investors anticipate that waning concerns about a US banking shakedown could increase the likelihood of another rate rise by the Federal Reserve, the US Dollar Index has also shown some signs of recovery after correcting to around 102.40. The US core Personal Consumption Expenditures Price Index data will be the primary topic of discussion this week. According to the consensus, monthly core PCE would grow by 0.4%, which would be less than the previous growth of 0.6%. Additionally, it is anticipated that the annual number will stay at 4.7%.

We don’t rely market predictions on data from each monetary policy meeting, according to Shinichi Uchida, deputy governor of the Bank of Japan. Following the inflation figures, we looked at a few indicators before deciding what to do at the time. Large-scale easing, according to former governor Kuroda, boosted markets and the economy.

USDCAD Analysis

USDCAD has broken the Descending triangle pattern in downside.

Christy Freeland, minister of finance for Canada, stated that financial institutions obtain dividends from domestic shares. Additionally, they got dividends from corporate businesses as well as tax revenue from banks and insurance firms.

That news increased the value of the Canadian dollar because the Canadian government’s revenue income increased and because higher oil prices benefited the country’s economy by increasing export revenues.

During the Asian session, the USDCAD pair encountered firm resistance near 1.3600. The downward bias for the Loonie asset appears to be strong, as the US Dollar Index appears vulnerable to further losses below 102.40. The USD Index has found intermediate support near 102.40, but it is likely to give up as risk mood improves. After easing financial concerns in the United States, the USD Index is under tremendous pressure. Fears of a US banking catastrophe have begun to fade, but remarks by US House Speaker Kevin McCarthy in an interview with CNBC on Tuesday that there was no need for blanket insurance on all bank deposits at this time, as reported by Reuters, could rekindle them.

Following remarks from US House Speaker Kevin McCarthy, S&P500 futures stayed mostly restricted on Tuesday. While the overall market sentiment appears to be positive, the Federal Reserve is anticipated to remain consistent in its interest rate decision at its next monetary policy meeting in May. Meanwhile, demand for US government bonds has stayed low as investors think the country will emerge from the banking crisis sooner rather than later. As a result, 10-year US Treasury rates increased to 3.57%.

According to Bloomberg, the Canadian Dollar remained volatile on Tuesday after Finance Minister Chrystia Freeland stated that dividends received by financial institutions from keeping domestic shares will be regarded as business income. This will result in billions of dollars in tax revenue from banks and insurance businesses who receive dividends from Canadian firms. On the oil front, the price of crude has risen to near $70.00 due to a weaker US dollar and expectations of additional penalties against Russia. The US Energy Information Administration’s oil inventory statistics will be closely monitored for additional guidance. According to consensus, the US EIA will record a 0.187 million barrel increase in oil stockpiles for the week concluding March 24. It is worth mentioning that Canada is the top oil exporter to the United States, and higher oil prices would further strengthen the Canadian Dollar.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

In advance of the Swiss ZEW and SNB Quarterly reports, Swiss Francs lost ground against comparable currency pairs.People rely on banks to protect their deposits, and we maintain more rules on banks to prevent this problem, according to the SNB, which stated that Credit Suisse’s default will be recovered like SVB Risk controlled by Fed.

During the sluggish markets on early Wednesday, USDCHF maintains buyers in control. Despite this, the Swiss currency pair increased the most the day before before showing the most recent pause above 0.9200, up 0.10% near 0.9208 at the time of publication. The most recent setbacks to the prior optimism, primarily on the global front, along with encouraging US Treasury bond yields, have contributed to the US Dollar’s late-Tuesday recovery from the weekly low. Among them are headlines implying that the US has blacklisted Chinese businesses and Beijing’s opposition to a summit between the presidents of Taiwan and the White House. The two-week peak in optimistic US inflation expectations, as indicated by the 10-year and 5-year breakeven inflation rates from the St. Louis Federal Reserve, may also put the risk-on stance to the test.

However, the risk profile remains favourable due to the Swiss National Bank’s ability to contain the Credit Suisse turbulence and the optimism surrounding the Silicon Valley Bank transaction. It’s important to note that the USDCHF pair can continue to move higher when there are no significant disappointments in the US statistics. The US Conference Board’s consumer confidence index increased to 104.2 in March from the previously reported 103.4 on Tuesday, which was higher than the anticipated 101.0. In addition, the US Housing Price Index increased in January by 0.2% MoM, beating expectations of -0.6% and readings of -0.1%, while the S&P Case-Shiller Home Price Indices met predictions of 2.5% YoY, down from 4.5% in December. The US 10-year and 2-year Treasury bond yields print a three-day uptrend around 3.58% and 4.10%, respectively, amid these moves, and the S&P 500 Futures record modest gains, the first in three days. The US Dollar Index also increases bids to 102.60, recording its first daily advances in three days.

The Swiss ZEW Survey results for March can provide the USDCHF pair with instant direction before the SNB’s Quarterly Bulletin and the secondary US data. The pair traders will look for signs of the Swiss economy’s resilience for further guidance in light of the SNB’s most recent defence of the banking sector. Above all, a clear indication will depend on Friday’s release of the US Core Personal Consumption Expenditure (PCE) Price Index for February, the Federal Reserve’s preferred inflation indicator.

USD Index Analysis

US Dollar index is moving in the Descending channel and the market has reached the lower high area of the channel.

Data on US consumer confidence were higher than anticipated last night, which had an unimpressive impact on the US dollar’s movement.

US FED stated that fundamental balance sheet mismanagement leads in SVB defaulting.

Public financial deposits made by SVB for long-maturity bonds resulted in a mismatch in the balance sheet, which prompted SVB to feel pressure to sell its long-term maturities quickly. Long-term treasury rates fall more quickly when rate increases are made in succession.

On Tuesday, the US dollar performed poorly against its main counterparts, as measured by a -0.4% drop in the DXY Dollar Index. Taking a deeper look, this month has been the worst for DXY since November, with a loss of about 2.4%. Despite improving economic statistics and a higher 2-year Treasury yield, the Greenback did not fare well with traders. Data on consumer confidence from the Conference Board was transmitted at 14 GMT. March’s actual result of 104.2 was above both the predicted 101 and the previous month’s 103.4. The effects of the failure of Silicon Valley Bank didn’t prevent this month’s uptick in optimism.

A notable finding in the study is the drop to 49.1% of respondents who said they had their pick of plentiful jobs. That was the first decline in five full months. Even so, the interpretation is more impressive when viewed through the lens of history. The Nasdaq 100 index also fell as a result of investors selling off technology companies. The latter has dropped by about 1.1%, making this week its worst performance since early March. There is no significant economic event risk in the Asia-Pacific trading period on Wednesday. As a result, investors will have to consider how the market as a whole is feeling. Ahead of the opening chime at the Tokyo Stock Exchange, futures on Wall Street are trending slightly higher. For this reason, if risk desire rises, the safe-haven US Dollar could fall even further.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Madis Muller, a policymaker at the European Central Bank, stated that bank defaults in the US and Swiss regions shouldn’t extend to our region in Europe.

The rate of inflation in the Europe zone is sharply falling, and we will shortly achieve our goal of 2% inflation in the future.

Yesterday, the EURUSD gained after US Consumer Confidence statistics exceeded expectations.

Bank problems will not extend to the Eurozone. Madis Muller, a policymaker at the European Central Bank, made the remark on Tuesday. He also noted that it is premature to celebrate the decline in prices.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

In his speech, Bank of England Governor Bailey discussed how inflation will shortly decline and rate increases will continue until the inflation target is reached.

Shop inflation in the UK economy is 8.9% versus the anticipated 8.4%, according to BRC. For the UK economy, rising food inflation is still a worry. Bank of America analysts claimed that in their opinion, the Bank of England did not raise interest rates until 2024.

In the early Asian session, the GBPUSD pair has shown choppy movement below 1.2350. After a massive rise, the Cable has stalled out, but investors are betting that it will resume its upward trajectory as risk appetite improves. Because investors do not believe the Federal Reserve will make any bold choices regarding interest rates in the near future, the major index has been supported. Even with a growing U.S. goods trade deficit, S&P500 futures were volatile on Tuesday. Reuters reports that automobiles and parts exports were particularly low, along with those of consumer and capital products. Additional merchandise shipments decreased by 2.3%.

The USDX fell sharply to near 102.40 as investors braced for ongoing pressure on the US CPI from tight credit conditions from US banks. This comes amid a turbulent climate that is prone to further financial instability. The focus will stay on the release of GDP data for the United States going forward. The annualized GDP is forecast to stay at 2.7% on Thursday. Not only that, but it’s possible that quarterly core Personal Consumption Expenditures will also stay put at 4.3%.

After raising rates by 25 basis points last week to 4.25%, the Bank of England Governor Andrew Bailey has left the door open for further policy-tightening, which has kept the Pound Sterling strong. The Bank of England would be happy to raise interest rates further if there was proof of sustained inflation. Moreover, the British Retail Consortium reported that retail price inflation across the country rose to 8.9% from 8.4%, the highest figure in 18 years. The persistent inflation in UK stores can largely be attributed to the rising cost of food. Bank of America predicts that the BoE will hold interest rates constant until 2024, meaning that there will be no further rate hikes.

AUDUSD Analysis

AUDUSD is moving in an ascending channel and the market has reached the higher low area of the channel.

Today’s Australian CPI figures were lower than anticipated, coming in at 6.8% instead of the 7.2% anticipated. This is month-over-month data; quarterly CPI data will begin in April. However, the RBA is anticipated to halt rate hikes during the month of April. Following the release of April’s quarterly CPI data, the RBA may take rate hikes or make a decision to pause at the May monthly meeting. A 25bps point rate reduction is anticipated at the conclusion of 2023.

Overnight, the Australian Dollar gained ground as rising risk appetite boosted parts of the market while leaving others unaffected. It was then undermined by today’s CPI figure, with the RBA’s rate path taking centre stage. Going into the New York close, some commodities, including the Australian dollar, New Zealand dollar, and other high beta currencies, found support. So far this week, the price of WTI petroleum oil has risen by more than 6%. On Tuesday, the market took a minor hit as speculation resumed about whether or not the Federal Reserve would raise interest rates at its upcoming meeting in early May. Investors’ concerns about a possible contagion have been allayed, at least temporarily, by the apparent resolution of the banking problem. Yesterday, US officials travelled to Capitol Hill to testify before the Senate.

Basic mismanagement of the balance sheet was emphasised as the root of SVB Financial’s problems. The bank borrowed from its clients to purchase Treasuries with a long time until maturity, creating what is known as a duration mismatch or asset-liability mismatch. This implies that long-term bonds are being used as a form of risk management for cash deposits with a maturity of zero days. The rapid increase in yields from 2018 through 2022 caused a severe decline in the worth of these bonds. No changes were made to the depositor requirement. The positive news for morale is that the SVB issue appears to be isolated to that bank rather than a systematic issue.

In any event, ahead of today’s Australian Bureau of Statistics monthly CPI figure, AUDUSD settled near 67 cents on that news. They began collecting this information in September of last year, and they’ve already released two updates in between quarterly summaries. There is a 62-73% weighted quarterly basket covered by these images. The RBA tracks the quarterly CPI in comparison to its mandated inflation goal of 2-3% across the business cycle. The current number of 6.8% year over year through the end of February is below the predicted 7.2%. The Australian dollar fell because of the reassuringly low inflation rate. Unfortunately, this monthly figure has not yet proven to be a good predictor of the complete basket CPI for the following quarter. The only way to compare the two sets of statistics is by looking at the year-over-year change through the end of 2023. There was a 0.6% variation in those images.

At their April monetary policy conference, the RBA is expected to pause for the first time in their rate hike cycle since May of last year. The market is pricing in a 25 basis point cut in interest rates by the end of the year and does not anticipate any further rate increases. Inflation data for the first quarter will be made public towards the close of April. Ahead of the RBA’s next decision in May, it will be closely monitored for clues on the validity of where inflation genuinely lies. In the aftermath of the banking crisis, US yields plummeted, but they have since stabilised. Similar to the decline in rates seen in US notes, ACGBs followed suit. The yield spread on benchmark 10-year bonds is roughly 25 basis points in support of the greenback, while the yield spread on 3-year parts of the curve is roughly 95 basis points in favour of the big dollar. Compared to the Fed, the RBA has a wider gap in the short term.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

After US Consumer confidence increased yesterday, the New Zealand Dollar gained. US House Speaker McCarthy stated that we did not require universal insurance for all institutions, but concerns about US banks still exist. Investors are stimulated to fear by this communication.

After a day of choppy trading on Monday, the NZDUSD pair is back on solid ground on Tuesday, trading in the 0.6230-0.6235 range ahead of the North American session as robust intraday gains are maintained. The US dollar falls for a second day in a row as concerns about a full-blown banking crisis subside, and this turns out to be a crucial factor supporting the NZDUSD pair. The market’s concerns about a contagion were eased after First Citizens Bank & Trust Company acquired Silicon Valley Bank. In addition, regulators’ reassurances that they were prepared to handle any liquidity shortfalls helped restore investors’ faith and reverse the recent pessimistic trend. Meanwhile, the US central bank has softened its stance on containing inflation and hinted at a pause in interest rate increases last week. This adds to the general pessimism about the US dollar and helps push the Kiwi Dollar higher against the Greenback. However, traders may be hesitant to place aggressive bullish bets around the major and further gains may be capped for the time being if US Treasury bond yields stage a strong follow-through recovery.

The NZDUSD pair has been moving back and forth within a familiar trading band for the past two weeks, indicating technical indecision over the pair’s near-term trajectory. The market’s inability to gain traction last week above the 200-day Simple Moving Average provides additional justification for hesitating before making bold optimistic wagers or repositioning for a further appreciating move. Short-term trading opportunities are now anticipated in the form of US macro news. On Tuesday, the Conference Board will issue their Consumer Confidence Index, and the Richmond Manufacturing Index will be released. This, in addition to US bond yields and general risk sentiment, could affect the USD market dynamics and give the NZD/USD a boost. However, all eyes will be on Friday’s release of the US Core PCE Price Index, the Fed’s favoured inflation gauge.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/