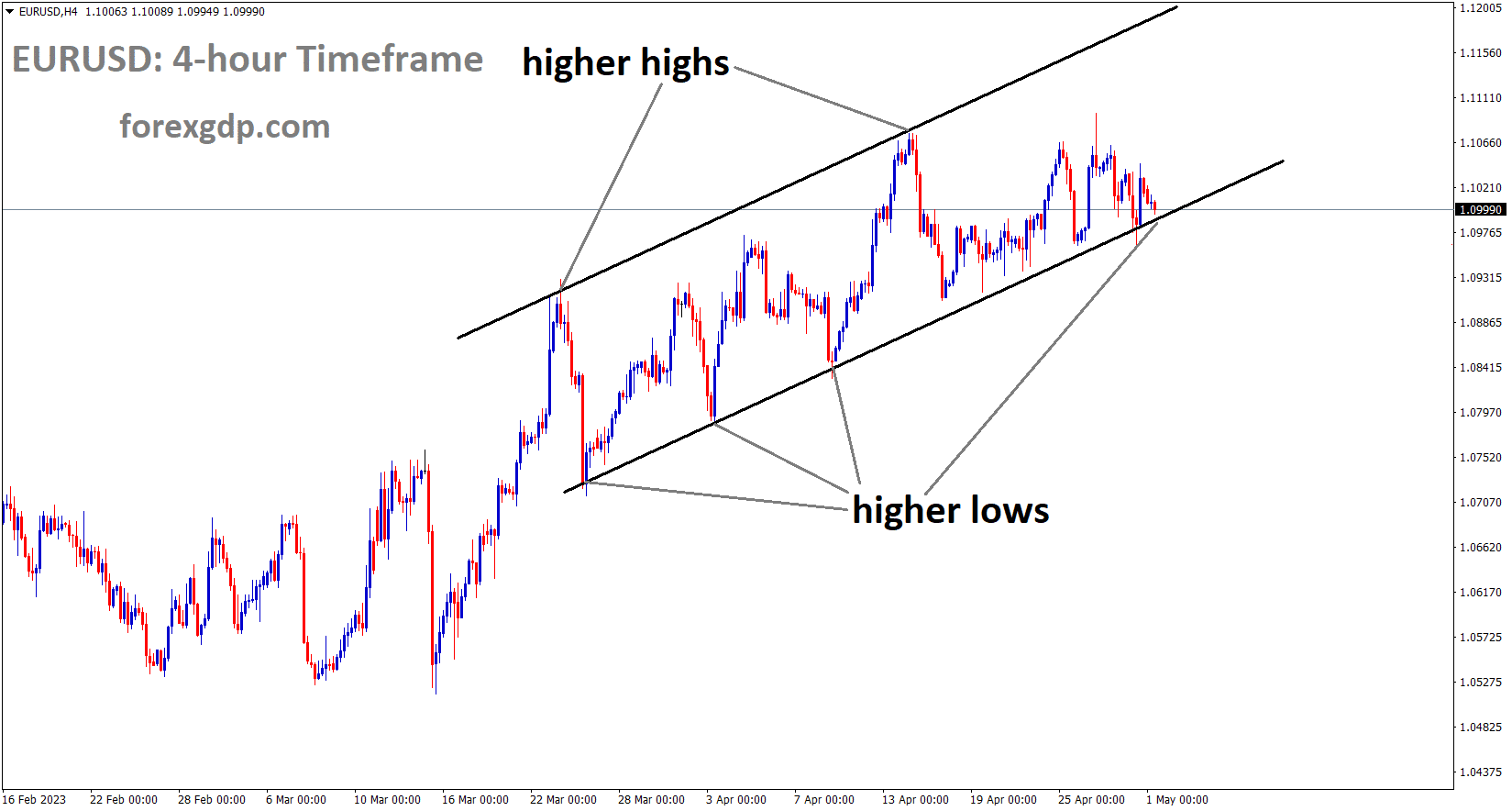

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The ECB raised the interest rate by 25 basis points this week as a result of the Euro CPI and German CPI data’s little decline from the previous reading last week.

The failure of US First Republic Bank prompts calls for the Federal Insurance Corporation and private and institutional institutions to submit bids to resolve the problem. The series of ECB rate increases will assist the Euro zone move out of the US zone’s recession region and into positive territory.

The EURUSD currency pair was offered near 1.1010 on Monday during the Asian session, continuing its third straight day of declines while remaining near its highest levels since April 2022. In doing so, the Euro pair carries the weight of both the US’s robust inflation signals as well as the recent relaxation of hawkish bets on the ECB. The concerns about an economic downturn and the problems with the First Republic present another obstacle for pair buyers at the multi-month high. After First Republic’s stock price crashed due to a withdrawal exodus, the Federal Deposit Insurance Corporation solicits bids for the troubled US bank. Nevertheless, a number of prestigious private companies, including JP Morgan, made takeover offers for the bank. The results, which are about to be made public, can only inspire naive confidence because a private player’s quick defence of the bank won’t address the larger financial issues. Contrarily, the same increases concerns about future large public banks taking similar moves, which helps to maintain the risk-off attitude.

In other places, ECB hawks back off amid negative recent numbers from the EU and Germany. According to the Harmonised Index of Consumer Prices (HICP) index, preliminary readings of Germany’s inflation for April decreased on Friday to 7.6% YoY from the 7.8% predicted and previous levels. Additionally, the country’s inflation as measured by the Consumer Price Index (CPI) decreased to 7.2% YoY from 7.3% market consensus and 7.4% earlier readings. Additionally, both the QoQ and YoY results for the initial readings of the Eurozone’s Gross Domestic Product for the first quarter of 2023 were mixed. While the annual growth slowed to 1.3% from 1.4% market forecasts and 1.8% prior, the Eurozone Q1 GDP increased to 0.1% QoQ from 0.0% prior, versus 0.2% expected. In a similar vein, Germany’s Q1 GDP increased on a quarterly basis to 0.0% from -0.4% prior and 0.2% analysts’ estimates, but the annual data fell to -0.1% from 0.9% previous readings and 0.3% market projections.

On the other hand, early projections of the US Gross Domestic Product for the first quarter of 2023, sometimes referred to as Advance readings, showed conflicting results. However, the GDP Price Index grew slightly to 4.0% on an annualised basis from 3.9% previously and 3.8% market consensus, while the headline US GDP Annualised eased to 1.1% from 2.0% expected and 2.6% prior. Furthermore, the Core Personal Consumption Expenditure (PCE) Price Index, the Fed’s preferred inflation indicator, increased from 4.7% to 4.6% in March, exceeding expectations of 4.5% and matching market forecasts of 0.3% for both MoM and YoY. Along the same lines, compared to the 1% increase seen previously, the US Employment Cost Index increased by 1.2% in Q1 2023.The CME Group FedWatch Tool indicates lower market bets on the Fed cutting interest rates in September amid these manoeuvres, as well as higher odds of the Fed raising rates by 0.25% in May and June. As a result, S&P 500 Futures register marginal losses even though Wall Street ended positively and rates decreased. Moving on, Monday’s holidays in a number of European markets may limit swings in the EURUSD pair even if the US ISM Manufacturing PMI is scheduled for release. However, the Fed meeting on Wednesday, the ECB’s announcements on monetary policy on Thursday, and the US jobs report for April on Friday will receive the bulk of the attention. Overall, bulls seem to be losing pace, but it will be difficult for bears to regain the upper hand.

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Prior to this week’s hectic US economic calendar, gold prices are consolidating. Rising US Treasury 10-year yields act as resistance to rising gold prices. Compared to non-yielding assets like gold, real yield assets are more valuable.

A critical week of US data points and a meeting of the Federal Open Market Committee are approaching, yet gold is still holding steady. Market attention will be on the FOMC meeting, however ISM and non-farm payrolls data will also be widely monitored. A 25 basis point increase in the Fed funds target rate on Wednesday has pretty much been priced in by the interest rate market. The market has almost entirely disregarded predictions for additional raises, and rate traders are anticipating possible cuts at the end of the year, so the post-FOMC press conference may have some sway. The impact of Wednesday’s decision may be greater for gold depending on how the yield curve reacts. Both nominal and real yields have recovered heading into this week after declining last week. The market-priced inflation rate determined from Treasury inflation protected securities for the same tenor less the nominal yield equals the actual yield. The 10-year real yield was as low as 1.13% early last week before rising to 1.36% on Friday. At the time of going to print today, it is currently trading slightly around 1.30%.

SILVER Analysis

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel.

The asset reached a seven-week high at that point, but there was little association with gold, with the price staying within the US$ 1,969–2,049 range it had been in over the previous month. The price of the yellow metal may be significantly impacted by changes in the real yield on Treasury bonds because it is a non-interest-bearing asset. The large USD DXY index has recently been mired in a range as a result of the lack of direction in real yields. Gold volatility has been declining due to the lack of direction in XAUUSD and the US Dollar index more broadly. The SVB collapse and worries about the US banking industry caused it to spike higher, but the swing lower may represent the market’s acceptance of gold’s overall higher levels. The GVZ index measures gold price volatility similarly to the VIX index measures S&P 500 volatility. The ‘big dollar’ and XAU/USD could move next, and the Fed meeting this week might be the trigger.

USDCAD Analysis

USDCAD has broken the Ascending channel in downside.

Canadian GDP came in at 0.10% MoM, which is far lower than expected. Lower GDP favours the Bank of Canada’s decision to maintain interest rates through 2023. Rate reductions are anticipated in early 2024 to reduce inflation and consumer spending. Following the announcement by OPEC+ to reduce oil production in March, oil prices have decreased.

Data made public on Friday revealed that, contrary to market expectations, Canada’s monthly GDP increased by 0.1% in February. The Bank of Canada should remain on hold for the remainder of 2023 rather than initiating another rate hike, according to analysts at CIBC, until rate cuts begin early in 2019.The Canadian economy had already hit a wall by March 2023 after blasting out of the gate at the beginning of the year. The monthly GDP increased by 0.1% in February, which was somewhat less than the consensus estimate and a significant slowdown from the upwardly revised 0.6% increase in January. In addition, the March advance estimate implies that GDP modestly contracted to conclude the quarter, suggesting that there will be little growth in the second quarter.

The danger of a decline in economic activity during the second quarter is increased by the weak conclusion to the first quarter and the transitory but damaging impact of the public sector strike on Q2 GDP. The Bank of Canada will, however, ignore the volatility and concentrate on working to contain inflation and inflation expectations. Although a faltering economy should prevent policymakers from initiating another interest rate hike, we do not anticipate any reductions until the beginning of next year.

USD Index Analysis

USD index is moving in the Descending channel and the market has reached the lower high area of the channel.

The US dollar ended the month of January relatively weaker. The US Non-Farm Payrolls are anticipated to decline this week as a result of the US bank crisis, while the FED is projected to boost interest rates by 25 basis points this week. US Data’s last week’s postings were less impressive than anticipated.

The DXY index, which tracks the performance of the U.S. dollar, declined slightly this past week, falling about 0.10% to 101.68, hurt by a rebound in equity markets and strong performance by tech stocks on Wall Street after strong earnings from major companies like Microsoft and Meta Platforms. High-impact events that could strengthen the U.S. dollar’s bearish bias will occur next week, therefore it is crucial to attentively monitor the U.S. economic calendar to make better trading decisions. However, the Fed’s decision on monetary policy on Wednesday and the nonfarm payrolls survey on Friday are two events that merit close attention. Let’s start with the U.S. central bank. As part of their continuous attempts to bring inflation back to the 2.0% objective, authorities there are anticipated to increase interest rates by 25 basis points to 5.00%-5.25%. Given that this choice has already been discounted, the market will focus mostly on the forecast horizon guidance.

Traders should keep an eye out for comments on the outlook as the FOMC signalled last month that its tightening campaign was coming to an end after upheaval in the U.S. banking industry heightened risks to the economy and elevated the chance of a recession. The U.S. dollar is anticipated to decline if the Fed officially presses the pause button as markets try to anticipate the next actions, which in this scenario would be rate reduction. Monetary policy divergence is anticipated to work against the dollar because other important central banks, like the ECB, are still likely to raise borrowing prices a couple more times this year. The U.S. jobs data will be the main topic of discussion on Wall Street on Friday. The U.S. banking sector crisis may have overestimated March’s data, which showed the economy adding 236,000 jobs, but the April report should make up for this error by more accurately representing those developments. For the aforementioned reason, the NFP data might fall short of expectations and produce a loss of 178,000 jobs. Soft statistics might lead to a dovish recalibration of the Fed’s policy stance, which would be bad for the U.S. currency. On the other hand, a terrible report might be good for the dollar in the near run because it would scream “recession” and cause investors to become more risk averse. Due to its safe-haven characteristics, the U.S. dollar typically benefits during times of market turmoil.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market is falling from the higher high area of the channel.

The Bank of England ought to have taken action to curb the UK’s double-digit inflation, rising food costs, and labour shortage.

The Bank of England intended to keep inflation rates low by raising interest rates, but nothing of the like happened.

In the Asian session, the GBPUSD pair is attempting to overcome the 1.2600 round-level resistance. After failing to maintain above 1.2580, the Cable has somewhat corrected. However, the degree of the Cable’s correction is noticeably smaller than the US Dollar Index’s recovery, suggesting that the Pound Sterling is still holding some strength. S&P500 futures have reduced losses from early Asia as investors have turned their attention back to the strong quarterly results released by American tech-savvy companies. The attraction of risk-perceived assets is anticipated to increase as market participants’ appetite for risk begins to revive. The USD Index is running into obstacles as it attempts to climb beyond 101.80. Despite the fact that consumer spending has consistently increased, the dollar index fell substantially on Friday. The core Personal Consumption Expenditure Price Index for March came in at 0.3%, in line with expectations and the prior report.

Spending on essential goods and services is resilient, which suggests that inflation will continue to be persistent. The Federal Reserve must remain committed to its course of tightening monetary policy. Data from the US ISM Manufacturing PMI will be the main topic on Monday. Investors anticipate modest increases in PMI numbers to 46.6 from the previous publication of 46.3. Data from the New Orders Index, which measures forward demand, is anticipated to increase from its previous release of 44.3 to 45.5. The market is predicting that the Bank of England will maintain its policy-tightening phase, which is now stopping the United Kingdom’s double-digit inflation rate. In spite of a labour shortage and continually rising food prices, the UK’s inflationary pressures are quite persistent and show no signs of slowing down.

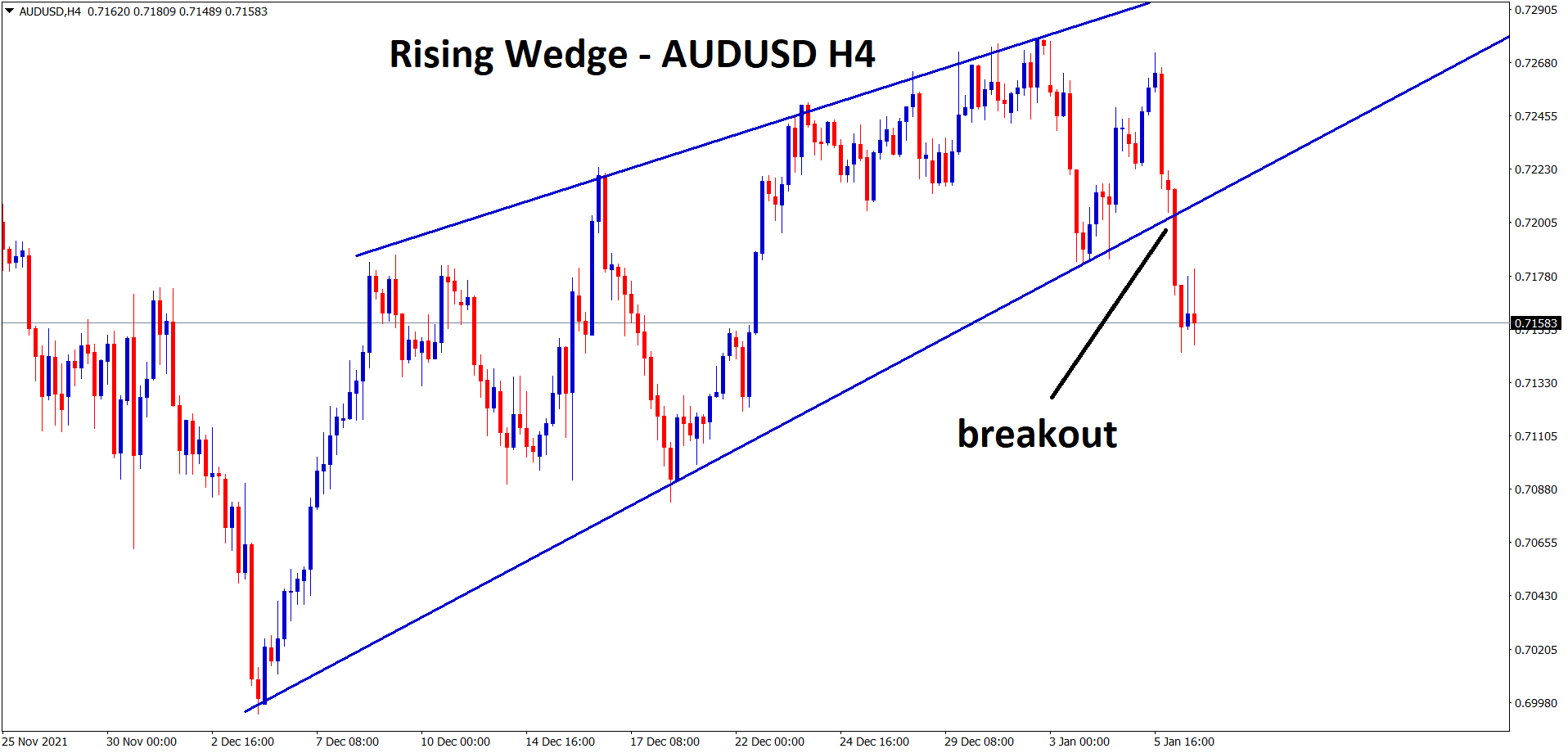

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Australian Quarterly CPI data is reported as 7.0% YoY compared to 7.8% before.

Due to the pace at which inflation is declining, the RBA may postpone the rate hike tomorrow. The rate boost will then be postponed into 2023. Since iron ore prices dropped 10% last week due to China’s slowing economy, the Australian economy is starting to pick up this week.

In the wake of CPI statistics and a macro trading environment with areas of uncertainty, the Australian Dollar declined last week. The path of the AUDUSD could be determined by the outcomes of the monetary policy meetings of the RBA and Federal Reserve this coming week. Australian headline CPI was 7.0% year-over-year at the end of the first quarter as opposed to the 6.9% predicted and 7.8% earlier. Instead of the 6.7% predicted and 6.9% seen, the RBA’s preferred metric of trimmed mean inflation for the same period was 6.6%. Price pressures have slowed down, but they are still significant and considerably beyond the bank’s required target of 2 to 3% for the cycle. The meeting minutes from the RBA’s April meeting hinted that a second rate increase would occur in May. The market anticipates no change on Tuesday, and if the bank does tighten policy, it might support the Australian dollar temporarily. The market anticipates a 25 basis point increase at the Fed’s Federal Open Market Committee meeting on Wednesday, when the Fed will convene to vote on its target rate.

A rise in AUDUSD volatility would be a legitimate prediction if either central bank departs from market expectations. Going into the weekend, market mood was a little bit mixed, with the Dow, S&P 500, and Nasdaq ending the week in the black while the Russell 2000 and the ASX 200 finished lower. First Republic’s problems seem to be becoming worse rather than better, and the market is openly debating the likelihood of the Federal Deposit Insurance Corporation acting to support the troubled bank. After falling more than 10% last week on the Singapore futures exchange, concerns over China’s recovery have continued to weigh on the iron ore price. However, copper and gold have remained stable at the same time. Looking ahead, attention will be on the RBA and Fed meetings. Any unexpected changes in the interest rate differential could cause the AUDUSD to move noticeably. especially if it affects the yield curve further out.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has reached the higher high area of the channel.

No modifications to the YCC or the Bank of Japan’s monetary policy have kept the JPY volatile against other currency pairs.

Governor of the Bank of Japan Ueda stated that once global uncertainties are reduced, inflation in Japan will quickly decline and wage increases will soon be offset. Consumer confidence in Japan increased from 33.9 to 35.4.

The Yen pair is pushing the round number of 137.00 while also refreshing the highest levels since early March. A difference between the monetary policy outlooks of the Federal Reserve and the Bank of Japan might be viewed as the primary catalyst when looking at the Yen pair’s most recent upward movements, which were the largest in 2023 The Japanese Consumer Confidence Index for the same month increased to 35.4 from 33.9 prior and 32.4 market estimates, which is noteworthy given that the final readings of Japan’s Jibun Bank Manufacturing PMI for April confirmed the initial 49.5 data, reflecting a decrease in activity.The newly appointed Governor Kazuo Ueda’s defence of the easy-money policy by asserting that it is appropriate to continue monetary easing to reach the 2% inflation objective in line with wage growth.

GBPCHF Analysis

GBPCHF is moving in an Ascending channel and the market has reached the higher low area of the channel.

In response to political and public pressure, UBS stated that the acquisition of the Swiss bank Credit Suisse is almost complete. The European Union is awaiting approval of UBS, and judgement will be rendered on June 9.

Details about the new merged bank are becoming more clear as UBS’s acquisition of former rival Swiss bank Credit Suisse approaches completion. According to NZZ am Sonntag on Sunday, UBS is attempting to separate the Swiss division of Credit Suisse and have Andre Helfenstein, the current CEO, oversee it. According to a source cited by the Swiss publication, UBS has changed its mind about a spin-off after first considering it “out of the question” due to mounting political and public pressure. UBS executives have stated time and time again that all possibilities remain open with regard to Credit Suisse’s domestic operations. Several sources were cited by NZZ as confirming that Tom Naratil, the former co-head of UBS’s global wealth management division, would return to the company after leaving in October. UBS opted not to respond.

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

As a result of ongoing rate hikes and maintaining adequate buffers to prevent losses, the RBNZ claimed that there is little danger to New Zealand banks.

Banks must maintain enough profits to handle potential rate hikes from the RBNZ and hedge funds against losses.

According to the Reserve Bank of New Zealand early on Monday, banks in the nation are relatively less at risk from rising interest rates since they are required to retain enough capital to cover potential losses. A portion of the RBNZ’s May 2023 Financial Stability Report was made public in the midst of ongoing financial concerns related to the recent collapse of First Republic Bank. The repricing profiles of banks’ assets and liabilities in New Zealand are matched, and any discrepancies are hedged using financial products. Banks are encouraged to carefully manage the risk since they must also keep enough capital to offset any potential losses resulting from any residual interest rate risk.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/