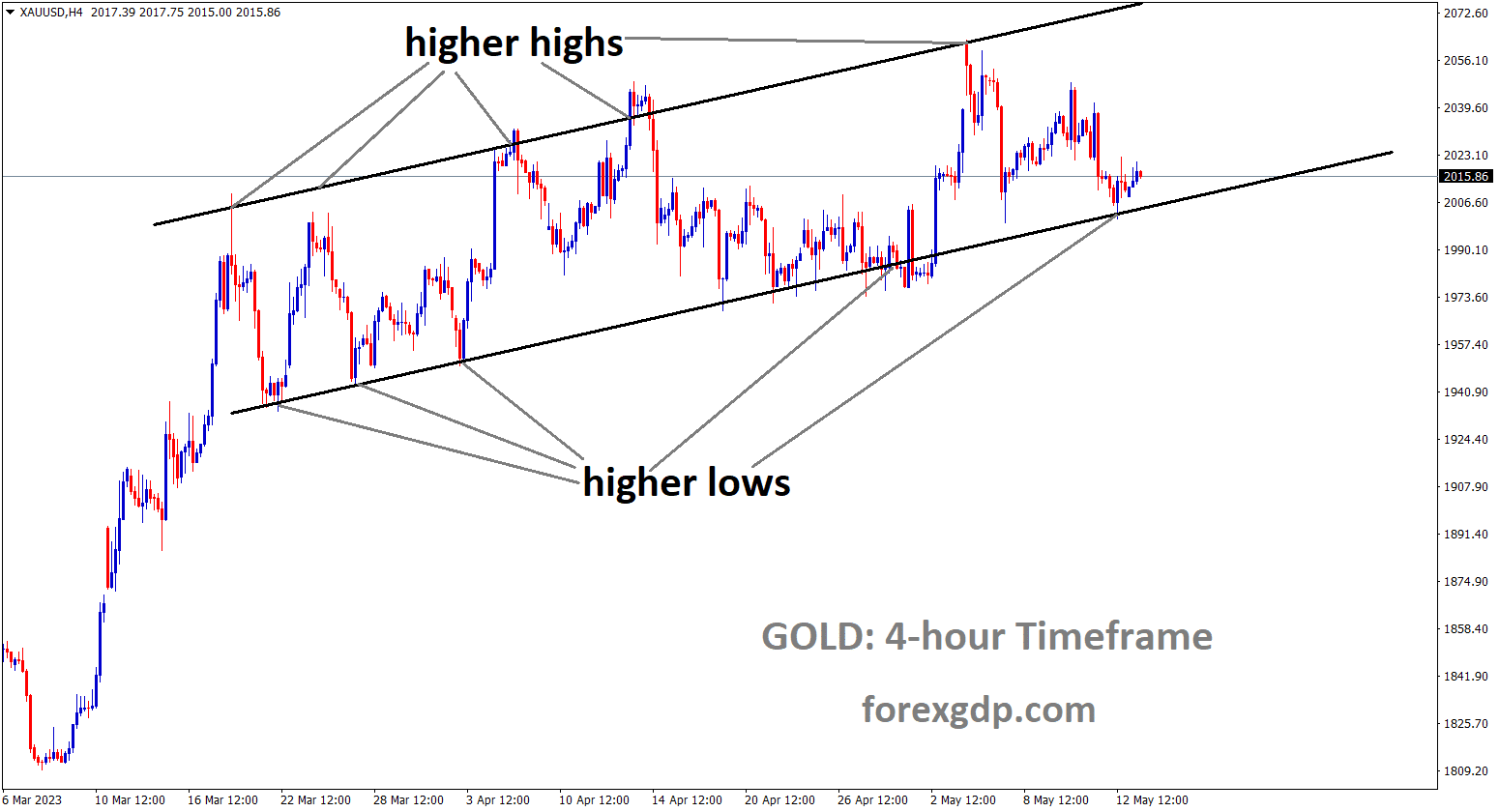

GOLD Analysis

XAUUSD is moving an Ascending channel and the market has reached the higher low area of the channel.

The annual high for gold prices was reached on Thursday of last week, and despite the US dollar’s impressive recovery, the price of the precious metal has not fallen as sharply. Building on yesterday’s impressive increase in the dollar index, the long-term inflation component of the University of Michigan consumer sentiment survey revealed the highest number since 2011. Given the appeal of gold as a safe haven at a time when US regional bank jitters and the US debt ceiling impasse have reappeared, it is challenging to argue that its recent selling is likely to turn into a runaway market. Therefore, the outlook for gold is bullish for the coming week, especially since gold bulls are likely to be lured by the possibility of a bullish continuation at the new lower levels.

USDJPY Analysis

USDJPY is moving an Ascending Triangle and the market has rebounded from the higher low area of the pattern.

While the Australian and New Zealand Dollars are stronger today following significant gains for the US Dollar last Friday, the Japanese Yen continued to decline. Japanese PPI came in higher than expected at 5.8% year-on-year to the end of April as opposed to the predicted 5.6%. This Thursday, the national CPI is scheduled to be released, and according to a Bloomberg survey of economists, the annual headline figure will rise to 3.5% from the previous 3.2%. The Bank of Japan’s decision to maintain its loose monetary policy stance may be called into question by increasing price pressure. Earlier today, the People’s Bank of China (PBOC) added 25 billion Yuan in liquidity while maintaining the medium-term lending facility (MLF) rate at 2.75%.

Despite the measure, there was little movement in the APAC equity markets on Monday, and futures point to a flat opening to the Wall Street session. Despite this, the TOPIX index for Japan is currently trading close to its 30-year high. This week, markets seem to be primarily focused on the US debt ceiling issue. US Treasury Secretary Janet Yellen made it clear over the weekend that the economy and financial markets would suffer if Congress is unable to lift it. President Joe Biden is confident that a deal will be reached, and on Tuesday, he is anticipated to meet with Speaker of the House Kevin McCarthy. Up until Thursday, both the US Senate and the US House of Representatives are in session. The President will remain in Washington until Wednesday, according to his schedule. The logistics to reach a satisfactory conclusion may become more challenging if a deal is not reached by Thursday.

USDCAD Analysis

USDCAD is moving in Descending Triangle and the market has reached the lower high area of the pattern.

As investors await the release of Canada’s Consumer Price Index and discussions regarding the US debt ceiling, the loonie asset is anticipated to remain underwhelming. After printing a new five-week high of 102.75, the US Dollar Index has shown a loss in upward momentum, which has given risky assets some strength and suggested an improvement in market sentiment. Canada’s core CPI is expected to soften from its previous release of 4.3% to 3.9% in terms of economic data. Compared to the previous release’s headline CPI of 4.3%, it is now down to 3.7%. The Bank of Canada will be able to maintain its current monetary policy following the publication of the anticipated Canada inflation report.

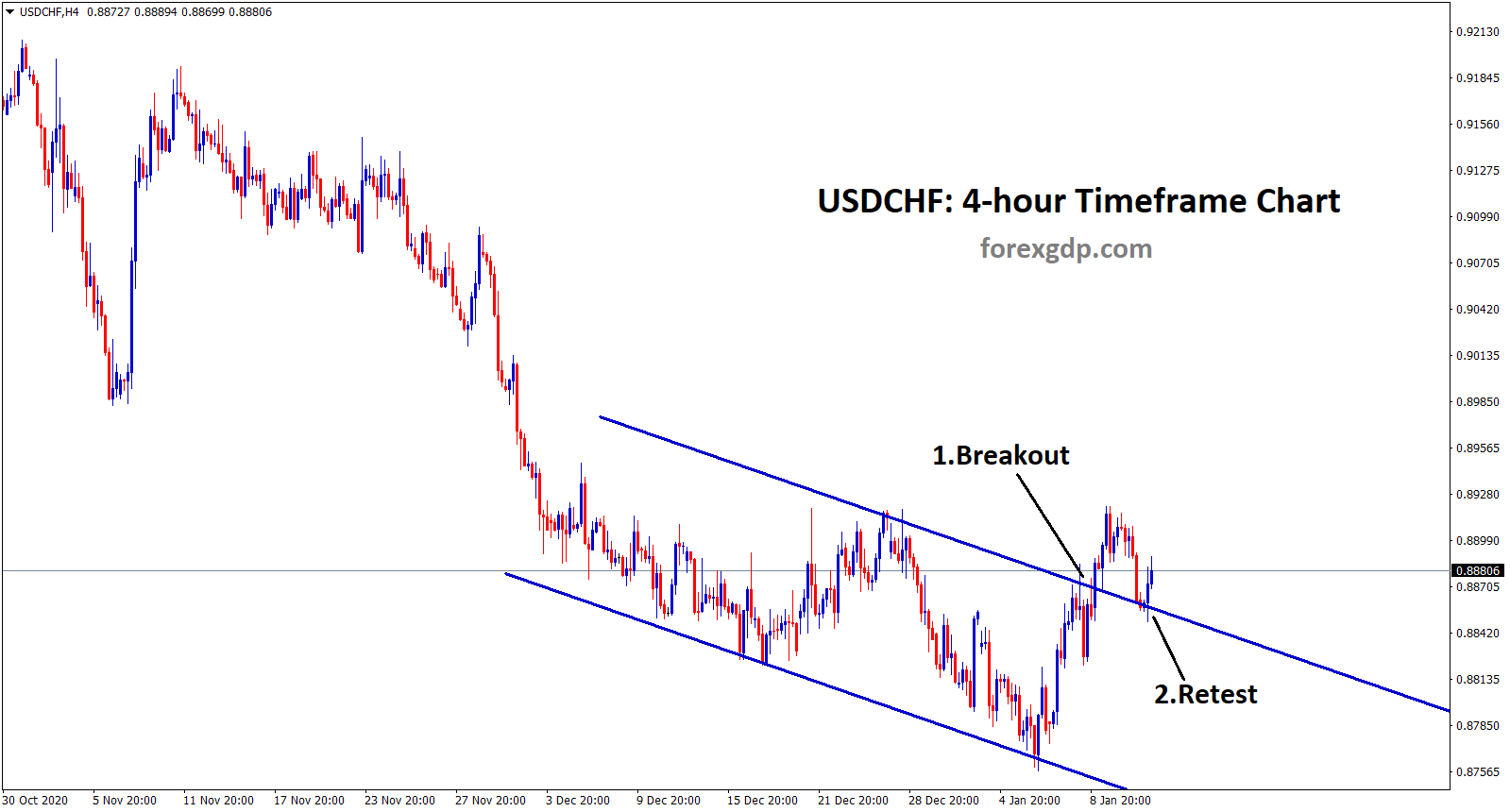

USDCHF Analysis

USDCHF is moving in Ascending channel and the market has reached the higher low area of the channel.

On Monday, negotiations for an improved free trade agreement between the United Kingdom and Switzerland will start. British Trade Secretary Kemi Badenoch will travel to Bern in an effort to increase the export of financial and professional services. Guy Parmelin, the economy minister of Switzerland, and Badenoch will meet to begin discussions on how to modernise the rollover agreement, which essentially recreated the relationship the two countries had when Britain was a member of the European Union.Badenoch said in a statement that updating our trading relationship to reflect the strength of our companies working in fields ranging from finance and legal to accountancy and architecture would benefit both the UK and Switzerland, two of the world’s top service economies. The initial round of negotiations starts on May 22.

According to the British government, trade between the two nations is worth approximately 53 billion pounds ($66.9 billion) annually, ranking Switzerland as Britain’s tenth-largest trading partner. Due to its highly developed financial sector and well-recognized legal system, Britain believes it has a strategic advantage in the areas of services and digital trade, which are not covered by the current agreement. In addition, Britain wants to facilitate business travellers’ cross-border travel, boost private sector investment, and get rid of any remaining Swiss tariffs on British products like red meat, baked goods, and chocolate, according to a statement from Badenoch’s department.

USD Index Analysis

USD Index is moving an Ascending channel and the market has reached the higher low area of the channel.

The past week saw the US Dollar surge higher against its key competitors, recording the best 5-day stretch of the year thus far. Much focus was given to the most recent University of Michigan Sentiment report as the week came to a close. It demonstrated that consumer expectations for inflation in the coming year and in the next five to ten years were higher than anticipated. This is true even though the sentiment index itself fell short of expectations. The majority of Americans are still concerned about price increases, which could have long-term effects on the economy. The most recent US CPI report broke earlier this week. The core gauge of inflation, which excludes volatile components, was in line at 5.5% while headline inflation unexpectedly fell to 4.9%. This indicates that persistent underpinning price pressures exist. As a result, traders have been gradually pricing in expectations for a near-term Federal Reserve rate hike over the past week.

The US Dollar increased on Friday as a result of rising Treasury yields and a decline in risk appetite. The coming week will see a noticeable slowdown on the US economic calendar. Retail sales, MBA mortgage applications, and initial unemployment claims are important statistics to keep an eye on. The latter is gradually rising, a warning sign that the tight labour market may be starting to worsen. The end of the week is probably when things will get the most interesting. Former Fed Chair Ben Bernanke and Fed Chair Jerome Powell will take part in a policy panel. Markets could be in for a volatile week if Mr. Powell keeps shooting down expectations for a rate cut in the near future. That is encouraging for the haven-linked US Dollar, which is also policy-sensitive.

EURUSD Analysis

EURUSD is moving in Descending Channel and the market has reached the lower high area of the channel.

Over the weekend, European Central Bank officials flashed conflicting signals about the bloc’s monetary policy and upcoming actions. The ECB interest rate hikes are nearing their conclusion, according to ECB Vice President Luis de Guindos, who made this statement to an Italian newspaper. The policymaker also cautioned that even if current indicators are positive, higher borrowing costs could have a negative impact on bank asset quality.The final stretch of our path towards tighter monetary policy has now begun. And for that reason, we are going back to normal, with 25 basis-point steps. Right now, the increased margins more than make up for any potential losses brought on by the rising NPLs.

A slowing economy and interest rate increases will increase the cost of bank funding and may result in a rise in non-performing loans. Although we do not anticipate a wave of NPLs, this is not the time to become complacent. De Guindos also issued a warning regarding shadow banks, which are non-bank financial institutions like funds and insurers that are more vulnerable to liquidity risk and are experiencing some tension. Peter Kazimir, an ECB policymaker, added that in order to help curb inflationary pressures, interest rates may need to be raised for a longer period of time than initially anticipated.

GBPUSD Analysis

GBPUSD is moving an Ascending channel and the market has reached higher low area of the channel.

Following the BoE meeting on Thursday, the GBP selloff persisted and accelerated on Friday as the GBPUSD fell under the psychological level of 1.2500, trading at 1.2460 as of this writing. As shown by sterling’s gains against the Euro, the decline in GBPUSD was more due to the dollar than the pound. The central bank’s updated growth forecasts were one of several intriguing takeaways from the Bank of England meeting. The bank maintained its recent position with hazy forward guidance, towing the line that additional increases may be forthcoming if inflation demonstrates more persistent symptoms. Taking a closer look at the BoE forecast, the Central Bank anticipates that inflation will drop to levels that are significantly below its target over the ensuing 24 months. Intriguingly, the projections do not call for any additional interest rate increases because the current rate of 4.5% is thought to be sufficiently constrictive. Energy costs are considered to be a significant factor in this. However, the BoE is navigating uncharted territory, just like many Central Banks. More so than GBP weakness, the resurgent dollar’s strength was to blame for the selloff in cable that followed the rate hike.

The UK GDP data was released on Friday morning, and by all accounts the 0.1% growth in Q1 GDP paints a positive picture. However, a closer examination reveals that the March contraction and February stall do not portend well for Q2. According to comments from the ONS, the contraction in March was an anomaly brought on by the bad weather because retail sales were also impacted.This week, the Bank of England (BoE) made it clear that two sets of data releases on wages and inflation would determine the course that the Central Bank would take in June. Given that two policymakers (Dhingra and Tenreyro) have already voted to halt rate increases, wage growth is likely to be the deciding factor. Recent BoE Business Survey data have suggested a potential moderating on this front, but let us wait and see what Tuesday’s reading reveals. A positive surprise in wage growth could increase the likelihood of a rate hike while boosting GBP demand, whereas a negative surprise could support expectations that the BoE will pause its rate hikes in June.

The general mood of the markets is still shaky, and the mounting uncertainty surrounding the US debt ceiling is only making matters worse. Although the Pound may not be directly affected, GBPUSD may experience difficulties from a USD perspective. Surprisingly, the situation with the US debt default has helped the USD recently as markets seek safe havens, with the JPY also benefiting. With any developments regarding the US default or heightened recessionary fears to be felt across markets, this creates a downside risk for the GBPUSD.

GBPJPY Analysis

GBPJPY is moving in Descending Channel and the market has reached the lower high area of the channel.

Shigeyuki Goto, Japan’s Economy Minister, said that the Bank of Japan Governor Kazuo Ueda explained at the meeting how the central bank will maintain the ultra-loose policy to sustainably and steadily achieve price target. The meeting was held on Monday and was co-hosted by the Japanese Cabinet Office and the Bank of Japan.The government and BoJ working closely together, sharing a common goal, and working towards achieving it were some of the meeting’s main topics of discussion. The government thinks it is important for the BoJ to evaluate its previous monetary policy actions. BoJ must react swiftly to any changes or economic downside risks.

AUDUSD Analysis

AUDUSD has broken the descending channel in upside.

Last week, the Australian Dollar initially rose to a new peak, but any hopes of gaining ground were dashed when the US Dollar reclaimed the ascendancy as the week came to a close. Despite some turbulence over the past few days, during which US and Chinese inflation gauges slowed, the AUDUSD rate is still confined to the range it has been in for some time. Some people who want a less hawkish Fed have cheered the easing of price pressures in the US, but the decline in Chinese CPI and PPI may portend worries about global growth in 2023. On perceived haven buying, the US dollar found support, and industrial metals fell as less demand was anticipated from China.

Some of Australia’s major exports, including aluminium, copper, and iron ore, have recently come under pressure due to lower expectations for economic growth. Wheat has also experienced a decline. Australia’s ASX 200 equity index posted a slight gain last week despite the depressing outlook. The majority of global equity indices also barely changed. At the same time, a sharp increase in US Dollar buying has caused a noticeable increase in currency volatility.For the time being, it appears that there is a limit to risk aversion in the foreign exchange market, which may reflect the market’s belief that a potential slowdown in earnings will be partially offset by a less hawkish Fed.

NZDCAD Analysis

NZDCAD is moving in Descending channel and the market has fallen from the lower high area of the channel.

The funding for up to four new schools and 300 new classrooms will be included in this year’s budget, according to the announcements made by the prime minister and the minister of education, Chris Hipkins. According to Hipkins, the funding would result in 6600 additional student spaces, 2200 of which would be available right away. Hipkins also noted that at the current pace of construction, the 100,000 additional student spaces estimated to be required in 2017 would have been built by the end of 2024. According to him, about 60,000 of those 100,000 had already received funding, which amounted to about 2700 classrooms. This means that it will take another six years to complete the remaining school buildings that will be needed, he added. He claimed that a $300 million package included in the Budget would provide funding for 300 additional classrooms, with $100 million going towards resolving immediate issues and $200 million going towards long-term roll growth. In addition to the 16 new schools that have been opened since Labour took office, Tinetti announced that an additional $100 million would be used to build up to four more. The remaining two new schools will be announced after the first two, which will be in Auckland and Papamoa. According to Tinetti, they would be put in those roll-growth areas and other places where new schools are required as determined by the National Growth Plan. Hipkins explained that in order to avoid inflating the price the government paid for the land, they would need to secure it first.

The announcement was made at Wellington’s Ridgway School, where new facilities were officially opened a year prior by Hipkins, the time’s education minister. This morning, he started by asking the students what they thought of the old buildings. One of them responded that they were worn out and dingy, and he gathered a show of hands from those who preferred the new classrooms. He remarked that it was impressive that everyone—including some teachers—had raised their hands. “We are going to build 3000 new classrooms across the nation thanks to the money we are investing in addition to the money we already have. So, 300 new classrooms are funded by the budget for this year, which is a lot. It was wonderful that the kids were in “such wonderful buildings, but we want to see every young person in this country learning in warm, dry, beautiful buildings just like this,” Tinetti said as she turned away from the microphones to speak to the kids. When Labour became the government in 2017, Hipkins told reporters that schools were overcrowded and that children were being taught in gyms and libraries. He claimed that the funding made public today would keep up the government’s funding of roughly 4000 student spots every three months. The government needed to address both literacy and numeracy issues, he said, even though it was not the ideal solution.

If teachers, students, and young people are in higher-quality spaces, teaching and learning will improve. “The quality of teaching and the quality of learning is going to be the thing that is going to turn around literacy and numeracy, and the minister can speak at great length about the work that we are doing in that area, but I am not going to say that we should just ignore the state of our school buildings while we focus on literacy and numeracy,” said the minister. The government has invested $2.1 billion in school property since the 2017 election, plus $400 million in the Schools Investment Package and $150 million in the National School Redevelopment Programme, according to Tinetti. “I have firsthand experience with some of our outdated, damp, and chilly classrooms; in fact, I have taught in them, and it is frankly not acceptable. Previous administrations might have approved of that, but not us. She also hinted at future Budget announcements for the construction of Kaupapa Mori and Mori medium schools. Relocatable classrooms were occasionally used in the short term while redesign and rebuild work was being planned, according to Hipkins, who noted that building new classrooms was frequently associated with other work like redevelopment, which could mean it took a little longer.

In order to ensure that we have the classrooms available when they are required due to population growth, we do occasionally use movable classrooms. According to him, schools were heavily involved in the design of the spaces, which helped them achieve the teaching style they desired. Hipkins acknowledged that they frequently lacked air conditioning but stated that the goal was to keep gyms and libraries out of classrooms. Hipkins has hinted at a straightforward budget on Thursday that will fund the issues that matter most to New Zealanders, such as assistance with living expenses and cyclone relief.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/