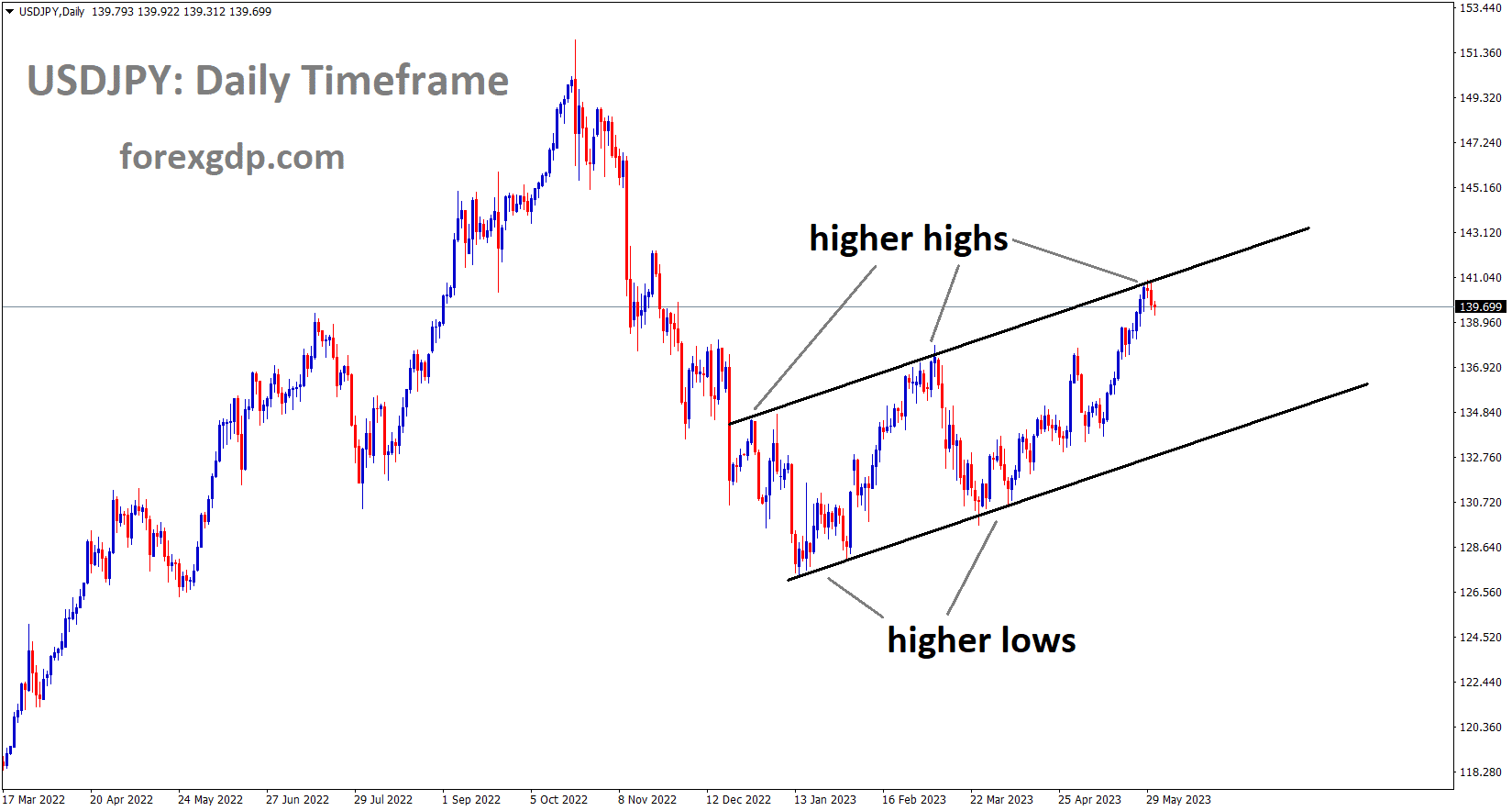

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher high area of the channel.

Japan’s industrial production for the month of April fell to -0.40% from a gain of 1.4% and a previous reading of 1.1%. The loose monetary policy of the Bank of Japan makes the Japanese Yen vulnerable to Counter pairs. JPY weakness against USD was brought on by lower-than-expected China manufacturing PMI data in May.

As markets readjusted to the possibility of Japanese authorities intervening in USDJPY on Wednesday, the Japanese Yen appreciated towards the end of the Asian session. Japanese Vice Finance Minister for International Affairs Masato Kanda hinted late on Tuesday that the government might take action to stop the depreciating Yen. We will closely monitor changes in the currency market and take the appropriate action as necessary, he said. He continued, “If necessary, we will not rule out every option available.” In relation to intervention, he added, “The Bank of Japan directly intervened several times last year as USD/JPY rose.” The bank persevered and continued selling USDJPY towards the peak near 152 despite its initial attempts to stop the flow by buying Yen near 137. In retrospect, the jawboning would have seemed inevitable with the USDJPY above 141. There is still a chance that market participants will hear more verbal appeals. For the time being, the BoJ’s extremely loose monetary policy is still in effect, and today’s industrial production in Japan is not seen as supportive of a shift in the stance. In April, output fell from the previous month by 0.4%, falling short of expectations for a 1.4% increase.

As of Wednesday, it appears that the next few meetings will be centred around passing the debt agreement. After several remarks made by Washington lawmakers over the course of the previous night, it is anticipated that it will pass. With the exception of USD/JPY, the US Dollar is stronger overall, with the high beta AUD and NZD bearing the brunt of the Chinese PMI numbers coming in below expectations. Chinese manufacturing PMI for May came in at 48.8 versus the expected 49.5, and the non-manufacturing component registered at 54.5 versus the anticipated 55.2. As a result, the composite PMI reading decreased from 54.4 to 52.9. The outlook for slowing growth in the region is becoming apparent as APAC equities are all down. The only positive aspect of today’s trade is South Korea’s KOSDAQ.

After falling overnight, Treasury yields are stable heading into the European session. The largest drops were seen in the 2-year note, which is currently trading at 4.4% after edging 4.64% late last week. With the front-month COMEX futures contract now trading back near US$ 1,980 after yesterday’s bounce off support at US$ 1,936, the decline in yields boosted gold. After yesterday’s collapse, crude oil is still under pressure. While the Brent contract is below US$ 73.50 bbl, the WTI futures contract is below US$ 69.50 bbl.

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel.

Prior to the US Debt Deal, which is expected to be completed by June 5th and the Voting system set up by today, gold prices are stabilising. This will prevent the US from defaulting on its obligations to make the aforementioned payments. This Friday, US Non-Farm Payroll data will be released. Yesterday, US Consumer Confidence data came in higher than anticipated, which caused Gold’s value against the USD to decline.

After defending its close support level of $1,950.00 during the Tokyo session, the price of gold has begun to recover. In general, the price of the precious metal is stabilising between $1,953 and 1,960 as investors wait for the publication of the United States Employment data. S&P500 futures have added more losses in Asia, indicating a decrease in market participants’ willingness to take risks. After successfully holding the key support level of 104.00, the US Dollar Index has produced a V-shaped recovery. Investors should take note that despite the extreme strength of the US Dollar bulls, the Gold price has been able to defend the downside. Falling US Treasury yields are boosting the price of gold. The US Treasury yields have been significantly impacted by growing optimism that the novel US debt-ceiling proposal will pass with flying colours in Congress. Ten-year US government bond yields have decreased by 3.68%.

A cautious approach should be used because the US Dollar’s strength and growing expectations of another Federal Reserve interest rate hike could put pressure on the price of gold. The US JOTLS Job Openings data and the publication of the Fed’s Beige Book will be closely watched in the coming months. Estimates show that there are now 9.375 million fewer job openings overall than there were when 9.59 million were released.

US Dollar index

US Dollar index is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The US Consumer Confidence data came in higher than anticipated the day before, pushing the USD up against other currency pairs. Still, a deal on US debt must be reached by today or this week in order to prevent a default on June 5th. The two main factors influencing the direction of the US dollar this week are the US ADP employment change and the US non-farm payrolls data.

The US Dollar Index maintains Tuesday’s retreat from a multi-day high early on Wednesday while retesting its intraday low near 104.00. As a result, after reversing from the highest levels since mid-May on Tuesday and breaking the five-day uptrend, the gauge of the greenback against six major currencies declines for the second straight day. The market’s worries that US policymakers will block the US debt ceiling agreement in Congress despite an impending default may be the cause of the dollar’s most recent decline. Mixed US data and month-end positioning are supporting the DXY’s decline. Speaking of the numbers, the Consumer Confidence Index for the US Conference Board fell slightly in May from an earlier reading of 103.70 (upwardly revised from 101.30) in April. According to additional information in the survey report, consumer inflation expectations for the coming year decreased slightly from 6.2% in April to 6.1% in May. In addition, the May Dallas Fed Manufacturing Business Index fell to -29.1 from -23.4, which was below market expectations of -19.6.

However, it should be noted that Thomas Barkin, president of the Richmond Fed, stated that he is seeing evidence that demand is being slowed down by interest rate increases. However, softer US data gave the risk-off mood a floor as US Republicans like Chip Roy and Ralph Norman demonstrated their willingness to reject the US debt ceiling agreement elsewhere. In this context, Wall Street ended with a mixed performance, but US Treasury bond yields continued to be under pressure. Although the DXY is likely to continue to be under pressure before the important data or events, a favourable outcome of the Senate’s vote on the steps to prevent a US default, which is very likely, can keep the dollar buyers in control. A positive surprise from the US JOLTS Job Openings for April, which are also predicted to decline, could reinforce the hawkish Fed bets and revive the US Dollar bulls. However, it is important to note that any definite rejections from the US Congress will not be ignored.

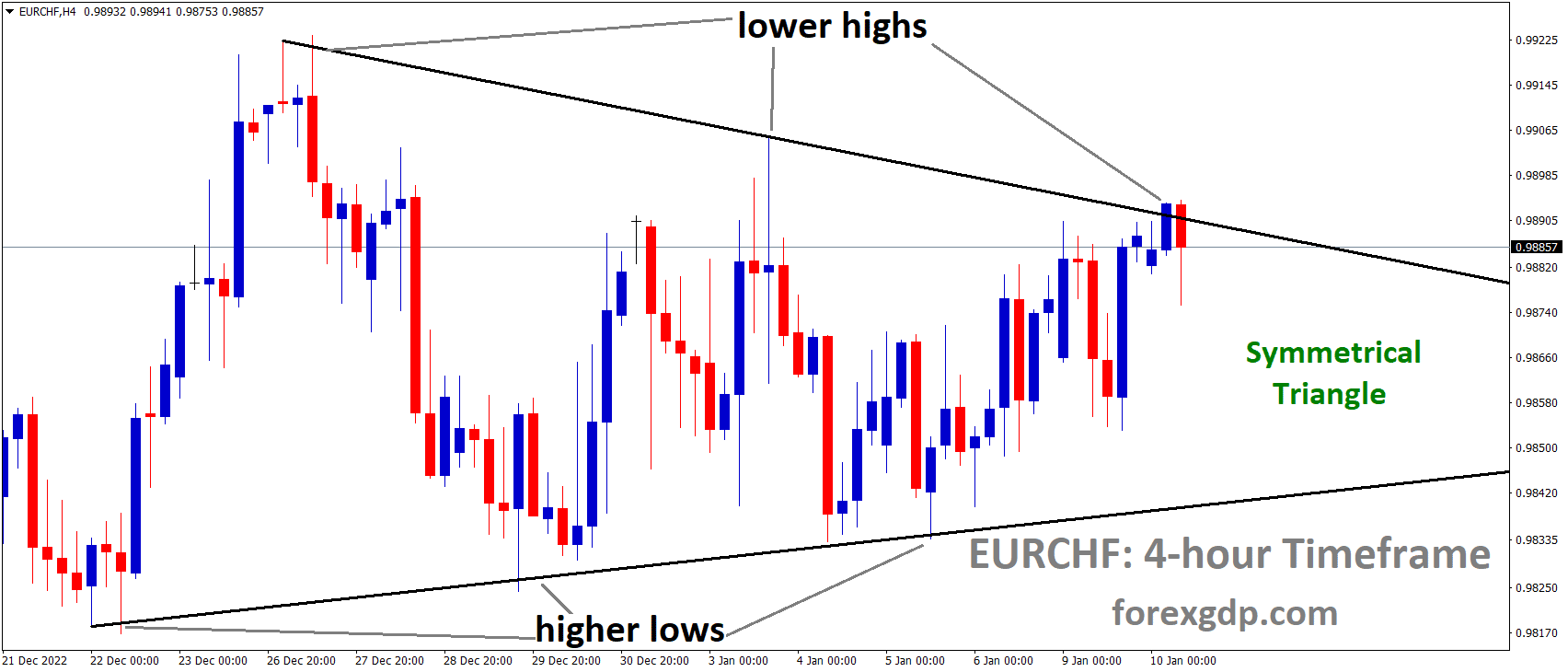

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Inflation in France is slightly declining, according to recent CPI data, GDP growth for the quarter came in at 0.20%, and monthly CPI data came in at 0.10% compared to the forecasted 030%. Maintaining 0.10% economic growth in 2023 and using taxation measures for businesses that can not contribute to bringing down food price inflation may be necessary.

French Finance Minister Bruno Le Maire stated that inflation is going down, and is actually going down quite strongly,” following the release of the French growth and inflation data. Keep the 1.0% economic growth prediction for 2023. If businesses do not contribute enough to help reduce the inflation of food prices, taxation measures may be used. The first quarter’s final Gross Domestic Product for France was confirmed at 0.2% QoQ. The nation’s consumer price index, meanwhile, experienced a 0.1% monthly decline in May. A 0.3% increase in the reported period was anticipated by the consensus forecast.

EURNZD Analysis

EURNZD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Due to China’s Manufacturing PMI data coming in lower than expected today 48.8 printer versus 49.2 expected, the New Zealand Dollar is weakening in the markets. Generally, a manufacturing sector gauge reading above 50 indicates healthy activity.

Following the release of mixed China’s official PMI data, the NZD has fallen. The Manufacturing PMI was reported by China’s National Bureau of Statistics at 48.8, which was less than the estimates of 49.4 and the previous release of 49.2. While the Non-Manufacturing PMI increased from the consensus 50.7 to 54.5, it still lagged behind the previous reading of 56.4Before the May Caixin Manufacturing PMI data are released, the New Zealand Dollar will continue to trade. The consensus estimate places the economic data at 49.5. It is important to remember that New Zealand is one of China’s top trading partners, and a stagnant performance of China’s factories could have an effect on the New Zealand Dollar.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The business sentiment index and the inflation forecast for the month of May are displayed by Lloyds Bank. The Lloyds Bank Barometer experienced its first decline in May, dropping to 28% from 33% in April. However, Reuters said that this is an average indicator and nothing to worry about. Due to the higher wage prices and interest rates currently in effect in the UK, inflation is on the rise.

Going into Wednesday’s London opening, the GBPUSD is holding onto modest losses as it continues the early Asian session pullback from a one-week high and breaks a three-day uptrend near 1.2390. However, recent gains in the Cable pair may be related to the US Dollar’s broad recovery, negative worries about the UK’s fundamentals, and hawkish Federal Reserve (Fed) bets. Additionally, the Pound Sterling bears are able to maintain control due to concerns about an impending US default and mixed US data. The previous day, the Lloyds Bank released its business sentiment index and May inflation signals as part of its monthly releases. The Lloyds Bank Business Barometer fell to 28% in May from 33% in April, its first decline since February, but in line with the survey’s long-term average, according to Reuters. Hann-Ju Ho, senior economist at Lloyds Bank, is also quoted in the news as saying that the economic environment continues to be difficult, made worse by persistent inflation and increased wage pressures. The US Dollar Index, on the other hand, increases bids to around 104.25 after breaking a six-day uptrend close to its highest levels in ten weeks. Following the US dollar’s most recent gains, the market’s worries about the upcoming US default and the dismal May China activity data receive significant attention. Anxiety ahead of important data or events and the US Republicans’ demonstrated willingness to vote against the deal to prevent the debt-ceiling expiration may also be weighing on sentiment and the price of the GBPUSD.

Even though recent US data have been mixed, it is important to note that the market’s relative hawkish bias towards the Federal Reserve versus the Bank of England weighs on the Pound Sterling pair. The Consumer Confidence Index for the US Conference Board fell slightly to 102.30 for May from an earlier reading of 103.70 for April which had been upwardly revised. According to additional information in the survey report, consumer inflation expectations for the coming year decreased slightly from 6.2% in April to 6.1% in May. In addition, the May Dallas Fed Manufacturing Business Index fell to -29.1 from -23.4, which was below market expectations of -19.6. The mildly offered S&P500 Futures and the US Treasury bond yields, which reflect the market’s current caution, may give the GBP/USD bears reason for optimism before the US House of Representatives votes on the debt ceiling agreement. The US JOLTS Job Openings for April expected at 9.375M versus 9.59M previously as well as the Chicago Purchasing Managers’ Index for May likely to decline to 47.0 from 48.6 are other important indicators to keep an eye on.

CADCHF Analysis

CADCHF is moving in an Ascending Channel and the market has reached the higher high area of the channel.

Due to the slowdown in China’s economy and the imminent completion of this week’s US debt agreement, oil prices have fallen sharply. This week’s CAD GDP data is scheduled, and if it is stronger than anticipated, it may strengthen the Canadian Dollar relative to other currencies. Canadian Q1 current account deficit was -6.17 billion, slightly better than expected (-9.35 billion) and the previous reading (-8.05 billion).

Crude Oil Analysis

Crude Oil price has broken the Ascending channel in downside.

As it prepares for the important growth data from Canada, the USDCAD retreats to 1.3600 in the early Asian session on Wednesday, reversing the previous day’s rebound from 1.3567 and easing from 1.3613. Anxiety before the US Senate’s vote on the debt ceiling deal may also be a problem for the Loonie pair. However, the quote is affected by a decline in the price of WTI crude oil. Major attention is paid to the month-end consolidation and the cautious mood before the most important data or events. The mixed US data may also pose a threat to the dollar. As a result, on Tuesday, the US Dollar Index reached its highest levels since mid-March before breaking a five-day uptrend and posting the largest daily loss since April 19. It ended the North American trading session around 104.05. As a result of concerns about the US policymakers’ capacity to avert the impending default, WTI crude oil, on the other hand, fell to its lowest levels in four weeks, falling more than 4.0% to record the biggest daily loss since May 2. In addition, expectations for increased oil production and US pressure to use the Strategic Petroleum Reserve put downward pressure on the price of black gold.

The Consumer Confidence Index for the US Conference Board fell slightly to 102.30 for May from an earlier reading of 103.70 for April (from 101.30), which had been upwardly revised. According to additional information in the survey report, consumer inflation expectations for the coming year decreased slightly from 6.2% in April to 6.1% in May. In addition, the US House Price Index increased 0.6% MoM in March compared to 0.2% expected and 0.7% in February (revised from 0.5%), while the S&P/Case-Shiller Home Price Indices decreased to -1.1% YoY in contrast to 0.4% in February and -1.6% in March. The Dallas Fed Manufacturing Business Index for May decreased even more, from -23.4 to -29.1, underperforming market expectations of -19.6. It should be noted that the Canadian Current Account deficit for the first quarter (Q1) decreased to $6.17 billion from the expected $9.35 billion and the previously reported $8.05 billion (revised), which puts downward pressure on the Loonie pair.

Wall Street closed mixed, reflecting the mood, but US Treasury bond yields remained under pressure as US Republicans like Chip Roy and Ralph Norman signalled their willingness to reject the US debt ceiling agreement. However, softer US data gave the risk-off feeling a foundation. Elsewhere Thomas Barkin, president of the Richmond Fed, stated that he is observing evidence that rising interest rates are reducing demand. Outside of the risk catalysts mentioned above, the US JOLTS Job Openings for April and Canada’s Gross Domestic Product for Q1 will be crucial for the Loonie pair to watch for clear directions. If Canadian growth exceeds pessimistic forecasts, the Loonie pair may experience new downside pressure.

AUDNZD Analysis

AUDNZD is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern.

Chinese Non-Manufacturing PMI came in at 54.5 vs. 55.5, and Manufacturing PMI came in at 48.8 vs. 49.5 expected. At the end of April, the monthly CPI indicator for the Australian economy ticked up to 6.8% YoY, exceeding the previous reading’s 6.4% and 6.3% predictions. Investors do not anticipate a change in rates at the RBA meeting on next Tuesday.

After the Chinese PMI fell short of expectations, the Australian Dollar fell to a six-month low under 65 cents. The information seems to have fueled the perception that the second-largest economy in the world is having trouble rekindling growth as it emerges from the pandemic era. Chinese manufacturing PMI for May came in at 48.8 versus the expected 49.5, and the non-manufacturing component registered at 54.5 versus the anticipated 55.2. As a result, the composite PMI reading decreased from 54.4 to 52.9. A survey of 3,000 manufacturers across China, mostly large businesses, produced the China PMI indices. Since it is a diffusion index, a reading above 50 is considered to be favourable for the Middle Kingdom’s economic outlook.

Australian private sector credit for April showed growth of 0.6% month-over-month versus the 0.3% anticipated at the same time as the release of the China PMI. Due to this, the annual read decreased from 6.8% to 6.6% over the previous year. The Australian Bureau of Statistics’ (ABS) monthly CPI gauge increased slightly to 6.8% year-on-year at the end of April, exceeding the previous predictions of 6.4% and 6.3%. The data released today follows yesterday’s disappointing report on Australian building approvals for April, which showed a decline of -8.1% month-over-month rather than the anticipated 2% increase.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

Swiss retail sales data hit a record low of -3.7% YoY, which is significantly lower than the previous reading of -1.9% and the current reading of -1.4%. Swiss GDP Q1 increased by 0.30% from the previous quarter. After lower retail sales data were printed, the Swiss Franc declined against other currency pairs.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/