XAUUSD Retreats on Fed Rate Cut Doubts Sparked by Job Market Strength

When gold prices take a hit, investors pay close attention—and this week was one of those times. If you’ve been wondering what’s been going on with gold lately and why it’s on track for a significant weekly loss, you’re not alone. Let’s break down everything that happened, why it matters, and what traders are looking out for next.

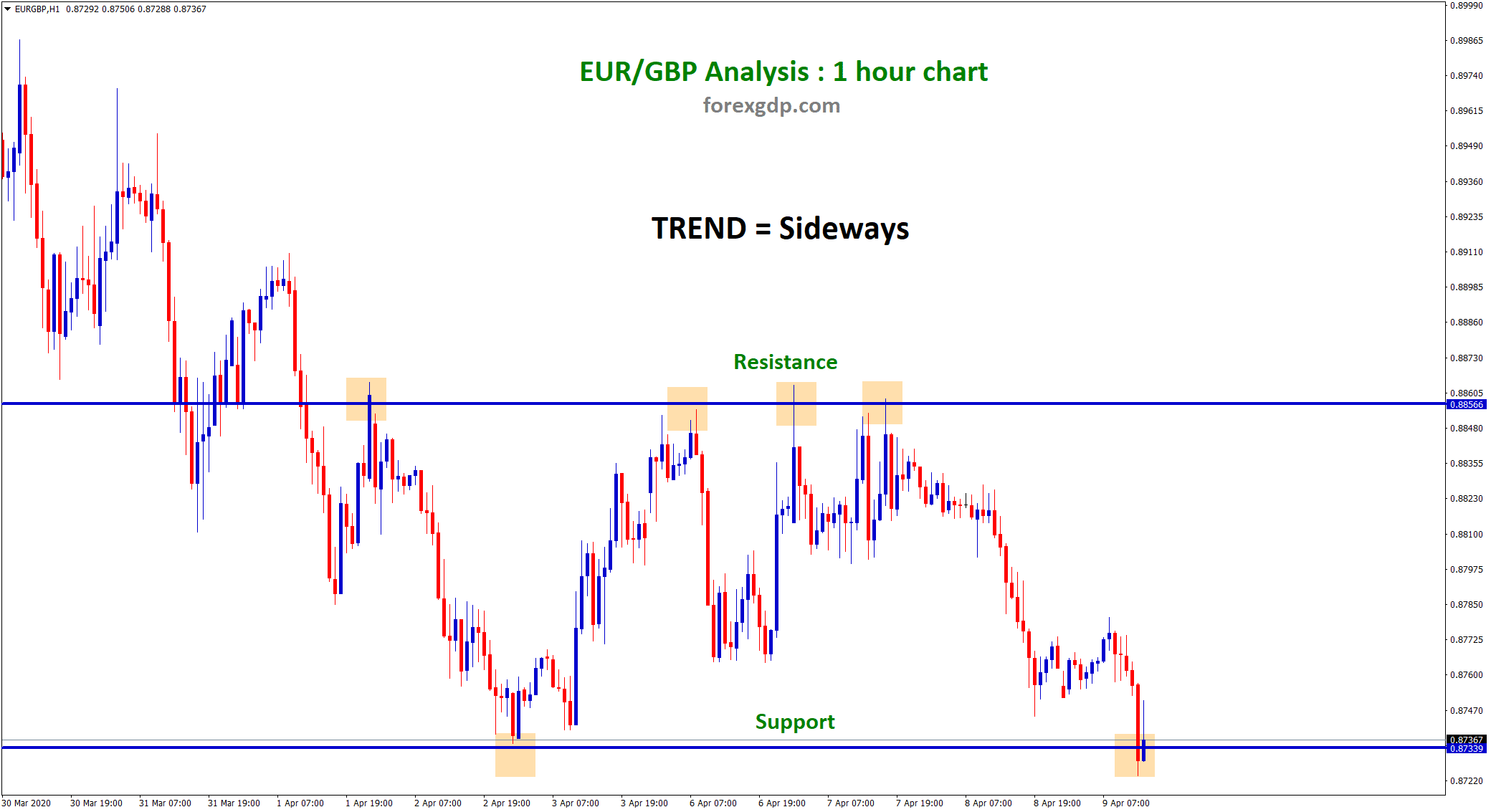

XAUUSD is moving in a downtrend channel, and the market has rebounded from the lower low area of the channel

Gold Takes a Hit: What’s Behind the Drop?

This week, gold prices slid more than 2.5%, and the reason isn’t just one thing—it’s a mix of better-than-expected economic data, changes in investor expectations about interest rates, and a growing sense of optimism in global markets.

Strong U.S. Jobs Report Shakes Things Up

One of the biggest drivers behind the drop in gold was the U.S. employment report for April. The Nonfarm Payrolls (NFP) data beat expectations, showing the U.S. economy added 177,000 jobs in April. That’s higher than what many economists had predicted.

What does that mean for gold? Well, when the job market looks strong, it signals that the U.S. economy is doing just fine. In turn, investors start thinking the Federal Reserve might not need to cut interest rates as much or as soon as previously hoped. And when interest rates stay high or even climb, gold—which doesn’t earn any interest—becomes less attractive.

On top of that, the unemployment rate held steady at 4.2%. That may seem like a small thing, but it added more weight to the idea that the economy isn’t in any trouble just yet. Less trouble means less urgency for the Fed to cut rates, and again, that’s not great news for gold.

Shifting Fed Expectations and Market Sentiment

Rate Cuts? Maybe Not So Fast

Until recently, many traders were betting that the Federal Reserve would cut interest rates multiple times this year. But after this latest batch of strong job numbers, those expectations have started to fade.

Investors now see fewer rate cuts ahead, and that shift has triggered some profit-taking in the gold market. Traders who were riding the wave of gold’s earlier rise are now stepping back, locking in their gains while they can.

Rising Treasury Yields Add More Pressure

Another key factor? U.S. Treasury yields shot up this week. The 10-year Treasury yield rose significantly, a sign that bond traders also believe the Fed might hold off on rate cuts. Higher yields typically pull attention away from gold, as investors look for better returns elsewhere.

It’s like this: if you can get a solid return from a safe investment like U.S. government bonds, gold has a harder time standing out.

Global Trade Optimism Dampens Gold’s Appeal

China and the U.S. Open the Door to Talks

Here’s another twist. China recently signaled that the U.S. is open to restarting trade negotiations. That’s big news. Any signs that two of the world’s biggest economies are willing to talk instead of fight over tariffs and trade rules helps calm the markets.

And when markets are calm, people are less likely to run to gold for safety. Gold is often seen as a “safe-haven” asset—something to hold when times get uncertain. But with global tensions cooling off, investors felt more confident putting their money elsewhere.

Risk-On Mood Returns

All of these pieces together created what you might call a “risk-on” environment this week. Investors were more willing to take chances, move money into stocks, and explore other opportunities. That’s generally bad news for gold, which thrives when people are nervous.

XAUUSD has broken the Ascending channel on the upside

So, this week’s decline wasn’t just about one report or one headline. It was the result of a broader change in mood across the financial world.

What’s Coming Next for Gold Traders?

With this week’s action behind us, all eyes now turn to the Federal Reserve’s upcoming policy meeting. While the Fed isn’t expected to raise or lower rates right now, everyone will be watching closely for clues about what might happen next.

Will the Fed hint at fewer cuts? Will they acknowledge the strong job market and growing stability? Any signals they give could move the gold market again.

For now, it seems like the market is adjusting to the idea that aggressive rate cuts may not be on the table. That could keep pressure on gold, at least in the short term.

Wrapping It All Up

Gold had a tough week. A stronger-than-expected U.S. jobs report, steady unemployment, and renewed hopes for U.S.-China trade talks all combined to weigh on the precious metal. As investors dialed back their expectations for interest rate cuts, gold lost some of its shine.

But this isn’t the end of the road for gold—not by a long shot. Its role as a store of value and hedge against uncertainty is far from over. Still, in a world where economic numbers are strong and investors feel good about taking risks, gold may face some headwinds.

If you’re following gold, the next few weeks could be very telling. Keep an eye on the Fed, global trade talks, and the overall tone of the market. Because when sentiment shifts, gold often moves with it.

EURUSD Jumps as Euro Inflation Heats Up and US Labor Market Holds Steady

The EUR/USD currency pair has seen some notable momentum lately—and it’s got traders, analysts, and everyday market watchers talking. But let’s skip the complex charts and technical jargon. Instead, let’s break down in simple terms what’s really moving this popular currency duo and why it’s catching so much attention right now.

Over the past few days, the euro has gained some solid ground against the US dollar. The main reason? A combination of strong economic data from Europe and some mixed signals coming from the United States. And when we say “mixed,” we’re talking about a blend of politics, inflation concerns, interest rate debates, and global trade dynamics.

US Economic Updates: Positive Job Growth, But Doubts Remain

Let’s start with the latest employment report from the US—what’s called the Nonfarm Payrolls (NFP). This report tracks how many new jobs were created over the past month, and it’s always a big deal because it gives insight into the health of the economy.

In April, the US added 177,000 new jobs. That’s a pretty solid number—especially since it beat the estimate of 130,000. It’s a signal that companies are still hiring and that people are still finding work, despite all the global uncertainty.

EURUSD is moving in an uptrend channel, and the market has reached the higher low area of the channel

However, there’s a bit of a twist here. Even though the job numbers were good, they weren’t quite as strong as they were the previous month, which had already been revised lower. On top of that, the unemployment rate stayed the same, and wage growth was slower than expected. Basically, people are getting hired, but they’re not necessarily earning a lot more.

So, what’s the catch? While job growth typically supports a strong dollar, these mixed signals about wages and inflation are making investors second-guess how aggressive the Federal Reserve (America’s central bank) will be with interest rate changes moving forward.

Why Trump’s Comments Shook the Dollar

Another key factor that’s influenced the dollar’s weakness is recent commentary from former US President Donald Trump. Shortly after the jobs report came out, Trump took to social media to share his views—and let’s just say, they stirred things up.

He talked about falling gas prices, cheaper groceries, and overall lower costs for American consumers. His main point? Inflation isn’t a big concern right now, and therefore, the Fed should lower interest rates.

Now, when a former president with strong influence makes such bold claims, it has an impact. Investors pay attention, and market reactions often follow. Trump’s remarks fueled speculation that there could be more pressure on the Fed to ease up on rates sooner rather than later, especially if inflation really is cooling off.

But not everyone agrees with this take. Some investors think the Fed might keep rates where they are for now—especially after seeing the better-than-expected jobs report. In fact, predictions for a June rate cut have actually dropped after the latest data came out.

The Eurozone Isn’t Sitting Still Either

While all this was going on in the US, some positive news was coming out of Europe too. A key report called the Harmonized Index of Consumer Prices (HICP) showed that inflation in the Eurozone was rising faster than expected in April.

This matters because inflation is closely tied to central bank policy. When prices are rising more quickly, central banks are more likely to keep interest rates steady or raise them to cool things down. So, the hot inflation data gave a little boost to the euro, as it made it less likely that the European Central Bank (ECB) would rush into cutting rates.

Even though the ECB is still concerned about the overall economic outlook—especially with global trade tensions still a factor—this inflation surprise added some short-term optimism to the European currency.

What about the ECB’s next move? Traders are currently expecting a modest rate cut in the coming months, but officials like Finland’s Olli Rehn have been clear: they’re open to all options, including rate cuts, if necessary. However, this latest data might cause them to pause and reconsider.

Trade Tensions and Global Politics: Still a Big Factor

Now, let’s not forget the broader backdrop here—ongoing trade relationships, particularly between the US and China. There have been some recent signs that things might be cooling off. China has indicated it’s open to restarting trade talks, and Trump himself has said he’s confident a deal can be made—but on America’s terms.

These kinds of political shifts influence currencies, especially the dollar. If the US and China manage to make peace on trade, that could help the global economy overall. But until there’s a solid agreement in place, markets will remain sensitive to every comment and development.

Add to that the potential for new trade deals between the US and countries like Japan, South Korea, and India—and you’ve got a lot of moving parts influencing how currencies behave.

Wage Growth: A Silent Influence

Another important (but often overlooked) aspect is wage growth in the US. The recent data showed only a small uptick in average hourly earnings—0.2% over the month, which is a bit slower than what many economists were hoping for.

Year-over-year, wage growth hit 3.8%, slightly below expectations. While this might not sound like a huge miss, it still matters. Slower wage growth can be a signal that inflation will stay tame, giving the Fed one more reason not to raise rates aggressively.

And remember—interest rates play a huge role in currency strength. Lower rates tend to weaken a currency, while higher rates support it. So, weaker wage growth can indirectly put downward pressure on the dollar, as it reduces the likelihood of future rate hikes.

Final Thoughts: What’s Driving the Momentum Now

At the end of the day, the rise in the euro and the fall of the US dollar is being driven by a mix of factors. Strong inflation data in the Eurozone, political pressure on the Federal Reserve in the US, and mixed signals from American job and wage data are all combining to tilt the scales.

We’re in a time where markets are highly sensitive to both economic releases and political developments. That means even a single comment—from a central bank official or a political leader—can move things dramatically.

If you’re watching the currency markets, it’s a reminder that there’s more to the story than just numbers. Sentiment, expectations, and confidence all play huge roles in shaping how these currencies perform.

The EUR/USD pair may continue to see swings based on how the Federal Reserve and the ECB respond to their respective economic landscapes. Whether you’re a trader, an investor, or just curious, keeping an eye on both sides of the Atlantic will help you understand where things might be headed next.

GBPUSD Pushes Higher with Fed Caution Looming Despite Strong US Employment Figures

Let’s start with the big picture. The United States added 177,000 jobs in April. That’s more than experts were predicting—but still a bit lower than March, when the country added 185,000 jobs. These numbers are important because they give us a sense of how strong the job market is in the US, and they influence how confident people feel about the economy.

GBPUSD is moving in an uptrend channel, and the market has reached the higher low area of the channel

Even though job growth was solid, the reaction in the financial world was a bit muted. The US Dollar didn’t strengthen as much as one might expect. Why? It’s all about what the market expected and how those expectations shape reactions. Since the actual job gain didn’t top the March figure and because the unemployment rate stayed at 4.2%, there’s still some uncertainty about how aggressively the US central bank—the Federal Reserve—will act.

Right after the numbers came out, former President Donald Trump jumped on his social platform to urge the Fed to cut interest rates. While political pressure like this doesn’t directly change policy, it does stir conversation.

For now, analysts believe the Federal Reserve might wait until July before deciding to lower rates. That delay could keep markets guessing, especially since job data is only one part of the puzzle.

Pound on the Rise: First Rally in Days

While the Dollar showed some hesitation, the British Pound had a different story. After several days of sliding down, it finally picked up again. This marked its first upward move in the past four sessions, bouncing back from the weekly low against the US Dollar.

But why did the Pound go up, especially with the US showing positive job data?

It turns out, market moods have been shifting in favor of taking more risks, especially with trade tensions between the US and China showing signs of cooling. When global investors feel more comfortable taking risks, they tend to move money out of the so-called “safe haven” assets like the US Dollar, and into other currencies, including the Pound.

This change in sentiment gave the GBP/USD pair a push upward, even though the UK has its own issues.

UK Manufacturing Shows Strain: Another Weak PMI

Back in the UK, there’s still trouble brewing in the manufacturing sector. The latest data from the S&P Global Manufacturing Purchasing Managers’ Index (PMI) shows contraction for the seventh month in a row. That’s a long streak of weakness.

These numbers reflect how tariffs and trade challenges are dragging on the UK’s factory output. It’s not just a temporary dip—it’s part of a longer trend of struggles in the sector.

Because of that, most analysts now believe the Bank of England will cut interest rates by 0.25% at its next meeting. This move would be aimed at supporting the economy by making borrowing cheaper and encouraging spending and investment.

Why It Matters: A rate cut in the UK while the US holds steady could narrow the interest rate gap between the two countries. This usually favors the currency with the higher rate, which in this case could still be the US Dollar. So even though the Pound is rising right now, it may face headwinds ahead if the expected UK rate cut plays out.

Fed Under Pressure but Likely to Hold for Now

Trump Calls for Rate Cuts Again

The Federal Reserve is at the center of attention, as usual. Even with good economic news like job gains and a rise in factory orders (up 4.3% for March), there’s still political and market pressure for the Fed to act.

Donald Trump’s public call for rate cuts adds to the mix, although the Fed is expected to move only based on actual economic data, not political influence. That said, when a former president speaks up, it grabs headlines and can influence market sentiment.

Right now, the Fed is expected to wait until July before considering rate changes. A lot will depend on how inflation behaves in the next couple of months and whether job growth continues at a healthy pace.

Factory Orders Show a Boost

Speaking of healthy signs, US factory orders showed a big jump in March, rising 4.3% from the previous month. That’s a strong sign that business demand is still ticking up—even though it came in just under the forecasted 4.5%.

This kind of data supports the idea that the US economy is still in good shape, even if it’s not booming. It gives the Fed one more reason to wait before pulling the trigger on any rate cuts.

Pound’s Rally Might Be Short-Lived

So, where does this leave the GBP/USD pair? Right now, the Pound is benefiting from a mix of improving global risk appetite and a softening Dollar. But the tide could turn again quickly.

If the Bank of England cuts rates next week while the Fed holds off until July, the interest rate advantage shifts toward the US. That would make the Dollar more attractive again, possibly putting downward pressure on the Pound.

And with UK manufacturing still showing signs of strain, there’s a ceiling on how much the Pound can rally unless the economic picture at home brightens.

Final Thoughts: A Delicate Dance Between Central Banks and Markets

To sum it up, both the US and UK economies are sending mixed signals. The US job market and factory sector are holding up, but not booming. The UK is dealing with persistent manufacturing weakness but may get some short-term boosts from global market sentiment.

The GBP/USD pair is caught in this delicate balance. Rate expectations, political comments, and global risk moods all play a role in pushing the currency in one direction or another.

For now, the Pound is enjoying a brief moment in the sun, but whether it lasts depends on what the Bank of England and the Federal Reserve decide in the weeks ahead. Investors will be watching closely—because in today’s market, even a single sentence from a central bank can move everything.

USDJPY Drops as U.S. Currency Wobbles and Japan Pushes Back on Tariffs

After pushing higher during the week, the USD/JPY currency pair is now slowing down. It’s hovering near the 145.00 mark, giving up some of its recent gains. The reason behind this pullback? It’s mostly tied to the US Dollar losing steam—thanks to a mix of economic data that’s left traders and investors scratching their heads.

Even though the US Nonfarm Payrolls (NFP) report came in stronger than expected, with 177,000 new jobs added in April, the rest of the economic landscape is a little shaky. Other key data, like the ISM manufacturing report and the US GDP numbers, have raised questions about how strong the US economy really is right now.

USDJPY is moving in a Descending Triangle, and the market has rebounded from the support area of the pattern

That uncertainty has traders once again betting that the Federal Reserve might cut interest rates sooner rather than later. So even though one piece of data looks good, others are pointing in the opposite direction—and that’s causing the USD to wobble.

A Closer Look at the U.S. Economy: Mixed Signals Galore

Jobs Are Growing, But Is That the Whole Story?

The U.S. economy added 177,000 jobs in April, beating market forecasts. At first glance, this looks like solid progress. But dig a little deeper, and the picture isn’t as rosy. The previous month’s job numbers were revised down significantly, which suggests the job market might not be as strong as the headline figures suggest.

The unemployment rate remained unchanged at 4.2%, which is still relatively healthy. However, jobless claims are creeping up, and some economists are concerned that we’re starting to see early signs of a slowdown in hiring. Wage growth also stayed flat at 3.8% year-on-year—steady, but not exciting.

These mixed signals are exactly why traders are now pricing in several interest rate cuts by the Federal Reserve before the end of the year. Right now, the swaps market suggests we could see up to four rate cuts in 2025, with the first possibly happening as early as June. That’s a big shift from where expectations were just a few months ago.

GDP Drops Into Negative Territory

Another red flag for the U.S. economy was the Q1 GDP figure. The economy shrank by 0.3% in the first quarter of the year. That’s a clear signal that growth is slowing down. Combined with weaker manufacturing data and cautious consumer spending, it paints a picture of an economy that’s cooling off.

For the USD, this kind of news typically isn’t great. If the Fed is seen as likely to cut rates, it reduces the appeal of the Dollar compared to other currencies that may offer better returns.

What’s Going on in Japan?

While the U.S. is battling economic uncertainty, Japan has its own set of issues to deal with. The Japanese government and the Bank of Japan (BoJ) continue to support an extremely loose monetary policy, and that’s not expected to change anytime soon.

Japan’s Labor Market: Strong but Not Perfect

Japan’s labor market remains relatively tight, but even here, cracks are beginning to show. The latest data revealed a slight uptick in the unemployment rate to 2.5%. That’s still low compared to many developed nations, but it’s a change from Japan’s typically ultra-stable employment scene.

Meanwhile, the job-to-applicant ratio—a key measure of labor market health—improved slightly. However, wage growth is still slowing down. That’s an important detail, because weak wage growth limits consumer spending, which in turn puts a damper on inflation—something the BoJ has been struggling to boost for years.

Because of these factors, the BoJ is widely expected to continue its ultra-accommodative monetary policy through at least 2025. That means low interest rates, continued asset purchases, and a generally supportive environment for financial markets.

Japan Takes a Tougher Stance in Trade Talks

On the geopolitical side, Japan’s Finance Minister made headlines by hinting that Japan could use its holdings of U.S. Treasury securities as a bargaining chip in trade talks with the U.S. This is a big deal because Japan is one of the largest holders of U.S. debt. It shows that Japan may be ready to play hardball when it comes to tariffs and trade restrictions.

There are also murmurs about new trade negotiations between the U.S. and China, and possibly a reopening of tariff discussions. Japan appears eager to be part of that conversation and is pushing for a re-evaluation of tariffs on its exports to the U.S.

Market Mood: What Traders Are Watching

Right now, traders are weighing all of this conflicting information to figure out what comes next. On one side, a strong jobs report hints at economic resilience. On the other side, shrinking GDP and weakening factory data scream slowdown.

Add to that Japan’s steady stance on monetary policy and its new trade ambitions, and you’ve got a very complicated equation for the USD/JPY pair.

The U.S. Dollar is likely to remain under pressure if the market continues to believe that the Fed will start cutting rates soon. That’s because lower interest rates tend to make the Dollar less attractive to investors seeking higher yields. On the flip side, the Japanese Yen could strengthen if market volatility increases or if geopolitical tensions rise.

Investors should also keep an eye on global developments, including China’s trade policies and how other major central banks react to shifting economic conditions. These broader factors will continue to play a role in shaping currency movements in the weeks ahead.

Final Summary

The USD/JPY pair is facing a bit of a reality check. After climbing earlier in the week, it’s now losing momentum as traders reassess their expectations for interest rate cuts in the U.S. The economic data is sending mixed signals—jobs are up, but growth is down. That’s leading to some uncertainty in the markets and a pullback in the Dollar.

On the Japanese side, a stable but slightly weakening labor market and continued low interest rates make for a calm backdrop. But Japan is also becoming more vocal in international trade talks, which could influence future market sentiment.

As always, the currency market is influenced by a mix of economic data, policy expectations, and global events. Keeping an eye on these factors—and staying flexible—is the best way to navigate the current market landscape.

USDCHF Slides Lower as Greenback Weakens Despite Solid U.S. Jobs Report

The USD/CHF currency pair has been sliding, leaving many traders and investors scratching their heads. You’d think strong job data from the United States would strengthen the U.S. Dollar, right? But surprisingly, that hasn’t been the case.

USDCHF is moving in a box pattern, and the market has rebounded from the support area of the pattern

The U.S. Dollar has been falling, even though April’s Nonfarm Payrolls (NFP) data came in better than expected. This is where things get a little more interesting than your typical market reaction. Instead of gaining momentum, the Dollar lost some ground. And one of the key reasons behind this strange behavior lies in political pressure and upcoming economic data from Switzerland.

Let’s dive in and break down what’s going on, why it matters, and what we could expect in the coming days.

Stronger Job Numbers, But a Weaker Dollar? Here’s Why

Let’s talk about the NFP report. The U.S. economy added 177,000 new jobs in April, a decent increase and well above the forecast of 130,000. The unemployment rate stayed steady at 4.2%. On the surface, this sounds like good news for the Dollar.

But despite this, the U.S. Dollar has been under pressure. And the reason isn’t economic — it’s political.

Trump’s Influence on Interest Rate Expectations

Former President Donald Trump has been vocal lately about wanting lower interest rates. Through a post on Truth.Social, he pushed for the Federal Reserve to cut rates. He pointed out lower gasoline prices, declining grocery costs, falling mortgage rates, and a generally strong job market as reasons why the Fed should ease its monetary stance.

Now, here’s where it gets complicated. When someone as influential as Trump speaks out about interest rate policies — especially in such a public way — it can shake investor confidence. People begin to question whether the Fed can act independently or whether it’s facing pressure to make politically driven decisions. That uncertainty tends to weaken the U.S. Dollar, as investors may start to doubt its reliability as a safe haven.

This isn’t the first time Trump has criticized the Federal Reserve or its chair. He’s been doing it for years, but each time he does, the market pays attention. And this time, it’s no different.

Swiss Franc Holding Steady Ahead of Inflation Data

Now let’s shift our focus to the Swiss side of things.

The Swiss Franc (CHF) hasn’t been making big moves, but it’s been holding its ground. Why? Because everyone’s waiting for Switzerland’s Consumer Price Index (CPI) data for April. This inflation report, which is expected to show a 0.2% monthly increase, could set the tone for how the Swiss economy — and more importantly, its central bank — reacts going forward.

Switzerland is known for its stable economy and conservative monetary policy. If the CPI figures come in stronger than expected, it might hint that inflation is picking up. And that could mean the Swiss National Bank (SNB) may consider tighter policies down the road.

Investors love certainty and stability. When Switzerland delivers that — even in the form of small but predictable economic data — it tends to support the value of the Swiss Franc. That’s another reason the USD/CHF pair is dipping.

Why Traders Are Playing It Cautiously Right Now

Right now, the market feels uncertain. On one hand, you have a strong U.S. job market. On the other, you have political noise suggesting the Fed should cut rates, which doesn’t really match the economic reality.

Investors are caught in the middle. Do they believe the data? Or do they follow the political narrative that could lead to rate cuts and a weaker Dollar?

This kind of contradiction creates confusion, and that confusion often leads to cautious trading. People don’t like to make bold moves when the direction isn’t clear. As a result, many are moving to safer currencies, like the Swiss Franc, while they wait for more clarity.

What Could Happen Next?

All Eyes on Swiss CPI

Once the Swiss CPI data is released, we’ll likely get a better idea of how the Swiss National Bank might respond. If inflation picks up, the Franc could gain more strength, which would further push down the USD/CHF pair.

More Pressure on the Fed?

If political voices continue to pressure the Fed for rate cuts — even if the economic numbers don’t support it — we could see the U.S. Dollar continue to weaken. Investors may start pricing in lower interest rates sooner than expected.

Cautious Approach by Investors

Until the noise settles, many traders might avoid taking big positions in USD/CHF. Instead, they might wait for clearer guidance from central banks or additional economic indicators that show where things are truly headed.

Wrapping It Up: A Tale of Two Currencies

In the end, the fall in USD/CHF isn’t just about numbers — it’s about narratives. Even though the U.S. job market is holding up well, the U.S. Dollar is struggling due to political pressure and shifting expectations around interest rates. On the other hand, the Swiss Franc is benefiting from its usual role as a safe and stable currency, especially with inflation data around the corner.

So while the economic picture may look strong in the U.S., investor behavior is being shaped by something more complex — a mix of uncertainty, politics, and cautious optimism about what’s next.

If you’re watching this pair, it’s not just about the charts or the forecasts. It’s about reading between the lines and understanding what’s really driving sentiment on both sides of the currency battle.

USDCAD Retreats as Market Cheers Trade Progress, Dollar Loses Edge

When it comes to currency pairs, the USD/CAD is always an exciting one to watch. But recently, it’s been moving lower, and many traders and investors are wondering what’s behind the decline. Is it something temporary? Or is there a larger trend shaping up? Let’s break down what’s really happening and what you should keep in mind going forward.

USDCAD is moving in an uptrend channel, and the market has reached the higher low area of the channel

What’s Going On With USD/CAD Right Now?

The USD/CAD pair has been slipping in recent sessions, and it’s mostly due to a combination of weaker sentiment surrounding the US Dollar and a more optimistic global risk environment. Simply put, people are feeling a bit more confident about taking risks, which means they’re pulling away from the Dollar and leaning more into other assets, including the Canadian Dollar.

The backdrop for this move has a lot to do with how traders are reacting to economic data and expectations for future decisions from central banks. It’s not just about one number or one report—it’s about the bigger picture.

The Labor Market: Mixed Signals from the U.S.

One of the key pieces of information that shook things up was the latest US Nonfarm Payrolls (NFP) report. On the surface, it looked good. The US added 177,000 jobs in April, which beat forecasts and helped calm some of the bigger fears about a serious slowdown in the labor market.

But when you dig deeper, it’s a mixed bag.

-

Past job numbers from February and March were quietly revised downward by a total of 58,000 jobs.

-

The Unemployment Rate stayed flat at 4.2%, showing no real improvement.

-

Wages grew by 3.8% compared to last year, which sounds okay—but it actually came in a little softer than expected.

-

Initial jobless claims rose to 241,000, the highest since mid-February.

-

Even more concerning, continuing claims (people staying on unemployment) reached the highest levels since November 2021.

So, while hiring hasn’t completely stopped, there are hints that things might be cooling off. That’s enough to keep hopes alive that the Federal Reserve could decide to cut interest rates soon—possibly as early as July.

Manufacturing Slows Down: What the ISM Report Tells Us

Another important piece of the puzzle is the ISM Manufacturing PMI, which measures how the factory sector is doing. In April, it dropped again, sliding to 48.7 from 49.0 the previous month. That’s not a massive drop, but it’s part of a pattern of softening.

A few things stood out:

-

The production component of the index fell sharply to 44.0. That’s a clear sign that factory output is slowing.

-

While new orders and hiring showed slight improvement, it wasn’t enough to offset the broader weakness.

-

Interestingly, the price index rose to 69.8, the highest it’s been since mid-2022. That tells us that even though production is down, input costs are rising—which keeps inflation on the radar.

All of this feeds into how the Federal Reserve might see the situation: economic growth is fragile, inflation isn’t gone, and rate cuts could still be on the table if the data keeps weakening.

Why the Canadian Dollar Is Holding Its Ground

While the US is dealing with a flood of data and uncertainty, Canada’s situation looks a little more stable for now. There hasn’t been a lot of major economic news from Canada recently, but the Canadian Dollar (CAD) is still managing to find strength. Here’s why:

1. Global Trade Hopes Are Back

One major factor supporting the loonie (Canada’s currency nickname) is renewed optimism about global trade. There have been hints that China might be willing to re-engage in trade talks with the United States, and that’s boosting risk sentiment across the board. When markets feel optimistic, commodity-linked currencies like the CAD usually benefit.

2. Commodity Prices Are Stabilizing

Canada is a resource-rich country, so its currency often rises and falls with the price of things like oil and metals. Lately, those prices have been relatively steady, which adds some extra support for the loonie.

3. Calm Before the Data Storm

There haven’t been any major economic reports from Canada lately, which means there’s been less noise for traders to react to. But that won’t last long—Canada is set to release its own labor market numbers soon, and those could move the needle one way or another.

What Should You Take Away From All This?

If you’re keeping an eye on USD/CAD, here are a few key takeaways:

-

The US Dollar is currently under pressure because of growing hopes that the Fed might cut rates. Weak jobless claims and manufacturing data are feeding into that outlook.

-

At the same time, Canada’s currency is holding up well thanks to a stronger global risk mood, steady commodity prices, and the possibility of easing trade tensions.

-

All of this has combined to push the USD/CAD pair lower, and while short-term moves can always shift based on headlines, the bigger trend right now favors the Canadian side—at least until more data comes in.

Final Summary

The recent drop in USD/CAD isn’t just a fluke—it’s part of a broader shift in market sentiment. The US economy is showing signs of strain, especially in the labor and manufacturing sectors. That’s keeping the door open for possible rate cuts, which has taken the shine off the US Dollar. On the flip side, Canada may not be making headlines, but its currency is benefiting from risk-on behavior, stable commodities, and improved trade talk hopes.

If you’re trading or investing in this pair, it’s important to stay tuned to upcoming data—especially from Canada—as it could help confirm whether this downtrend continues or if a reversal is coming. Until then, it looks like the loonie has the upper hand.

USD Index Wavers as Traders Weigh Job Market Surprises

When we think of the US Dollar, we often expect it to rise on the back of strong economic data. But sometimes, even upbeat numbers can’t keep it afloat. That’s exactly what happened recently. Even though the US economy added more jobs than expected, the dollar didn’t get the boost many anticipated. In fact, it slipped further. Let’s dig into why that happened and what’s really going on behind the scenes.

USD Index market price is moving in a descending channel, and the market has reached the lower high area of the channel

Strong Jobs Report? Not the Full Story

You might have heard that the Nonfarm Payrolls (NFP) report came out better than expected. That’s true—April saw 177,000 new jobs, beating the forecast of 130,000. On the surface, that sounds great. But as always, the devil is in the details.

Revisions Take the Shine Off

The headline number may have looked good, but when you dig deeper, earlier job numbers were revised downward. February and March together saw 58,000 fewer jobs than previously reported. That’s like celebrating a small win while forgetting about a bigger loss. These revisions made many investors question whether the labor market is really as strong as it appears.

Wages and Participation Stay Flat

Another important figure in the report is the Average Hourly Earnings, which stayed flat at 3.8% growth year-over-year. While that’s not bad, it’s also not improving. In other words, workers aren’t seeing bigger paychecks, and wage growth seems to be hitting a wall. On top of that, the Labor Force Participation Rate only moved up slightly. These aren’t signs of a booming economy.

Rate Cut Expectations Are Still High

Even with stronger-than-expected job growth, the markets are still betting that the Federal Reserve will cut interest rates soon—possibly as early as June.

Why a Rate Cut Could Be Coming

You might be wondering: why would the Fed cut rates when jobs are growing? Here’s why:

-

GDP Shrinkage: The US economy contracted by 0.3% in the first quarter. That’s not a good sign. Most of the decline was due to rising imports and weaker domestic demand. It signals that while people may have jobs, they’re spending less—and businesses are feeling it.

-

Softening Ahead: April’s job report might be the last strong one we see for a while. Many analysts believe the labor market will start to cool off by June. That’s when we could see slower hiring and potentially higher unemployment.

-

Inflation Not Raging: With wages not rising much and inflation pressures easing, the Fed doesn’t have a strong reason to keep rates high. Lower rates could give the economy a much-needed boost.

China Trade Hopes Take Center Stage

Another big reason the dollar took a step back is global politics—specifically, trade relations with China.

Tariff Talks Resurface

Reports suggest that China is open to restarting tariff talks with the US. This development added pressure to the dollar. Why? Because improved trade relations could mean fewer disruptions to global markets. That often leads investors to move away from the “safe haven” of the US Dollar and into riskier assets. When the world feels less chaotic, the dollar tends to lose some of its appeal.

Ukraine Deal Grabs Attention, But Has Little Impact

The US also signed a minor deal with Ukraine involving minerals. While that made headlines, it didn’t really move the needle economically. It didn’t involve any major financial commitments or defense promises, so its market impact was limited.

Mixed Signals Are Keeping Traders on Edge

It’s no surprise that financial markets are acting cautiously. There’s a lot of conflicting data out there, and that uncertainty is keeping the dollar in check.

ADP Numbers Miss the Mark

Earlier in the week, we saw a weak jobs number from the ADP employment report, which tracks private payrolls. Only 62,000 new private sector jobs were added—the lowest in almost a year. This sent a message that maybe the broader labor market isn’t as strong as April’s NFP number suggested.

Market Mood: Cautious Optimism?

Investors are trying to balance hope and worry. On one hand, the US still seems relatively stable. On the other, the potential for slowing growth and aggressive rate cuts means the dollar might not be the stronghold it once was. The sentiment right now is more about caution than confidence.

What Does It All Mean for You?

Whether you’re an investor, a traveler, or someone who follows global economics, the US Dollar’s recent slide tells an important story. Economic data doesn’t always paint the full picture. It’s about the broader context—and right now, that context is full of uncertainty.

-

The job market is decent, but not booming.

-

Growth is slowing, and inflation isn’t a major threat.

-

The Fed is expected to ease up, which usually weakens the dollar.

-

Global developments, especially in trade, are shifting investor attention.

All of this means we could be entering a new phase for the dollar—one where strength isn’t guaranteed, and caution is the new normal.

Wrapping It Up: The Dollar’s Balancing Act

So, where does the US Dollar go from here? That depends on several things: the next batch of economic data, the Fed’s decision in June, and how the global trade environment evolves.

Right now, the dollar is walking a tightrope. It’s trying to balance solid job numbers with a softening economy, potential rate cuts, and shifting global dynamics. It’s not falling off just yet—but it’s definitely feeling the wobble.

AUD/USD Rallies on Renewed Trade Confidence and Unsteady US Economic Trends

Let’s talk about the US Dollar. Lately, it’s been going through a bit of a rough patch. The US Dollar Index (often referred to as DXY) recently dropped below a key psychological point. After attempting to stay strong, it couldn’t hold its ground and slipped. This drop suggests that the momentum which once carried the dollar is starting to fade.

Now, this doesn’t mean the dollar is crashing or anything dramatic like that. But it’s definitely a sign that investors are taking a step back, watching, and waiting. They’re not as confident as they were just a few weeks ago. Why? Well, a mix of economic data and changing global sentiment is causing this shift.

AUDUSD is moving in an uptrend channel, and the market has fallen higher high area of the channel

One of the big factors in this story is the job report that recently came out in the US. Known as the Nonfarm Payrolls (NFP) report, it’s a key indicator of how the job market is doing. In April, the numbers came in slightly above expectations—177,000 new jobs were added. Sounds good, right? But here’s the thing: it’s actually a bit lower than the pace we’ve been seeing in past months. So yes, more people are getting hired, but it’s happening at a slower rate.

This slower job growth adds to a broader theme that the US economy might be losing a bit of steam. Inflation seems to be under better control, and the labor market, while still strong, is cooling just a bit. These signs are making many believe that the US Federal Reserve might soon take a more relaxed approach—perhaps even cutting interest rates. That’s something traders are definitely watching closely.

Australian Dollar Picks Up Strength

On the other side of the globe, the Australian Dollar is having a better time. The Aussie, as traders like to call it, has been gaining traction. And a big reason for that is improving trade relations, particularly between the US and China.

Trade tensions between the two giants have been a thorn in the side of global markets for quite a while. But now, it looks like things might be warming up. Chinese officials have recently shown some willingness to sit down and talk trade again. That’s music to the ears of countries like Australia, which rely heavily on trade—especially with China.

When there’s hope that trade barriers might ease, currencies like the Aussie dollar tend to benefit. And that’s exactly what we’re seeing now. It’s not just about trade, either. When the US dollar weakens and global risk sentiment improves, investors tend to look at other currencies. The Australian Dollar, being tied closely to commodities and trade, becomes an attractive option.

So between a softer US Dollar and a more upbeat mood in global markets, the Aussie is rising.

Mixed Signals from US Data: What Does It All Mean?

Let’s get back to the US for a second. Aside from jobs, there’s other data that’s painting a mixed picture. Take wage growth, for instance. It’s staying steady at around 3.8%. That’s not too hot, not too cold. It shows that while people are getting paid more, it’s not happening at a rate that would trigger big inflation worries.

Then there’s the voice of the US Treasury. Treasury Secretary Bessent has recently made it known that they’re in favor of the Federal Reserve cutting interest rates. That’s a big deal. Rate cuts usually come when the economy needs a bit of a boost. And if the Fed actually moves in that direction, it could weaken the US Dollar even more.

This kind of softer monetary policy makes borrowing cheaper and can help businesses and consumers spend more. But it also tends to reduce the appeal of the dollar because lower interest rates mean lower returns for investors holding US assets.

How Global Sentiment Shapes Currencies

Let’s take a step back and look at the bigger picture. Currency markets aren’t just driven by numbers—they’re driven by sentiment. And right now, that sentiment is shifting. With the US economy showing signs of slowing and other parts of the world looking a bit brighter, the balance of power is tilting.

Optimism around trade deals, hints of lower interest rates in the US, and stable wage growth are all adding up to create an environment where currencies like the Australian Dollar can thrive.

And it’s not just about the Aussie. Other currencies tied to trade, like the New Zealand Dollar or Canadian Dollar, also tend to benefit when global trade looks healthier and the US dollar weakens.

Where Are We Headed Next?

So, what’s the takeaway from all this?

The US Dollar is currently facing some headwinds. Slower job growth and pressure for interest rate cuts are key themes. Meanwhile, the Australian Dollar is seeing a nice lift from improved trade relations and a more positive outlook on the global stage.

For traders, businesses, or anyone watching currency markets, these shifts matter. They affect everything from import/export pricing to travel costs to investment strategies. It’s a constantly moving puzzle where every piece—jobs data, global politics, inflation trends—plays a role.

Right now, it’s a moment of transition. The US is still a powerhouse, but it’s slowing. Countries like Australia are finding opportunities to shine, especially as trade concerns ease. The next few months will likely bring more updates from central banks, more economic data, and probably more surprises.

Final Summary

To wrap it all up, the currency market is going through a period of subtle but important change. The US Dollar, once seen as rock solid, is showing a few cracks thanks to cooling job numbers and growing chatter about interest rate cuts. Meanwhile, the Australian Dollar is benefiting from better global vibes, especially around trade.

It’s a story of shifting confidence, where the momentum is quietly leaning away from the US and giving space to others like Australia. And in the world of currency, those small shifts can make a big difference.

If you’re watching these markets, this is a time to stay informed, stay nimble, and keep an eye on the bigger picture. Because the winds of change are definitely starting to blow.