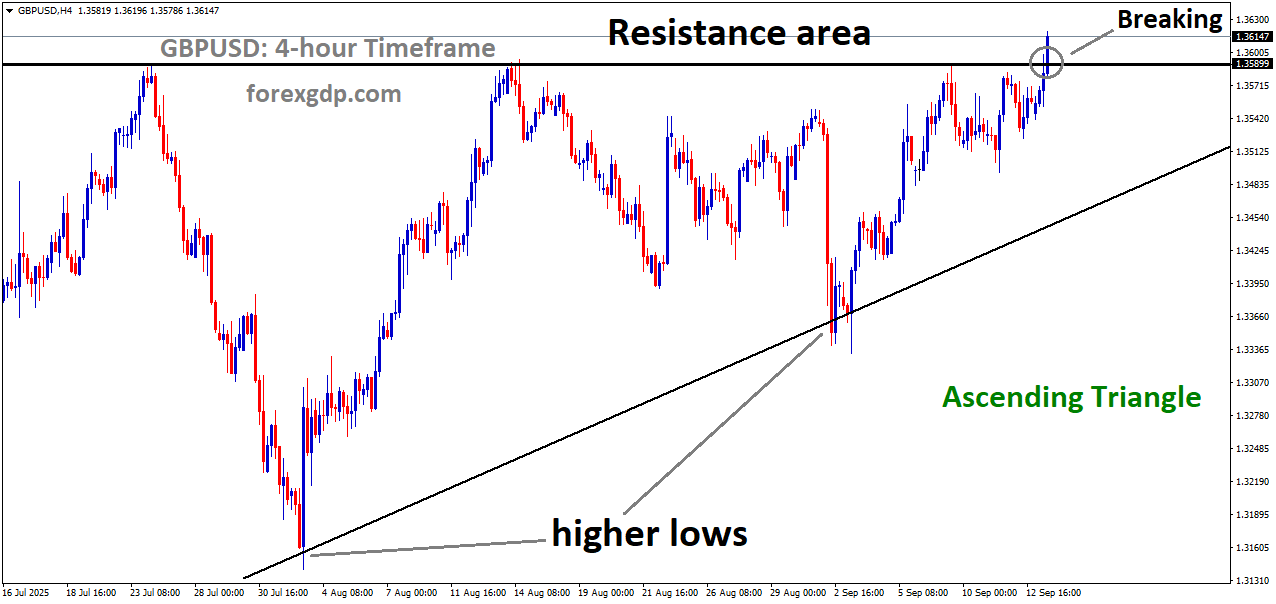

GBPUSD is breaking the resistance area of the Ascending Triangle pattern

GBPUSD Rises on Investor Anticipation of Fed and Bank of England Updates

When a new week kicks off with the Pound Sterling already climbing higher, you can bet there’s something interesting going on in the financial world. This week, all eyes are on two big players: the Federal Reserve (Fed) in the United States and the Bank of England (BoE). Both central banks are preparing to make monetary policy announcements, and these decisions are likely to shape not only currency movements but also how investors view the broader global economy.

So, let’s dive deeper into what’s happening with the Pound Sterling, why it’s making gains against the US Dollar, and what you should keep an eye on in the coming days.

Why the Pound Sterling Is Off to a Strong Start

The Pound Sterling (GBP) has been trading higher against the US Dollar (USD) at the beginning of the week. This momentum reflects a combination of factors tied to expectations about central bank policies, inflation, and labor market conditions.

The US Dollar is showing a cautious tone ahead of the Federal Reserve’s upcoming announcement. Investors are already pricing in the possibility of a rate cut, and when the Fed appears likely to ease policy, the Dollar usually softens. This gives the Pound room to climb higher.

On the other hand, the Bank of England is expected to take a different approach. Instead of cutting rates, they are seen as holding them steady. The reasoning here is tied to the UK’s stubbornly high inflation, which continues to trouble policymakers. If rates stay unchanged while US rates fall, the Pound naturally looks more attractive to investors.

In short, the current rise in GBP/USD is less about sudden strength in the Pound and more about shifting expectations for the Dollar and broader central bank decisions.

The Role of Inflation and Jobs in the UK

One of the biggest drivers behind the Bank of England’s cautious approach is inflation. The UK has been wrestling with high prices for a while now, and the latest expectations suggest headline inflation (measured by the Consumer Price Index, or CPI) may accelerate again. Current projections put CPI growth around 3.9%, the fastest pace in nearly two years.

This poses a challenge for the BoE. On one side, they don’t want to stifle the economy by keeping rates too high for too long. On the other, they can’t afford to ease policy when inflationary pressures are still running hot. It’s a tightrope act.

But inflation isn’t the only concern. The labor market is also in focus. Recent data points to the UK’s unemployment rate holding steady at about 4.7%. Wage growth has been slowing, though wages including bonuses are ticking slightly higher. The BoE has warned about potential weakness in the labor market, suggesting that while inflation remains a headache, risks to employment could grow.

For investors and policymakers alike, it’s a balancing act: how do you control inflation without tipping the jobs market into deeper trouble? That question will be at the heart of Thursday’s BoE announcement.

What’s Happening on the US Side?

While the UK is focused on inflation and labor trends, the US has its own economic puzzle. The Federal Reserve is widely expected to trim interest rates. According to market trackers, there’s an overwhelming chance of at least a small cut in the policy meeting this week.

Why? Much of it comes down to concerns about the American labor market. Despite earlier resilience, signs of slowing are becoming harder to ignore. The Fed has been signaling for months that its aggressive rate-hiking cycle is nearing an end, and now markets believe that easing is just around the corner.

At the same time, fresh data is about to land. US Retail Sales figures for August are due, and they’ll provide another look at consumer demand. Expectations are for slower growth compared to July. Since consumer spending is such a huge part of the American economy, weaker sales could reinforce the Fed’s decision to cut rates.

For the Dollar, this mix of a dovish Fed outlook and moderating data translates into weakness. And when the Dollar falters, currencies like the Pound often gain ground.

Why This Week Matters So Much

This isn’t just another typical trading week. The back-to-back announcements from the Fed and BoE, combined with key economic data from both the US and UK, create the perfect recipe for volatility. Currency traders, businesses with cross-border exposure, and even ordinary consumers paying attention to exchange rates will likely feel the effects.

For the UK, a hotter inflation print would pressure the BoE to keep its guard up, potentially delaying any talk of easing policy. But if the labor market continues to soften, the central bank may have to pivot sooner than expected.

For the US, confirmation of a rate cut could mark the beginning of a new policy cycle, one that shifts the global currency balance. With the Dollar potentially on the back foot, the Pound could maintain its recent upward push, at least in the short term.

Final Summary

The Pound Sterling’s rise at the start of this week is not just a random move—it’s rooted in expectations about what central banks in the UK and US are about to do. The Federal Reserve looks set to cut rates, weakening the Dollar, while the Bank of England is expected to hold firm due to persistent inflation concerns. Add in labor market risks on both sides of the Atlantic, and you’ve got a highly dynamic picture.

This week’s data releases—UK unemployment, wages, inflation, and US retail sales—will act as catalysts, pushing the Pound and Dollar in potentially sharp directions. For now, the Pound’s strength reflects a mix of opportunity and caution. Whether it can sustain those gains depends on how the numbers land and how central banks respond.

It’s a reminder that in the world of currencies, what happens in Washington and London doesn’t just stay there—it ripples across markets and into daily life worldwide.

EURUSD trades sideways with investor focus on France’s fiscal challenges

The global financial market often finds itself shifting gears when major announcements take place, and that’s exactly what happened after Fitch Ratings downgraded France’s sovereign debt. While the Euro tried to hold its ground, all eyes quickly turned to the upcoming Federal Reserve decision. Let’s break down what’s happening in a way that’s easy to follow.

EURUSD is moving in an uptrend channel, and the market has rebounded from the higher low area of the channel

Why France’s Downgrade Matters for the Euro

When Fitch, one of the top global rating agencies, cut France’s debt rating, it sent ripples through the market. The downgrade was tied to two major concerns:

-

Political Instability – With leadership changes and uncertainty surrounding the country’s government, investors are cautious about the long-term stability of France.

-

Rising Fiscal Deficit – The expectation that France’s debt will continue to climb made investors less confident about the country’s financial health.

Although the news was serious, the immediate impact on the Euro wasn’t as large as some might have expected. That’s because traders are paying closer attention to another major event – the Federal Reserve’s upcoming monetary policy decision.

All Eyes on the Fed’s Big Announcement

The US Dollar has been relatively quiet, moving in a narrow range, but that’s not surprising. Investors usually hold back before major events like a Federal Reserve meeting. Here’s why this week’s Fed decision is so important:

-

Interest Rate Policy – Markets are already expecting a rate cut, but the real focus is on what comes next. Will the Fed signal that more cuts are on the way?

-

Powell’s Speech – Whenever Fed Chair Jerome Powell speaks, investors listen closely. His tone and comments can either boost confidence in the US Dollar or cause it to weaken further.

This means that while the downgrade of France may have rattled some nerves, the bigger story is still unfolding in Washington.

The Role of the European Central Bank (ECB)

The ECB is also under the spotlight this week, though its schedule looks lighter compared to the Fed. Key appearances include:

-

President Christine Lagarde – Speaking at a panel in Paris, her comments may offer clues about how the ECB views France’s downgrade and whether it will influence broader European policy.

-

Isabel Schnabel – Her speech in Luxembourg could also shed light on the ECB’s next steps, particularly if market concerns about debt and growth spread beyond France.

While these events are not expected to be as market-moving as the Fed’s meeting, they still carry weight for the Euro’s near-term direction.

What’s Happening in the US Economy Right Now?

The American economy has been sending mixed signals, which is why the Fed’s decision feels even more critical. A few things stand out:

-

Weaker Consumer Sentiment – A recent survey from the University of Michigan showed that US consumers are feeling less optimistic, hitting a four-month low. Rising prices, partly influenced by tariffs, are making it harder for households to spend.

-

Soft Inflation Data – Both consumer and producer prices have come in lower than expected, reinforcing the case for the Fed to cut interest rates.

-

Retail Sales in Focus – With consumer confidence dropping, upcoming retail sales data will be closely watched. Strong sales could calm recession fears, while weak numbers might push the Fed toward a more cautious, supportive stance.

All of this creates a picture of an economy that’s slowing but not collapsing – a tricky balance for policymakers.

Bond Market Signals in Europe

Beyond currencies, bond markets are also reacting to recent events. France’s downgrade caused yields on its government bonds to rise, a sign that investors are demanding more return to hold what they now see as riskier debt.

-

10-Year Bonds – Yields climbed above 3.5%, showing a clear response to Fitch’s decision.

-

30-Year Bonds – These also rose, nearing 4.3%.

Even though these numbers aren’t at their highest levels from earlier in the year, they still highlight that investors are uneasy. For the Euro, this means bullish momentum may remain limited in the near term.

Why This Week Feels So Pivotal

Markets don’t like uncertainty, and this week has plenty of it. Between France’s political and fiscal challenges, softer US economic data, and the all-important Fed meeting, investors are holding back from making big moves until they get more clarity.

Think of it as a “wait-and-see” moment. Traders are willing to let the Euro and Dollar drift in narrow ranges for now, but once the Fed decision comes out, we’re likely to see stronger moves in one direction or the other.

Final Summary

In short, the Euro has been shaken but not broken by Fitch’s downgrade of France’s debt rating. While political instability and fiscal troubles in Europe are real concerns, they aren’t the main driver of the market right now. Instead, the spotlight is firmly on the US Federal Reserve and its upcoming decision.

If the Fed cuts rates and signals a more cautious outlook, the US Dollar could weaken, giving the Euro some breathing space. On the other hand, if Powell and his team strike a more balanced or even slightly hawkish tone, the Dollar might strengthen further.

For now, both the Euro and Dollar remain in a holding pattern, with traders waiting for the next big signal. This week is shaping up to be a decisive one, and the outcomes could set the tone for currency markets in the weeks ahead.

USDJPY Holds Steady While Traders Eye Key Central Bank Updates

The global currency market is always moving, but some weeks stand out as more important than others. Right now, the Japanese Yen (JPY) is in the spotlight as traders carefully watch both political changes in Japan and the upcoming decisions from major central banks. Let’s take a deep dive into what’s happening, why it matters, and what could come next for the Yen.

USDJPY is moving in a box pattern

A Month of Sideways Movement: Why the Yen Feels Stuck

Over the past month, the Japanese Yen has been trading within the same tight range. It hasn’t broken out strongly in either direction, leaving many traders feeling like the market is waiting for a trigger.

One big reason for this sideways movement is the uncertainty surrounding the Bank of Japan’s (BoJ) interest rate policy. For years, the BoJ has kept rates at ultra-low levels to encourage growth. Recently, though, hints of change have surfaced, but the exact timing of any hike remains unclear. Add in Japan’s current political shifts, and the atmosphere becomes even more unpredictable.

At the same time, global stock markets have been performing fairly well, and that usually reduces demand for the Yen, which is often seen as a safe-haven currency. When investors feel optimistic, they prefer riskier assets over safe ones like the JPY.

Central Bank Contrast: BoJ vs. The Fed

Perhaps the most interesting part of this story is the clear difference between the Bank of Japan and the US Federal Reserve (Fed).

-

BoJ’s Position: Many analysts believe the BoJ will eventually raise rates again this year. Japan’s economy has shown signs of improvement, with GDP growth getting revised upward, unemployment staying low, and wages rising. These are all signals that could push the BoJ toward more policy tightening.

-

Fed’s Position: On the other side of the Pacific, things look very different. Markets are increasingly convinced that the Fed is ready to cut interest rates soon. The US economy is slowing in certain areas, and inflation has shown signs of cooling. As a result, expectations for a rate cut are running high, and this has been pushing the US Dollar lower.

This contrast matters a lot. When one country is moving toward raising rates and another is moving toward cutting them, the currency of the rate-hiking country often gains strength. In this case, that means the Yen could benefit against the Dollar in the months ahead.

Politics, Trade, and Global Tensions Add Extra Layers

Japan’s Political Changes

Earlier this month, Japanese Prime Minister Shigeru Ishiba stepped down. Leadership changes like this always create questions about future government policies and their potential influence on economic decision-making. This uncertainty may encourage the BoJ to move more cautiously with rate hikes, since political stability often plays a role in financial policy.

Positive Economic Signs in Japan

At the same time, some news is working in favor of the Yen. Japan’s second-quarter GDP was revised upward, and the labor market remains strong. Real wages also grew for the first time in seven months. These developments support the case for the BoJ to move forward with policy normalization.

Global Geopolitics in Play

It’s not just Japan and the US driving the Yen’s moves. Global tensions are also shaping investor behavior:

-

The US recently pushed for new sanctions on Russia, following escalations involving Ukraine and NATO members.

-

In the Middle East, political voices are calling for stronger military positioning, with Iran urging Qatar to allow advanced missile deployments.

-

An upcoming summit of Arab-Islamic leaders in Doha also keeps geopolitical risks alive.

Whenever global tensions rise, safe-haven currencies like the Yen typically see increased demand. This adds another factor that could limit how much the Yen weakens, even if Japanese politics remain shaky.

Market Mood: Traders Waiting for the Big Decisions

Even though all these factors are in play, many traders are not making big moves just yet. That’s because two major events are happening this week:

-

The US Federal Reserve’s policy announcement (Wednesday): Markets want clarity on whether the Fed will confirm the expected rate cuts or hold steady for now.

-

The Bank of Japan’s policy update (Friday): Investors will be looking for any signals about when the next rate hike might come and how the BoJ views the latest economic data.

With both events happening so close together, it’s no surprise that investors are waiting on the sidelines. Everyone knows that whichever way these decisions go, they could set the tone for the Yen and the Dollar for weeks or even months ahead.

What This Means for the Japanese Yen Moving Forward

The Yen finds itself caught in the middle of different forces:

-

Political uncertainty in Japan makes it harder to predict central bank moves.

-

Stronger economic data points toward eventual BoJ tightening.

-

Global tensions increase demand for the Yen’s safe-haven appeal.

-

The Fed’s expected policy easing weakens the Dollar and indirectly supports the Yen.

All of this creates an environment where the Yen could see more strength in the medium term, especially if the BoJ sticks to its path of normalizing policy while the Fed begins cutting rates.

Final Summary

Right now, the Japanese Yen is at a crossroads. It has been stuck in a narrow range for over a month, but the upcoming central bank decisions could be the spark that sets it free. On one side, the BoJ faces political uncertainty but has improving economic data backing its case for higher rates. On the other side, the Fed looks ready to move toward rate cuts, which could weaken the US Dollar further.

At the same time, global geopolitical risks continue to support the Yen’s reputation as a safe-haven currency. Put all of this together, and the stage is set for some major moves once this week’s central bank updates are out.

If you’re keeping an eye on the currency market, now is the time to watch closely—because the Yen’s next big chapter might be just about to begin.

USDCAD under pressure as investors eye upcoming Fed and BoC moves

The currency markets are buzzing with anticipation this week as traders and investors focus on the upcoming policy meetings of the U.S. Federal Reserve and the Bank of Canada. The U.S. Dollar, while experiencing slight fluctuations, is holding within its recent range, and the Canadian Dollar is showing limited momentum ahead of these pivotal central bank announcements. Let’s take a closer look at what’s happening and why both currencies are under the spotlight.

USDCAD is breaking the higher low area of the uptrend channel

US Dollar Stays Cautious Amid Market Jitters

The U.S. Dollar began the week trading a bit lower but managed to remain within last week’s levels. This comes after Friday’s release of disappointing consumer sentiment data, which added pressure on the Greenback.

The University of Michigan’s Consumer Sentiment Index showed that American households are becoming increasingly cautious. Rising living costs and the ongoing impact of tariffs have weighed on confidence levels. The index fell to 55.4 in September, its weakest reading since May. This was well below both the August reading and analysts’ expectations, sending a clear signal that consumers are growing more uncertain about the economic outlook.

What stood out even more was the long-term inflation outlook, which has now increased for two consecutive months. While near-term inflation expectations remained steady, the longer-term rise suggests that households are concerned about persistent price pressures. For the Federal Reserve, this complicates things—it signals ongoing inflation worries but also highlights weak consumer confidence, a mix that makes policy decisions harder.

Why the Fed’s Next Move Matters So Much

Markets are heavily focused on the Fed’s upcoming meeting. Traders believe that the weaker consumer data strengthens the case for a dovish policy shift, meaning the central bank could soften its stance on interest rates.

If the Fed signals an easing cycle or hints at rate cuts, the Dollar could come under fresh selling pressure. The Greenback has been a safe-haven currency for much of this year, but investor appetite for holding it may fade if yields fall. On the other hand, if the Fed surprises markets with a more neutral or even slightly hawkish tone, the Dollar could rebound strongly.

For now, investors are hesitant to make bold moves. Many traders are choosing to stay cautious until Wednesday’s announcement, which is expected to set the tone for the Dollar in the weeks ahead.

Canadian Dollar Struggles to Gain Strength

While the U.S. Dollar is waiting for Fed signals, the Canadian Dollar (CAD) isn’t showing much strength either. Normally, weakness in the U.S. Dollar would provide some lift to the CAD, but that hasn’t been the case this time.

The main reason? Markets widely expect the Bank of Canada (BoC) to cut interest rates by 25 basis points this week. Such a move would reduce the Canadian Dollar’s appeal against other major currencies. Investors are already positioning themselves for this outcome, leaving little room for CAD to rally.

Adding to the cautious outlook is Canada’s Consumer Price Index (CPI) data, which is also due this week. Inflation numbers are expected to show further moderation, reinforcing the case for a BoC rate cut. If inflation continues cooling, it will give the central bank more justification to act on policy easing without worrying too much about fueling price growth.

Global Implications of Central Bank Moves

The decisions by the Fed and BoC won’t just impact the U.S. Dollar and Canadian Dollar—they will ripple across global financial markets.

-

For the U.S. Dollar: A dovish Fed would likely push investors toward riskier assets, weakening the Dollar while boosting equities and possibly emerging market currencies.

-

For the Canadian Dollar: A rate cut by the BoC may drag CAD lower, particularly if oil prices fail to provide any support. Since Canada’s economy is heavily tied to energy exports, oil often plays a key role in CAD’s performance.

-

For Investors Globally: Both decisions could influence bond markets, commodity prices, and cross-currency trades. Traders everywhere are watching closely because the direction of U.S. and Canadian policy often sets a broader tone for global central banking trends.

Final Summary

This week is shaping up to be a critical one for currency markets. The U.S. Dollar has been holding steady despite weak consumer confidence numbers, but all eyes are now on the Federal Reserve’s upcoming decision. Investors expect a softer stance from the Fed, which could weigh on the Dollar if confirmed.

Meanwhile, the Canadian Dollar is struggling to capitalize on USD weakness, as markets brace for a Bank of Canada rate cut. With inflation in Canada cooling and rate expectations already priced in, CAD may continue to face pressure.

In short, both currencies are at a crossroads. By midweek, the announcements from the Fed and BoC will provide clearer direction not only for the Dollar and Loonie but also for the broader global financial landscape. Until then, markets remain cautious, waiting for the next big move.

AUDUSD rallies as softer Fed stance sparks fresh optimism in markets

The foreign exchange market is buzzing with activity as the Australian Dollar (AUD) continues to climb against the US Dollar (USD). Investors are paying close attention to shifting expectations around the Federal Reserve’s monetary policy, upcoming US economic indicators, and important labor market data from Australia. Let’s dive deeper into what’s driving this momentum, why market sentiment is upbeat, and what traders are looking out for in the coming days.

AUDUSD is moving in an uptrend channel

Why the Market Is Excited About the Fed

The main reason behind the positive outlook for AUD/USD right now is the growing belief that the Federal Reserve is preparing to cut interest rates. Markets have been expecting this move for some time, but confidence is now stronger than ever that the Fed will announce its first rate cut during the week.

The Power of Monetary Easing

When a central bank lowers interest rates, it usually boosts investor confidence by making borrowing cheaper and encouraging economic growth. For the US Dollar, however, lower rates can weaken its appeal compared to other currencies, especially those linked with growth and risk sentiment, like the Australian Dollar.

In fact, analysts at major financial institutions have hinted that the Fed may not stop at just one rate cut. Many expect multiple cuts through the rest of the year, as the US labor market shows signs of stress and concerns about long-term growth remain. This anticipation has already been priced in by many investors, fueling strength in the Aussie.

Global Market Sentiment Keeps Risk Assets Attractive

Beyond Fed policy, the overall mood in global markets has been optimistic. Stock markets, such as the S&P 500 futures, have been trending higher, reflecting improved risk appetite among traders. When investors are feeling confident, currencies tied to commodities and global growth — like the Australian Dollar — tend to shine.

On the other hand, the US Dollar Index, which measures the strength of the Greenback against a basket of major peers, has been slightly weaker. This contrast highlights a shift in momentum: while the Dollar loses some of its safe-haven strength, the Aussie is gaining from the risk-on environment.

Key Economic Data on the Horizon

While Fed policy is the main driver, traders also have their eyes set on two important sets of economic data coming up this week.

US Retail Sales Data

On Tuesday, the US will release its Retail Sales figures. This report is a crucial indicator of consumer spending, which is the backbone of the American economy. Even moderate growth in retail sales signals resilience in the economy. However, if the numbers fall short of expectations, it could reinforce the case for the Fed to continue cutting rates more aggressively.

Australian Employment Data

Later in the week, attention will shift to Australia, where fresh employment figures are set to be released. The unemployment rate is expected to remain stable, and job additions are projected to continue, though at a slightly slower pace than before.

Why does this matter? The Reserve Bank of Australia (RBA) pays close attention to labor market conditions when deciding on its interest rate path. A strong jobs report could ease pressure on the RBA to consider rate cuts, while weaker results might push them toward policy adjustments later in the month.

How AUD/USD Traders Are Interpreting the Situation

The current setup is particularly interesting because both the US and Australian central banks are being closely monitored. However, the balance of expectations favors the Australian Dollar for now:

-

Fed outlook: Clear chances of rate cuts, which weigh on the US Dollar.

-

RBA outlook: Stable employment data could keep the RBA cautious, but not as aggressive as the Fed in easing policy.

This contrast gives AUD an edge in the short term. If risk sentiment continues to improve and data supports the case for steady Australian growth, the Aussie may maintain its upward trajectory.

Final Summary

The AUD/USD pair has been climbing on the back of upbeat market sentiment and strong bets that the Federal Reserve will begin cutting interest rates soon. Investors are closely monitoring upcoming US Retail Sales data and Australia’s labor market report for fresh clues on economic strength in both countries.

Right now, the combination of a softer US Dollar, improving global risk appetite, and steady Australian employment conditions is providing solid ground for the Aussie to outperform. Traders should watch the week’s data carefully, as any surprises could shift expectations for both the Fed and the RBA, ultimately influencing the next big move in AUD/USD.