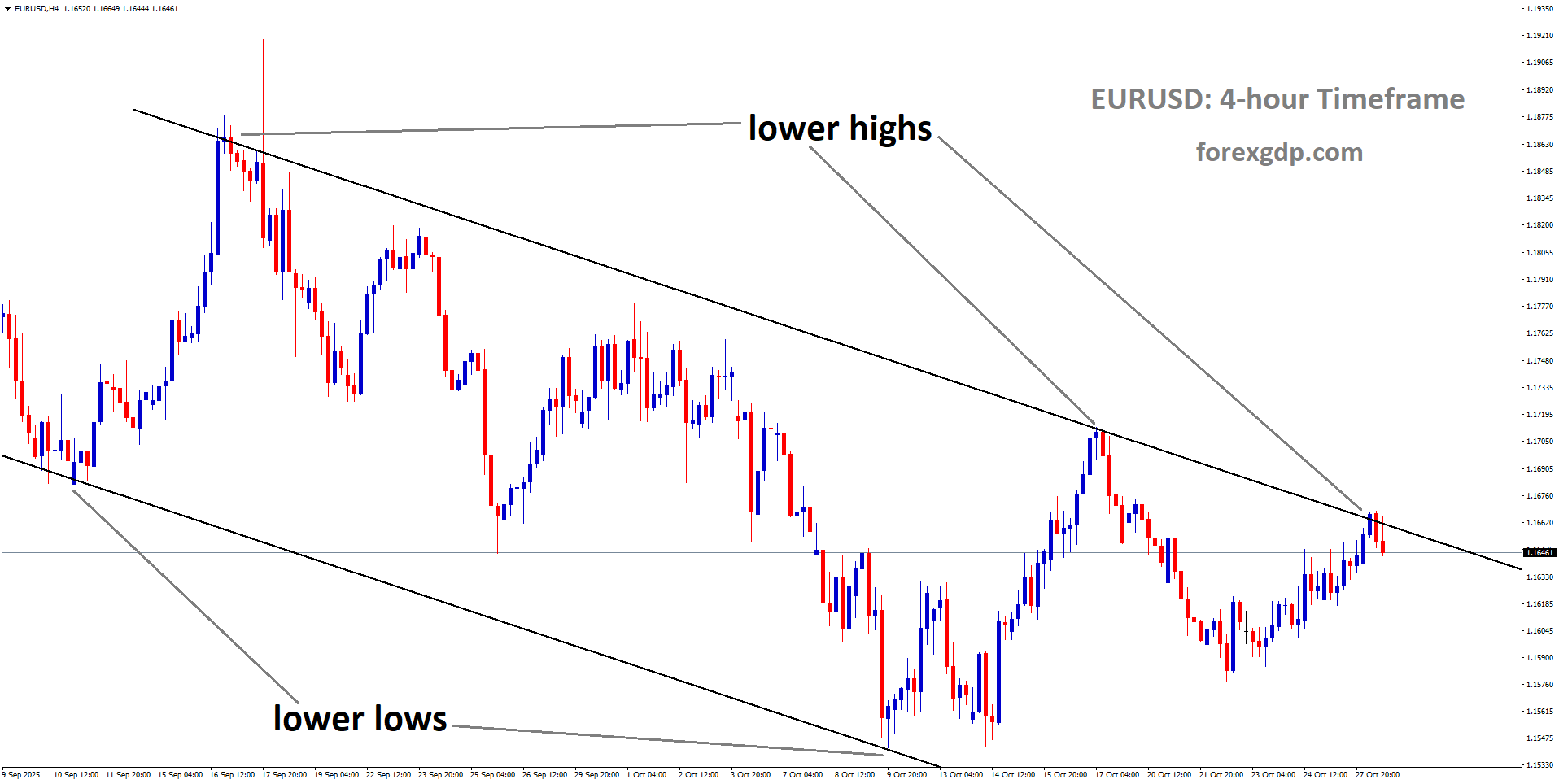

EURUSD is moving in a downtrend channel, and the market has reached the lower high area of the channel

EURUSD Strengthens on Market Optimism, Eyes Turn to Fed’s Next Move

The Euro has been making steady progress lately, showing strong momentum as it continues to climb against the US Dollar. This upward move comes as global investors find new reasons to stay positive, especially with the renewed hopes of a trade deal between the US and China and growing market expectations that the Federal Reserve will soon lower interest rates. These developments have increased risk appetite, pushing the Euro higher while putting pressure on the safe-haven US Dollar.

Why the Euro Is Gaining Momentum

In recent days, the Euro has seen consistent growth, extending its upward trend for nearly a week. This rise has been largely driven by renewed optimism in global trade relations and expectations of a potential rate cut by the US Federal Reserve. When markets expect the Fed to ease monetary policy, it generally weakens the US Dollar, making other currencies like the Euro more attractive to investors.

The positive sentiment in the market also stems from news that the United States and Japan have signed an important agreement concerning the supply of rare earth minerals. These materials are crucial for modern technology, and the deal is designed to reduce dependency on China. The cooperation between these two major economies has added a sense of stability to the market, encouraging investors to take on more risk.

Adding to that, the tone from the White House has been noticeably positive regarding trade relations with China. The US President has expressed optimism about achieving a productive deal with the Chinese government, and US Treasury officials have indicated that earlier threats of steep tariffs are no longer on the table. This has helped calm fears of an escalating trade war, further boosting investor confidence worldwide.

The Federal Reserve’s Role in Shaping Market Sentiment

Another key factor influencing the Euro’s recent strength is the expectation of a rate cut by the US Federal Reserve. The Fed’s decisions on interest rates often have a major impact on currency markets. When the Fed signals lower rates, it typically makes the US Dollar less appealing because investors seek higher returns elsewhere.

Recent US inflation data came in weaker than expected, reinforcing the belief that the Fed will act soon to support the economy by lowering rates. Market watchers are expecting a 25-basis-point rate cut, and there is growing speculation that another reduction could come before the end of the year.

However, the situation is somewhat complicated by the limited amount of recent economic data available. Ongoing government disruptions in the US have slowed the release of key statistics, making it difficult for the central bank to rely on concrete information. Still, traders are confident that the Fed will continue to lean toward a more supportive monetary stance, which tends to favor riskier assets like the Euro.

While investors await official confirmation, attention is turning to other US economic indicators, such as housing and consumer confidence data. These numbers might give some clues about the overall health of the US economy, but they are unlikely to change the current sentiment significantly. As long as optimism remains strong, the Euro is expected to hold its ground.

Market Mood: Risk Appetite Remains High

The broader market mood continues to support the Euro. Investors appear more willing to take chances in riskier assets as fears about global trade tensions fade. Normally, when markets feel uncertain or unstable, the US Dollar benefits because it is considered a safe haven. But right now, the situation is reversed—the more positive the mood, the weaker the Dollar becomes.

Even though some economic reports from Europe have not been encouraging, the Euro has managed to stay strong thanks to the upbeat global environment. For example, recent data from Germany showed that consumer confidence had fallen to its lowest level in seven months. Despite this, the Euro continues to benefit from overall optimism about trade and global growth.

This resilience highlights how market sentiment can sometimes outweigh local economic data. Investors are currently focusing more on international developments, such as trade negotiations and central bank policies, rather than on short-term fluctuations in consumer surveys or business sentiment reports.

US and Japan’s Partnership Adds Stability

One of the most significant developments adding to global stability is the cooperation between the United States and Japan. Their recent agreement on securing rare earth supplies is an important step in reducing reliance on China for critical raw materials used in everything from electronics to renewable energy systems. This deal not only helps both countries secure essential resources but also strengthens their economic ties, which reassures global markets.

In addition, the US Treasury has encouraged Japan to continue pursuing sound monetary policies, hinting that both nations are aligned in maintaining a balanced approach to growth and inflation. These coordinated efforts between major economies send a clear signal that global cooperation remains strong, despite the challenges of recent years.

This kind of international alignment helps to keep market volatility in check and supports risk sentiment. As a result, the Euro, which often benefits during periods of global confidence, continues to find steady demand.

How European and US Consumer Data Play a Role

While major geopolitical developments often dominate the headlines, smaller economic data points also play a role in shaping currency trends. In Europe, a recent survey from the European Central Bank revealed that inflation expectations among consumers have slightly eased for the next twelve months. Although this may indicate mild concern about slower price growth, it has not had a noticeable impact on the Euro’s performance.

In the United States, upcoming housing market figures and consumer confidence data could provide short-term direction. However, given the strong market belief in an upcoming Fed rate cut, these reports are unlikely to trigger major shifts unless they deliver a big surprise. Investors are currently more focused on policy and trade developments than on smaller data releases.

Final Summary

In simple terms, the Euro’s recent strength is being fueled by a mix of global optimism, trade cooperation, and expectations of easier monetary policy in the United States. The improving relationship between major economies, such as the US, China, and Japan, has reduced fears of a trade war, encouraging investors to move away from the safety of the Dollar and into riskier assets like the Euro.

Meanwhile, the Federal Reserve’s anticipated rate cut adds to the pressure on the US Dollar, further supporting the Euro’s upward move. Even though some European economic figures have shown weakness, the overall tone of the market remains positive, allowing the Euro to stay firm.

In the coming weeks, much will depend on how central banks and global leaders navigate these shifting economic conditions. But for now, the Euro’s outlook appears bright, supported by renewed investor confidence and an improving global atmosphere that favors growth and stability.

GBPUSD Drops as UK Price Cuts Spark Fresh Rate Cut Speculation

The Pound Sterling has seen a sharp drop against major global currencies this week, as new data suggests that UK retailers are cutting prices to attract customers. While the global market mood has improved, the British currency continues to weaken due to increasing expectations that the Bank of England (BoE) could soon lower interest rates.

Let’s take a closer look at what’s driving these movements and what it could mean for both the UK economy and international markets.

UK Retailers Slash Prices, Stirring Talk of BoE Rate Cuts

The latest figures from the British Retail Consortium (BRC) reveal that shop prices in the UK declined by 0.3% in October, marking the first fall since March. This drop shows that retailers are actively reducing prices to boost sales as consumer demand remains fragile.

When retailers start cutting prices, it often signals weakening inflation pressures — and for the Bank of England, that can be a reason to consider lowering interest rates to support economic activity.

Analysts believe that this latest move by retailers has strengthened the argument for a BoE rate cut in the near future. Lower rates would make borrowing cheaper for businesses and households, potentially giving the economy a short-term boost. However, it also means a weaker Pound as investors anticipate reduced returns from UK assets.

Market Expectations from the Bank of England

A Reuters survey taken during the European session suggests that the BoE might not cut rates before the end of the year, but markets are already pricing in at least one cut for early next year. The same poll predicts that UK inflation will continue to ease, falling to around 3.6% this quarter, and averaging 2.5% in 2026 and 2.1% in 2027.

GBPUSD is moving in a downtrend channel

These forecasts indicate a steady path toward the BoE’s target of 2% inflation. However, for now, the weak consumer demand and lower retail prices are adding pressure on policymakers to act sooner rather than later.

Global Mood Lifts as US and China Inch Toward Trade Deal

While the Pound struggles domestically, international developments are offering a glimmer of hope to global investors. Optimism has been rising over renewed progress in trade talks between the United States and China, the world’s two largest economies.

Earlier this week, US President Donald Trump shared his confidence in reaching a deal with China. Speaking to reporters on Air Force One, Trump said he expected to make an announcement after his scheduled meeting with Chinese leader Xi Jinping in South Korea later this week.

“I’ve got a lot of respect for President Xi, and I think we’re going to come away with a deal,” Trump said, suggesting the possibility of a visit to China in early 2026.

This statement has helped restore some risk appetite among investors, pushing them toward higher-yielding assets and away from safer currencies like the US Dollar.

Positive Signals from Washington and Beijing

Further boosting optimism were remarks from US Treasury Secretary Scott Bessent, who hinted that Washington might delay additional tariffs on Chinese imports. He also mentioned that China could pause its restrictions on rare earth exports, which have been a key point of tension between the two nations.

Such positive developments have raised hopes that trade relations between the US and China could stabilize, offering relief to global markets that have been rattled by tariff disputes for years.

Federal Reserve Expected to Cut Interest Rates

While the trade talks dominate headlines, another major event is shaping the financial landscape: the Federal Reserve’s upcoming policy decision.

The Fed is widely expected to cut interest rates, a move aimed at supporting the US economy amid signs of slowing growth, weak job demand, and a lingering government shutdown. The central bank’s decision could have significant ripple effects across global currency markets, including the British Pound.

Why the Fed May Cut Rates Again

Recent US data shows that inflation remains moderate, and several members of the Federal Open Market Committee (FOMC) have publicly voiced concerns about a weakening labor market. Fed Chair Jerome Powell, speaking earlier this month, acknowledged that “downside risks to the job market have increased,” reinforcing expectations of another rate cut.

In addition, the ongoing US government shutdown, now stretching into its fourth week, has added to the economic uncertainty. Many investors believe the Fed will use this opportunity to signal further support for growth through lower borrowing costs.

What to Expect from the Fed’s Outlook

Alongside the rate decision, traders will also watch for the Fed’s monetary policy projections, known as the “dot plot,” which shows where policymakers expect interest rates to be in the future.

At the September meeting, the Fed projected that the Federal Funds Rate could fall to around 3.6% by the end of the year, implying at least one more rate cut in December. If the Fed maintains this stance, it could put additional downward pressure on the US Dollar — though this might not be enough to lift the Pound substantially if the BoE also turns dovish.

Pound Sterling’s Reaction: Weakening Despite Global Optimism

Despite a generally upbeat global mood, the Pound has failed to gain traction. During Tuesday’s European session, the GBP/USD pair reversed early gains and slipped back as the Pound came under pressure from growing rate cut speculation.

The decline in UK retail prices has overshadowed the positive global sentiment, suggesting that traders are more concerned about domestic fundamentals than external developments.

Meanwhile, the US Dollar itself isn’t faring particularly well, as markets anticipate the Fed’s dovish stance. However, the combination of a soft Dollar and a weaker Pound has kept the currency pair largely range-bound, with neither side gaining a clear advantage.

What This Means for the Markets Going Forward

The next few weeks will likely be volatile for currency traders and investors. On one hand, optimism surrounding the US-China trade talks could support riskier assets and weaken the US Dollar. On the other hand, signs of cooling UK inflation and speculation about a BoE rate cut are expected to limit any meaningful rebound for the Pound Sterling.

Investors will continue to monitor inflation data, retail sales, and any fresh statements from central bank officials to gauge the next possible moves.

The interplay between these factors — easing UK price pressures, a cautious BoE, an accommodative Fed, and improving trade relations — will determine the short-term direction of major global currencies.

Final Summary

The Pound Sterling is underperforming as new data shows a rare decline in UK shop prices, raising speculation that the Bank of England could cut interest rates sooner than expected. While global sentiment has improved thanks to renewed optimism over a potential US-China trade agreement, domestic economic weakness continues to weigh on the Pound.

At the same time, the Federal Reserve’s expected rate cut is adding to market uncertainty, creating a delicate balance between global growth hopes and domestic economic concerns.

In the coming days, traders will keep an eye on both the BoE’s tone and the Fed’s policy stance. With inflation cooling and trade talks progressing, the overall market mood remains cautiously optimistic — but for the Pound, the road to recovery may still be a slow and uncertain one.

USDJPY Extends Rally Fueled by Intervention Hopes and Contrasting Monetary Outlooks

The Japanese Yen (JPY) is making a strong comeback this week, catching the attention of global traders and investors. On Tuesday, the currency extended its gains as speculation grew that Japan’s government might step in to prevent further weakness in the Yen. This possible intervention comes at a time when markets are preparing for two major events — the upcoming policy announcements from the Federal Reserve (Fed) in the United States and the Bank of Japan (BoJ).

The sudden shift in the Yen’s momentum isn’t just about intervention fears. It also reflects broader market sentiment. Investors are becoming cautious as they wait for clarity on the direction of monetary policies from two of the world’s most influential central banks. As a result, the Yen is benefiting from safe-haven demand, especially among traders who are adjusting their positions ahead of these key events.

Growing Confidence in Japan’s Economic Outlook

Recent data has added another layer of confidence to the Yen’s upward movement. Japan’s service-sector inflation rose for the second month in a row in September, signaling that the domestic economy continues to strengthen. This increase supports the idea that the Bank of Japan may gradually move toward tightening its monetary policy, a shift from its long-standing ultra-loose approach.

This stands in sharp contrast to the expectations for the US Federal Reserve, which is widely expected to start cutting interest rates in the near term. The difference in policy direction between the two central banks is significant. As investors anticipate softer policies from the Fed, the US Dollar (USD) has been losing some of its recent strength, further fueling gains in the Yen.

At the same time, Japan’s new Prime Minister, Sanae Takaichi, is expected to introduce major fiscal spending plans to support growth. While such policies could limit how much the Yen appreciates in the short run, they are likely to boost overall confidence in Japan’s economic prospects, keeping the currency well-supported.

Government Voices Raise Intervention Concerns

The market’s focus intensified after Japan’s Economics Minister, Minoru Kiuchi, made remarks highlighting the importance of stable foreign exchange movements. He emphasized that currency values should reflect economic fundamentals and that the government would closely watch for any excessive volatility that could harm Japan’s economy.

His comments came just as the Yen was beginning to gain strength, fueling speculation that authorities might be preparing for potential action to prevent erratic moves in the currency markets. Japan has a history of intervening to curb sharp declines in the Yen, especially when volatility threatens economic stability or drives import costs higher.

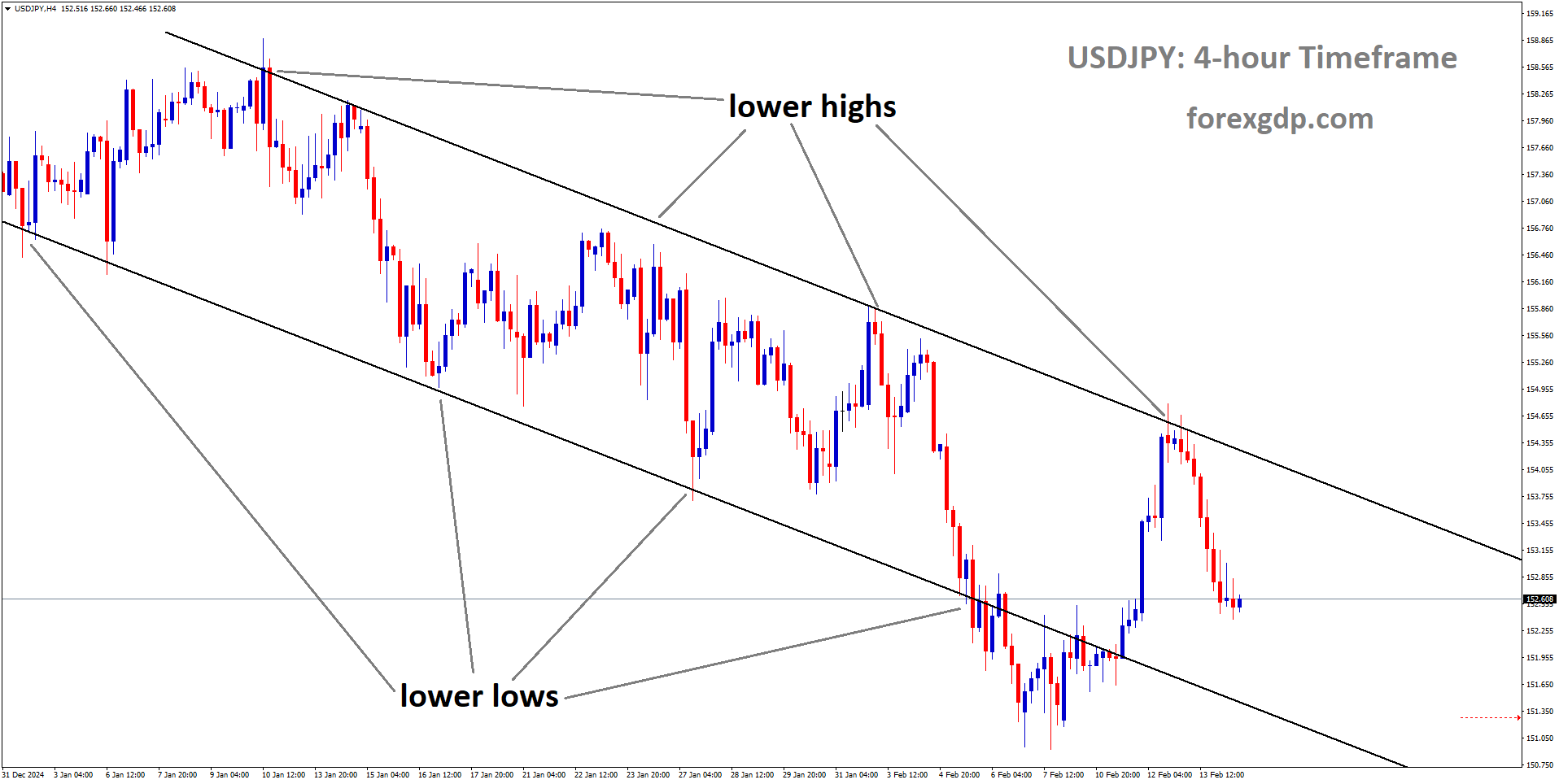

USDJPY is moving in a descending triangle pattern, and the market has reached the lower high area of the pattern

Prime Minister Sanae Takaichi also spoke about her ambition to strengthen the Japan-US alliance, describing it as a “new golden age” for bilateral relations. Around the same time, US President Donald Trump mentioned progress on a new and fair trade agreement with Japan, adding to the sense that cooperation between the two nations could be deepening.

All these statements together created a sense of political and economic alignment that encouraged investors to view the Yen more positively.

Market Sentiment and Central Bank Dynamics

While the Yen’s recent rally has been impressive, it’s important to understand the broader forces at play. The Bank of Japan is carefully balancing two conflicting goals — supporting economic growth and addressing rising inflation. The recent increase in the Services Producer Price Index (SPPI), which climbed to 3.0% in September, indicates that inflationary pressures are slowly building in Japan.

This has led traders to believe that the BoJ could consider tightening its policy sooner rather than later. In contrast, the US Federal Reserve appears to be moving in the opposite direction. Market participants now widely expect the Fed to lower borrowing costs by 25 basis points during its upcoming meeting. There’s even growing speculation that another rate cut could follow in December.

This clear divergence between the BoJ and the Fed has placed downward pressure on the US Dollar while boosting demand for the Yen. Investors often shift toward lower-yielding but stable currencies like the Yen when US interest rates start falling.

However, the story isn’t entirely one-sided. Prime Minister Takaichi, known for her pro-stimulus stance, may not be quick to support any aggressive tightening by the BoJ. As a result, traders will be paying close attention to the BoJ’s upcoming announcement to see whether policymakers hint at a rate hike by the end of the year or early next year.

Trade Optimism and Its Impact on the Yen

Adding to the mix, global trade developments have also influenced market behavior. Ahead of an anticipated meeting between US President Donald Trump and Chinese leader Xi Jinping, optimism grew that the two sides were close to reaching a trade deal. Trump even suggested that a final agreement could be signed as early as Thursday, which boosted risk appetite across markets.

When investor sentiment improves globally, safe-haven currencies like the Yen tend to lose some of their appeal. That’s because traders feel more comfortable moving their money into riskier assets like equities or emerging-market currencies. However, this time, the effect appears to be limited. Despite the optimistic tone surrounding trade talks, the Yen has managed to hold onto its gains, suggesting that the market remains cautious and focused on monetary policy developments rather than global trade alone.

Looking Ahead: What Traders Are Watching Next

With both the Federal Reserve and the Bank of Japan set to make policy announcements within days, markets are likely to stay on edge. Traders are carefully weighing the possible outcomes.

If the Fed confirms a rate cut, the US Dollar could weaken further, allowing the Yen to extend its rally. On the other hand, if the BoJ signals patience or delays its tightening plans, it could offset some of the Yen’s recent strength. The next few days are expected to bring heightened volatility as investors react to each new headline and policy statement.

Another factor to watch is Japan’s approach to potential market intervention. The authorities have made it clear that they want to avoid excessive fluctuations in the currency market, and any official move to stabilize the Yen could trigger swift and significant reactions across global financial markets.

Final Summary

The Japanese Yen’s resurgence reflects a complex mix of factors — government vigilance, diverging central bank policies, and evolving global sentiment. With renewed concerns about possible intervention and clear signs of economic resilience in Japan, the Yen has gained strong traction in recent days.

At the same time, the Federal Reserve’s expected move toward rate cuts has weakened the US Dollar, further supporting the Yen’s upward momentum. Political comments from Japanese leaders and improving economic data have only strengthened the belief that Japan is regaining economic confidence.

For now, traders are likely to stay cautious until both the BoJ and the Fed reveal their next steps. Whether the Yen continues to climb or pauses for a breather will depend largely on how these decisions shape market expectations in the weeks ahead.

In short, the Yen’s latest rally is not just a short-term reaction — it’s a reflection of deeper shifts in global monetary dynamics and renewed confidence in Japan’s ability to navigate economic change with resilience.

USD/CHF Stays Under Pressure with Fading Chances of Swiss Rate Cuts

The USD/CHF currency pair continues to slide, marking its fourth straight day of losses. The movement comes amid shifting monetary policy expectations from both the Swiss National Bank (SNB) and the US Federal Reserve (Fed). While the Swiss Franc finds strength in a steady domestic policy outlook, the US Dollar struggles as markets prepare for another rate cut by the Fed.

A Stronger Swiss Franc: Why the SNB’s Policy Outlook Matters

The Swiss National Bank has taken a steady and cautious approach toward its monetary policy. Recent minutes from its September meeting revealed that officials are not considering a return to negative interest rates—a move that was once a cornerstone of Switzerland’s monetary stance.

The End of Negative Rates

For years, the SNB relied on negative interest rates to counter the strong Swiss Franc and protect its export-driven economy. However, times have changed. The SNB now believes that its earlier measures have already produced the desired economic impact, and the effects are still filtering through the system.

By downplaying the risk of deflation, the SNB has made it clear that Switzerland’s economy remains stable enough to withstand tighter financial conditions. This shift has boosted investor confidence in the Franc, giving it an upper hand against the US Dollar.

Market Confidence Returns to the Franc

As expectations of further easing fade, the Swiss Franc becomes more appealing to traders seeking stability. The SNB’s confidence in the resilience of the economy sends a powerful message: the country doesn’t need to rely on artificial support anymore.

This renewed trust strengthens the Franc’s position in the global currency market. As a result, the USD/CHF pair continues to weaken, reflecting the widening difference between the Swiss and American economic outlooks.

The US Dollar Faces Pressure from Fed Rate Cut Expectations

While the Swiss Franc gains from stability, the US Dollar is under pressure as traders brace for another round of interest rate cuts by the Federal Reserve. Market sentiment suggests that the Fed will likely announce a 25-basis-point reduction in its upcoming meeting.

Fed’s Balancing Act: Inflation vs. Growth

The Federal Reserve is walking a fine line. On one hand, inflation remains above the 2% target, which argues against easing monetary policy too quickly. On the other, the labor market is showing signs of fatigue, and parts of the economy are slowing down.

This creates a dilemma: should the Fed prioritize fighting inflation, or should it focus on preventing an economic slowdown? Many traders believe the Fed will choose to support growth by cutting rates, especially as financial markets have already priced in a high probability of such a move.

USDCHF is moving in a downtrend channel

Government Uncertainty Adds to the Pressure

The recent US government shutdown has further complicated matters. It’s creating uncertainty among policymakers, businesses, and investors alike. The longer the shutdown drags on, the greater its potential impact on economic performance.

This instability gives the Fed another reason to act sooner rather than later. By cutting rates, the central bank aims to inject confidence back into the economy. However, lower interest rates also make the US Dollar less attractive compared to currencies like the Swiss Franc, which now carry a perception of steadiness and strength.

Global Trade Sentiment and Its Influence on the Dollar

Amid the monetary shifts, global trade developments are also shaping currency movements. Optimism surrounding the ongoing US-China trade negotiations has created mixed reactions in the market.

Positive Trade Talks Bring Temporary Relief

Over the weekend, senior officials from the United States and China announced that they had reached a preliminary framework agreement on key trade issues, including tariffs. The announcement followed meetings held in Malaysia and sparked hopes of a potential resolution when Presidents Trump and Xi meet later in South Korea.

This progress has temporarily reduced safe-haven demand for the US Dollar. Typically, during uncertain times, traders flock to the Dollar for security. But when optimism rises—such as during positive trade developments—the need for such protection fades. This shift in sentiment limits the Dollar’s upside potential.

Safe-Haven Dynamics Benefit the Franc

Interestingly, while the Dollar often acts as a global safe haven, the Swiss Franc shares that same reputation. In times of economic tension, investors tend to move toward the Franc as well. However, in this case, the combination of a confident Swiss policy stance and cautious US outlook is tilting the balance in favor of Switzerland’s currency.

A Tug of War Between Two Monetary Worlds

The current USD/CHF trend reflects a broader global story—a tug of war between two different monetary strategies. The Swiss National Bank is signaling stability and patience, while the US Federal Reserve leans toward easing and support.

This divergence in policy direction is critical for traders and investors. It highlights the importance of understanding not just economic indicators, but also the psychology of central banks. When one central bank holds steady and another moves toward loosening policy, currency markets react accordingly.

For now, the Swiss Franc appears to be the stronger contender. Its rise isn’t just about Switzerland’s internal policy—it’s also a reflection of global investors’ search for safety and confidence in uncertain times.

Final Summary

The USD/CHF decline paints a clear picture of the shifting global economic landscape. As the Swiss National Bank rules out negative interest rates and reinforces its trust in Switzerland’s economic resilience, the Franc gains strength. Meanwhile, the US Dollar faces downward pressure from expectations of another Federal Reserve rate cut, uncertainty from government gridlock, and mixed signals from global trade talks.

Investors are closely watching how these developments unfold. The balance between monetary stability in Switzerland and policy flexibility in the United States will continue to drive the USD/CHF pair in the coming weeks. For now, the scales seem to tip toward the Swiss Franc—a currency that stands firm amid the turbulence surrounding global monetary policy.

AUDUSD Struggles to Hold Ground as Traders Weigh RBA’s Next Move

The Australian Dollar (AUD) faced renewed weakness after an early session of steady gains, largely driven by shifting expectations surrounding central bank policies in both Australia and the United States. While optimism had supported the currency earlier, the tone has changed as global traders refocus on interest rate outlooks and macroeconomic signals that could influence both the AUD and the USD in the near term.

RBA’s Firm Stance Keeps Traders on Alert

The Reserve Bank of Australia (RBA) has remained in the spotlight as investors assess its approach toward monetary policy tightening. RBA Governor Michele Bullock’s recent comments hinted that the labor market in Australia still appears somewhat tight, even as the unemployment rate showed a minor increase. Her remarks led markets to reconsider their previous expectations of a rate cut, with the probability of such a move dropping sharply.

This cautious optimism from the RBA has provided some temporary relief to the Australian Dollar, as traders interpret Bullock’s message as a sign that the central bank is not yet ready to pivot toward easing. A tight labor market often signals underlying economic strength, which could discourage policymakers from lowering interest rates too quickly.

Market Eyes Inflation Data for Clearer Direction

Investors are now turning their attention to the upcoming quarterly inflation report and the monthly Consumer Price Index (CPI) figures. These data releases are expected to play a major role in determining whether the RBA maintains its current stance or adjusts rates in the coming months.

A stronger inflation reading could reinforce expectations that the RBA will keep rates steady for longer, while a weaker report might reignite discussions about potential cuts. For traders, these numbers are more than just statistics—they are signals that shape currency movements and influence short-term strategies in the forex market.

US Dollar Weakens as Fed Rate Cut Bets Grow

On the other side of the globe, the US Dollar (USD) has lost some ground amid growing market belief that the Federal Reserve (Fed) will deliver another rate cut soon. The dollar’s slide reflects investor concerns that the US economy may be slowing, prompting the Fed to act preemptively to sustain growth.

Market Confidence in Fed Rate Cuts Rises

According to market indicators, such as the CME FedWatch Tool, traders are heavily pricing in another interest rate reduction in the near term. The potential cut comes as part of the Fed’s broader effort to balance the dual challenge of high inflation and a softening labor market.

")

Recent economic reports from the US have shown mixed signals. Inflation appears to be gradually easing, with the latest Consumer Price Index (CPI) data showing a slower year-over-year increase. While the numbers remain above the Fed’s 2% target, the pace of price growth is cooling. At the same time, job growth has moderated, suggesting that economic momentum could be slowing more than policymakers anticipated.

These developments are feeding speculation that the Fed might continue its cautious easing cycle, aiming to prevent a deeper slowdown without reigniting inflationary pressures.

Trade Optimism Between the US and China Boosts Risk Sentiment

Beyond central bank decisions, another key factor influencing the Australian Dollar’s movement is the improving tone in global trade discussions—particularly between the United States and China.

Officials from both countries have reportedly made meaningful progress on several contentious issues, including trade tariffs and export controls. These advancements have paved the way for a potential high-level meeting between US and Chinese leaders to finalize a broader trade agreement.

This development matters for Australia because China is its largest trading partner. Any sign of easing trade tensions between Beijing and Washington tends to lift sentiment toward commodity-linked currencies like the AUD. When China’s economy shows stability or growth potential, demand for Australian exports—especially raw materials—often rises. That connection makes the AUD a reliable indicator of global trade confidence.

Why US–China Progress Matters for Australia

A resolution in trade disputes between the two major economies could have a ripple effect. Increased global demand and higher trade volumes would likely support Australian industries tied to mining, energy, and agriculture. For currency traders, such progress injects optimism and can lead to a stronger appetite for risk-sensitive assets like the Australian Dollar.

Mixed Economic Signals from Australia’s Business Sector

Recent reports on Australia’s business activity have presented a mixed picture of the economy’s health. The latest Manufacturing Purchasing Managers Index (PMI) slipped slightly below the neutral threshold, indicating a mild slowdown in factory output. However, the Services PMI showed improvement, suggesting that consumer-related industries continue to perform well.

AUDUSD is moving in an uptrend channel, and the market has rebounded from the higher low area of the channel

This contrast reflects the broader economic environment—one where some sectors feel the pressure of higher borrowing costs, while others remain resilient. For policymakers and investors, these figures highlight the importance of balancing economic growth with inflation control, a challenge that both the RBA and the Fed are currently facing.

Global Sentiment and Its Ripple Effect on the AUD

The performance of the Australian Dollar is often tied to broader global risk sentiment. When optimism prevails in markets—whether due to trade progress, easing monetary policies, or signs of economic recovery—currencies like the AUD tend to benefit. However, during periods of uncertainty, investors often move toward safer assets such as the US Dollar.

Right now, traders are juggling multiple influences:

-

The RBA’s careful approach to monetary policy.

-

Expectations of interest rate cuts from the Fed.

-

Developments in global trade relations.

-

Shifting inflation and employment data from both economies.

Each of these factors can sway the AUD/USD exchange rate, sometimes sharply and unpredictably.

Final Summary

The Australian Dollar’s recent weakness highlights how sensitive global currencies are to changes in central bank expectations and international developments. While the RBA’s firm stance on inflation control has temporarily supported the AUD, the broader outlook remains uncertain as traders await fresh data on prices and employment.

Meanwhile, the US Dollar faces downward pressure as the Fed leans toward further rate cuts to cushion the economy. The tug-of-war between these policy directions is creating a dynamic environment for currency markets, where sentiment can shift rapidly based on even minor data releases or comments from policymakers.

Adding another layer of complexity is the improving tone in US–China trade relations—a factor that could provide some indirect relief for the Australian economy if progress continues.

For now, traders and investors are keeping a close watch on economic indicators from both nations, knowing that the balance between policy caution and growth optimism will determine where the AUD heads next. In a world where every central bank statement and economic report matters, the coming weeks are likely to remain eventful for anyone tracking the Australian Dollar’s journey.