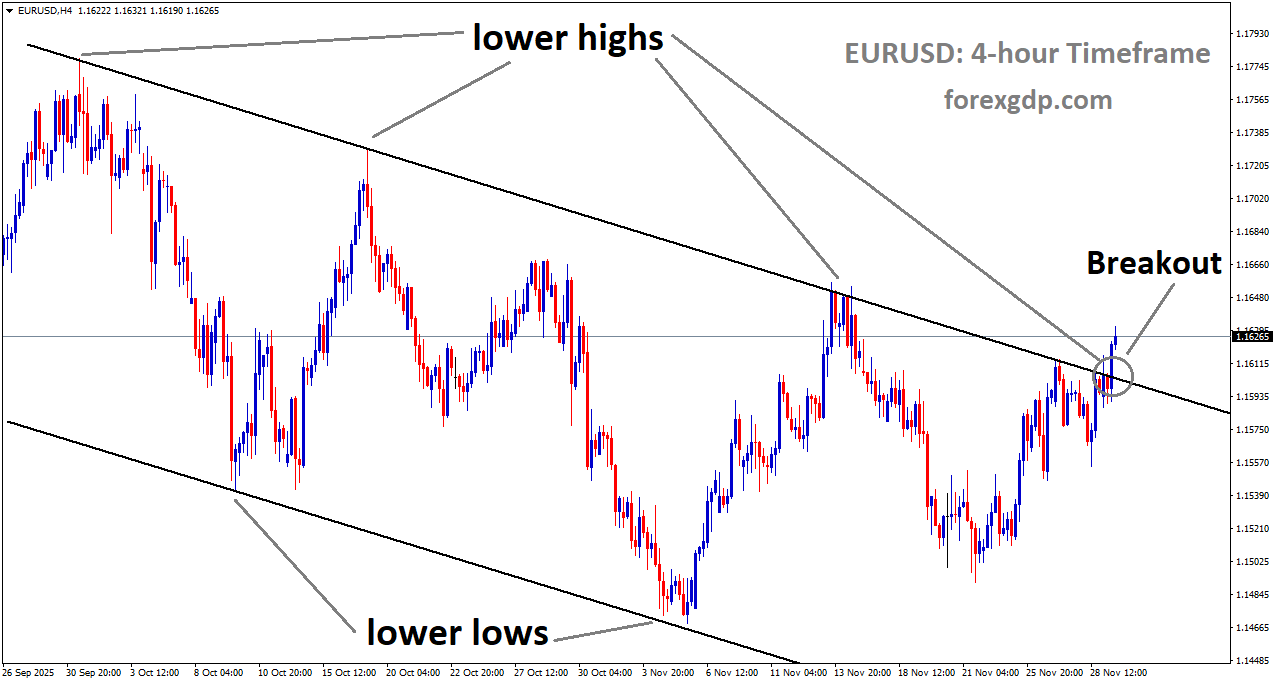

EURUSD has broken the descending channel on the upside

EURUSD pushes upward with the Dollar slipping across global markets

The Euro has been climbing steadily, reaching its highest level in two weeks as it moves beyond 1.1620. This steady rise continues even though recent data shows manufacturing activity in the Eurozone slipping more than expected. The latest manufacturing reading for November came in slightly weaker, but that has not been enough to slow the currency’s momentum.

Much of the Euro’s strength comes from a softer US Dollar. Investors remain cautious about holding the Dollar as they prepare for a potential interest rate cut from the US Federal Reserve. With the Fed widely expected to ease policy soon, the Dollar has struggled to find support, helping the Euro extend its winning streak.

Shifting Expectations for US Monetary Policy

The US Dollar remains under pressure as markets anticipate that the Federal Reserve could reduce interest rates next week. This expectation alone has been enough to keep the Dollar on the defensive, encouraging traders to move into other currencies, including the Euro.

There is also added attention on developments in US monetary leadership. Reports suggest that President Donald Trump may nominate Kevin Hassett, a known supporter of looser policy, as the next Federal Reserve chair. A figure seen as more cautious about tightening financial conditions would likely reinforce expectations of lower interest rates, adding another layer of pressure on the Dollar.

Later in the day, Federal Reserve Chairman Jerome Powell is scheduled to appear at a panel in California. However, he is not expected to comment on monetary policy due to the blackout period ahead of the December meeting. Even so, markets will be listening closely for any signals related to the economic outlook.

Eurozone Manufacturing Data Fails to Halt the Euro’s Advance

A Deeper Look at the Latest Economic Readings

New data from the Eurozone shows manufacturing activity falling to a five-month low in November. The final HCOB Manufacturing Purchasing Managers’ Index recorded a level of 49.6, slipping below both the preliminary estimate and the October figure. A reading below 50 indicates contraction, raising questions about the health of the region’s industrial sector.

Yet, the Euro has not been significantly affected. With broad weakness in the US Dollar dominating market sentiment, the currency has continued to attract buyers. Investors appear more focused on global shifts in monetary policy than on short-term regional data.

Why the Euro Still Looks Resilient

The main driver behind the Euro’s strength is confidence that the Federal Reserve will begin easing interest rates soon. Markets expect a 25-basis-point cut next week, with the possibility of more reductions in the coming year. Lower US interest rates typically weaken the Dollar, making other currencies more appealing.

In addition, Powell’s appearance at the Hoover Institution is expected to be centered on a memorial lecture rather than policy guidance. With no new monetary comments anticipated, traders are turning their attention to upcoming US economic data to gauge the next move for the Dollar.

Key US Data in Focus

Manufacturing Outlook in the US

Later in the day, the US will release the latest ISM Manufacturing PMI for November. Forecasters expect a slight decline from October’s reading, suggesting that manufacturing activity could remain sluggish. The Prices Paid component is expected to rise, which could offer clues about inflation trends. Many investors will also watch the employment component closely, as labor data continues to be a major influence on policy expectations.

A Busy Week for Economic Indicators

This week brings a wide range of economic updates that could influence both the Euro and the US Dollar. Some of the most important data releases include:

Eurozone Data Highlights

-

Harmonized Index of Consumer Prices (HICP) on Tuesday

-

Services PMI readings across the region on Wednesday

US Data Highlights

-

Services PMI on Wednesday

-

ADP Employment Change report on Wednesday

-

Personal Consumption Expenditures (PCE) Price Index on Friday

Each of these reports has the potential to shape market expectations about inflation, growth, and future interest rate decisions. With so many key indicators lined up, traders are preparing for possible shifts in currency trends throughout the week.

Growing Investor Attention on Global Conditions

Currency movements this week are being driven not only by individual data releases but also by broader expectations about global economic policy. The Euro’s current rise shows how much influence the US Dollar’s performance has on global markets. Even with weaker manufacturing numbers in Europe, the currency continues to attract strength because of shifting sentiment around the US economy.

At the same time, investors are closely watching political developments that may influence central bank leadership and long-term monetary direction in the United States. Decisions about interest rates, inflation management, and economic growth strategies all play a central role in shaping currency trends.

Final Summary

The Euro has reached its strongest levels in two weeks, supported largely by broad weakness in the US Dollar. Despite weaker manufacturing activity in the Eurozone, the currency continues to advance as markets expect the Federal Reserve to cut interest rates soon. Upcoming US data, including the ISM Manufacturing PMI and the PCE Price Index, will play a significant role in shaping expectations for policy decisions in the weeks ahead. With heavy economic calendars on both sides of the Atlantic, investors are preparing for an active period in currency markets as new information continues to influence the larger monetary outlook.

USDJPY declines with a sharp intraday boost supporting the strengthening Yen

The Japanese Yen began the week with a solid performance, gaining momentum against the US Dollar as expectations for a potential Bank of Japan rate hike grew stronger. A shift in global sentiment toward safer assets and softer tones surrounding the US Dollar also played a role, helping the Yen move to its highest level in two weeks during early European trading.

Market Mood Supports the Yen

The new week opened with a cautious atmosphere in global markets, giving the Yen an additional boost. When investors grow uncertain, they often turn to currencies seen as safe havens, and the Yen is one of the most favored. This shift helped strengthen the Japanese currency while adding pressure on the USD/JPY pair.

USDJPY is breaking the lower low area of the downtrend channel

At the same time, the US Dollar slid to its lowest level in nearly two weeks. This decline came as traders grew more confident that the Federal Reserve may take a more accommodative approach in the months ahead. With the Dollar losing support and the Yen gaining fresh momentum, the USD/JPY pair continued to drift lower.

Rising Confidence in a BoJ Rate Hike

Expectations for tighter monetary policy in Japan have been building steadily. Comments from Bank of Japan Governor Kazuo Ueda reinforced the belief that Japan could soon lift interest rates again. Ueda stated that the central bank would move forward with a rate increase if economic trends and price developments continue as anticipated.

This renewed confidence pushed yields on Japanese government bonds to their highest levels in several years. Notably, the two-year bond yield reached 1% for the first time since mid-2008, while the 20-year yield returned to levels last seen in late 2020. Higher yields tend to make a currency more appealing to investors, giving the Yen another layer of support and narrowing the gap between Japanese rates and those of other major economies.

Mixed Economic Signals From Japan

Japan’s latest economic reports also added context to the Yen’s performance. The Ministry of Finance confirmed that capital spending rose for a third consecutive quarter, increasing 2.9% on a yearly basis from July to September. Although this marked a slowdown compared to the previous quarter’s stronger growth, it still pointed to ongoing business investment resilience.

The country’s Composite PMI for November was finalized at 52.0, slightly higher than the previous month. The figure suggests steady, if modest, expansion in the private sector. While manufacturing remained under pressure and contracted for a fifth month in a row, the service sector continued to show growth, helping balance the overall reading.

Prime Minister Sanae Takaichi also emphasized continued responsible fiscal management, noting that the government will keep a close eye on interest rate movements and economic conditions. Her comments added stability to broader policy expectations.

Pressure on the US Dollar Continues

While domestic factors supported the Yen, developments in the United States placed additional weight on the Dollar. Several Federal Reserve officials recently hinted at the possibility of more accommodative policy, which encouraged traders to price in higher odds of a rate cut by December. This outlook weakened the Dollar’s appeal and helped drive the Dollar Index to its lowest point in nearly two weeks.

With the US currency losing ground, the USD/JPY pair extended its decline, slipping further below the mid-155 range during Asian trading hours.

Eyes on Upcoming US Data

Investors are now turning their attention to key US economic data scheduled for release this week. These early-month indicators will provide fresh clues about the health of the American economy and could influence expectations for Federal Reserve policy. The ISM Manufacturing PMI, due later today, is one of the first major reports that traders will focus on.

The upcoming data is expected to shape not only market sentiment surrounding the US Dollar but also the short-term direction of the USD/JPY pair. If the reports show signs of slowing activity or softer inflation, they may reinforce expectations of easier monetary policy from the Federal Reserve, which could continue to pressure the Dollar.

Broader Forces Shaping the Yen’s Movement

The Yen’s recent strength has been the result of several overlapping forces. On one side, expectations for a move by the Bank of Japan have created upward pressure by signaling a shift away from the ultra-loose monetary policy that defined much of Japan’s recent economic history. Higher bond yields only strengthened the currency’s appeal.

On the other side, the global market environment has played a key role. The cooling risk appetite helped drive demand toward safe-haven currencies, and the Yen was a major beneficiary. Meanwhile, the US Dollar faced challenges from shifting monetary policy expectations and uncertainty around the economic outlook.

This combination of domestic and international factors created the ideal backdrop for the Japanese Yen to climb to multi-week highs.

What Traders Are Watching Next

With the Yen gaining ground and the Dollar under pressure, traders are closely monitoring how upcoming US data and future comments from central bank officials might shift expectations. The degree to which economic reports align with or challenge current market assumptions could set the tone for currency movements throughout the week.

If Japan continues to signal a clear path toward higher interest rates while the United States leans toward easing, the narrowing rate gap may support further Yen strength. However, market conditions can shift quickly, and investors will be paying close attention to every new development.

Summary

The Japanese Yen started the week with strong gains, supported by rising expectations that the Bank of Japan may raise interest rates soon. Higher domestic bond yields, ongoing global caution, and weakening sentiment around the US Dollar all contributed to the Yen’s rise. Meanwhile, dovish expectations for the Federal Reserve pushed the Dollar lower, further shaping the movement of the USD/JPY pair. With important US economic data on the horizon, markets are watching closely for the next signals that could influence the direction of both currencies.

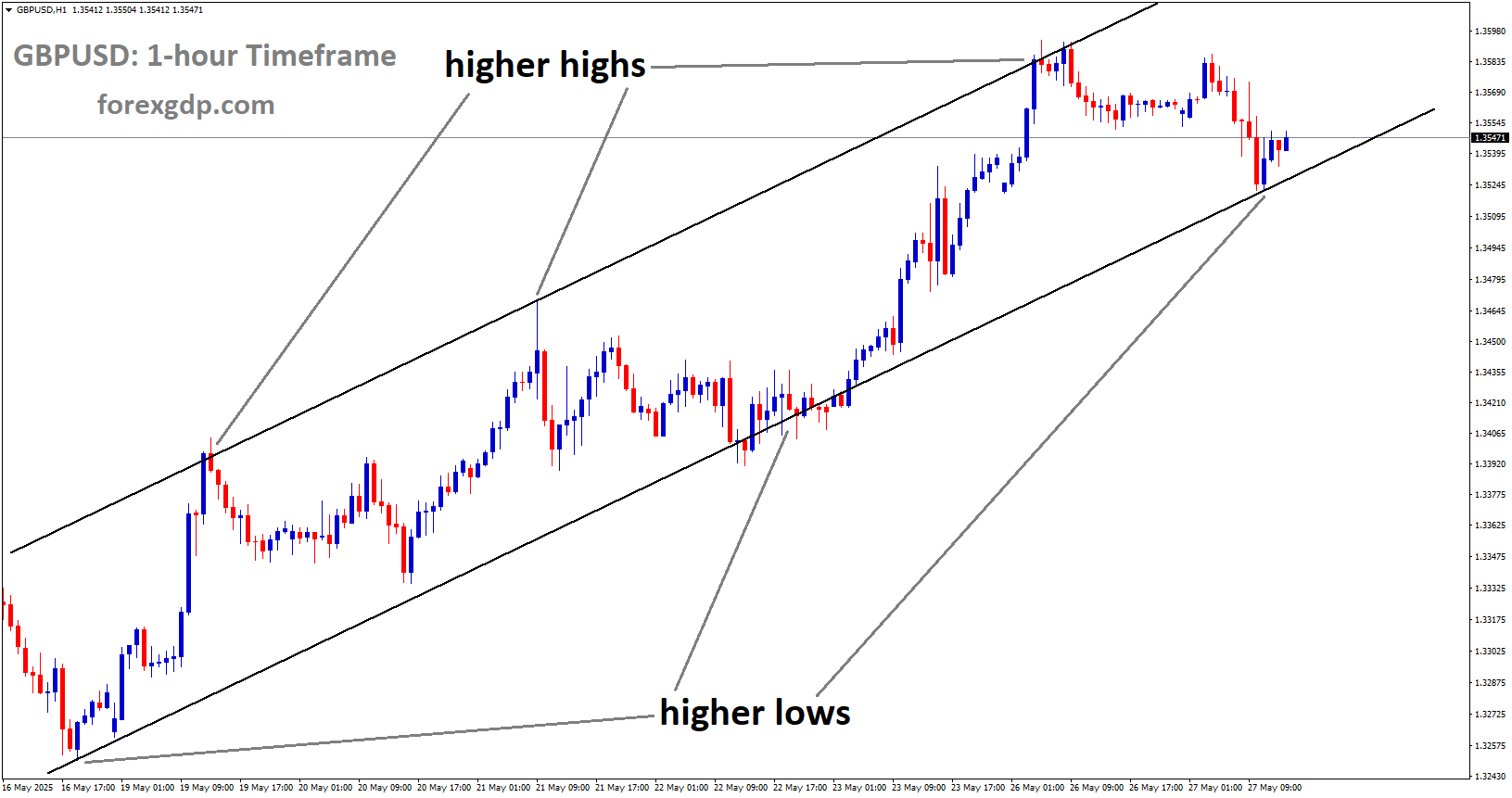

GBPUSD dips as sliding gilt yields and BoE rate-cut bets pressure the Pound

The Pound Sterling begins the week on a softer note, slipping against several major global currencies. This early weakness comes as investors grow more confident that the Bank of England may soon begin easing its monetary policy. With the next decision approaching, many traders anticipate that the central bank could announce a rate cut, reflecting signs of a cooling UK economy.

Recent economic data from the United Kingdom has shown slowing job growth and more moderate inflation. These trends have strengthened the belief that policymakers may choose a more supportive stance to help stabilize economic momentum. As expectations for a policy shift rise, the Pound has been unable to build upward traction.

Fiscal Policy Adds Additional Weight

Beyond monetary policy speculation, the UK’s latest fiscal plans have also shaped market sentiment. Chancellor Rachel Reeves recently outlined significant tax increases intended to address the country’s financial gap over the coming years. The announcement has influenced UK government bond performance, contributing to a decline in yields and putting further pressure on the Pound.

The government intends to raise a sizable amount of additional revenue over the next several years, aiming to improve the country’s fiscal health. While analysts acknowledge the commitment to reducing debt, concerns remain about the challenges involved in carrying out these plans. Credit rating agencies have highlighted that although the direction is positive, the risks tied to implementing such large adjustments cannot be ignored.

International Market Focus Turns to the Federal Reserve

US Policy Expectations Guide Currency Movements

Across the Atlantic, the US Dollar is also under pressure as investors position themselves ahead of an important Federal Reserve meeting. Market participants are widely expecting the Fed to begin reducing interest rates soon, which has contributed to broad Dollar softness.

GBPUSD is breaking the lower high area of the downtrend channel

Weakness in US labour indicators and expectations of limited inflationary impact from recent trade measures have added to speculation that the central bank may shift toward a more accommodative stance. As a result, the Dollar has continued to move lower, influencing major currency pairs and adding volatility to global markets.

With a heavy calendar of economic reports due this week, traders are preparing for possible swings. Labour market readings, in particular, remain in focus as they offer insight into the underlying strength of the US economy.

Key US Data Releases Shape the Week

One of the most anticipated reports will be the ADP Employment Change figure for November. This reading tracks hiring activity within the private sector and is often watched closely as an indicator of labor market conditions. Analysts expect a smaller increase in employment compared to the previous month, suggesting demand for workers may be moderating.

Another important release is the Manufacturing Purchasing Managers’ Index, which helps measure the health of US factory activity. A further decline in this index would point to ongoing challenges for manufacturers, adding momentum to expectations of future policy adjustments.

How These Developments Interact in Global Currency Markets

The Pound and Dollar Navigate Shifting Economic Landscapes

Both the Pound and the US Dollar are currently weighed down by expectations of interest-rate cuts from their respective central banks. This creates a unique environment within the foreign exchange market, where traders are attempting to evaluate which economy may soften more quickly and how each central bank may respond.

For the Pound, domestic pressures such as softer labour data and the government’s fiscal strategy contribute to uncertainty. For the Dollar, global investors are closely watching whether the Federal Reserve will confirm the expectations that markets have already priced in.

Because both currencies face similar challenges, the movement between them may remain narrow until clearer signals emerge. However, economic surprises from either side could quickly shift the balance.

Investor Sentiment and the Road Ahead

With several important announcements scheduled in the coming days, traders are preparing for a week marked by caution and quick reactions. Economic data from both the UK and the US will play significant roles in shaping expectations about future policy decisions.

If upcoming reports suggest further cooling in either economy, it may strengthen the case for more aggressive support measures. On the other hand, any signs of resilience could delay anticipated policy moves and shift market sentiment.

For now, the environment remains one of careful observation, with investors weighing incoming information against the broader backdrop of global economic uncertainty.

Final Summary

The Pound Sterling begins the week under pressure as markets prepare for potential interest-rate cuts from the Bank of England. Softer UK economic data and recently announced tax increases contribute to the currency’s subdued performance. Meanwhile, the US Dollar also weakens as investors expect the Federal Reserve to ease policy soon. A series of upcoming US economic releases, including employment and manufacturing data, will be key for market direction. With uncertainty surrounding both economies, traders remain cautious as they wait for clearer signals from policymakers on each side of the Atlantic.

USDCAD edges higher past 1.3950 as strong Canadian GDP fails to cap momentum

The USD/CAD currency pair started the week with moderate gains, moving near the 1.3980 level during Monday’s Asian session. While this rise reflects a partial recovery from earlier losses, the broader outlook for the pair is shaped by evolving expectations around economic policy in both the United States and Canada. With traders watching upcoming US manufacturing data and reassessing central bank paths, the pair’s direction will depend on shifting sentiment rather than strong momentum from either side.

US Dollar Softens as Rate-Cut Expectations Grow

The US Dollar faces pressure as expectations build for the Federal Reserve to cut interest rates at its upcoming policy meeting. Recent remarks from Fed officials have leaned toward a more cautious and less restrictive stance, especially in light of several weaker US economic indicators. This has encouraged markets to anticipate an easier policy path in the near term.

USDCAD is moving in an uptrend channel, and the market has reached the higher low area of the channel

Traders are assigning a high probability to a 25-basis-point reduction at the Fed’s December meeting. This shift in expectations has made the Dollar more vulnerable, allowing the Canadian Dollar to gain some footing despite mixed broader market sentiment. With the US economy losing steam in key areas, investors are waiting for fresh clues from the latest ISM Manufacturing PMI report, due later on Monday. That data may help determine whether the recent softening in the Dollar will continue.

Impact of Kevin Hassett’s Potential Fed Nomination

Another factor weighing on the US Dollar is the possibility of Kevin Hassett, a White House economic adviser, becoming the next Federal Reserve chair. Hassett is widely viewed as favoring a more accommodative policy approach. His stance aligns with the administration’s interest in encouraging faster and deeper rate cuts to support economic growth.

The prospect of a dovish leader at the helm of the Fed adds to market expectations that the central bank could move toward a longer cycle of reduced borrowing costs. For currency markets, this translates into added pressure on the Dollar, as investors tend to favor currencies backed by stronger or steadier policy paths. Until the nomination is confirmed, traders are likely to stay alert to any signals from policymakers or the White House that could shift the tone.

Canadian Dollar Finds Support in Stronger GDP Results

While the US faces increasing speculation around policy easing, Canada enters the week with fresh economic data that exceeded expectations. Statistics Canada reported that the country’s Gross Domestic Product expanded at an annualized rate of 2.6% in the third quarter. This marks a sharp rebound from the previous quarter’s contraction and significantly surpasses earlier forecasts.

The stronger performance gives the Bank of Canada more breathing room as it navigates its own rate-cutting cycle. The unexpected strength in GDP has led markets to scale back assumptions that the central bank will make additional cuts in the near term. This shift supports the Canadian Dollar, providing a counterbalance to the broader global uncertainty that often influences the Loonie, especially given Canada’s reliance on trade and natural resources.

A Clear Rebound for Canada’s Economy

The latest figures signal that domestic activity in Canada is holding up better than analysts anticipated. After a weak second quarter, the third-quarter rebound suggests that consumer spending, production, and investment all contributed to renewed momentum. This improvement helps ease concerns about a potential prolonged slowdown and strengthens the view that Canada may maintain more stable economic footing heading into the coming months.

For currency traders, this means the Canadian Dollar has a firmer base compared to earlier expectations. With the Bank of Canada less pressured to accelerate rate cuts, the CAD may continue to find underlying support, even if global risk sentiment remains mixed.

How Both Central Banks Shape the USD/CAD Outlook

The USD/CAD pair now sits at the intersection of two contrasting economic narratives. In the United States, softer data and a rising likelihood of policy easing are creating downward pressure on the Dollar. At the same time, Canada’s stronger-than-expected GDP performance is giving the Loonie a slight advantage, lifting market confidence in the currency.

However, the path ahead will depend heavily on new economic releases and policy signals. The Fed’s upcoming decision and guidance will likely have the largest immediate effect, as markets attempt to determine whether the central bank will confirm the expected rate cut or take a more cautious approach. Any shift in tone could quickly influence the Dollar’s performance.

Key Factors to Watch

-

US economic indicators: Manufacturing data, labor statistics, and inflation trends will play major roles in shaping upcoming policy decisions and currency movements.

-

Fed leadership news: Any confirmation or rejection of Hassett’s potential nomination could shift market expectations.

-

Bank of Canada policy direction: While the latest GDP numbers reduce pressure on the BoC, future data could still influence its policy stance.

Summary

The early-week gains in USD/CAD reflect a modest recovery for the US Dollar, but underlying momentum remains limited as markets prepare for potential rate cuts by the Federal Reserve. Expectations for easier US monetary policy, combined with speculation about dovish leadership at the Fed, are weighing on the Dollar’s broader appeal.

Meanwhile, Canada’s stronger-than-projected GDP growth boosts confidence in the Loonie, reducing expectations of further near-term easing by the Bank of Canada. These contrasting trends set the stage for a cautious but dynamic trading environment. As investors monitor upcoming economic reports and policy signals, the USD/CAD pair is likely to remain sensitive to even small shifts in sentiment across both economies.

EURJPY drops with Yen gaining strength on mounting BoJ hike speculation

EUR/JPY has moved lower at the start of the week, reflecting a clear change in investor sentiment. The pair’s retreat toward 180.50 comes as the Japanese Yen gains strength once again, helped by rising expectations that Japan may soon take a further step toward normalizing its monetary policy. Fresh comments from Bank of Japan Governor Kazuo Ueda have renewed market focus on Japan’s rate outlook and encouraged traders to reposition toward the Yen.

BoJ Signals Keep the Yen Supported

Governor Ueda noted that the Bank of Japan is prepared to raise interest rates if the economy and inflation continue to align with its medium-term forecasts. He highlighted that confidence in the baseline scenario for price growth is improving. These comments were enough to push Japanese government bond yields to their highest levels in years, reinforcing the belief that a policy shift is coming.

EURJPY is moving in an uptrend channel, and the market has reached a higher high area of the channel

The stronger yields point to a narrowing difference between Japanese returns and those offered in other large economies. As this gap shrinks, the Yen becomes more attractive to global investors. This dynamic places natural downward pressure on EUR/JPY, especially at a time when risk appetite in broader markets remains fragile. When sentiment turns cautious, safe-haven currencies like the Yen attract even more attention, adding to the momentum already underway.

The Euro’s Support Is Present, but Limited

While the Yen is benefiting from renewed optimism about Japan’s economic path, the Euro is not entirely without support. Many investors believe the European Central Bank has reached a stable point in its policy direction. Recent remarks from ECB President Christine Lagarde suggest that interest rates are at a level deemed appropriate for current economic conditions. Other policymakers, including Joachim Nagel, have echoed the view that the existing stance remains suitable.

However, this stability does not carry the same weight as the growing expectations surrounding the Bank of Japan. The Euro’s support is steady but has yet to spark any major upside interest, especially against a strengthening Yen.

What to Watch in the Eurozone

The next key event for the Euro is Tuesday’s release of the latest inflation readings, measured through the Harmonized Index of Consumer Prices (HICP). Forecasts suggest headline inflation may rise by 2.2% year over year in November, with core inflation expected at around 2.5%.

A reading that comes in above expectations could help the Euro regain some footing. Stronger inflation would boost the argument for the ECB to maintain higher borrowing costs for longer, reducing the appeal of monetary easing anytime soon. This scenario would offer some relief to the Euro and potentially slow the pace of its decline against the Yen.

How Market Caution Is Shaping Currency Moves

Broader market sentiment also plays a role in the pair’s movement. Investors are currently showing a preference for safer assets as caution spreads through global equity markets. The Yen often benefits during such periods because it is traditionally viewed as a protective asset during uncertain times.

This cautious environment amplifies the impact of any policy signals coming from the Bank of Japan. With expectations of tightening rising and risk appetite falling, the Yen gains support from multiple directions. This combination makes it more difficult for the Euro to find strong ground, particularly when its own backing is driven more by stability than by the promise of policy change.

Near-Term Outlook for EUR/JPY

The trend appears tilted in favor of the Yen for now. With repeated indications from BoJ officials that a tightening phase is approaching, the currency continues to gather momentum. Unless new developments emerge that significantly change the outlook for the Euro or shift global risk sentiment, the path ahead looks challenging for EUR/JPY.

Investors will watch upcoming data closely, especially the Eurozone inflation figures. Even so, unless the Euro receives a meaningful catalyst, the overall bias remains aligned with Yen strength. The backdrop of potential policy normalization in Japan, combined with a careful and cautious market mood, keeps pressure on the pair.

Summary

EUR/JPY is feeling the weight of a stronger Yen as expectations build around Japan’s potential move toward higher interest rates. Governor Ueda’s remarks have boosted confidence in future tightening, lifting Japanese bond yields and giving the Yen renewed momentum. Although the Euro is supported by the ECB’s steady message, it lacks the compelling narrative that currently favors the Yen. With investors leaning toward safe-haven assets and upcoming Eurozone data yet to provide a decisive push, the near-term outlook continues to favor Yen strength and leaves EUR/JPY under pressure.