The latest minutes from the U.S. Federal Reserve’s January meeting are drawing attention from economists, investors, and everyday borrowers alike. Many people want to understand why the central bank decided to hold interest rates steady and what might happen next.

At the heart of the discussion is a delicate balancing act. The Fed is trying to control inflation while also protecting the job market. These goals do not always move in the same direction. As we look ahead to 2026, the big question is how these decisions will shape mortgage rates and housing affordability.

Why the Federal Reserve Chose to Pause

During its January 16–17 meeting, the Federal Reserve decided to keep its key interest rate unchanged. After cutting rates in December, policymakers agreed that it was time to pause and observe how the economy develops.

Fed Chair Jerome Powell explained that there was broad support for holding rates steady. This was a change from December, when officials were divided. Some members wanted deeper cuts, while others preferred no cuts at all. By January, opinions had moved closer together.

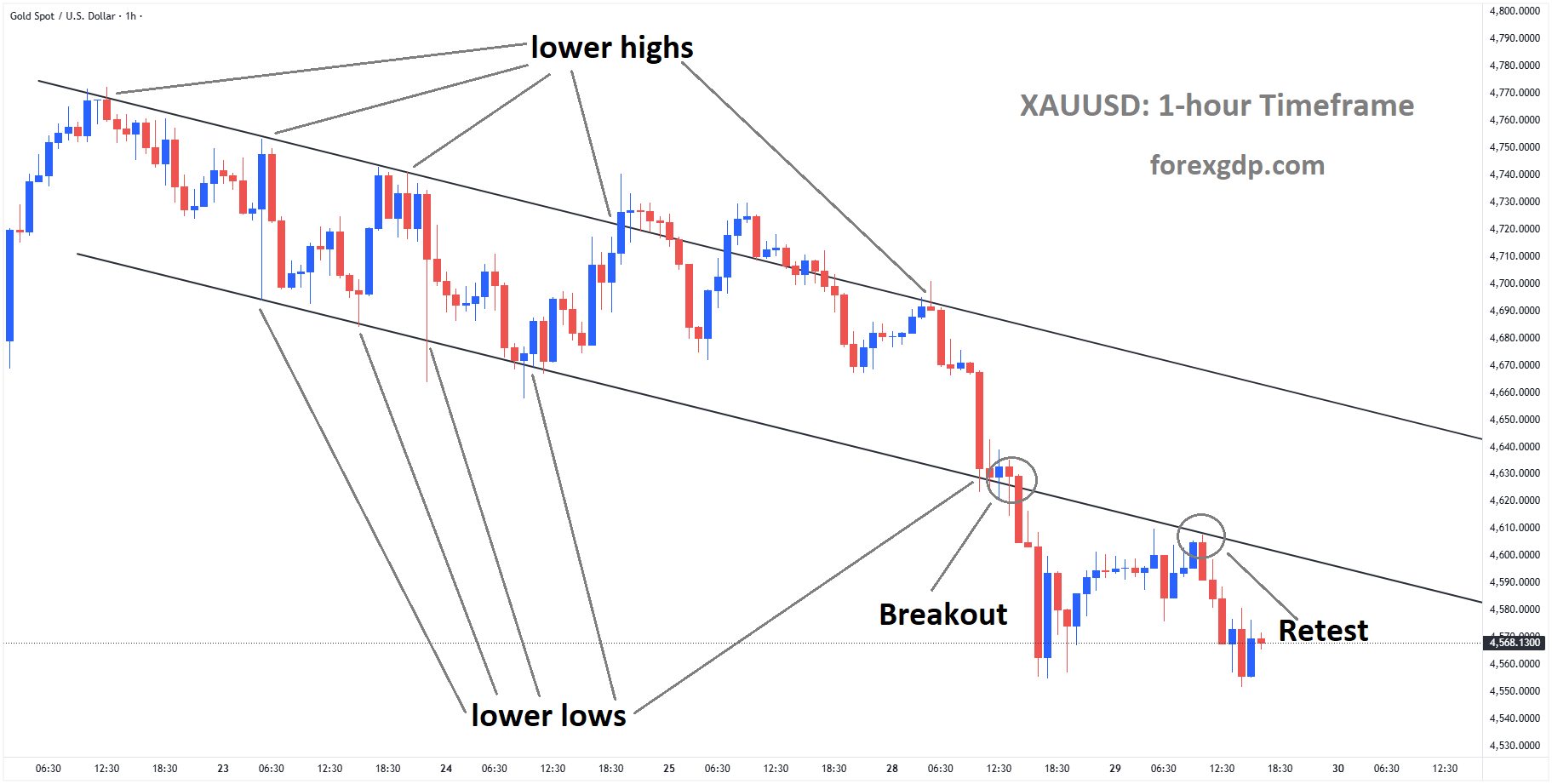

XAUUSD is moving in an Ascending Triangle pattern, and the market has rebounded from the higher low area of the pattern

Balancing Inflation and Employment

The Federal Reserve has two main goals:

-

Keep inflation around 2% per year

-

Support maximum employment

Recently, inflation has remained above the Fed’s target, while the job market has shown signs of softening. In past months, this created tension. Raising rates can help lower inflation, but it can also slow hiring. Cutting rates can support jobs but may risk higher inflation.

Powell noted that these risks appear to be easing somewhat. The danger of inflation rising sharply has declined, and the risk of a sudden jump in unemployment has also lessened. Still, inflation progress has been slower than many hoped.

What Could Lead to More Rate Cuts?

Some Fed officials believe that if inflation continues to cool in the coming months, additional rate cuts could be justified later this year. Others are more cautious. They want to see clear and lasting signs that inflation is truly under control before making further moves.

Another factor influencing inflation is trade policy. High import tariffs have pushed up costs for businesses, and many companies have passed those costs on to consumers. While officials believe the biggest impact from tariffs may be behind us, they are still watching closely.

For now, the Fed’s message is simple: wait and see.

Why Mortgage Rates Don’t Always Follow the Fed

Many people assume that when the Federal Reserve cuts interest rates, mortgage rates automatically fall as well. In reality, it is more complicated.

Mortgage rates are influenced by long-term market forces, especially the 10-year Treasury yield and the market for mortgage-backed securities. These are shaped by investor expectations about inflation, economic growth, and overall stability.

After the Fed’s December rate cut, mortgage activity actually declined. Some investors interpreted the Fed’s comments as a sign that the rate-cutting cycle might be nearing its end. As a result, mortgage rates did not fall as much as some borrowers expected.

This shows that mortgage rates do not move in perfect sync with Fed decisions.

Expert Predictions for Mortgage Rates in 2026

Financial experts have shared a range of views about what to expect in 2026. While there is no single consensus, most agree that dramatic changes are unlikely.

Limited Rate Relief Ahead

Ralph DiBugnara, a real estate expert and president of Home Qualified, does not expect major rate cuts next year. He points out that the December rate cut was small and not unanimously supported by Fed members. This lack of full agreement suggests that policymakers are cautious.

According to DiBugnara, affordability challenges will likely continue unless the Fed takes a more aggressive approach. He believes officials are still trying to fully understand what is driving inflation, especially with newer factors like tariffs affecting consumer spending.

XAGUSD has broken the descending channel in upside

In his view, significant relief for homebuyers may not come quickly.

Rates Higher Than Many Hope

Jeffrey M. Ruben, president of WSFS Home Lending at WSFS Bank, expects mortgage rates to remain higher than many borrowers would prefer. However, he does not see them moving far outside historical norms.

Before the pandemic, mortgage rates were typically just under 5%. Ruben believes that level may represent a more normal balance for the market. He does not expect a return to the ultra-low rates seen during the pandemic years.

Recent Fed rate cuts were partly aimed at supporting the labor market. Still, ongoing inflation pressures, trade uncertainty, and slow wage growth have kept investors cautious. That caution has helped keep longer-term rates elevated.

A Modest Drop Could Unlock Affordability

Michael Merritt of BOK Financial sees cautious optimism for 2026. Many economic models suggest mortgage rates could move slightly lower. Even a modest decline could make a meaningful difference for buyers.

GBPUSD is moving in a descending triangle pattern, and the market has rebounded from the support area of the pattern

The National Association of Realtors has estimated that if rates dip below 6%, millions more households could afford a median-priced home. Lower rates could also encourage refinancing activity, bringing more movement into the housing market.

However, forecasts remain sensitive to changes in economic data, especially movements in Treasury yields.

Mid-to-Upper 5% Range Possible

Darren Tooley, a senior loan officer at Cornerstone Financial Services, believes rates may fall below 6% and remain in the mid-to-upper 5% range for much of 2026.

He stresses that mortgage rates depend heavily on investor confidence and long-term inflation expectations. The difference between Treasury yields and mortgage rates remains higher than historical averages, which has also affected borrowing costs.

USDJPY reached the resistance area of the box pattern

Tooley highlights several key factors to watch:

-

Monthly job creation reports

-

Wage growth trends

-

The impact of tariffs on inflation

-

Overall economic strength

He also reminds borrowers that rates rarely move in a straight line. Short-term increases are possible, even in a broader downward trend.

Key Economic Factors Shaping 2026

Looking ahead, several major forces will shape interest rates and mortgage rates:

Inflation Trends

If inflation continues to decline steadily, the Federal Reserve may feel more comfortable cutting rates further. But if inflation stalls or rises again, the Fed may keep rates steady for longer.

Labor Market Strength

A strong job market supports consumer spending, but too much strength can keep inflation high. On the other hand, weak job growth could push the Fed to lower rates more quickly.

BTCUSD is moving in an ascending channel, and the market has rebounded from the higher low area of the channel

Trade Policy and Tariffs

Tariffs have added cost pressures to the economy. How these policies evolve will influence inflation and, in turn, interest rate decisions.

Wage Growth and Affordability

Slow wage growth limits how much homebuyers can afford. Even if mortgage rates decline slightly, affordability challenges could remain if incomes do not keep pace.

What This Means for Homebuyers and Borrowers

For people considering buying a home or refinancing, the outlook suggests modest changes rather than dramatic shifts.

Mortgage rates in 2026 are unlikely to return to the historic lows seen during the pandemic. At the same time, most experts do not expect sharp increases either. Instead, the market may settle into a more stable range, with gradual ups and downs along the way.

Borrowers should pay attention to broader economic signals rather than focusing only on Fed announcements. Inflation reports, job data, and investor sentiment all play a role in determining mortgage costs.

Final Thoughts

The Federal Reserve’s decision to pause interest rates reflects a careful approach to a complex economy. Inflation is easing but remains above target. The job market is cooling but not collapsing. Policymakers are watching closely before making their next move.

For mortgage rates in 2026, experts generally expect moderate improvement but not a dramatic return to ultra-low borrowing costs. Economic forces such as inflation, employment, tariffs, and wage growth will continue to shape the path forward.

Homebuyers and homeowners should prepare for a market defined by gradual changes rather than sudden swings. Patience, careful planning, and attention to economic trends will be essential in navigating the year ahead.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!