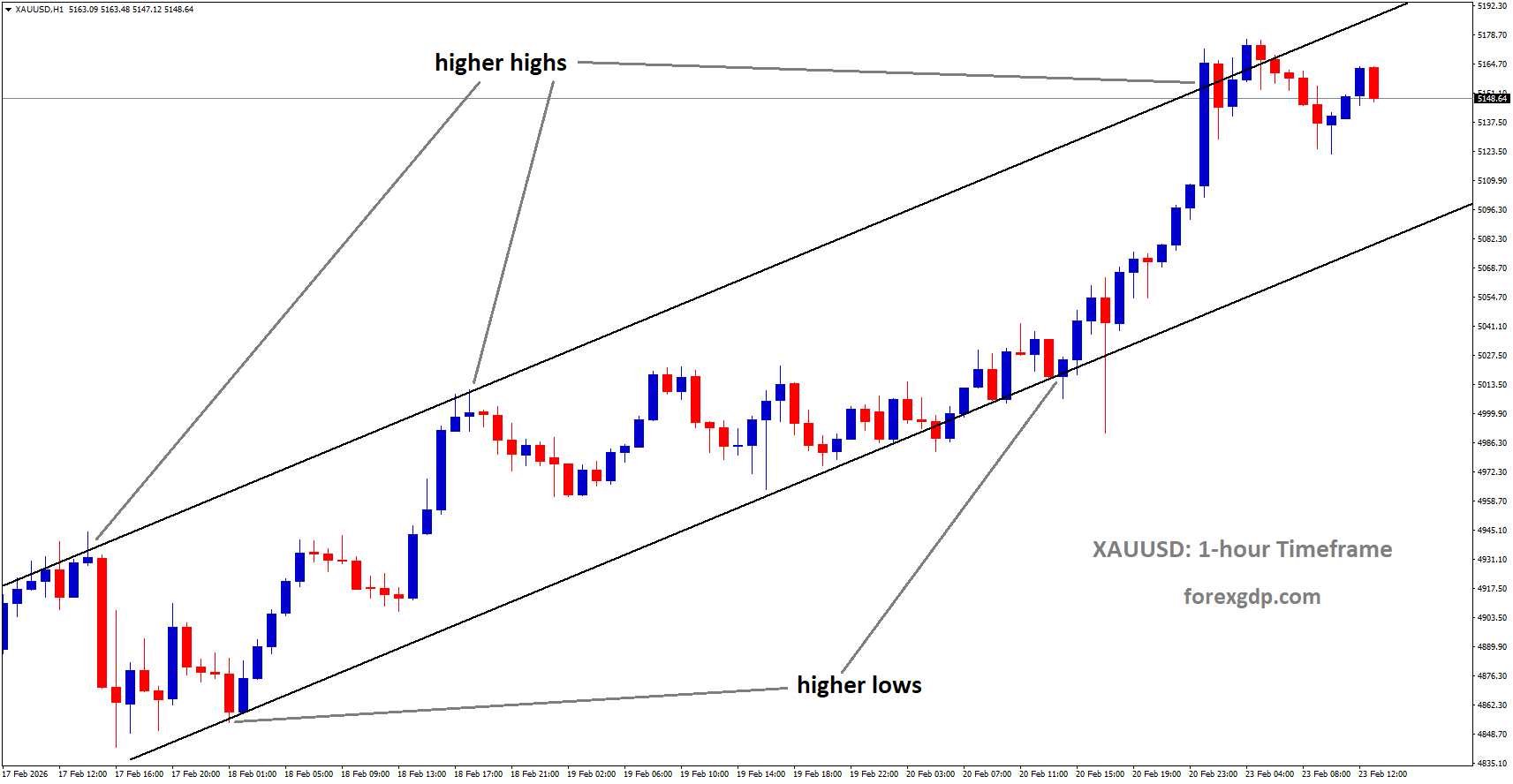

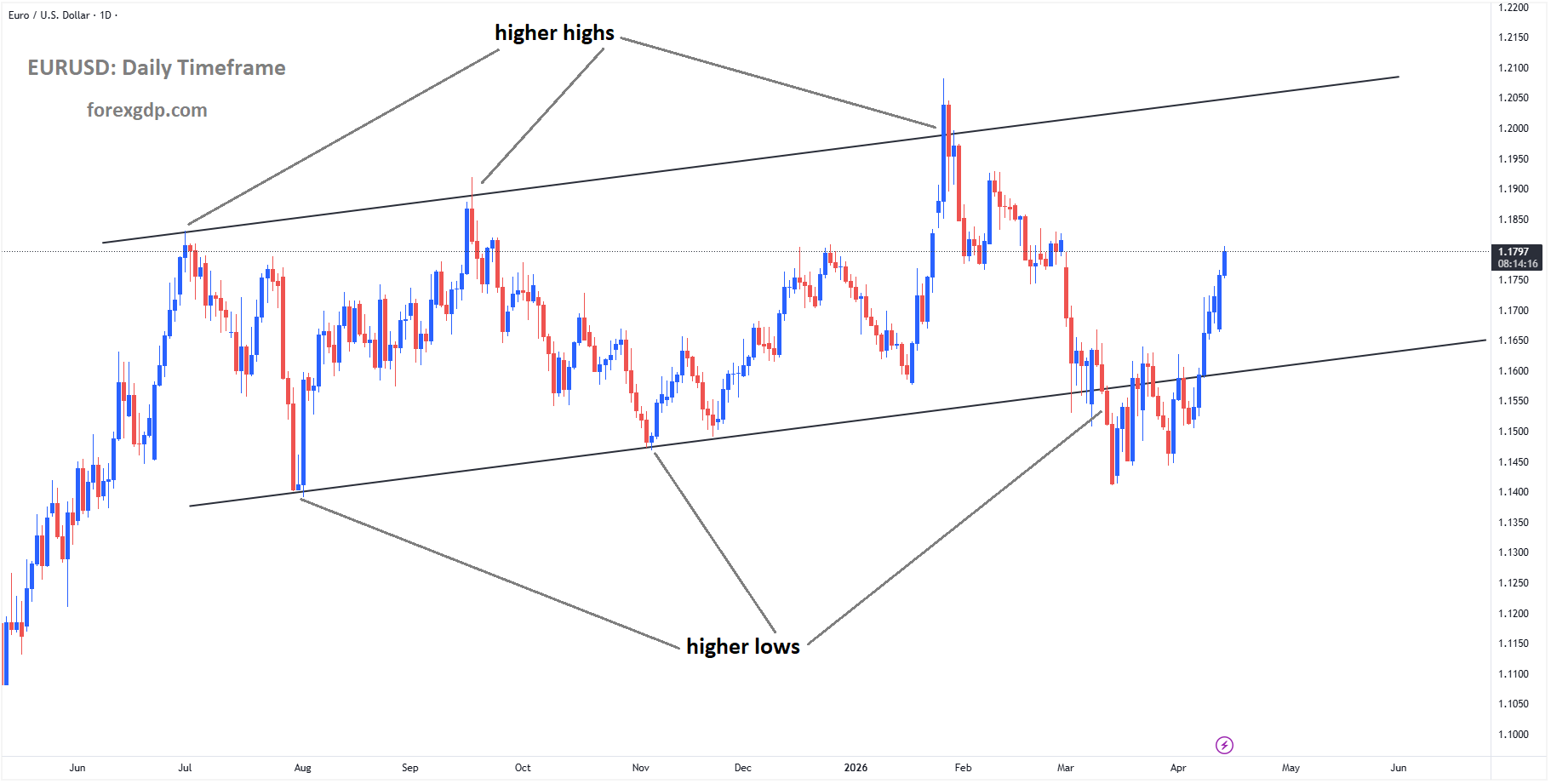

EURUSD is moving in a box pattern

EURUSD Gains Momentum as Markets Brace for High-Impact US Employment Report

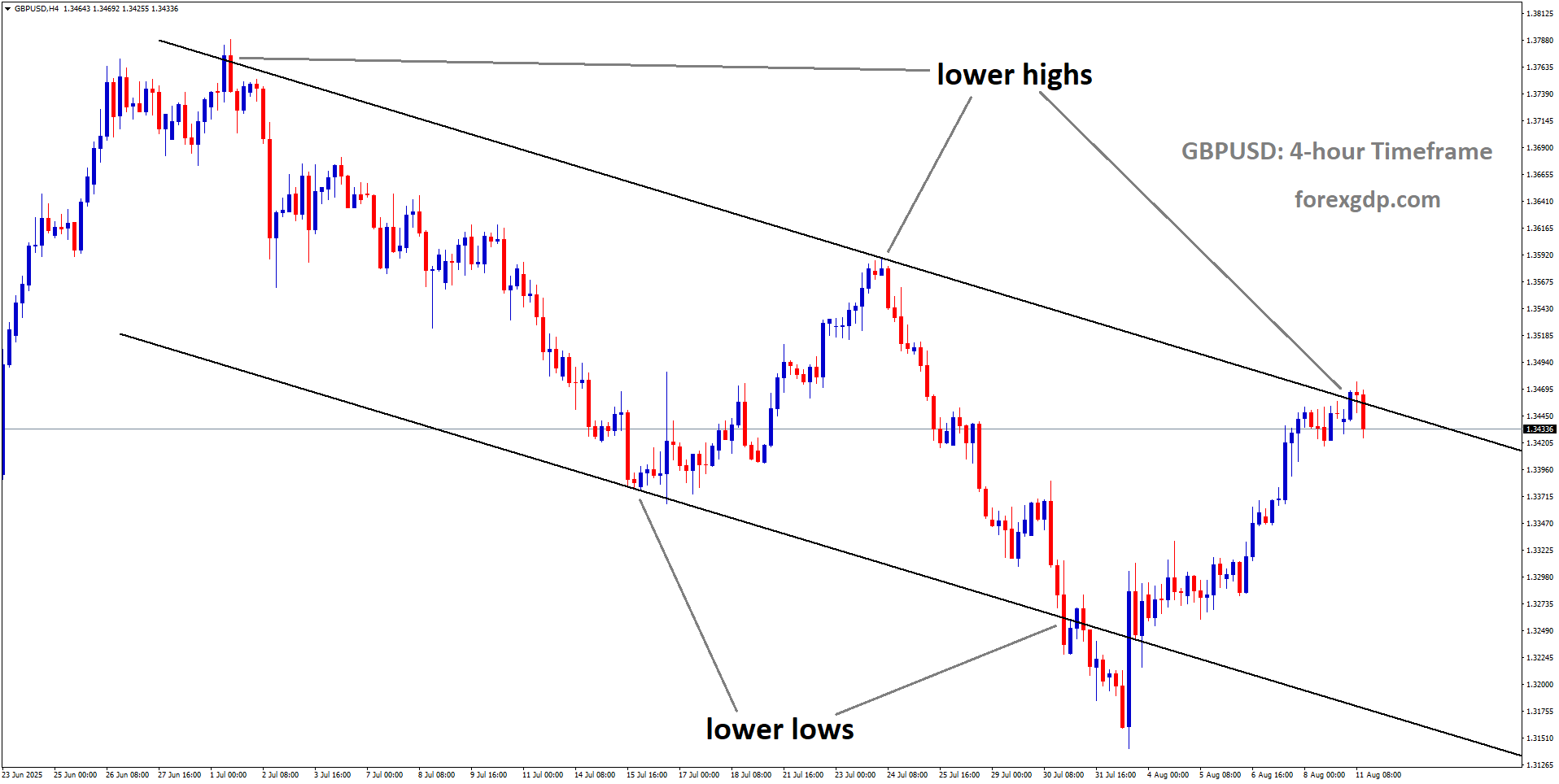

GBPUSD Under Pressure Ahead of NFP Release with Rising Geopolitical Risks in Focus

The British Pound gained modest support against the US Dollar on Friday, with the GBP/USD currency pair moving closer to the 1.3430 level during the early European trading session. While the pair managed to recover some ground during the day, broader market concerns continue to limit stronger gains.

GBPUSD is breaking the lower high area of the symmetrical triangle pattern

Investors remain focused on growing geopolitical tensions in the Middle East, as well as an important US employment report scheduled for release later in the day. Both developments are expected to play a major role in shaping market sentiment and influencing the direction of major currencies.

GBP/USD Sees Limited Recovery Amid Global Uncertainty

The Pound showed some resilience against the US Dollar during Friday’s trading session, allowing GBP/USD to edge higher. However, despite this rebound, the pair remains on track for a second consecutive week of losses.

Market participants are becoming increasingly cautious due to ongoing instability in the Middle East. Heightened geopolitical risks often push investors toward safer assets, reducing demand for currencies that are considered more sensitive to market sentiment. The British Pound is often viewed as one of these risk-sensitive currencies, making it vulnerable during periods of uncertainty.

As a result, any gains in GBP/USD have remained relatively restrained, with traders reluctant to take aggressive positions before receiving more clarity on both geopolitical developments and upcoming economic data.

Middle East Tensions Continue to Influence Financial Markets

One of the key factors affecting investor sentiment is the ongoing conflict involving Iran, Israel, and regional groups in the Middle East.

Efforts by US President Donald Trump to reduce tensions and move forward with a peace agreement involving Iran have recently encountered fresh challenges. Reports indicate that Hezbollah, a group backed by Iran, rejected a proposed ceasefire agreement in Lebanon. At the same time, Israel stated that it would not remove its military presence from the country.

These developments have raised concerns that the conflict could become more complicated and difficult to resolve.

Iranian Foreign Minister Abbas Araghchi also emphasized that communication channels with the United States remain open. However, he warned that any Israeli attack on Beirut could trigger a broader escalation and potentially restart direct tensions involving both Iran and the United States.

Safe-Haven Demand Benefits the US Dollar

Whenever geopolitical risks increase, investors often move money into assets considered safer during uncertain times. The US Dollar typically benefits from this behavior because of its status as one of the world’s leading reserve currencies.

As concerns about the Middle East continue, demand for safe-haven assets has strengthened. This trend has supported the US Dollar while placing additional pressure on currencies such as the British Pound.

The lack of significant progress in peace negotiations between Washington and Tehran has further contributed to market caution. Until there is greater confidence that tensions are easing, traders may continue favoring defensive positions.

Mixed Signals From Bank of England Officials

Comments from senior Bank of England policymakers have also attracted attention this week, adding another layer of uncertainty for the Pound.

Megan Greene Highlights Inflation Risks

Bank of England policymaker Megan Greene suggested earlier in the week that there could be a stronger case for higher interest rates if the conflict involving Iran continues. According to Greene, prolonged geopolitical tensions could lead to broader price increases across the economy.

Higher inflation typically increases pressure on central banks to tighten monetary policy. If interest rates rise, a currency can become more attractive to investors because of the potential for improved returns.

Greene’s remarks therefore provided some support for the idea that UK borrowing costs could remain elevated for longer than previously expected.

Andrew Bailey Takes a More Cautious Approach

Despite Greene’s comments, Bank of England Governor Andrew Bailey offered a more cautious assessment.

Bailey indicated that the central bank is not rushing to increase interest rates while uncertainty surrounding the Middle East remains high. He also pointed to the relatively weak pace of economic growth in the United Kingdom as a factor supporting a more measured approach.

His comments were viewed as more dovish by markets, suggesting policymakers may prefer to wait for clearer economic signals before making any significant changes to monetary policy.

The difference in views among Bank of England officials has created uncertainty around the future direction of UK interest rates, making it harder for the Pound to build sustained momentum.

US Employment Report Becomes Main Market Focus

While geopolitical events remain important, traders are now turning their attention to the latest US labor market data.

The May employment report is expected to provide valuable insights into the health of the American economy and could significantly influence expectations for future Federal Reserve policy decisions.

Economists are forecasting that the US economy added around 85,000 jobs during May. Meanwhile, the unemployment rate is expected to remain unchanged at 4.3%.

Employment figures are closely monitored because they offer a snapshot of economic strength. Strong hiring typically signals a healthy economy, while weaker job growth can raise concerns about slowing activity.

How the Jobs Report Could Affect GBP/USD

The outcome of the employment report may determine the next move for the US Dollar and, by extension, GBP/USD.

If job creation exceeds expectations and unemployment remains stable, confidence in the US economy could strengthen. This would likely support the US Dollar and potentially limit gains in the Pound.

On the other hand, if the report shows weaker-than-expected hiring or signs of labor market softness, investors may reassess the outlook for the US economy. Such a scenario could weaken the Dollar and provide support for GBP/USD.

Because of the report’s importance, many traders are expected to remain cautious until the data is released.

Summary

The GBP/USD pair managed to post modest gains during Friday’s European session, but broader market concerns continue to weigh on sentiment. Escalating tensions in the Middle East, uncertainty surrounding US-Iran negotiations, and increased demand for safe-haven assets have limited the British Pound’s upside potential.

At the same time, mixed messages from Bank of England officials have created uncertainty about the future path of UK interest rates. Investors are now waiting for the US employment report, which is expected to provide crucial clues about the strength of the American economy and could shape the near-term direction of both the US Dollar and GBP/USD.