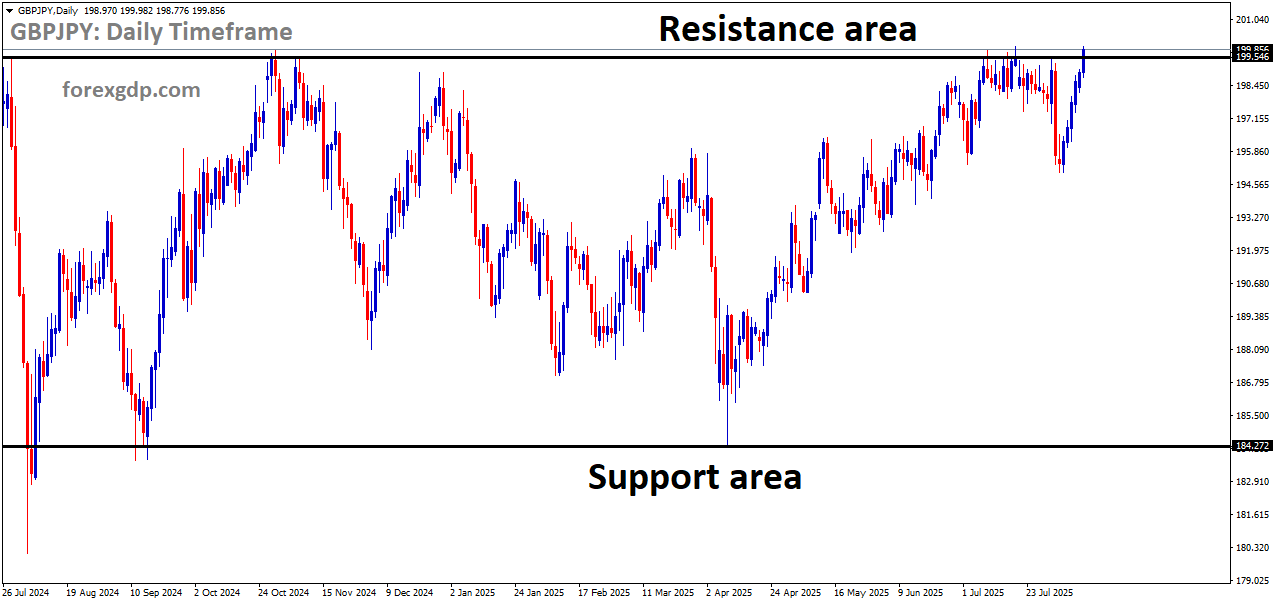

GBPJPY is moving in a box pattern, and the market has reached the resistance area of the pattern

Daily Forex Trade Setups Aug 12, 2025

Stay on top of market trends with our Daily Forex Trade Setups (Aug 12, 2025)

GBPJPY Gains Momentum Following Positive UK Employment Report

The British Pound has been on a winning streak lately, holding firm near its highest levels of the year. After six straight days of gains, the currency continues to ride a wave of positive momentum, largely driven by unexpectedly strong employment data from the UK. For traders, investors, and anyone keeping an eye on the economy, these numbers are a welcome sign that the job market is still resilient, even as global economic uncertainty looms.

UK Employment Figures Deliver a Pleasant Surprise

Recent figures from the UK Office for National Statistics painted a picture of a stable, if not slightly improving, job market. Unemployment remained steady at 4.7% in the three months leading up to July, matching analysts’ expectations. But what really caught attention was the drop in unemployment claims.

In July, the number of people requesting unemployment benefits fell by 6,200. Even more striking, June’s previous estimate — which initially suggested a sharp increase in claims — was revised to reveal a notable decline instead. These updates flipped market sentiment, as most forecasts had expected a rise in jobless claims rather than a fall.

The drop in claims is a signal that the labor market isn’t cooling as quickly as some had feared. While net employment did dip slightly by 8,000, the loss was far smaller than predicted. This follows a sharper drop in June, but the softer decline suggests that the labor market might be stabilizing rather than sliding into trouble.

Why the Bank of England Is Likely to Hold Steady

The Bank of England (BoE) has been in a tough spot lately, balancing inflation concerns with the need to support economic growth. The latest employment numbers strengthen the case for keeping interest rates steady rather than rushing to cut them.

At its last meeting, the BoE’s monetary policy committee showed clear resistance to rate cuts, with several members arguing that more time is needed to see how the economy responds to previous policy moves. These fresh employment figures give them even more reason to wait before making any major shifts.

Another factor in play is wage growth. While still positive, wages in the UK have been rising at their slowest pace in nearly a year — up 4.6% in the three months to June, compared to 5% previously. Slower wage growth may help ease inflationary pressures without requiring immediate intervention from the central bank.

In short, the combination of steady unemployment, fewer jobless claims, and moderating wage growth creates a case for patience. The BoE can afford to watch and wait rather than rush into rate cuts that might not be necessary yet.

A Tale of Two Currencies: Pound vs Yen

While the Pound is enjoying strength, the Japanese Yen is facing a much rougher patch. Recent comments from the Bank of Japan (BoJ) have dampened investor enthusiasm for the currency.

The BoJ has maintained its stance on gradually tightening monetary policy, but a combination of trade concerns and uncertainty over the impact of US tariffs has created hesitation. Market watchers now believe the BoJ will likely delay further rate hikes in the near term.

This softer outlook for the Yen adds to the Pound’s relative appeal. Currency traders often compare opportunities across major markets, and when one central bank appears cautious while another holds a steady, confident line, the stronger currency naturally attracts more interest.

What This Means for Businesses and Consumers

A stronger Pound can have different effects depending on your perspective. For businesses that rely on imported goods and services, it’s generally a good thing — a more valuable currency means imports cost less. For holidaymakers traveling abroad, it boosts spending power.

However, for exporters, a rising Pound can be a challenge, as it makes their goods more expensive for foreign buyers. This could put some pressure on UK manufacturers and businesses that rely heavily on overseas sales.

GBPJPY is moving in an uptrend channel

For everyday consumers, the current job market stability is encouraging. Steady employment rates suggest that the economy isn’t in immediate danger of a downturn, which can help maintain consumer confidence. That said, the pace of wage growth will be something to watch, as it affects how far people’s paychecks go in the face of inflation.

Final Summary

The Pound’s current strength is being fueled by solid UK employment figures and a supportive economic backdrop. With unemployment steady, jobless claims falling, and wage growth slowing just enough to ease inflation worries, the Bank of England has room to keep interest rates steady for now. Meanwhile, the Japanese Yen’s weaker position gives the Pound an extra boost in global currency markets.

While this is positive news for importers and travelers, exporters may feel the pinch. For consumers, the resilience of the job market offers reassurance in uncertain times, even as broader economic challenges remain. All eyes will be on future employment data and central bank moves to see whether this winning streak for the Pound can continue.

EURUSD Gains Ground as Traders Await Inflation Clues from the US

The euro has been holding its ground after a recent pullback, fueled by renewed optimism over potential peace negotiations in Ukraine and a cautious wait for key US inflation data. Traders and investors are balancing geopolitical developments with economic indicators, shaping the market’s mood as the week unfolds.

Geopolitical Hopes Lifting the Euro

The European currency has found some strength following news that suggested possible progress in peace discussions between Russia and Ukraine. Reports indicated that Russian President Vladimir Putin had floated the idea of a ceasefire in exchange for territorial concessions in Eastern Ukraine.

EURUSD is moving in an Ascending channel, and the market has rebounded from the higher low area of the channel

While Ukrainian President Volodymyr Zelenskyy rejected the proposal outright, the very fact that such talks are on the table has stirred hope in the market for some form of compromise or pathway toward ending the conflict. Even without concrete results, such developments often help ease investor anxiety, especially in Europe, where the war’s impact has been felt deeply.

Adding to the anticipation, a scheduled meeting between Putin and US President Donald Trump in Alaska later this week has caught traders’ attention. Although it’s unclear if the talks will lead to any breakthrough, markets tend to react positively when diplomatic efforts gain visibility. For now, this geopolitical backdrop has given the euro a mild lift while the US dollar remains subdued.

US Inflation Data: The Week’s Big Market Mover

While geopolitics is providing one side of the narrative, the other major focus is on US economic data—specifically the Consumer Price Index (CPI) report for July. This data is critical because it offers fresh clues about inflation trends in the United States and, in turn, the Federal Reserve’s next policy moves.

Why the CPI Report Matters

The CPI measures how prices for everyday goods and services are changing over time. If inflation comes in hotter than expected, it could signal that the Federal Reserve might delay or scale back any interest rate cuts, which typically strengthens the US dollar. On the other hand, a softer reading might encourage the Fed to act sooner to lower rates, putting downward pressure on the dollar and potentially supporting the euro.

Recent labor market data and public remarks from Fed policymakers have already fueled expectations that an interest rate cut might be on the table for September. However, a strong CPI reading could quickly shift those assumptions. This is why traders are on high alert—today’s report could set the tone for market direction in the coming weeks.

Global Trade Developments Adding to the Mix

In addition to geopolitical and inflation-related factors, the broader trade environment is also playing a role in market sentiment. The United States and China recently agreed to extend their trade truce for another 90 days, avoiding the implementation of steep reciprocal tariffs.

Although the extension was largely anticipated by investors and didn’t cause a major market swing, it has added a slight bearish bias to the US dollar. When tensions ease between the world’s two largest economies, safe-haven demand for the dollar tends to fade a bit. This is another factor that has indirectly supported the euro in recent sessions.

Calm Trading Conditions Before the Storm

The start of the week has been relatively quiet for most major currencies. The US Dollar Index, which measures the dollar against a basket of leading global currencies, has been holding steady after a mild rebound over the last two trading days.

With many traders adopting a wait-and-see approach ahead of the US CPI report, price movements have been limited. The absence of high volatility suggests that markets are storing up energy for a potentially sharp reaction once the inflation numbers are released.

Upcoming Central Bank Commentary

After the inflation report, investors will also be listening closely to speeches from Federal Reserve officials Thomas Barkin and Jeffrey Schmid. Both are known for their more hawkish views, meaning they tend to favor tighter monetary policy to keep inflation under control. Their comments could either reinforce or counter the market’s immediate reaction to the CPI data, making them another key point to watch today.

Eurozone Economic Outlook in the Spotlight

Across the Atlantic, the eurozone has its own set of economic updates to digest. The ZEW Economic Sentiment Survey is expected to reveal a further decline in confidence both across the euro area and in Germany, its largest economy. Persistent concerns about growth, energy prices, and geopolitical uncertainty have been weighing on sentiment for months.

However, the bigger test for the eurozone this week will be Thursday’s release of preliminary second-quarter Gross Domestic Product (GDP) figures. These numbers will show whether the region’s economy is maintaining momentum or sliding closer to stagnation. A strong reading could strengthen the euro’s position, while weaker-than-expected data might leave it more vulnerable to pressure from a stronger dollar.

What Traders Are Watching Next

Right now, the market is balancing multiple themes:

-

Geopolitical risks: Any signs of progress—or setbacks—in Ukraine peace talks could cause sudden swings in the euro.

-

US inflation trends: A stronger-than-expected CPI could boost the dollar, while a weaker number might support the euro.

-

Trade relations: Continued calm in US-China relations helps ease pressure on global markets, indirectly supporting risk-sensitive currencies.

-

Eurozone data: The upcoming GDP release will give investors a clearer picture of the region’s economic health.

Final Summary

The euro is currently benefiting from a combination of diplomatic hopes and cautious optimism ahead of critical US economic data. While peace talks in Ukraine remain uncertain, the mere possibility of progress is easing some geopolitical pressure. At the same time, traders are preparing for the US CPI release, knowing it could sharply influence the Federal Reserve’s interest rate path and the dollar’s strength.

In this environment, currency movements remain measured, with market participants carefully weighing every piece of news. Over the next few days, the interplay between US inflation figures, central bank commentary, and eurozone economic updates will likely determine whether the euro can extend its gains or faces renewed pressure. For now, the focus is on staying alert, watching the data, and being ready for the next market catalyst.

GBPUSD Pushes Upward as UK Employment Outlook Improves

The Pound Sterling (GBP) has found solid ground this week, moving higher against several major currencies after the release of encouraging UK employment figures. With fresh labor market data showing robust job creation, traders and investors have renewed confidence in the UK economy. This wave of optimism comes as the markets prepare for more important updates later in the week, including the UK’s Q2 GDP numbers and the latest US inflation report.

UK Labor Market Shows Impressive Strength

The latest numbers from the Office for National Statistics (ONS) revealed that the UK added 239,000 jobs in the second quarter of the year — a clear sign of strength in the country’s employment sector. This is a notable jump from the 134,000 jobs created in the three months ending May and a significant recovery from earlier periods when hiring was subdued.

One of the reasons for this earlier slowdown was the rise in employers’ social security contributions to 15%, which initially made businesses cautious about expanding their workforce. However, the recent data suggests that companies have adjusted and are now feeling more confident about taking on new staff.

GBPUSD is moving in a descending channel, and the market has reached the lower high area of the channel

The unemployment rate held steady at 4.7%, in line with expectations. Another positive sign came from the Claimant Count Change, which showed a drop of 6,200 in July, despite forecasts pointing to an increase. This decline means fewer people are claiming unemployment benefits, indicating an overall improvement in the labor market.

Wage Growth Sees a Slight Cooldown

While job creation is booming, wage growth has shown signs of slowing down slightly. The figures show that Average Earnings (excluding bonuses) rose at a steady 5% year-on-year, matching expectations. However, when bonuses were included, the growth rate eased to 4.6%, slightly below forecasts and the previous 5% reading.

This moderation in pay growth might be welcomed by the Bank of England (BoE), which is carefully watching wage trends as part of its strategy to manage inflation. Slower wage growth can reduce pressure on prices, making it easier for the central bank to maintain a balanced approach to interest rates.

Bank of England’s Cautious Approach Continues

The positive jobs report gives the Bank of England more breathing room to continue its “gradual and careful” approach to monetary policy. Just last week, the BoE decided to cut interest rates by 25 basis points to 4%, a move supported by a narrow majority of policymakers.

The strong employment figures are likely to reassure the central bank that the economy remains resilient, even as it navigates through a period of slower wage growth and controlled inflation pressures.

Key Events Ahead: GDP and US Inflation Data

While the jobs data has given the Pound a short-term boost, traders are now shifting their attention to the next big catalysts.

UK GDP Report

On Thursday, the UK will release its Preliminary Q2 Gross Domestic Product (GDP) figures, along with factory output data for June. These numbers will provide a clearer picture of how the economy is performing overall. Strong growth figures could further support the Pound, while any signs of weakness might dampen the recent momentum.

US Inflation Numbers

The other major focus for global markets this week is the US Consumer Price Index (CPI) report. Scheduled for release on Tuesday, the CPI data will reveal how inflation in the United States moved in July. Investors will be closely watching this to determine whether recent price increases are a temporary spike or part of a longer-term trend.

If US inflation rises more than expected, it could strengthen the US Dollar as traders anticipate that the Federal Reserve might delay interest rate cuts. On the other hand, softer inflation data could weaken the Dollar and give the Pound an additional lift.

Federal Reserve Signals and Global Trade Developments

In recent weeks, several Federal Reserve officials have indicated that they are more focused on the weakening labor market than on inflation risks. For example, Fed Governor Michelle Bowman has expressed support for gradually moving from restrictive monetary policy toward a more neutral stance. She also noted that recent employment numbers have reinforced her expectation of three interest rate cuts this year.

On the global trade front, there has been a positive development between the United States and China. Both countries have agreed to extend their tariff truce for another 90 days. China’s Commerce Ministry also announced measures to reduce non-tariff barriers for American companies and a temporary suspension of adding certain US firms to its “unreliable entities” list. This step has been seen as a sign of easing tensions, which could benefit global trade flows and investor confidence.

What This Means for the Pound Sterling

With the labor market showing clear strength, the Pound is enjoying a supportive environment. The combination of falling unemployment claims, steady job creation, and a stable unemployment rate points to a resilient UK economy. However, the slightly slower pace of wage growth might limit inflationary pressures, giving the BoE more flexibility in its policy decisions.

The upcoming GDP figures will be crucial in determining whether this momentum can continue. At the same time, the US CPI results could create volatility in the GBP/USD exchange rate, depending on how they influence expectations for Federal Reserve policy.

Final Summary

The UK’s latest jobs report has given the Pound Sterling a welcome lift, with employment numbers far exceeding expectations. Despite a slight slowdown in wage growth, the overall picture of the UK labor market is one of strength and resilience. The Bank of England is likely to take this as a sign that its measured approach to interest rates is working, especially as inflation pressures ease.

Looking ahead, attention will shift to the UK’s GDP release and the US inflation report, both of which have the potential to drive significant market moves. In the bigger picture, easing trade tensions between the US and China also add a layer of optimism to the global outlook.

For now, the Pound remains supported by solid economic fundamentals — but the next few days could determine whether this momentum builds further or faces a temporary setback.

USDJPY Holds Steady as Traders Brace for Key US Inflation Report

The Japanese Yen (JPY) has been moving in a tight range lately, caught between conflicting signals from the Bank of Japan (BoJ) and the US Federal Reserve (Fed). While some factors point toward a possible rate hike in Japan, others suggest the BoJ might hold off for now. On top of that, investors seem cautious, waiting for the release of the latest US inflation numbers before making their next move.

This combination of uncertainty and anticipation has kept the USD/JPY pair from making big moves, even though global markets are showing a generally positive tone. Let’s dive into what’s really going on behind the scenes.

USDJPY is moving in an uptrend channel

BoJ’s Mixed Signals Leave Yen Traders Unsure

Over the past week, the Japanese Yen hit a one-week low before bouncing back slightly. However, this recovery has been modest because the BoJ’s stance on interest rates is far from clear.

On one hand, the BoJ recently raised its inflation forecast, hinting at the possibility of a rate hike before the year ends. This would be a big shift from its long-standing ultra-loose monetary policy and could give the Yen a boost.

On the other hand, political uncertainty at home and concerns over Japan’s economic health are making investors wonder if such a move is realistic. Calls from opposition parties to increase government spending and cut taxes are adding another layer of complexity. Meanwhile, higher US tariffs could slow Japan’s economic momentum, making aggressive policy tightening less appealing.

Why the Yen Struggles in a Risk-On Market

In times of global uncertainty, the Yen is often seen as a safe-haven currency. But when investor confidence is high, demand for safe-haven assets usually drops—and that’s exactly what’s happening now.

Recent strength in global equity markets suggests that investors are feeling optimistic, even after the latest tariff announcements. This “risk-on” sentiment has weighed on the Yen, making it less attractive compared to other currencies, especially the US Dollar.

That said, the divergence between BoJ and Fed policies is helping to keep USD gains in check. While the BoJ may be leaning (slowly) toward a rate hike, the Fed is widely expected to start cutting rates in the coming months. In fact, markets are betting on at least two rate cuts by the end of the year, with the first possibly coming in September.

US Data Could Set the Tone for USD/JPY

Right now, traders are holding back from making big moves in USD/JPY because everyone’s waiting for the US Consumer Price Index (CPI) report. Inflation data is a key factor in shaping Fed policy decisions, and this release could either strengthen or weaken the case for upcoming rate cuts.

The anticipation comes after a disappointing US Nonfarm Payrolls report last week, which showed that job growth slowed more than expected. That data reinforced the view that the Fed might need to act sooner to support the economy.

In the meantime, the Yen’s direction could also be influenced by upcoming events, including speeches from Fed officials and other US economic data releases like the Producer Price Index (PPI) on Thursday. For Japan, the focus will be on its Preliminary Q2 GDP figures due on Friday, which will provide more clues about the country’s economic health.

Falling Real Wages Raise Concerns in Japan

Adding to the uncertainty, Japan’s inflation-adjusted real wages fell for the sixth straight month in June. This is troubling because it suggests household spending power is shrinking, which could hurt overall consumption.

Without a strong, consumption-driven recovery, the case for aggressive BoJ tightening becomes harder to justify. Policymakers will need to balance their inflation goals with the risk of slowing growth.

What This Means for Traders

For now, USD/JPY is stuck in a waiting game. If the US CPI report comes in hotter than expected, it could strengthen the Dollar and push the pair higher. But if inflation shows signs of cooling, it might encourage the Fed to move ahead with rate cuts, giving the Yen a chance to recover.

USDJPY is moving in a descending triangle pattern, and the market has rebounded from the support area of the pattern

Longer term, the big question is whether the BoJ will actually raise rates this year. If it does, the move would be symbolic as much as economic—showing that Japan is finally moving away from years of ultra-loose policy. Until then, traders will likely remain cautious, reacting to every new piece of economic data from both sides of the Pacific.

Final Summary

The Japanese Yen is caught in the middle of a tug-of-war between mixed BoJ signals and changing Fed expectations. While Japan’s higher inflation forecast hints at possible rate hikes, weak wage growth and political uncertainty make aggressive moves less likely. Meanwhile, the Fed is leaning toward rate cuts, but the exact timing will depend heavily on upcoming inflation data. With both sides in flux, traders are choosing to wait, watching key economic releases and policy statements before committing to new positions in USD/JPY.

AUDUSD Finds Support as US Pushes Back China Tariffs Before Key RBA Meeting

The Australian Dollar (AUD) is holding its ground against the US Dollar (USD) as traders keep a close watch on important developments that could shape currency markets in the days ahead. With the Reserve Bank of Australia’s (RBA) policy decision just around the corner and key global economic events unfolding, both investors and analysts are paying extra attention to what’s coming next.

RBA Policy Decision: What’s at Stake for the Australian Dollar

The Reserve Bank of Australia is preparing for its highly anticipated policy meeting, and expectations are running high that it could cut interest rates by 25 basis points. While markets are mostly convinced of this outcome, the real action will likely come from the RBA’s accompanying statement and the Governor’s remarks.

AUDUSD is moving in a descending channel, and the market has reached the lower low area of the channel

Investors will be watching closely to see how the RBA frames its decision in terms of inflation control, economic growth, and future monetary policy plans. Even a slight change in tone could influence the Australian Dollar’s short-term direction.

Why This Decision Matters

The RBA’s interest rate policy directly impacts borrowing costs, consumer spending, and investment. A rate cut often signals that the central bank is trying to stimulate economic growth, but it can also put downward pressure on the currency. However, in this case, the Australian Dollar has managed to remain steady, possibly due to supportive global factors.

US-China Tariff Truce: A Temporary Boost for Risk Sentiment

One major factor supporting the Australian Dollar is the recent move by the US administration to delay new tariffs on China for an additional 90 days. Australia has deep trade ties with China, so any easing of tensions between the world’s two largest economies tends to be positive for its currency.

China has responded to the US extension by pausing its own planned tariffs on American goods for the same period. This mutual pause in trade hostilities has helped stabilize market sentiment, giving risk-related currencies like the AUD some breathing space.

The Bigger Picture

While the temporary truce offers relief, it’s far from a permanent solution. Investors know that trade disputes can flare up again with little warning. For now, though, this pause gives the Australian Dollar some short-term resilience, especially ahead of the RBA’s decision.

The US Side of the Story: Inflation, the Fed, and Political Moves

While the Australian market watches the RBA, global traders are also focused on developments in the United States. The US Consumer Price Index (CPI) report is due soon, and the data will be closely analyzed to see whether inflation pressures are cooling or heating up.

Federal Reserve Rate Cut Expectations

Markets have been adjusting their bets on the US Federal Reserve’s next move. Recent data shows an 84% probability of a rate cut in September, slightly lower than the previous week’s 90% estimate. Several Fed officials have been weighing in on the matter:

-

Michelle Bowman, a Fed Governor, suggested that three rate cuts could be appropriate this year, citing a weaker labor market as a bigger concern than potential inflation spikes.

-

Mary Daly, President of the San Francisco Fed, noted that the fight against inflation isn’t over yet and that the Fed may need to act even without complete economic clarity.

-

Susan Collins and Lisa Cook from the Fed also pointed to ongoing uncertainties that could make policy adjustments tricky.

These differing viewpoints reflect the challenge the Fed faces—balancing inflation control with economic growth and employment concerns.

Political Changes at the Fed

Adding to the mix, US President Donald Trump has nominated Stephen Miran to join the Federal Reserve Board of Governors and is reportedly considering replacements for the current Fed Chair. Christopher Waller, another Fed Governor, is said to be a top contender for the role. Such changes could influence the central bank’s approach in the months ahead, potentially affecting currency markets globally.

China’s Economic Signals: Mixed But Better Than Expected

China’s latest inflation figures offered a small surprise for the markets. The Consumer Price Index remained flat year-over-year in July, avoiding the slight decline that analysts had expected. Meanwhile, the Producer Price Index showed a drop of 3.6% compared to the same time last year.

For Australia, these numbers matter because China is its largest trading partner. Stable or improving economic conditions in China can help support demand for Australian exports, indirectly giving the AUD a lift.

Geopolitical Tensions Still Lurking

While there’s currently a pause in US-China trade tensions, it’s clear that geopolitical risks are still in the background. Reports suggest that President Trump has warned China about possible future tariffs, even making comparisons to trade penalties on India over its oil purchases from Russia.

For traders and investors, this means that any sudden escalation could quickly undo the recent calm in currency markets. The Australian Dollar, often seen as a risk-sensitive currency, would likely be among the first to react to any fresh turbulence.

What Traders Are Watching Next

In the short term, all eyes are on two key events:

-

The RBA Decision and Governor’s Speech – Markets will be looking for any hints about future rate moves and the central bank’s view of the economy.

-

The US CPI Report – This could influence not only the US Dollar but also global risk sentiment, indirectly impacting the AUD.

The combination of domestic monetary policy changes and global economic signals will likely shape the Australian Dollar’s path in the coming days.

AUDUSD is rebounding from the major support area

Final Summary

The Australian Dollar is holding steady ahead of a crucial RBA policy decision that could see interest rates trimmed. A temporary easing of US-China trade tensions has offered short-term support, while traders also keep an eye on US inflation data and Federal Reserve moves.

With China’s economy showing mixed but slightly better-than-expected data, and geopolitical uncertainties still present, the currency markets remain in a delicate balance. The next few days could set the tone for the AUD’s performance, making this a period of heightened attention for investors, businesses, and anyone following global financial trends.