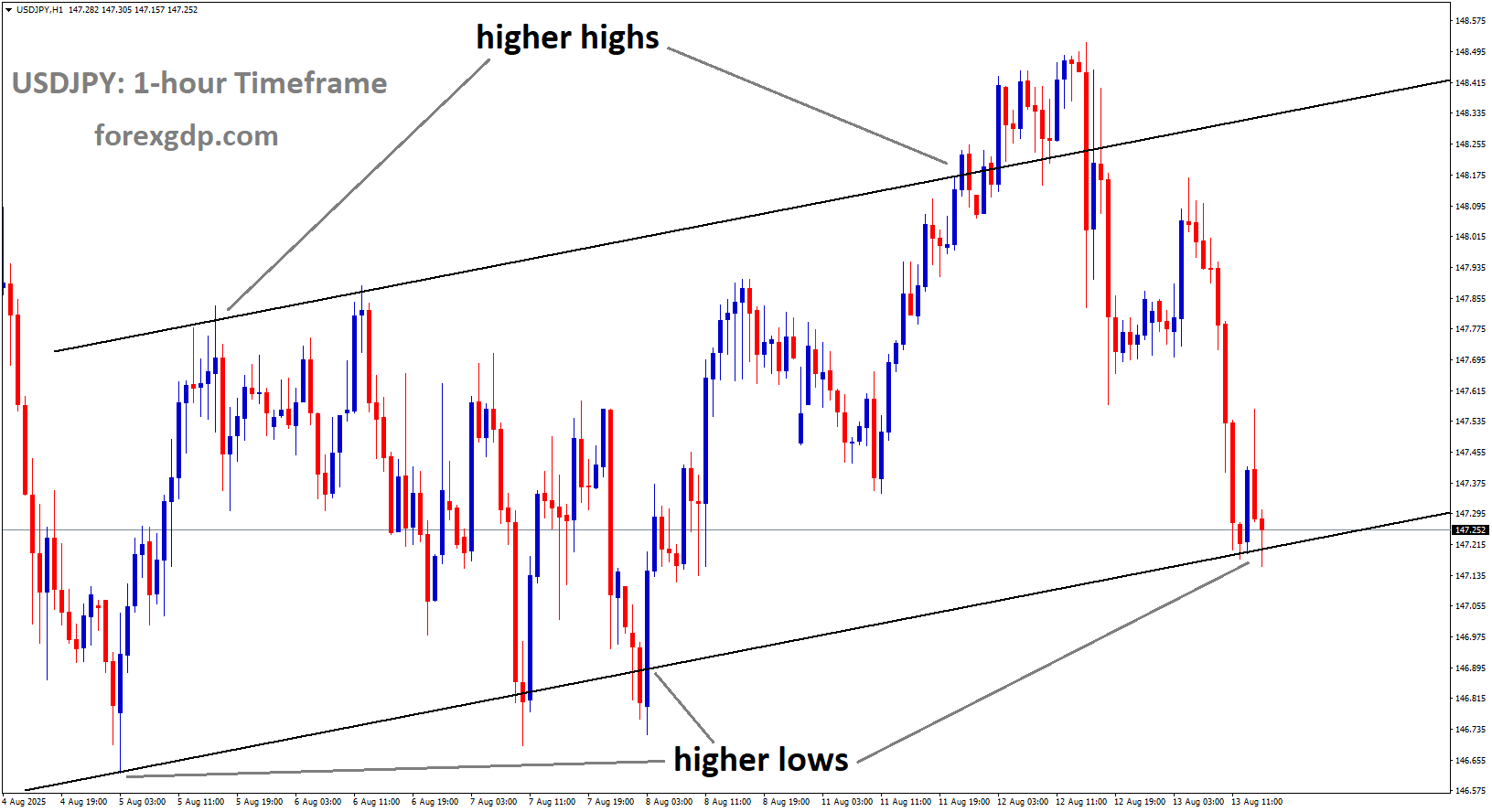

USDJPY is moving in an uptrend channel, and the market has reached the higher low area of the channel

Daily Forex Trade Setups Aug 13, 2025

Stay on top of market trends with our Daily Forex Trade Setups (Aug 13, 2025)

USDJPY Slips as Dollar Softens, Yen Struggles to Build Momentum

The Japanese Yen (JPY) is quietly making moves, and if you’re watching global currencies, it’s probably caught your eye. The Yen recently turned higher for the second day in a row, not because of major economic strength, but largely due to weakness in the US Dollar (USD). But there’s a lot more behind this story — from central bank strategies to inflation concerns and even shifting global sentiment.

Let’s dig into what’s really happening behind the scenes and why the Yen is behaving the way it is right now.

Why the Yen Is Bouncing Back (But It’s Not What You Think)

You might expect that a stronger currency is a sign of a stronger economy. But when it comes to the Yen, it’s not quite that straightforward. Right now, the Japanese Yen is gaining ground mainly because the US Dollar is stumbling.

So, what’s dragging the USD down? It comes down to changing expectations around interest rates in the US. Many traders are starting to believe the Federal Reserve might begin cutting interest rates soon — possibly as early as next month. That would make the Dollar less attractive to investors, especially when compared to currencies like the Yen.

At the same time, the Bank of Japan (BoJ) is keeping everyone guessing. While they’ve hinted at the possibility of raising interest rates, they haven’t committed to a clear timeline. This uncertainty has traders hanging on every word from Japanese policymakers, which means even a hint of future rate hikes can swing the Yen one way or the other.

What’s Going On With Japan’s Economy?

Let’s talk about Japan itself. The country has been dealing with some mixed signals recently, and that’s partly why the BoJ hasn’t moved aggressively yet.

Slowing Wholesale Inflation

Earlier this week, Japan reported a slowdown in wholesale inflation. For the fourth month in a row, wholesale prices have cooled off. That might sound like good news, but it also means there’s less pressure on the BoJ to act quickly on rate hikes.

However, not everything in the inflation story is easing. Prices of food and agricultural goods are still climbing, which shows that inflation is starting to spread out more broadly across the economy. That kind of price behavior keeps investors on edge, thinking maybe — just maybe — the BoJ could still raise rates before the end of the year.

Real Wages and Political Jitters

Another area of concern is Japan’s real wages. They’ve been falling steadily, which makes it harder for households to keep up with rising prices. That weak consumer spending can drag down economic growth, and it gives the BoJ yet another reason to take a cautious approach.

Add to that the ongoing political uncertainty within Japan and fears about how higher US tariffs might impact Japanese exports, and it becomes clear why there’s no rush to tighten policy just yet.

Global Risk Sentiment: A Silent Driver of Currency Moves

Another piece of the puzzle that’s often overlooked? Global risk appetite.

Right now, the overall market mood is pretty upbeat. Recent progress in US-China trade relations and efforts by the US and Russia to ease tensions over the Ukraine war have boosted investor confidence. When global markets feel safe, investors usually pull their money out of safe-haven assets like the Yen and move it into riskier investments like stocks.

But oddly enough, despite this risk-on environment, the Yen is still holding its ground. That tells us a lot about just how weak the US Dollar has become — and how sensitive the markets are to what central banks might do next.

All Eyes on the Fed and BoJ: Who Moves First?

Right now, it’s all about central bank expectations. Investors are betting that the Bank of Japan might raise interest rates before the year ends. At the same time, there’s growing belief that the US Federal Reserve is getting ready to start cutting rates.

Why the Fed Is Expected to Cut

The latest US consumer inflation report didn’t show any surprises. Both headline and core inflation matched expectations — with the core rate even slightly higher than before. But here’s the catch: these numbers weren’t enough to shift the overall thinking that the US economy is starting to slow down.

There are signs of weakening in the US labor market and broader economy. Combine that with the belief that recent price pressures caused by tariffs are temporary, and suddenly a rate cut in September doesn’t seem far-fetched. In fact, markets are now pricing in the possibility of not just one, but possibly two rate cuts by the end of the year.

BoJ’s Delicate Balancing Act

On the other side, the Bank of Japan is taking a slow and cautious approach. While they’ve acknowledged that inflation is gradually moving in the right direction, they’re also wary of making any sudden moves that could shock the fragile recovery. The risk of tightening too quickly — especially when wages are still weak — is something they’re trying to avoid.

So we’re left with this weird tension: A weaker Dollar due to expected Fed cuts, and a cautiously stronger Yen thanks to the mere possibility of BoJ tightening.

What to Watch Next

Here’s what’s coming up that could shake things up even more:

-

US Producer Price Index (PPI): This report, due soon, could give new clues about how inflation is evolving in the US and whether the Fed’s rate path needs to change.

-

Japanese GDP Data: A preview of Japan’s second-quarter GDP figures is on the horizon. If growth is stronger than expected, it could boost the Yen further and increase the chances of a BoJ rate hike.

USDJPY is moving in an uptrend channel

-

FOMC Speeches: A number of US central bank officials are scheduled to speak this week. What they say about the economy, inflation, and rate cuts will have a big impact on how the USD/JPY pair moves.

Wrapping It All Up

The Yen’s recent moves aren’t just about Japan — they’re a reflection of what’s happening across the global economy. From the Federal Reserve’s potential rate cuts to Japan’s inflation worries, every piece of news is like a ripple in a very sensitive pond.

For now, the Yen is getting a bit of a boost thanks to a weaker US Dollar and lingering hopes for a BoJ rate hike. But with so many moving parts — inflation data, political uncertainty, central bank strategies — it’s clear that this story is far from over.

So, whether you’re a trader, an investor, or just someone curious about what’s shaping the world economy, keep an eye on both Tokyo and Washington. The next move could come from either side — and it might just surprise us all.

EURUSD Stays Strong with Traders Eyeing Looming Fed Policy Shift

The Euro is enjoying a fresh wave of strength against the US Dollar, riding the momentum of softer inflation data coming out of the United States. The latest figures have sparked renewed optimism that the Federal Reserve might ease interest rates as early as September. This change in sentiment has tilted the currency markets in favor of the Euro, while the US Dollar finds itself under mounting pressure.

EURUSD is moving in a descending channel, and the market has reached the lower high area of the channel

Why the Euro is Gaining Momentum

The shift in market mood began when the US released its July Consumer Price Index (CPI) data. Inflation was steady instead of accelerating, which immediately gave traders hope that the Federal Reserve could pivot toward a rate cut sooner than expected. The lower pace of inflation combined with a cooling labor market has made the case stronger for monetary easing.

One key factor behind this optimism is that the impact of recently imposed tariffs has not yet shown up in the inflation numbers. This reassured investors that the central bank has room to act without fear of immediate price spikes. With borrowing costs already high, a potential rate cut could support economic growth, encourage spending, and ease pressure on households.

Fed Policy Expectations and Political Influence

While economic indicators are nudging the Fed toward a looser monetary policy, political factors are adding another twist to the story. There’s growing speculation that leadership changes at the central bank could bring in officials more aligned with the current administration’s preference for an accommodative stance.

If this happens, it could make rate cuts more likely in the coming months, further eroding the appeal of the US Dollar to investors. Markets are now betting heavily on a September cut, with many expecting at least one more before the end of the year. The combination of economic data and political developments has made traders increasingly cautious about holding dollars.

Investor Sentiment: Risk Appetite on the Rise

A weaker US Dollar often boosts global market sentiment, and that’s exactly what’s happening now. With lower inflation reducing the need for aggressive rate hikes, risk appetite is growing. Investors are moving away from safe-haven assets like the Dollar and seeking better returns in other currencies and markets.

Even without major new economic data from Europe, the Euro is benefiting from this global shift in sentiment. German inflation numbers released recently confirmed a stable price trend, adding a subtle layer of confidence for Euro bulls. Although the impact of this data was minimal compared to the US CPI, it reinforced the idea that Europe’s inflation situation is under control for now.

The Bigger Picture for Currencies

The recent developments highlight a broader trend in currency markets: sentiment often shifts quickly when inflation and interest rate expectations change. In this case, the Euro is gaining mainly because the Dollar is losing favor, not because of a sudden surge in European economic strength.

However, the implications are significant. A sustained period of US Dollar weakness could boost European exports by making them cheaper for international buyers, potentially supporting economic growth in the Eurozone. On the other hand, if the Fed hesitates to cut rates despite market expectations, the Dollar could recover sharply, putting the Euro rally at risk.

EURUSD is moving in an Ascending channel, and the market has rebounded from the higher low area of the channel

Final Summary

The Euro’s recent rally is a clear example of how currency markets react to shifting interest rate expectations. Softer US inflation has opened the door for potential Federal Reserve rate cuts, pulling the Dollar lower and giving the Euro room to climb. Political factors and investor risk appetite are adding extra fuel to the move.

While the focus remains on September for a possible Fed decision, traders know that sentiment can turn quickly. For now, though, the Euro is enjoying its time in the spotlight, and the Dollar is struggling to find support in the face of growing expectations for easier US monetary policy.

GBPUSD Trades Calmly with Eyes on UK Economy and Fed Policy Shifts

When it comes to currencies, the British Pound has been surprisingly calm lately. It hasn’t shown wild swings or shocking moves — it’s just waiting. And so are traders. The reason? Everyone’s keeping their eyes on one key number: the UK’s second-quarter GDP report.

Let’s unpack what’s going on and why this calm before the storm matters — not just for the Pound but for anyone keeping track of the global economy.

What’s the Big Deal About UK GDP Data?

The Gross Domestic Product (GDP) basically tells us how well a country’s economy is doing. It measures the total value of goods and services produced — in other words, is the economy growing or shrinking?

GBPUSD has broken the descending channel on the upside

Slower Growth Could Raise Concerns

Analysts expect the UK economy to have grown just a tiny bit — around 0.1% — between April and June. That’s much lower than the solid 0.7% growth seen in the first quarter. On a yearly basis, it’s expected to come in at about 1%, which is also weaker than what the Bank of England (BoE) hoped for.

What does this mean? It suggests that the UK economy might be slowing down. While it’s not shrinking, it’s definitely not racing ahead either.

And here’s the thing — when growth slows, pressure starts to build. Especially on the Bank of England, which is already juggling some pretty tricky decisions.

Why the Bank of England Is in a Tight Spot

The BoE has a tough job: keeping inflation under control without choking off growth. It’s like trying to balance on a tightrope in a windstorm. And right now, there’s turbulence on both sides.

Inflation Still Hanging Around

Inflation has been stubbornly high in the UK. Recently, the BoE even adjusted its inflation forecast, expecting consumer prices to rise 2.7% over the next year — more than the 2.4% they predicted earlier. That’s not good news for households already dealing with higher costs.

Job Market Cooling Off

At the same time, the job market is showing signs of cooling. The number of job vacancies in the UK dropped by 44,000 between May and July. And employers are becoming more cautious. In fact, some companies aren’t replacing workers who leave, let alone hiring new ones.

One reason for this pullback? A recent increase in employers’ social security contributions, which has made hiring more expensive. Companies are simply choosing to hold off on expanding their teams.

That puts the BoE in a bind: inflation is still a problem, but the economy and the job market are both slowing. Raising interest rates too much could make things worse, but not acting on inflation could cause prices to spiral.

What’s Happening with the Pound and the US Dollar?

While the UK watches its own data, traders are also keeping an eye on the United States — and it’s been a busy time across the Atlantic too.

Fresh US Inflation Numbers Shift the Mood

New inflation data out of the US came in more or less in line with what traders expected. Headline inflation rose 2.7%, and core inflation — which leaves out food and energy — rose to 3.1%. Both numbers were a little softer than feared, and that was enough to get people thinking.

Thinking about what? Interest rate cuts. Specifically, whether the US Federal Reserve (the Fed) might cut rates in its next policy meeting.

Right now, traders believe there’s a high chance — over 90% — that the Fed will go ahead with a rate cut in September. That’s a big jump from earlier in the week.

And when traders start pricing in rate cuts, the US Dollar tends to weaken. That’s part of why the Pound has been able to hold its ground against the Dollar recently. In fact, it’s even gained a little.

Is a Fed Rate Cut Really Locked In?

Not everyone’s convinced that a rate cut is guaranteed. Some economists are warning that there’s still a lot of data to come — especially another round of jobs and inflation reports — before the Fed meets.

Basically, it’s not a done deal. One strong report could easily swing the decision the other way. And that uncertainty is keeping markets a little on edge.

What to Watch Next: Market Sentiment and Central Bank Speeches

With all this data swirling around, markets are hanging on every word from central bankers.

In the US, speeches from three key Federal Reserve officials — Thomas Barkin, Raphael Bostic, and Austan Goolsbee — are coming up. Investors will be watching for any hints about how the Fed is leaning.

Will they confirm that a rate cut is likely? Or will they signal caution and suggest waiting for more data? Either way, their words could move markets.

GBPUSD is moving in an Ascending channel

Meanwhile, back in the UK, the upcoming GDP report could be a big turning point. If it comes in weaker than expected, the pressure on the BoE might intensify. And that could influence how the Pound moves in the days to come.

Final Summary

Right now, the British Pound is like a boat drifting calmly before the waves hit. Everyone’s waiting for Thursday’s GDP report — a key signal of where the UK economy is heading next.

At the same time, US inflation data has added fuel to hopes of a Fed rate cut, putting downward pressure on the Dollar and giving the Pound some breathing room.

But this calm might not last. A weaker UK GDP number could raise fresh concerns about the health of the British economy. And if the US Fed changes its tone or if new data surprises traders, markets could move fast.

So, if you’re following currency markets, stay tuned. The next few days could bring the kind of shifts that end the quiet and stir up the storm.

NZDUSD Pushes Higher Beyond 0.5950 with Rate Cut Hopes in Focus

The New Zealand Dollar (NZD) has been showing signs of strength against the US Dollar (USD) in recent sessions, fueled by a mix of economic factors and political developments. With a softer US Dollar, rising expectations of a US Federal Reserve interest rate cut, and an extended tariff truce between the US and China, market sentiment around the NZD/USD pair has shifted positively. Let’s break down the main factors driving this move and what it could mean going forward.

The US Dollar’s Weakness Opens the Door for NZD Strength

One of the primary reasons behind the New Zealand Dollar’s upward movement is the recent weakness in the US Dollar. Investors have been reacting to softer US economic data, particularly inflation figures that came in cooler than anticipated. This shift has changed the market’s expectations for the Federal Reserve’s next moves.

NZDUSD is moving in an Ascending channel, and the market has reached the higher high area of the channel

The latest US Consumer Price Index (CPI) report indicated that overall inflation rose modestly on a yearly basis. While prices are still growing, the pace has been slower than some feared. Importantly, the core CPI—excluding food and energy—was slightly higher than forecast but still aligned with a broader trend of moderation.

This cooling inflation has led traders to believe the Federal Reserve may cut interest rates sooner rather than later, potentially as early as September. Lower interest rates typically weaken the US Dollar because they reduce returns for investors holding dollar-denominated assets. As the USD loses ground, other currencies like the NZD can benefit from increased demand.

Political Developments Add to the Positive Mood for NZD

While economic data often takes the spotlight, political events can have just as much influence on currency markets. This week, US President Donald Trump announced another 90-day extension of the tariff truce with China, avoiding the immediate escalation of trade tensions.

Just before the previous agreement was set to expire, the US signed an executive order to maintain the current pause on new tariffs. China responded in kind, stating that it would also suspend additional tariffs on US goods for the same period.

For New Zealand, this is more than just a headline. China is one of its largest trading partners, and the Kiwi Dollar is often seen as a “China-proxy” currency in global markets. Any sign of easing trade tensions between the US and China tends to boost confidence in the New Zealand economy, supporting the NZD. However, analysts are cautious, noting that while some uncertainty has been removed, trade relations remain fragile. Any renewed tensions could quickly reverse the recent optimism.

Why Market Sentiment Matters for NZD/USD

Beyond the hard data, market sentiment plays a big role in currency movements. At the moment, traders are more willing to take on risk, especially in currencies linked to commodity exports and global growth, like the NZD.

The combination of a softer US Dollar, reduced trade tensions, and expectations of lower US interest rates has created a favorable environment for the Kiwi. Even though New Zealand’s own economic challenges remain, the currency is gaining from the perception that global headwinds may be easing slightly.

Investor Behavior and Risk Appetite

When investors feel more confident about the global economy, they tend to seek higher returns in riskier assets. The New Zealand Dollar often benefits in these scenarios because of the country’s strong trade ties, stable political environment, and history of relatively higher interest rates compared to other developed nations.

In contrast, when uncertainty rises, investors typically rush back to “safe haven” assets like the US Dollar, the Japanese Yen, or gold. This push-and-pull dynamic is a constant driver of the NZD/USD exchange rate.

Looking Ahead – What Could Influence the Next Move?

Although recent developments have given NZD/USD a boost, there are still many factors that could shift the trend in the coming weeks.

-

Federal Reserve Communications

Later today, speeches from senior Fed officials, including Chicago Fed President Austan Goolsbee and Atlanta Fed President Raphael Bostic, could provide fresh clues on the central bank’s thinking. If they signal stronger support for a rate cut, the US Dollar could weaken further, pushing NZD/USD higher. -

Trade Developments Between the US and China

The current tariff truce offers some breathing room, but the underlying issues between the two largest economies remain unresolved. Any signs of renewed conflict could hurt the NZD’s outlook, given New Zealand’s dependence on trade with China. -

Global Economic Data

Economic reports from major economies—including manufacturing data, employment figures, and commodity demand—could influence market sentiment. Strong global growth data tends to favor the NZD, while weak data could pull it down.

NZDUSD is moving in a descending channel, and the market has rebounded from the lower low area of the channel

Final Summary

The NZD/USD pair has recently found support from a weaker US Dollar, growing expectations of a Federal Reserve interest rate cut, and a temporary easing of US-China trade tensions. The latest US inflation data has tilted the odds toward looser monetary policy in the US, reducing the Greenback’s appeal and giving the Kiwi room to rise. Meanwhile, the 90-day extension of the tariff pause between Washington and Beijing has boosted confidence in trade-linked currencies, although uncertainty remains over the long-term outcome.

For now, the tone in the market is cautiously optimistic. Investors will be watching closely for any shifts in US central bank policy or fresh developments in the US-China relationship. While the New Zealand Dollar has gained ground recently, its next move will depend heavily on whether current favorable conditions persist or give way to renewed global uncertainty.

EURGBP Stays Firm as Markets Eye Crucial UK GDP Release

The EUR/GBP currency pair has been holding firm in early European trading, showing resilience despite mixed signals from both the Eurozone and the United Kingdom. While political developments between the United States and Russia are adding an interesting twist to the market atmosphere, recent economic data from Europe and the UK is playing a major role in guiding investor sentiment. Let’s break down what’s been happening and why it matters.

A Political Twist: US-Russia Talks Spark Optimism

One of the biggest stories influencing the Euro’s recent strength comes from outside Europe altogether — a high-profile meeting planned between US President Donald Trump and Russian President Vladimir Putin. Scheduled to take place in Alaska on Friday, the discussion is aimed at finding a resolution to the ongoing war in Ukraine.

EURGBP is moving in a box pattern

This meeting was announced a week in advance, coinciding with Trump’s deadline for Russia to agree to a ceasefire or face additional US sanctions. The geopolitical stakes are high, and any progress could have ripple effects across global markets. For the Euro, this adds a layer of support, as improved diplomatic conditions could benefit European economies indirectly by reducing uncertainty and geopolitical tensions.

While the market is watching these developments closely, traders are cautious. Past negotiations between global leaders on such sensitive issues have often been unpredictable, meaning investors are balancing optimism with a realistic view of possible outcomes.

Eurozone Sentiment Takes a Hit

Despite the political boost from US-Russia talks, the Euro is not without challenges. Fresh data from the Eurozone has revealed a notable dip in investor confidence.

The latest ZEW Economic Sentiment Survey for August showed a sharp decline in optimism. The Eurozone reading dropped to 25.1 from 36.1 in July, while Germany — the region’s largest economy — saw sentiment plunge from 52.7 to 34.7. Both figures were significantly below market expectations.

This decline in confidence suggests that investors and analysts are becoming more cautious about the region’s economic outlook. Weak manufacturing data, slower consumer spending, and global uncertainties may be contributing to this shift in sentiment. While the political news from across the Atlantic offers a short-term lift, these numbers serve as a reminder that the Eurozone’s economic challenges remain in play.

The UK Jobs Market Sends Mixed Signals

On the other side of the EUR/GBP equation, the British Pound has its own set of influences. The UK labour market has shown signs of softening, with employment data suggesting weaker job growth. However, one key metric remains strong — wage growth.

Rising wages, even in the face of slowing job creation, suggest that inflationary pressures in the UK are still a concern for the Bank of England (BoE). As a result, traders have scaled back expectations for an imminent interest rate cut. According to market data, a BoE rate reduction is now fully priced in only for February 2026, a shift from earlier bets on a sooner move.

This change in expectations is important because interest rate decisions directly impact currency values. Higher interest rates generally make a currency more attractive to investors, meaning the Pound could find some support if the BoE maintains a cautious stance.

Why This Matters for EUR/GBP

When the Euro gains from geopolitical optimism but is held back by weak economic sentiment, and the Pound gets a boost from central bank caution despite softer jobs data, it creates a tug-of-war effect in the EUR/GBP exchange rate. This balancing act is exactly why the pair has been holding steady rather than making a sharp move in either direction.

Investors are essentially weighing two competing stories:

-

For the Euro: Political developments may offer short-term relief, but economic fundamentals raise questions about long-term strength.

-

For the Pound: A less dovish BoE may support the currency, but economic data is not entirely encouraging.

What Traders and Investors Are Watching Next

Looking ahead, one of the most important upcoming events for this currency pair will be the release of the UK’s preliminary Gross Domestic Product (GDP) figures for the second quarter. Set for Thursday, this data will offer a clearer view of how the UK economy is performing and could tip the balance for the Pound.

EURGBP is moving in a descending triangle pattern

Meanwhile, in the Eurozone, markets will be keeping a close eye on any additional political or economic developments. The outcome of the Trump-Putin meeting could have far-reaching consequences, especially if there are concrete steps toward easing tensions in Ukraine.

Final Summary

The EUR/GBP currency pair is currently shaped by a mix of political headlines and economic realities. Optimism from planned US-Russia talks has given the Euro some lift, but weak economic sentiment data is holding back further gains. On the UK side, a cautious Bank of England is offering support to the Pound despite a softer jobs market.

This combination of factors is creating a balanced market, with neither currency taking a decisive lead. In the days ahead, GDP data from the UK and the outcome of high-level diplomatic talks will be the main drivers to watch. For now, EUR/GBP remains steady, reflecting a market in wait-and-see mode — ready to react when the next big development hits.