US President Donald Trump is making a bold move to change how Americans can invest their retirement savings. He wants to make it simpler for workers to use their 401(k) plans for alternative assets like cryptocurrencies, private equity, real estate, gold, and other non-traditional investments that have typically been out of reach for the average person.

This decision could reshape the way retirement savings are managed, potentially offering more opportunities — but also raising concerns about risk. Let’s break down what this means, why it matters, and how it might affect everyday workers in the future.

A Shift in How Retirement Accounts Could Work

For decades, retirement accounts in the US — especially 401(k) plans — have mainly focused on traditional investments like stocks, bonds, and mutual funds. These are seen as relatively safer and easier to manage for long-term growth.

Now, Trump has ordered regulators to review existing rules that discourage employers from including alternative assets in retirement plans. This includes not only digital currencies like Bitcoin but also investments such as:

-

Private equity funds – ownership stakes in private companies not traded on the stock market.

-

Real estate – properties or real estate investment opportunities.

-

Precious metals – such as gold, which some see as a hedge against inflation.

-

Other alternative investments – assets that don’t fall into the typical stock-and-bond categories.

Under his directive, the Department of Labor has 180 days to examine the rules and suggest ways to make it easier for employers to offer these options.

Why This Move Could Be a Big Deal

Retirement accounts in the US are a massive pool of money. Since most workers no longer get a traditional pension that guarantees income after retirement, 401(k)s have become the main way to save for the future.

With a 401(k):

-

Employees can put aside part of their paycheck for investments.

-

Employers often match a portion of the contributions.

-

Growth is tax-deferred until the money is withdrawn.

By opening the door to alternative investments, Trump’s proposal could give people access to opportunities that were once limited to wealthy investors and big institutions. In theory, this could mean:

-

Higher growth potential – Some alternative investments can outperform traditional markets in certain conditions.

-

More diversification – Holding a mix of different assets could help spread risk.

-

New funding sources for businesses – Companies in private equity, crypto, and real estate could benefit from the influx of retirement money.

However, with potential rewards also come potential pitfalls.

The Risks Critics Are Pointing Out

Not everyone is celebrating this idea. Critics argue that alternative investments often come with higher risks and can be harder to manage within a retirement account. Here’s why:

1. Higher Fees

Private equity and other alternative funds often charge more in fees compared to traditional investments like index funds. Over decades, higher costs can eat into retirement savings significantly.

2. Less Transparency

Public companies must disclose detailed financial information regularly. Many alternative investments don’t have the same strict reporting requirements, making it harder for everyday investors to fully understand what they’re buying into.

3. Liquidity Issues

Some investments, like private equity or real estate projects, can take years before you see returns. If an investor needs quick access to cash, it might be difficult or even impossible to sell these assets immediately.

4. Complexity for Employers

Current laws hold employers responsible for making sure the retirement options they offer are suitable. Including high-risk investments could make them more cautious, or lead to legal challenges if things go wrong.

Big Names Already Moving Into This Space

Even before Trump’s latest move, some major financial companies were exploring ways to bring alternative investments into retirement accounts. Giants like State Street and Vanguard — both leaders in retirement plan management — have already partnered with firms such as Apollo Global and Blackstone to design private equity-focused retirement funds.

This suggests the industry is preparing for a shift, even if regulatory changes take time to roll out. If the Department of Labor eases the restrictions, these companies could be ready to offer new options quickly.

A Look Back at Past Efforts

This isn’t the first time Trump has tried to push for broader investment choices in retirement plans. During his first term, his administration encouraged retirement plans to include private equity options. However, fears of lawsuits and complex rules kept many employers from moving forward.

Later, under former President Joe Biden, the Department of Labor reversed Trump’s earlier guidance and took a more cautious stance. In fact, in 2022, the Department advised employers to be extremely careful before allowing cryptocurrencies in retirement accounts. That cautionary note has now been rolled back under Trump’s direction.

What This Could Mean for the Average Worker

If these changes go through, an employee could eventually log into their 401(k) account and see options beyond mutual funds and index funds. They might be able to allocate part of their savings into a cryptocurrency fund, a real estate investment project, or a private equity pool.

For some, this could be an exciting opportunity to grow wealth in new ways. For others, it could feel like a risky gamble with retirement money that needs to last decades.

Financial experts often warn that alternative investments should only be a small portion of a portfolio, especially for those who aren’t experienced investors. That’s because while these assets can offer big rewards, they can also suffer big losses — and in retirement planning, stability often matters just as much as growth.

Final Summary

Donald Trump’s push to expand retirement account investment choices could mark a major change in how Americans prepare for the future. By making it easier to invest in crypto, private equity, real estate, gold, and other alternative assets, millions of workers might soon have access to opportunities that were once reserved for the wealthy.

However, these options also come with higher fees, less transparency, and greater risk compared to traditional investments. Employers will have to weigh the potential benefits against the responsibilities and risks of offering them.

For workers, the key takeaway is simple: more choices can be powerful, but they also demand more knowledge and caution. If the rules change, it will be up to each saver to decide how adventurous they want to be with their retirement money — and how much risk they’re willing to take on the path to building their future.

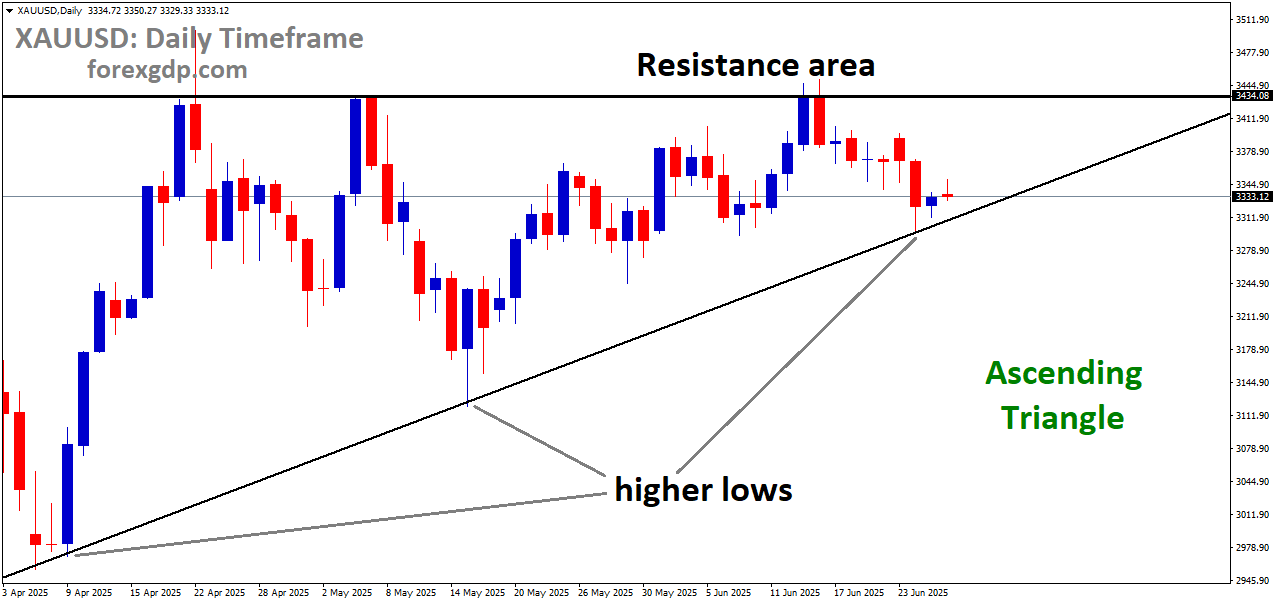

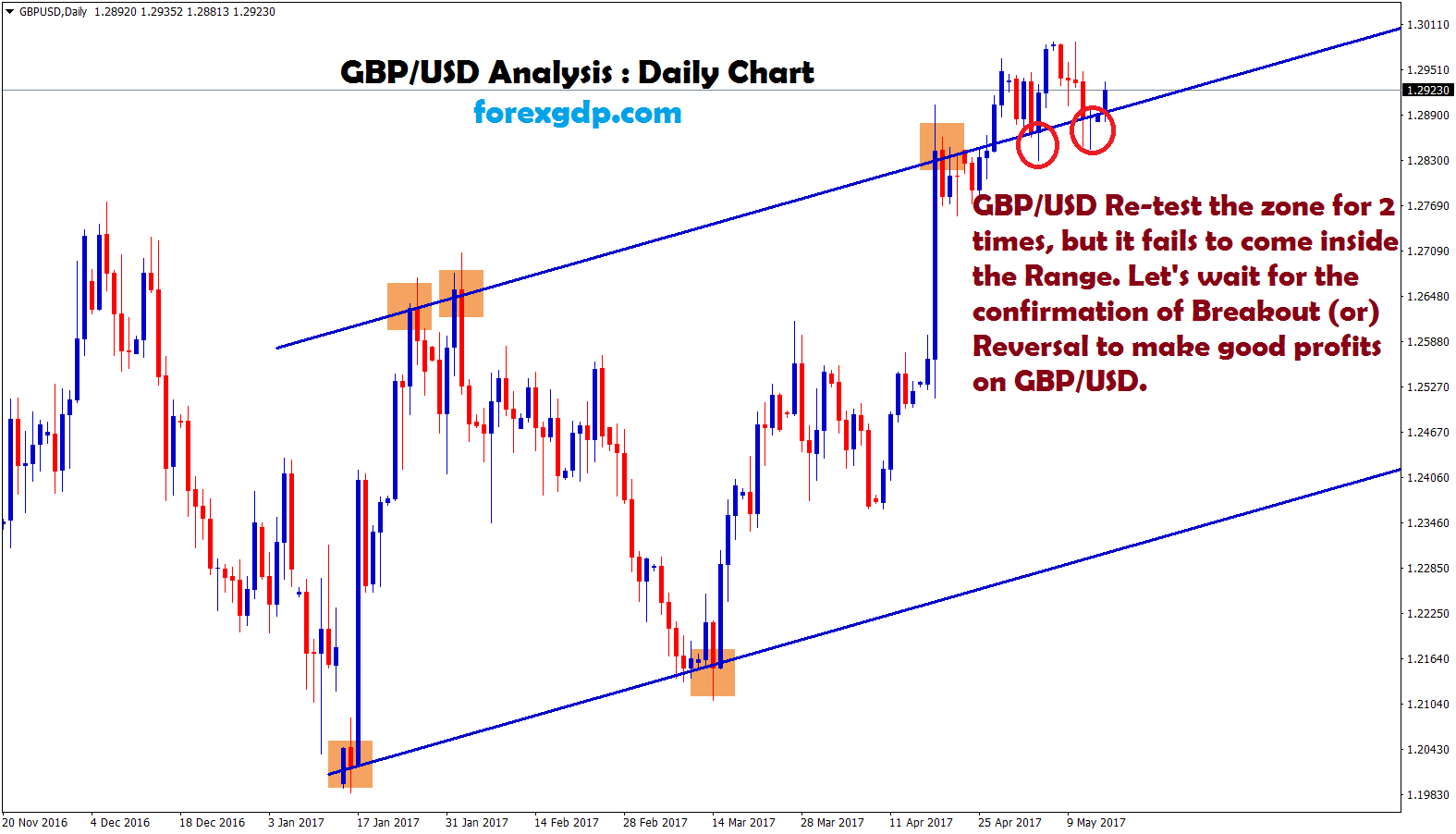

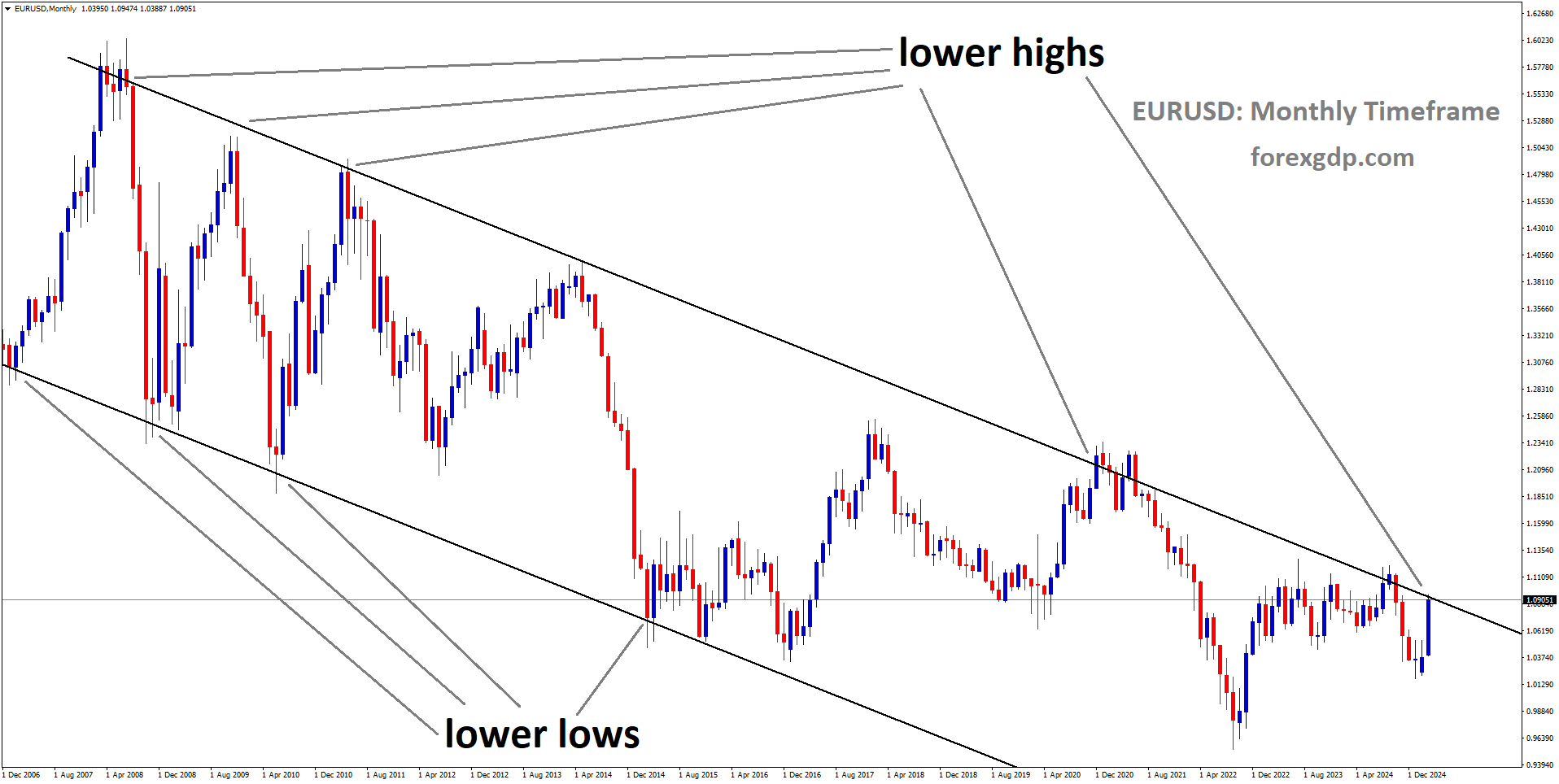

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!