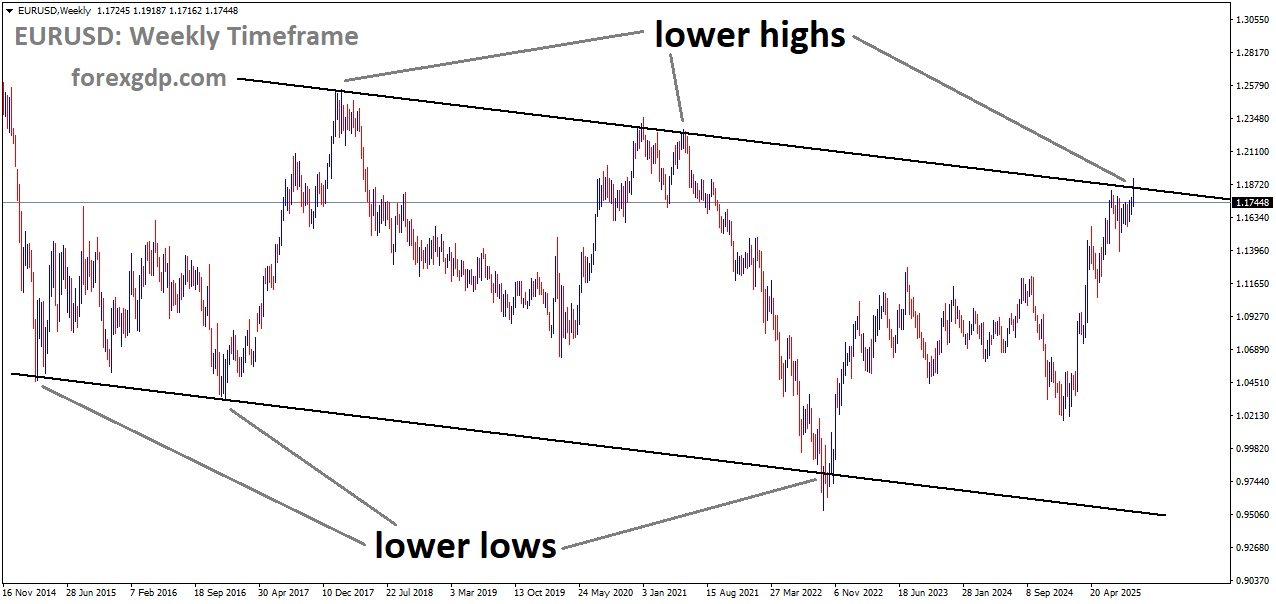

EURUSD is moving in a downtrend channel, and the market has reached the lower high area of the channel

EURUSD Weakens Again with Greenback Supported by Positive US Economic Reports

When we talk about global currencies, the Euro and the US Dollar are often at the center of attention. Recently, the Euro has been under pressure, while the Dollar has shown resilience thanks to stronger economic data coming from the United States. At the same time, political unrest in Europe has added more weight on the Euro, keeping it on the defensive. Let’s break down what’s happening, why it matters, and what could lie ahead.

Why the Dollar Is Holding Strong

The US Dollar has been finding support because of a mix of economic data and investor sentiment. Two big reports gave it a lift:

-

Jobless Claims Report – The number of Americans filing for unemployment benefits dropped much more than expected. Fewer claims suggest that the job market is stronger than many thought, and that usually gives the Dollar more strength.

-

Manufacturing Activity – A fresh survey on factory output showed a sharp rebound. After months of weakness, this recovery was welcomed by investors and further boosted the Dollar.

These reports helped ease worries that the US economy might be heading toward a sharp downturn. Investors still believe the Federal Reserve may cut interest rates again in the near future, but the stronger data gave some relief and prevented panic.

Europe’s Political Tensions and Their Impact on the Euro

While the US Dollar was riding positive data, the Euro had its own problems. In France, a wave of protests has been building up. Thousands of people across the country have been demonstrating against proposed spending cuts. The protests are not only about economic reforms but also about broader frustrations with the government.

This political unrest adds uncertainty to the European economy. Investors usually dislike uncertainty, and when it happens in one of Europe’s biggest economies, it tends to put pressure on the Euro. Even though there hasn’t been much fresh economic data from Europe, these political developments are enough to weaken the currency.

The Role of Central Banks

Central banks play a huge role in shaping how currencies move, and right now both the Federal Reserve (Fed) and the European Central Bank (ECB) are in focus.

Federal Reserve’s Position

The Fed has already lowered interest rates in recent months, and markets expect another cut soon. Futures markets even show that most traders are betting on two more small cuts before the year ends. Rate cuts usually weaken a currency, but since the US economy still looks relatively stable compared to Europe, the Dollar has managed to stay strong.

European Central Bank’s Tone

On the other side, the ECB has been more cautious. The Vice President recently said that the bank’s current stance is “appropriate,” but he also admitted that risks remain high. That kind of message hints that the ECB may keep easing its policies if needed. Such dovish signals often pressure the Euro further.

Global Trade and the US Supreme Court’s Role

Another interesting development is in the United States, where the Supreme Court will soon decide on the legality of trade tariffs. These tariffs have been a major part of US trade policy, and their fate could influence not just the Dollar but also global trade flows. If the court rules against them, it could shake up markets and affect how investors see the US economy.

For now, traders are cautious but not overly worried. The decision is still weeks away, but it adds another layer of uncertainty in the background.

How Investors Are Reacting

Right now, investors are caught between two forces:

-

Positive US data that supports the Dollar.

-

Political risks and dovish signals from Europe that weaken the Euro.

At the same time, expectations of more rate cuts from the Fed are keeping the Dollar from rallying too strongly. This balance has created a market mood that’s neither fully optimistic nor fully fearful.

Investors are also watching closely for the next moves from both central banks. Any hint of changes in policy could quickly shift the balance.

The Bigger Picture

Currencies don’t move in isolation. The Dollar’s strength or weakness often depends not just on the US economy but also on what’s happening in other regions. Right now, Europe’s unrest makes the Euro look vulnerable, which in turn makes the Dollar look like a safer bet.

EURUSD is moving in an uptrend channel

Global trade policies, central bank decisions, and political developments all play their part. While the Dollar is not expected to soar dramatically, it still has an edge over the Euro in the current environment.

Final Summary

The Euro is under pressure, weighed down by political unrest in France and the lack of fresh positive drivers in Europe. Meanwhile, the US Dollar has found support in stronger-than-expected jobless claims and manufacturing data, even though investors still expect the Federal Reserve to cut interest rates again.

With central banks staying in focus and political uncertainty lingering, the balance between the Euro and the Dollar remains delicate. For now, the Dollar holds the upper hand, but upcoming policy decisions and political events could easily shift the tide again.

GBPUSD Drops as UK Debt Pressures Spark Gilt Market Surge

The Pound Sterling has been under heavy pressure recently, with multiple economic and political factors combining to create uncertainty for the UK currency. From rising government borrowing to cautious moves by central banks, the financial landscape is shifting quickly, and these changes are leaving their mark on the British pound. Let’s break down the key drivers behind the market mood and what they could mean in the months ahead.

GBPUSD has broken the uptrend channel on the downside

UK Borrowing Surges: A Warning Sign for the Economy

One of the biggest triggers behind the latest wave of selling in the Pound is the news about public sector borrowing in the UK. Recent figures revealed that the government borrowed nearly £18 billion in August, the highest amount for that month in the past five years. To put it in perspective, economists had been expecting a much smaller figure, closer to £12.8 billion.

This surge in borrowing highlights the deepening fiscal challenges faced by the UK. When a government borrows more than expected, it raises questions about how it will handle its finances moving forward. Will taxes be increased? Will spending be cut? Or will both happen together? These are the difficult questions policymakers now face as they prepare for the Autumn budget.

Why Rising Borrowing Matters

High borrowing levels don’t just affect government accounts—they ripple through the wider economy. More borrowing means the government will issue more debt, and that pushes up yields on UK gilts (government bonds). Recently, yields on long-dated gilts jumped sharply, signaling investors are demanding more return for lending to the government. While this reflects concerns about fiscal stability, it also directly impacts borrowing costs for households and businesses, making mortgages and loans more expensive.

US Data Shakes Things Up: Retail Sales Surprise

While the UK is wrestling with borrowing issues, across the Atlantic, the United States posted stronger-than-expected retail sales data. Consumer spending, measured by retail sales, rose by 0.5% in August, beating the market’s forecast of 0.4%. Even on a yearly basis, spending showed steady growth.

This might sound like a small difference, but in economic terms, it signals that American consumers are still spending with confidence, despite inflationary pressures and higher borrowing costs in recent months. Interestingly, online shopping and clothing-related purchases showed particularly strong demand.

Stronger US retail performance often supports the US dollar because it gives the Federal Reserve more room to manage interest rates without worrying about growth slowing too sharply. And when the US dollar strengthens, the Pound often feels the pressure in comparison.

Bank of England’s Careful Approach

At home, the Bank of England (BoE) has taken a cautious stance. In its recent policy update, the BoE decided to keep interest rates steady at 4%, with the majority of policymakers voting in favor of holding rather than cutting. This decision wasn’t surprising, given that UK inflation has been stubbornly high in recent months.

The central bank also announced that it will slow down its program of quantitative tightening, meaning it will reduce the pace at which it sells government bonds back into the market. Between October 2025 and September 2026, the BoE plans to sell around £70 billion worth of gilts, compared with £100 billion in the past year. This is seen as a way to avoid putting too much pressure on financial markets while still gradually unwinding pandemic-era policies.

Inflation Outlook

The BoE expects inflationary pressures to peak around 4% in September. While this is lower than the extreme levels seen previously, it is still above the bank’s 2% target. Keeping inflation under control while managing growth remains a delicate balancing act.

Federal Reserve’s Shift: Rate Cuts Ahead

Adding to the mix, the US Federal Reserve recently cut its benchmark interest rate by 25 basis points, lowering it to a range of 4.00%-4.25%. What really caught attention, though, was the Fed’s signal that two more rate cuts could come before the end of the year.

This move was largely in response to signs that the US labor market is cooling. Jobless claims fell slightly last week, but the Fed acknowledged that the risks are no longer balanced, and the economy is not showing the same level of strength in employment as before. Fed Chair Jerome Powell admitted that he could no longer describe the labor market as “solid,” a statement that carries significant weight for investors.

For the Pound, this dynamic creates an interesting challenge. Normally, rate cuts in the US might weaken the dollar, giving other currencies like the Pound some breathing room. But with the UK’s fiscal concerns dominating headlines, the pound has struggled to take advantage of this shift.

Global Confidence and What Comes Next

Right now, the interplay between UK domestic challenges and global monetary policy is setting the tone for the Pound Sterling. On one hand, rising borrowing and fiscal uncertainty at home are making investors cautious about the UK’s financial outlook. On the other hand, global policy changes, especially in the US, are shifting the balance of power in currency markets.

GBPUSD is moving in an Ascending channel, and the market has reached a higher high area of the channel

Investors are also keeping a close eye on speeches and statements from key policymakers, such as upcoming remarks from San Francisco Fed President Mary Daly. Any hints about the pace and timing of further US interest rate cuts could influence how markets position themselves in the near term.

Final Summary

The Pound Sterling is caught in a complex web of fiscal concerns, central bank decisions, and global economic trends. With UK borrowing surging, government bond yields rising, and the Autumn budget on the horizon, the domestic picture is far from stable. At the same time, strong US retail data and a dovish shift from the Federal Reserve are adding extra layers of pressure.

For now, the outlook for the Pound remains uncertain. Much will depend on how the UK government addresses its fiscal challenges in the coming months and how central banks on both sides of the Atlantic balance their fight against inflation with the need to support growth. One thing is clear—the next few months will be critical in shaping the Pound’s trajectory in global markets.

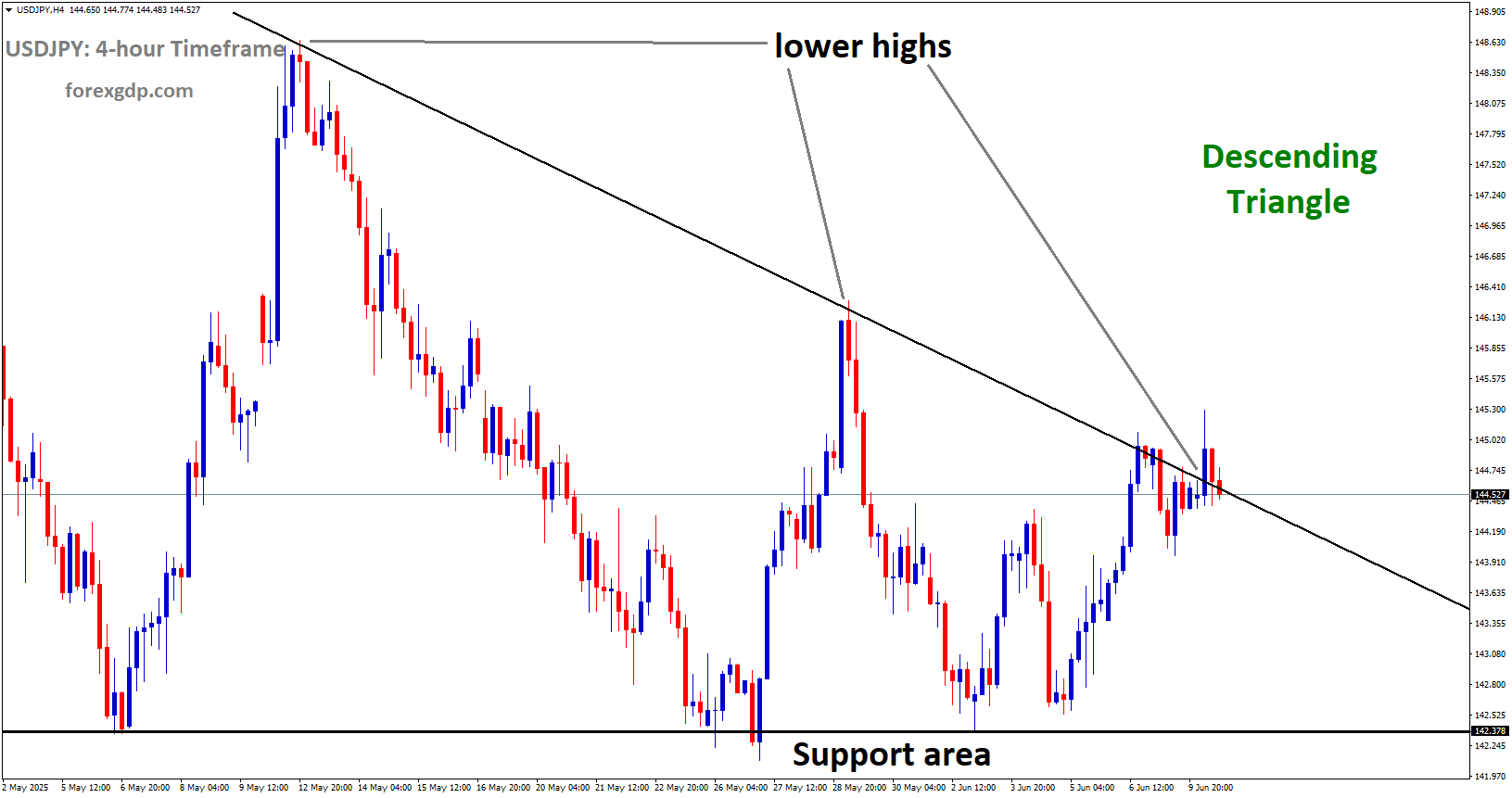

USDJPY holds ground while BoJ Ueda outlines future policy stance

The global currency market is always buzzing with excitement, but when it comes to the Japanese Yen (JPY), things often get even more interesting. Recently, the Bank of Japan (BoJ) kept interest rates steady yet again, but the tone from Governor Kazuo Ueda left no room for doubt—the central bank isn’t afraid to hike rates in the near future if the economy keeps moving in the right direction. This subtle yet powerful signal has drawn attention worldwide and given the Yen a solid push.

USDJPY is rebounding from the retest area of the broken downtrend channel

Let’s dive deep into what’s going on with the Yen, the BoJ’s stance, and how global developments are shaping the USD/JPY relationship.

BoJ’s Decision: A Hawkish Hold That Turned Heads

For the fifth meeting in a row, the Bank of Japan decided to keep its rates unchanged. On the surface, this might sound like business as usual, but here’s where it gets interesting: two members of the board actually dissented, calling for a rate hike. That dissent alone highlights how the internal mood at the BoJ is shifting, leaning more toward tightening policy sooner rather than later.

During his press conference, Governor Kazuo Ueda struck a cautious but confident tone. He mentioned that while global growth is showing signs of moderation, Japan’s domestic economy is still supported by favorable conditions. More importantly, he reiterated that if the economy and prices behave in line with forecasts, the central bank is prepared to raise rates. This hawkish undertone was enough to spark fresh demand for the Yen.

Why Investors Are Paying Attention

The BoJ has long been known for its ultra-loose monetary policy, often standing apart from other major central banks. So, when officials even hint at raising rates, global investors pay close attention. A potential shift away from years of easy money policies could mark a big turning point for Japan’s financial outlook and the Yen’s position on the global stage.

Inflation Trends and Domestic Challenges

While the BoJ’s words carry weight, domestic data paints a mixed picture. Japan’s core consumer prices slowed down in August, rising at the slowest pace in nine months. For an economy that has spent decades battling low inflation, this slowdown brings up questions.

Core Inflation Eases

-

Core CPI (excluding fresh food) rose by 2.7% in August, down from 3.1% in July.

-

A separate gauge that strips out fresh food and fuel showed a slight dip too, from 3.4% to 3.3%.

Although inflation is still above the BoJ’s 2% target, the slowdown hints that price pressures may be easing. This creates a bit of a puzzle: should the BoJ act on its hawkish stance now, or should it wait to see if inflation trends continue cooling?

Political and Economic Uncertainty

Add to that the ongoing domestic political uncertainty and external pressures like U.S. trade tariffs, and it becomes clear why the central bank is moving cautiously. These headwinds make it risky to commit to aggressive tightening, even if there’s a case for it.

Global Forces: USD Strength and Fed’s Influence

The Japanese Yen doesn’t move in isolation—it’s always dancing with global partners, most notably the U.S. Dollar (USD). Right now, the Fed’s policies are playing a huge role in shaping the USD/JPY outlook.

Fed’s Stance Keeps Dollar Afloat

Recently, Federal Reserve Chair Jerome Powell made remarks that fueled the Dollar’s rebound. While the Fed has already cut rates once as a form of “risk management,” Powell stressed that risks to inflation remain tilted upward. He made it clear that the Fed isn’t rushing to cut again and will decide on a meeting-by-meeting basis.

This careful but slightly hawkish tone has allowed the Dollar to preserve its recovery after hitting its weakest level since early 2022. For the USD/JPY pair, this has acted like a counterbalance to the BoJ’s hawkish stance.

Diverging Paths Create Market Tension

Here’s the catch: the Fed is still widely expected to cut rates twice more in 2025, while the BoJ is leaning toward eventual hikes. This divergence is fascinating for traders and investors. On one hand, a softer Fed could weaken the Dollar over time. On the other hand, even the smallest move from the BoJ toward higher rates could make the Yen more attractive. This push-and-pull keeps the USD/JPY pair in focus.

How Investors Are Reacting

Right now, investor sentiment toward the Yen is cautious optimism. Many believe that while the BoJ hasn’t pulled the trigger yet, the groundwork is being laid for policy tightening. This makes the Yen more appealing, but not enough for traders to go all in just yet.

Bond Yields Tell the Story

Yields on Japanese government bonds recently climbed to levels not seen since 2008. That’s a clear reflection of shifting expectations. When bond yields rise, it often signals that investors believe rate hikes are coming. This, in turn, narrows the yield gap between Japan and other economies, reducing the appeal of holding foreign currencies over the Yen.

USDJPY is moving in an uptrend channel, and the market has reached the higher low area of the channel

Looking Ahead: What’s Next for the Yen and USD/JPY?

The coming weeks and months could be crucial for both the Yen and the Dollar. Investors will be watching closely for three things:

-

BoJ’s Next Move: Will the central bank finally raise rates in October, or will they hold back again?

-

Inflation Data: If core inflation keeps slowing, the pressure to hike may ease. But if it stabilizes above 2%, the BoJ could feel compelled to act.

-

Fed’s Cuts: Two more cuts from the Fed in 2025 could reshape the USD/JPY outlook, especially if the BoJ surprises with its own tightening.

The combination of these factors makes for an unpredictable but exciting landscape.

Final Summary

The Japanese Yen is gaining attention not because the BoJ did something dramatic, but because of what they might do next. Governor Ueda’s hawkish hints, coupled with dissenting voices within the BoJ, suggest that Japan may finally be stepping away from its ultra-loose policy era. At the same time, slowing inflation, political uncertainty, and external headwinds make the timing tricky.

Globally, the Dollar’s strength adds another layer of complexity. The Fed’s cautious but hawkish approach contrasts with its expected rate cuts in 2025, creating a unique dynamic with Japan’s potential tightening. For investors and traders, this means the USD/JPY pair could remain volatile and highly sensitive to every policy statement and data release.

In short, the Yen’s story is no longer about standing still—it’s about preparing for a possible shift, one that could redefine its role in the global currency market.

GBPJPY recovers ground after Bank of Japan signals policy shift

When currencies start moving quickly, it often comes down to major decisions made by central banks or unexpected data releases. That’s exactly what happened recently with the British Pound and the Japanese Yen. The Pound managed to climb back from its weekly lows thanks to a mix of Bank of Japan policy updates and surprisingly strong UK retail sales figures. Let’s break down what drove these movements and what they might mean going forward.

GBPJPY is moving in a box pattern, and the market has reached the resistance area of the pattern

The Bank of Japan’s Policy Shift Shakes the Yen

The Japanese Yen has always been one of those currencies that traders keep a close eye on. Its movements are often influenced heavily by the Bank of Japan (BoJ), which plays a major role in shaping investor confidence.

Recently, the BoJ decided to keep its benchmark interest rate unchanged at 0.5%. While that in itself wasn’t much of a surprise, what truly caught markets off guard was the announcement that the bank plans to start selling its holdings of exchange-traded funds (ETFs) and real estate investment trusts (REITs).

This move signaled a potential shift in strategy. By reducing exposure to these assets, the BoJ hinted that it’s becoming more confident in the strength of the Japanese economy and financial markets. Initially, this caused the Yen to surge, as investors read the announcement as a more hawkish stance.

But things didn’t stop there. BoJ Governor Kazuo Ueda followed up with comments stressing that Japan’s economy remains resilient despite global challenges such as tariffs. He also emphasized that the central bank would continue to tighten monetary policy if economic data and inflation trends lined up with forecasts. His words gave the Yen another boost, showing that Japan might be ready to take more serious steps toward normalization.

UK Retail Sales Surprise on the Upside

While Japan was making headlines with its monetary policy, the UK was drawing attention with fresh economic data. Retail sales figures came in stronger than expected, and this gave the Pound some much-needed support.

For the month of August, UK retail sales rose 0.5% compared to the previous month. On a year-over-year basis, sales increased by 0.7%. Both figures beat market expectations, which had been slightly more cautious. Even more encouraging was the fact that when fuel sales were excluded, overall retail activity was still up by 0.8% monthly and 1.2% annually.

The strongest contributions came from clothing, non-store retail (such as online shopping), and specialist food shops. These categories reflect consumers’ willingness to spend, even during a time of ongoing cost-of-living concerns. For the British economy, this kind of consumer resilience is important because household spending makes up a significant portion of GDP.

When the retail sales data was released, the Pound began to recover against the Yen. The timing couldn’t have been better, as the UK figures helped offset the earlier pressure created by Japan’s hawkish central bank stance.

Pound vs Yen: A Currency Tug of War

The recent back-and-forth between the Pound and Yen highlights how quickly currency markets can shift. On one side, you have Japan’s central bank signaling more confidence in its economy, which boosts the Yen. On the other, you have the UK showing stronger-than-expected consumer activity, which supports the Pound.

At first, the Yen’s jump looked set to dominate the story. But as the day progressed, the Pound found its footing thanks to the positive UK data. By the end of the week, the Pound had managed to climb back above its earlier lows, showing that market forces are often a balancing act between different regions’ economic signals.

What This Means for the Broader Economy

-

For Japan: The BoJ’s decision to hold rates steady but reduce ETF and REIT holdings signals a cautious but meaningful step toward normalizing policy. Investors will likely watch closely for further hints of tightening, especially if inflation continues to move higher.

-

For the UK: Strong retail sales suggest that, despite challenges like inflation and rising borrowing costs, consumers are still willing to spend. This resilience could help support growth in the near term, even if other sectors of the economy remain under pressure.

GBPJPY is moving in an uptrend channel, and the market has reached the higher low area of the channel

-

For Global Markets: The tug-of-war between the Pound and Yen is a reminder of how interconnected economies are. A central bank move in Asia and a consumer spending update in Europe can combine to create big swings in exchange rates.

Final Summary

The Pound’s rebound against the Yen shows how sensitive currencies are to both monetary policy shifts and fresh economic data. The Bank of Japan rattled markets with its announcement about selling ETFs and REITs, while Governor Ueda’s remarks underlined a readiness to keep tightening policy if conditions allow. This gave the Yen an early advantage.

However, the UK’s retail sales data quickly turned the tide. By showing that British consumers are still spending strongly, the figures gave the Pound enough momentum to bounce back from its lows.

For traders, investors, and even everyday observers, this episode is a clear example of how currency markets reflect a blend of global and local forces. While Japan and the UK may be thousands of miles apart, their economic decisions and data releases can collide in real time to shape the movements of major currencies.

USDCAD Strengthens with Dollar Gains While Canada Faces Pressure

The foreign exchange market has been buzzing with attention as the US Dollar (USD) continues to climb steadily against the Canadian Dollar (CAD). Over the past few days, the greenback has shown strength, while the Canadian currency remains under pressure. Let’s dive into what’s fueling this momentum, why the USD is performing so well, and what challenges the CAD is currently facing.

USDCAD is moving in an uptrend channel, and the market has reached the higher low area of the channel

Why the US Dollar is Gaining Strength

One of the main reasons behind the recent boost in the US Dollar comes from positive US economic data. In simple terms, the numbers have been stronger than what analysts expected, and that naturally makes investors more confident about holding dollars.

Stronger Jobless Claims

Recent unemployment claims in the US dropped much more than anticipated. When fewer people are filing for jobless benefits, it usually means that the labor market is holding up well. A healthy job market reflects resilience in the economy and boosts faith in the US Dollar.

Manufacturing Shows Improvement

Another encouraging report came from the Philadelphia Federal Reserve, which revealed an unexpected rebound in manufacturing activity. For investors, this is a signal that the American economy is not slowing down as quickly as some had feared. Manufacturing is often seen as a backbone of growth, so signs of stability bring renewed optimism.

Together, these two reports—jobs and manufacturing—gave the USD an extra lift, helping it extend its winning streak for several consecutive days.

Canadian Dollar Under Pressure

While the US Dollar is enjoying a surge, the Canadian Dollar is facing challenges of its own. The Bank of Canada recently made a decision that has weighed heavily on its currency.

Interest Rate Cuts from the Bank of Canada

Earlier this week, Canada’s central bank lowered its benchmark interest rate. Cutting rates typically makes a currency less attractive to global investors because returns on Canadian assets become lower compared to other markets. On top of that, the Bank of Canada hinted that more rate cuts could follow. This cautious outlook added further pressure on the Canadian Dollar, which has already been struggling to keep pace with the USD.

Weak Retail Sales Expectations

Adding to the troubles, Canada’s retail sales numbers are expected to show a decline. Consumer spending is a key part of any economy, and when people buy less, it signals weakness in growth. If retail sales fall as predicted, it could reinforce concerns about Canada’s economic slowdown, pushing the CAD even lower.

A Tale of Two Economies

The contrast between the US and Canada right now couldn’t be clearer. On one side, you have the US showing resilience with stronger jobs and manufacturing. On the other, Canada is cutting rates while battling softer consumption.

Investor Sentiment

Investors tend to favor currencies that look safer and more promising. At this moment, the US Dollar fits that description better than the Canadian Dollar. This is why we’re seeing a continuous shift toward the USD and away from the CAD.

Global Perspective

Globally, the US economy still holds a dominant position. Any signs of strength in America often magnify demand for the greenback. Meanwhile, commodity-linked currencies like the Canadian Dollar can become vulnerable if domestic conditions weaken, especially when combined with a dovish central bank policy.

What This Means for Traders and Businesses

For those actively involved in trading or international business, these movements are significant. A stronger US Dollar means American companies importing goods from Canada may find slightly better terms. On the flip side, Canadian exporters may face more challenges as their earnings lose value when converted back into Canadian dollars.

For everyday consumers, exchange rate fluctuations may not always be obvious immediately, but they do impact travel costs, online purchases, and even fuel prices, given Canada’s strong ties to global commodities.

USDCAD is moving in a box pattern, and the market has rebounded from the support area of the pattern

What to Watch Next

The next few weeks will be important for both currencies. Investors will closely follow:

-

Upcoming US economic releases: If job numbers and manufacturing continue to stay strong, the USD may hold its edge.

-

Bank of Canada’s stance: Any hints about further rate cuts could add more pressure on the CAD.

-

Retail and consumer data from Canada: Weak numbers will confirm that the Canadian economy is losing steam, while stronger-than-expected results may provide a small relief.

Final Summary

The US Dollar has been on a winning streak, lifted by strong economic indicators such as falling unemployment claims and improved manufacturing activity. This strength has created confidence among investors and reinforced the Dollar’s dominance on the global stage.

Meanwhile, the Canadian Dollar is struggling, pressured by the Bank of Canada’s recent interest rate cut and weak retail sales outlook. Together, these factors have created a clear divide between the two currencies, with the USD outperforming the CAD.

For traders, businesses, and even consumers, these shifts highlight how economic data and central bank decisions can quickly change the direction of currencies. As things stand, the US Dollar continues to shine, while the Canadian Dollar faces headwinds that may take time to ease.

AUDUSD Under Pressure with US Dollar Gaining from Fed’s Balanced Approach

The Australian Dollar (AUD) has had a challenging time recently, slipping for several days against the US Dollar (USD). A mix of weaker-than-expected local jobs data and the strengthening of the US Dollar has kept the Aussie on the back foot. However, despite the struggles, there are still reasons for optimism that the currency might regain some stability in the near future. Let’s dive into the details and explore what’s going on with the Aussie Dollar, why it matters, and what could happen next.

AUDUSD has broken the uptrend channel on the downside

Australia’s Job Market Sends Mixed Signals

One of the main drivers behind the Australian Dollar’s muted performance has been the latest employment report. The figures showed that Australia lost more jobs than expected in August. Instead of adding positions, the employment change turned negative, showing a contraction after a previously strong month.

What made the report particularly disappointing was the contrast with market expectations, which had forecast solid job growth. The number of jobs lost wasn’t enormous, but it was enough to signal that the labor market may not be as strong as previously thought.

On the positive side, Australia’s unemployment rate remained steady at 4.2%. While not alarming, the job losses highlighted the fragility of the current recovery. For currency traders and investors, these numbers painted a picture of an economy that is holding steady but still facing uncertainties.

Why Interest Rate Expectations Are Crucial

Another factor shaping the Aussie Dollar’s movements is speculation about the Reserve Bank of Australia’s (RBA) next steps. Interest rates play a big role in currency markets because they determine how attractive a currency is to global investors.

At present, markets are pricing in only a slim chance of an RBA rate cut in the short term. For September, the odds of a cut are around 20%, which is relatively low. However, November looks more uncertain, with markets seeing a much higher possibility of a rate cut later this year.

AUDUSD is falling from the retest area of the broken Ascending Triangle pattern

The reason behind this cautious stance from the RBA is inflation. Prices are still running above the central bank’s comfort zone, making it difficult for policymakers to justify immediate rate cuts. Inflationary pressures mean the RBA has to tread carefully, balancing the need to support growth with the goal of keeping inflation under control.

The US Dollar Keeps Gaining Strength

While the Aussie has been struggling, the US Dollar has been enjoying broad-based gains. Much of this strength has come after the release of the latest US labor market data, particularly weekly jobless claims.

The figures showed that fewer Americans filed for unemployment benefits than expected, a sign that the US job market remains resilient despite ongoing global challenges. With fewer layoffs and steady hiring, confidence in the US economy is holding up.

A stronger job market supports the idea that the US Federal Reserve might not need to aggressively ease policy, at least in the immediate term. This sentiment has pushed the US Dollar higher, adding more pressure on the AUD/USD pair.

Global Developments Add to the Mix

Currency markets don’t operate in isolation, and global events have also played a role in shaping the fortunes of the Australian Dollar.

For example, US-China relations remain a critical backdrop. Reports that US President Donald Trump could extend a trade truce with Chinese President Xi Jinping created fresh headlines. Trade tensions have a direct effect on Australia because China is its largest trading partner. Any sign of easing tensions usually supports the Aussie, while renewed conflicts weigh heavily on it.

On top of that, Chinese economic data released recently has been somewhat softer than expected. Retail sales growth slowed, and industrial production came in weaker than forecasts. While officials in Beijing described the economy as “generally steady,” they also acknowledged that businesses are struggling with external pressures. For Australia, this matters because its economy is closely tied to China’s demand for commodities and exports.

What the RBA Thinks Right Now

The Reserve Bank of Australia has been closely watching these developments. Sarah Hunter, the RBA’s Assistant Governor, recently noted that the central bank is getting closer to achieving its inflation target. That’s good news because hitting the target gives the RBA more flexibility in managing monetary policy.

She also emphasized that risks to the outlook are fairly balanced. In other words, the RBA does not see the economy tipping too far in either direction just yet. Hunter highlighted that the central bank is keeping a close eye on consumer spending and overall economic activity to ensure growth remains steady.

Her remarks suggest that the RBA isn’t rushing to cut rates but is keeping the door open if conditions worsen. This kind of cautious optimism reflects the uncertainty of today’s global economy.

Why the Aussie Dollar Still Has a Fighting Chance

Even though the Australian Dollar has been under pressure, it’s not all doom and gloom. Here are a few reasons why the currency might still find some support:

-

Limited rate cut expectations: With only a small chance of an immediate RBA rate cut, the Aussie isn’t facing the same downside risks it would if cuts were guaranteed.

-

Global trade hopes: Any improvement in US-China trade relations would likely boost the Australian Dollar, given its reliance on China.

-

Resilient domestic demand: If consumer spending holds up, it could support growth and give investors more confidence in Australia’s outlook.

AUDUSD is moving in a descending channel, and the market has reached the lower high area of the channel

These factors mean that while the Aussie Dollar has dipped, it could rebound if conditions align favorably in the coming weeks.

Final Summary

The Australian Dollar’s recent weakness has been driven by a mix of domestic and global factors. A disappointing jobs report raised concerns about the strength of the labor market, while the US Dollar gained momentum on the back of stronger-than-expected American data. At the same time, global events—from US-China trade talks to signs of a slowing Chinese economy—added further complexity.

Despite these challenges, the outlook for the Aussie isn’t entirely bleak. With the Reserve Bank of Australia adopting a cautious but balanced approach, and with opportunities for global trade tensions to ease, the currency still has a path to recovery. The next few months will be key in determining whether the Australian Dollar can regain its footing or continue to face headwinds.

For now, it’s a story of patience and cautious optimism—watching how economic data unfolds and how central banks respond to the ever-changing global landscape.