USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The failure of SVB Bank and Signature Bank in the US has caused the US dollar to weaken in the markets. Even so, the markets continue to suffer, and 2-year Treasury Yields are now at 4.20%, up from 3.94% but still well below 5%.

The US CPI data is a highly anticipated report due this week. The FED is anticipated to pause rate increases in light of the failure of SVB Bank, and markets do not anticipate any immediate rate increases in the coming months.

As a result, until the SVB Bank Issue is resolved, the US Dollar will continue to deteriorate.

After a disastrous start to the week, the US Dollar’s decline has so far stopped today. Although Treasury rates have increased across the curve, they are still far below the highs reached last week. The benchmark 2-year note dropped to 3.94% overnight, well below 5% plus at this time last week, before ticking up to 4.20% in the Asian session. The effects of SVB and Signature Bank’s collapse are still being felt. Regional US banks’ stock values are suffering steep declines, but large-cap banks are holding up somewhat better, despite continuing to lose money. The KBW bank index, which tracks 23 publicly traded US financial names, is down from nearly 116 at the beginning of this month to trade below 80 overnight. In the Monday cash session, Wall Street as a whole maintained its stability, and so far, futures are pointing to a good start to their day.

All of the APAC equity indices are in the red, with Japan heading the decline. The TOPIX index there was briefly dragged down by sharp drops in banking equities that totaled over 3%. It comes as no surprise that Korea’s KOSDAQ index is significantly lower, down more than 2.5%, given the pressure on the technology industry. In all the turmoil, gold has held onto recent gains as a combination of collapsing real yields, USD weakness and a rush to perceived safety appear to have boosted the precious metal.

During the North American period, crude oil fell slightly before rising toward the close. With the WTI futures contract close to US$ 74 bbl and the Brent contract close to US$ 80 bbl at the time of going to press, it has slightly declined going into the European session. This puts today’s US CPI figure and its implications for the Federal Open Market Committee (FOMC) meeting next week in sharp relief. Whatever the print, doubt seems to be the only thing that is certain. According to a Bloomberg poll of economists, the CPI will rise 0.4% from one month to the next in February. The European Central Bank (ECB) conference is on Thursday, so pan-European inflation data will continue to be released today and tomorrow.

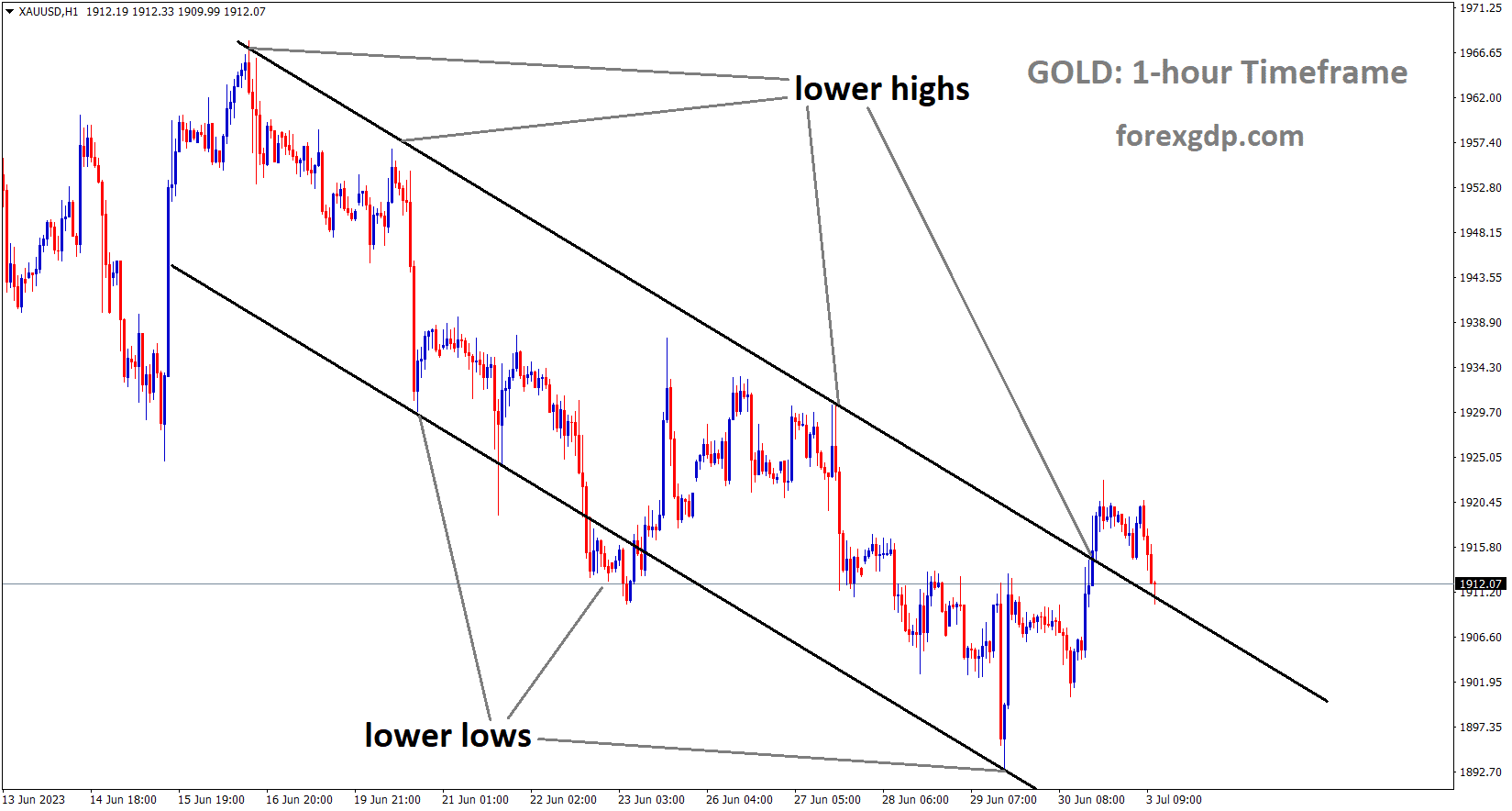

GOLD Analysis

XAUUSD Gold price has broken the Box Pattern in Upside.

Due to the collapse of SVB and Signature banks, gold rose from its lows to reach a six-week peak.The FED’s rate increases on US treasuries are more dubious, and the collapse of SVB Bank, which resulted in a 192 billion dollar default, has caused the US FED to print additional US dollars in an effort to stabilize public trust in banks. In the past two days, non-yielding assets have been preferred over producing assets in the panic markets.

Overnight, gold reached a six-week high as market ripple effects from the collapse of Silvergate Financial Corp., SVB Financial, and Signature Bank continue. The US Dollar has been hit hard, undermined by the Treasury yields protracted retreat with the 2-year note trading more than 100 basis points lower from its 15-year peak above 5% last week, hitting 3.94% yesterday. The greater the duration, the less the yields collapsed further out along the curve. Real yields fell sharply, with the closely monitored 10-year falling to 1.16% from the high seen last week at 1.72%. This is significant for the price of gold. Real yields for a given duration are the nominal yield less the market-priced inflation rate.

The decline in returns from other investments may benefit gold because it is a non-interest bearing asset. The OVZ index is a measure of gold volatility, much like the VIX index is a gauge of market-priced volatility for the S&P 500. It is not unexpected that it has increased during the current precious metals rally as markets rebalance after the most recent disruptions. The 1-month 25 delta risk reversal has shot up in the gold futures market. This suggests that the market may be more eager to purchase gold calls than gold puts, which may be an indication that demand for assets perceived as safe-haven investments is increasing.

The US CPI report that will be released later today might not have the same effect on Fed rate hike forecasts that it would have had if the banks hadn’t collapsed. Instead of the anticipated 50 basis point move that was priced in last week, the interest rate market now assigns a 70% chance of a 25 basis point increase. If CPI prints below forecasts of 0.4% month-on-month for February, it may see the chance of a raise in rates by the Fed next week deteriorate. This might result in pressure on the US Dollar, which might make bullion more alluring.

USDCAD Analysis

USDCAD is moving in the Descending channel and the market has reached the lower high area of the channel.

USDCAD is consolidation at the top level in the markets, Bank of Canada Governor Tiff Mackhlem said last week no change in the interest rate due to inflation being under control, Canadian Labor Markets increased higher of unemployment, if this condition worsens then CAD CPI data will rise in the markets. The Bank of Canada will then consider the rise in market interest rates.

In the early European session, the USD/CAD pair is encountering resistance as it attempts to extend its recovery above 1.3740. Until the publication of United States Consumer Price Index (CPI) data, the Canadian dollar is anticipated to perform in a range. Previously, the asset rebounded from a five-day low of 1.3677 as investors grew anxious ahead of the US inflation report and the demand for safe-haven assets increased. Below 104.00, the US Dollar Index (DXY) is exhibiting back-and-forth movement. Next week’s interest rate decision by the Federal Reserve (Fed) will be influenced by the release of US Inflation data, which is scheduled for next week. It appears that the USD Index is gaining strength to extend its recovery as the publication of US Inflation data will pave the way. S&P500 futures are attempting to preserve gains made during the Asian trading session.

As a result of the Silicon Valley Bank (SVG) collapse, risk appetite remains subdued and global equities continue to underperform. The yield on 10-year US Treasury bonds has rebounded to near 3.57 percent as investors anticipate that US inflation data will increase the demand for safe-haven assets.The primary catalyst of the week, US inflation, will be released on Tuesday and is anticipated to produce a flurry of forex market activity. An acceleration in U.S. inflationary pressures cannot be ruled out given the resiliency of the overall demand, the strength of employment bills, and the optimistic labor market. The US Bureau of Labor Statistics reported last week that the number of payrolls produced by the US economy in February increased significantly more than anticipated. The Jobless Rate increased to 3.6%. And, Average Hourly Earnings increased by 4.6%, which was less than the 4.7% increase that was expected.

The US labor market appears positive despite a rise in the unemployment rate because businesses are consistently ramping up their hiring efforts. In addition, employment expenses continue to rise, indicating that households are able to induce inflation once more. Analysts at Wells Fargo anticipate “another monthly increase of 0.4% in the overall CPI in February, which would put the annual rate at 6.0%.” We still anticipate that inflation will gradually decline, but the process will likely be choppy and time-consuming. Despite some improvement in the trajectory of price growth over the past couple of quarters, prices are still rising well above the Fed’s 2% target, and the tight labor market suggests that there are still inflationary pressures that could prevent a full return to 2% inflation.

The present monetary policy is sufficiently restrained by it to keep Canadian inflation in check, according to the Bank of Canada (BoC). In March, Governor Tiff Macklem of the Bank of Canada (BoC) decided to enable the current monetary policy to demonstrate its potential. Nonetheless, an unexpected rise in the employment rate and an increase in the employment cost index suggest that inflation could be rekindled. In addition to maintaining the status quo on monetary policy, Bank of Canada Governor Tiff Macklem left the door open for additional interest rate hikes in the event that inflation exceeds expectations. In the meantime, oil prices have declined as the market anticipates a decline in demand for the commodity. Notably, Canada is the leading oil exporter to the United States, and lower crude prices would have an effect on the Canadian dollar.

USDCHF Analysis

USDCHF has broken the Descending channel and the market has retested the broken area of the channel.

The US Dollar has declined against the Swiss Franc over the past two days due to the collapse of SVB Bank and Signature Bank. According to Reuter’s polls, there is now only a 60% chance of a 25bps rate hike next week and a 30% chance of a hiatus.

US Dollar is now dependent on today’s US CPI data release; if it comes in higher, the FED may raise interest rates; if it comes in lower, the FED may halt this month and skip to next month.

The Swiss Franc benefited from funds transferred from crisis markets to protect markets such as the Swiss Franc, Euro, British Pound, Australian Dollar, New Zealand Dollar, and Japanese Yen.

The USD/CHF fluctuates around the intraday peak for the first time in five days prior to Tuesday’s European session. In doing so, the Swiss Franc (CHF) pair tracks the US Dollar’s most recent corrective rebound amid a recovery in US Treasury bond yields prior to the release of Consumer Price Index (CPI) data. It should be noted, however, that the recent bearish market sentiment encircling the Federal Reserve (Fed) appears to test buyers prior to the release of the most important US data.

In spite of this, US 10-year Treasury bond yields post modest gains of approximately 3.58% after rebounding from the monthly low of 3.418%, while the two-year counterpart yields post modest gains of approximately 4.19% after rebounding from the lowest levels since September 2022. The yields on two-year Treasury bonds in the United States fell the most since 1987 the day before. Despite the US government’s denials, a significant decline in US Treasury bond yields could be attributed to the concerns generated by the Silicon Valley Bank (SVB) and Signature Bank failures.

Regarding Fed bets, CME stated, “Traders see a 33% chance that the Fed will hold rates this month, while market pricing indicates rate cuts as early as June.” On the same line, Reuters reported that US Fed Fund Futures have priced in a 69% chance of a 25-bps raise at next week’s Fed policy meeting, along with a greater than 30% chance of a pause. Prior to the SVB collapse, the market was poised for a 50-bps increase last week, according to the news. Wall Street closed mixed, as did the Asia-Pacific region, while S&P 500 Futures reversed a three-day downtrend by rebounding off their lowest levels since the beginning of January. In the future, the US CPI will be more significant for USD/CHF traders, as the Fed’s wagers have already been reversed. According to market expectations, the headline US CPI is likely to decrease to 6.0% YoY from 6.4% previously, while CPI excluding Food & Energy is likely to decrease to 5.5% YoY from 5.6% previously.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

This week’s ECB Monetary Policy Meeting is expected to result in an increase in interest rates of 50 basis points, which will provide significant support for the Euro against other currency pairs. As a result of the collapse of the SVB Bank, it is now appropriate for the Euro to make ground against the US Dollar. Due to the higher Euro CPI and the rate increase, it is critical to fight inflation and bring it down.

As the USD selloff persisted, the EURUSD rallied overnight, reaching a new one-month high of 1.0737. The currency strength chart below, as the European session begins, shows the safe-haven dollar weakening as risk mood improves, weighing on EURUSD.The EURUSD has retreated slightly in the European morning, flirting with 1.0700 once more as markets digest the SVB news and emergency measures taken by US officials to restore confidence in the banking sector. Regulators verified that customers would be able to access their deposits on Monday, while also establishing a new facility to provide banks with access to emergency funds.

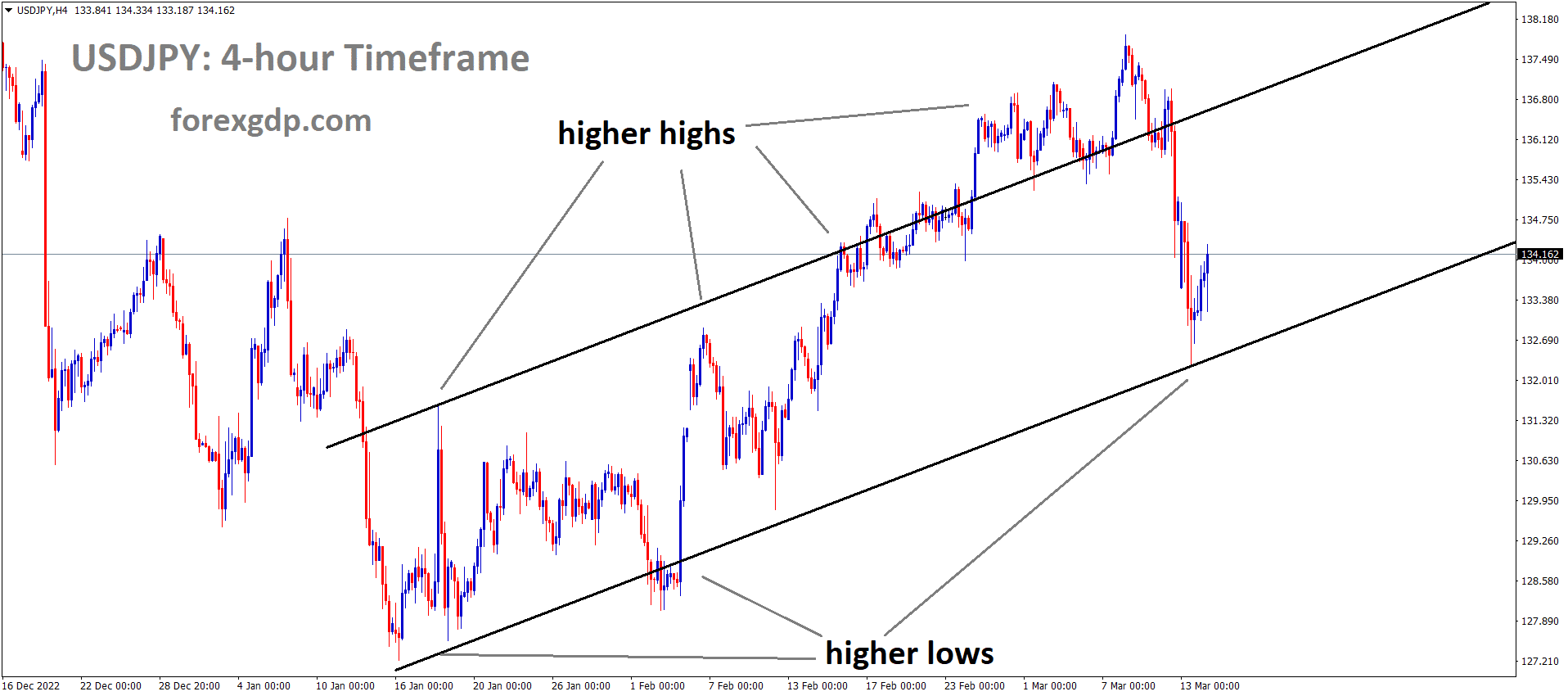

EURJPY Analysis

EURJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Since market participants reduced their estimates for a 50bps Federal Reserve rate hike at its March meeting on Friday, the upside potential for the EURUSD still appears to be more promising going forward. In comparison, the European Central Bank (ECB) will announce its interest rate decision on Thursday, with market participants expecting a 50 basis point increase. This rhetoric has been echoed by ECB President Christine Lagarde and a few ECB policymakers in recent weeks, as inflation in the Eurozone stays uncomfortably high.There are no major data releases scheduled for today, but there are some big events coming up this week, including US inflation data and, of course, the ECB rate decision. Both are expected to be driving forces for EURUSD price action in Q2 2023.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

In the UK, the December job change was 65K instead of the 52k expected, and the January unemployment rate was 3.7% instead of the 3.8% forecast.

The UK labor market is still improving, strengthening GBP relative to other currency combinations. Gasoline prices are likely to be eliminated from the UK Budget, which was given this week by UK Chancellor Jeremy Hunt. This is because it is estimated that the cost of gasoline prices will drop from GBP13 billion to GBP2 billion. The SVB Bank collapse causes market panic selling, and HSBC UK declares that buying the SVB UK branch is a strategic acquisition for its franchise business in the UK.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

NAB business conditions decreased to 17 from 18 versus 21 anticipated, while NAB business confidence decreased to -4.0 from 0.0% predicted and 6.0% previously. This information makes AUD weaker against other currencies, and yesterday’s modest AUD rally following the collapse of SVB makes the USD weaker on the market. Due to China’s support for Russia during the Ukraine conflict through under-relationships, China and Russia’s cooperation causes a small rift in Australia and China’s relationship.

As traders prepare for the US inflation figures early on Tuesday, the AUD/USD declines to 0.6650, down 0.25% on the day. The most recent decline in the price could also be attributed to market concerns about China and Russia, as well as disappointing data from Australia. In spite of this, the Aussie-Dollar pair rose the most since early February the day before due to widespread US Dollar weakness. The AUD/USD bulls were able to take a respite as a result of the National Australia Bank’s (NAB) negative sentiment indices for February. It should be noted that the NAB Business Conditions index decreased to 17 from 18, compared to 21 market expectations, while the NAB Business Confidence index plummeted to -4.0 compared to 0.0% analyst expectations and 6.0% previously.

In other regions, US Treasury bond yields post modest gains after a sharp decline the previous day. On the same line is the most recent minor increase in S&P 500 Futures prices. Consequently, US 10-year Treasury bond yields oscillate around 3.56%, having rebounded from the monthly low of 3.418%, whereas the two-year counterpart yields have rebounded from the lowest levels since September 2022 to post modest gains of approximately 4.05% as of press time. In addition to market positioning and NAB data, AUD/USD traders may have attributed the previous day’s gain to US inflation expectations before recording the most recent decline. According to the 10-year and 5-year breakeven inflation rates from the Federal Reserve Bank of St. Louis (FRED), US inflation expectations fell to their lowest levels since early February. In doing so, the inflation indicators for the five-year and 10-year horizons fell for the fifth and sixth consecutive days.

Moreover, the recent revival in US Treasury bond yields enabled the AUD/USD pair to consolidate the gains made as a result of US banking regulators’ defense of Silicon Valley Bank (SVB) and Signature Bank.

In spite of this, the damage to Federal Reserve (Fed) wagers appears to challenge AUD/USD bears ahead of February’s crucial US Consumer Price Index (CPI) data. According to the most recent information from Reuters, the US Fed Fund Futures have priced in a 69% chance of a 25-bps raise at the Fed policy meeting next week, with a greater than 30% chance of a pause. Reuters reported that the market was positioned for a 50-bps increase prior to the SVB collapse last week. On the same line as the CME, which noted that traders see a 33% probability that the Fed will hold rates this month, market pricing indicates that rate cuts are expected as early as June. In the future, the US CPI will be essential for intraday direction, but investors should pay more attention to risk catalysts and yields. Consequently, the US CPI is likely to decline to 6.0% YoY from 6.4% previously, while the CPI excluding food and energy may fall to 5.5% YoY from 5.6% previously.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Fourth Quarter GDP data for New Zealand is anticipated to decline by 0.2% compared to 2.0% in the third quarter, and Annual GDP (4Q) has increased by 3.3%, which is lower than the 6.4% predicted in the previous month.

During the Asian session, the NZD/USD pair has extended its correction below 0.6220. As investors grow anxious in advance of the United States Consumer Price Index (CPI) data release, the New Zealand dollar is anticipated to exhibit extreme volatility in the near future. After an unexpected increase in the number of payrolls generated in the US economy in February and a less-than-anticipated increase in Average Earnings, it is not possible to rule out an increase in inflationary pressures. However, the consensus indicates a decrease in the headline CPI to 6.0% from 6.4% in the previous release. In addition, core inflation, which excludes crude and food prices, is anticipated to decrease to 5.5% from 5.6% in the previous report.

US Index has recovered to near 103.80, which appears to be a retracement after a steep decline. MUFG Bank economists believe that only a significant favorable surprise in US inflation could propel the US Dollar forward. S&P500 futures are indicating a decent recovery as investors disregard the volatility associated with the collapse of Silicon Valley Bank (SVB). In addition, demand for US government bonds has decreased, resulting in a rise in 10-year US Treasury yields above 3.5%. Regarding the New Zealand Dollar, investors await the publication of Gross Domestic Product (GDP). (Q4). According to estimates, the New Zealand economy has shrunk by 0.2% compared to the 2.0% growth seen in the third quarter. The annual GDP (Q4) grew by 3.3%, which is less than the previous expansion of 6.4%.

Crude Oil Analysis

Crude Oil is moving in the Descending channel and the market has reached the horizontal support area of the minor Box pattern.

Due to the failure of the Silicon Valley bank, crude oil prices dropped by 2.55% yesterday and by 3.3% since last Wednesday. Because oil is a significant export good, falling crude oil costs make the Canadian dollar weaker.Investors anticipate that the US FED will reduce interest rates by 150 basis points by year’s end, which would cause the US dollar to keep falling in the markets.

In response to last week’s failure of Silicon Valley Bank, WTI crude oil prices decreased 2.55% on Monday as market turbulence stayed high. The commodity’s loss since last Wednesday is about 3.3%. Crude oil that is linked to sentiment has been vulnerable and could continue to be so in the days, weeks, and months ahead as traders gauge the probability that the US economy will experience a recession. Investors punished regional bank stocks on Monday despite the government’s efforts to boost trust in the financial system.

But a closer look shows that Monday’s market reaction seems to put much more weight on expectations of a Federal Reserve turn than worries about a recession. (for now). In actuality, dealers have already factored in rate reductions of about 150 basis points by this year’s fall. In reaction, traders flocked to tech stocks and the haven-linked US Dollar fell. The Dow Jones underperformed the Nasdaq 100. Crude oil prices continued to decline during Tuesday’s Asia-Pacific trading period, with WTI falling nearly 1.25% by 3 GMT. The market volatility might worsen over the next 24 hours. All eyes are on the US CPI data at 12:30 GMT. Inflation is anticipated to decrease even more in February, from 6.4% to 6.0% y/y. Recall that the January print was stickier than expected. Another unexpectedly strong print could revive expectations of a Fed rate increase, putting crude oil at risk.

Don’t trade all the time, trade forex only at the confirmed trade setups.

🎁 80% NEW YEAR OFFER for forex signals. LIMITED TIME ONLY Get now: forexgdp.com/offer/