XAUUSD Analysis

XAUUSD Gold Price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The last three months have seen a decline in gold prices, and the upcoming quarter is expected to show similar trends. The US Treasury yields are higher compared to non-yielding assets as a result of central banks raising interest rates.

Gold prices failed to maintain their upward trend from the first three months of the year in the second quarter and were on course to decline by more than 3% by the end of June. Rising yields and a reevaluation of monetary policy expectations in response to sticky inflation both in the U.S. and Europe put pressure on the yellow metal. The chart below demonstrates how, following the brief slump brought on by the unrest in the banking sector back in March, the Federal Reserve’s tightening roadmap for 2023 repriced sharply higher and quickly. Nominal yields experienced a significant rebound as sentiment increased, with short-dated ones on the verge of surpassing their March peak. Real yields in the United States, a true indicator of borrowing costs and the kryptonite of gold, also increased, hurting rate-sensitive assets. The chart below illustrates how bullion declined as the U.S. 10-year Treasury Inflation-Protected Security increased. The chart shows XAU/USD on an inverted scale to better show the correlation. In the near future, market dynamics will not be in gold’s favour. For instance, the Fed’s hawkish guidance, which assumes 50 basis points more tightening through the end of the year and higher rates for longer, is likely to have a negative impact on precious metals as summer approaches. Gold will continue to be vulnerable due to the upward bias in nominal and real yields, which suggests that additional losses may be impending.

The outlook, though, will not be negative forever. Cracks will start to show as the system is forced to absorb the FOMC’s aggressive hiking campaign, just as they did in March when two regional banks failed. Although the US economy has fared remarkably well, it will struggle to sustain rates above 5.0% for an extended period of time, especially at this point in the business cycle. Traders will start pricing in aggressive rate cuts by the central bank once signs of recession are obvious and difficult to ignore in the data, sending the Treasury curve tumbling lower and volatility soaring. As of right now, gold prices should be supported by declining yields and market volatility, which will pave the way for a significant rebound later in the year. Timing the sequence of events could be challenging, but the steady increase in U.S. jobless claims, a leading indicator, indicates that the economy might not yet be about to collapse under the weight of an overly restrictive monetary policy for more than a few months. According to these hypotheses, gold may experience some volatility early in the third quarter before regaining its composure by mid-summer.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The BoJ’s dovish policy stance will be supported by Japan’s Tankan Manufacturing survey, which is predicted to lower inflation. Japan’s Manufacturing PMI for June came in at 49.8, which was in line with expectations. To control the Yen depreciation against foreign pairs, BoJ’s intervention on the forex market is something to fear.

In the midst of a slow start to yet another crucial trading week, the USDJPY oscillates around 144.60 as it searches for new cues to defend intraday gains. This occurs amid conflicting risk catalysts and dismal Japan data, reversing the previous day’s decline from the highest levels seen since November 2022. The Bank of Japan’s (BoJ) dovish monetary policy bias appears to be supported by Japan’s Tankan Manufacturing Survey for the second quarter (Q2) of 2023 because it anticipates low inflation. The final negative reading of Japan’s Jibun Bank Manufacturing PMI for June, which came in at 49.8, matching initial forecasts, is another factor that may have weighed on the USD/JPY exchange rate. The market’s worries about Japan intervening elsewhere lessen as a result of the Yen pair’s decline from 145.07 the day before. However, the USDJPY bulls are also encouraged by the conflicting reports regarding China and the cautious atmosphere ahead of this week’s important data and events, including the minutes of the Federal Open Market Committee’s monetary policy meeting and the US jobs report. It is important to note that the market had mixed reactions to US Treasury Secretary Janet Yellen’s trip to China from July 6 to July 9. Although the news appears to be good on the surface, the details are less impressive, as US Treasury Secretary Yellen is expected to raise concerns about the Uyghur Muslim minority’s human rights violations, China’s recent decision to forbid the sale of Micron Technology memory chips, and Chinese actions against foreign due diligence and consulting firms, according to Reuters.

On the other hand, the US Personal Consumption Expenditure (PCE) Price Index, the preferred inflation indicator of the Federal Reserve (Fed), came in for May at 0.3% MoM and 4.6% YoY versus market expectations of reprinting the 0.4% and 4.7% figures for monthly and yearly prior readings. The key inflation figures thus represented the smallest yearly gain in the previous six months. Additionally, the Personal Consumption Expenditure (PCE) Price for the first quarter of 2023 decreased to 4.1% QoQ from 4.2% expected and prior, while the Pending Home Sales declined to -2.7% MoM for May from 0.2% expected and -0.4% prior (revised). As a result, the Fed Chair Jerome Powell’s support for “two more rate hikes in 2023” is questioned by the slowing of consumer spending and the ease of inflation, which pressures USD/JPY buyers. S&P500 Futures struggle to match the positive Wall Street performance amid these plays, while US Treasury bond yields have recently been in decline. The US ISM Manufacturing PMI for June will now join the risk catalysts in guiding intraday moves, but major focus will be placed on the Fed Minutes and the US Nonfarm Payrolls report for a clear indication.

USDCAD Analysis

USDCAD is moving in the Box pattern and the market has reached the resistance area of the pattern.

The USDCAD pair begins the new week on an upbeat note after a strong Friday two-way price swing, and it keeps its bid tone, circling around the mid-1.3200s throughout the Asian session. On Monday, the US Dollar attracted some buyers due to growing expectations that the Federal Reserve will continue to tighten its monetary policy. This is thought to be a major factor supporting the USDCAD pair. Recall that Fed Chair Jerome Powell reiterated last week that interest rates may still need to rise by as much as 50 basis points by the end of this year. Additionally, the odds of a 25 bps lift-off at the upcoming FOMC policy meeting in July are nearly 85% according to market pricing, and the bets were reinforced by the fact that the US PCE Price Index is still significantly higher than the 2% inflation target. In fact, according to a report released on Friday by the US Bureau of Economic Analysis, the annual PCE Price Index slowed in May from 4.3% to 3.8%, and the core measure—which excludes the volatile food and energy components—moved lower from 4.7% to 4.6%. However, more information revealed that US consumer spending slowed significantly in May, which is preventing USD bulls from making aggressive bets and limiting any appreciable upside for the USDCAD pair. Meanwhile, Crude Oil prices maintain the significant recovery gains from last week and have little impact on the commodity-linked Loonie.

Crude oil Analysis

Crude oil Price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The Bank of Canada raised interest rates again at its upcoming meeting as a result of lower consumer inflation for the month of May and a drop in Canadian GDP last week. Because of China’s Covid-19 recovery, the opening of manufacturing zones, and the relaxation of lockdown regulations, crude oil prices have increased.

However, the weaker Canadian Dollar and support for the USDCAD pair may persist as a result of May’s domestic consumer inflation, which increased at its slowest rate since June 2021. However, the Bank of Canada is still free to raise interest rates in July given the monthly Canadian GDP print that was released on Friday. In turn, this makes it wise to hold off on setting up positions for the pair’s recent bounce from the 1.3115 region, or its lowest level since September 2022, touched last week, until there is strong follow-through buying. The release of the ISM Manufacturing PMI later on Monday during the early North American session is the first of several significant US macroeconomic data points scheduled at the start of a new month. The FOMC meeting minutes on Wednesday and the closely watched US monthly employment figures, commonly referred to as the NFP report on Friday, will continue to be the main points of attention. This will fuel demand for the CAD and make this a busy week for the USDCAD pair, along with Canadian jobs data and oil price dynamics.

EURCAD Analysis

EURCAD is moving in the Box pattern and the market has fallen from the resistance area of the pattern.

Inflation data for Germany were 6.4% (YoY) in June compared to 6.1% in May and 6.3% expected. In order to combat rising inflation readings and anxieties brought on by Germany’s recession, the ECB Central Bank must raise interest rates further.

Although it lacks direction, the EURGBP remains lower near 0.8590, and the bears are still in charge going into Monday’s European session. In doing so, the cross-currency pair allays concerns that the European Central Bank (ECB) faces numerous difficulties in defending its hawkish bias while also defending a recent positive headline from the UK. The UK Times reported that British Health Secretary Steve Barclay was prepared to give doctors a larger pay rise and called for the suspension of consultant strikes in order to resume negotiations. The National Health Services chief issued a warning that the disruption to routine healthcare would become “more significant” this month, which coincided with Barclay’s admission, according to the news. It should be noted that the UK’s employment report showed a mixed picture and suggested that the country’s labour shortage may be easing. In contrast, the Consumer Price Index (CPI) readings for Germany’s inflation increased to 6.4% YoY in June from 6.1% in May and 6.3% expected. In a similar vein, the Harmonised Index of Consumer Prices (HICP), the European Central Bank’s (ECB) preferred inflation gauge, increased to 6.8% on an annual basis from 6.3% previously and 6.7% market forecasts. Additionally, the preliminary HICP inflation rate for the Eurozone increased to 0.3% MoM from 0.0% expected and from prior readings, while the annual figures decreased to 5.5% from 5.6% market expectations and 6.1% previous readings.

It is important to note that the European Central Bank officials made an effort to defend their preference for rate increases, but weaker inflation data and looming concerns about Germany’s impending recession prevent markets from believing them, which in turn drags down the price of the EURGBP. The price of the pair is alternatively restrained by UK inflation data and the hawkish stance of Bank of England policymakers. Moving forward, it will be crucial to keep an eye on the final Eurozone and UK PMI readings for the month of June to determine the direction of the EUR/GBP pair. Watch out for central bankers’ remarks and risk-creating factors.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

This week’s Swiss inflation data is expected to come in at 1.8%, down from the previous reading of 2.2%. The SNB Chairman has already stated that additional rate increases will be implemented to curb Swiss Zone inflation readings.

After a brief recovery move to near 0.8957 in the Asian session, the USDCHF pair has since declined. Prior to significant economic events, the Swiss Franc asset is anticipated to continue its downward trajectory after breaching the critical support level of 0.8930. As investors become more cautious ahead of the start of the quarterly results season and the release of the United States Manufacturing PMI data (June), S&P500 futures are exhibiting choppy movements in early Europe. Investors are concerned that banking stock quarterly results may be muted due to tight credit conditions and that technology stock prices may continue to decline due to expectations of weak guidance. Due to the generally positive market sentiment, the US Dollar Index (DXY) has encountered barriers around 105.00. By year’s end, investors believe that the Federal Reserve (Fed) will not raise interest rates more than once. Jerome Powell, the Fed’s chairman, has already stated that two modest interest rate increases are necessary.

The release of the US Manufacturing PMI at 14.00 GMT will continue to be the topic of discussion on Wall Street later in the day. Manufacturing PMI is expected to rise to 47.2 from its previous reading of 46.9, according to the preliminary report. This suggests that the economic data would keep contracting for another seven months.

GBPCHF Analysis

GBPCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Investors are anticipating June inflation data as it relates to the Swiss Franc. Annual Consumer Price Index data is projected to soften to 1.8% from the 2.2% reported in the previous release. Price pressures are greatly impacted by the Swiss National Bank’s (SNB) increased interest rates. Thomas J. Jordan, the chairman of the SNB, has already stated that additional rate increases are anticipated.

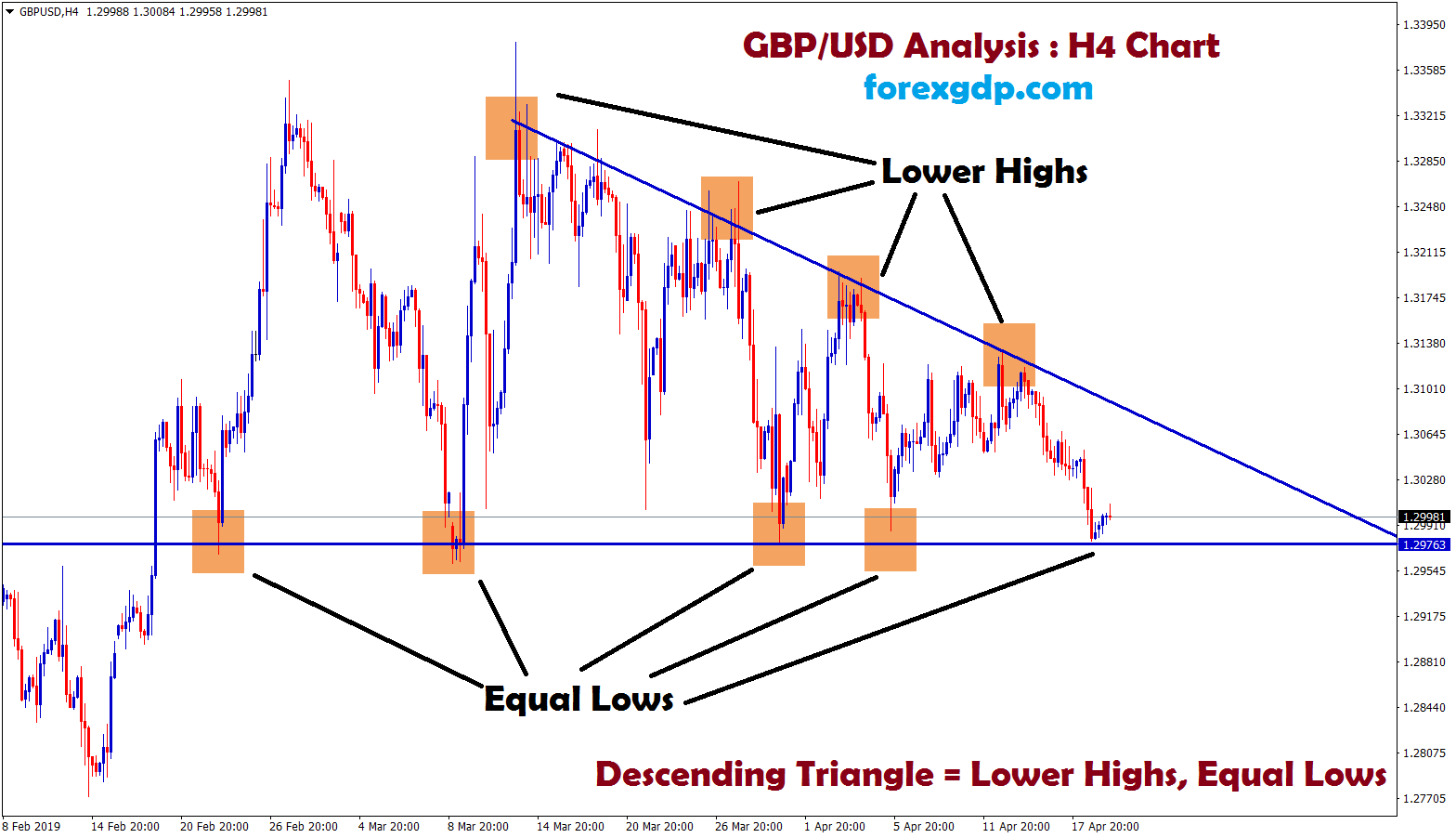

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

With mixed labour market data and improving labour market conditions, UK growth is in danger of entering a recession. GDP for Q1 came in at 0.10% versus 0.20% expected. To safeguard people’s welfare and access to health benefits, the UK Health Department is likely to increase doctors’ salaries.

Bulls are looking for more cues to support the run-up from the previous day in the face of a sluggish start to the crucial week as GBPUSD flirts with the round number of 1.2700. However, the recent inaction of the Cable duo may also be attributed to conflicting headlines regarding the employment and growth situations in the UK as well as a lack of a clear market response to the news of the US-China talks. The UK Times reported that British Health Secretary Steve Barclay was prepared to increase doctors pay raises and called for an end to consultant strikes so that talks could resume. The National Health Services chief issued a warning that the disruption to routine healthcare would become “more significant this month, which coincided with Barclay’s admission, according to the news. It should be noted that the UK’s employment report showed mixed results and suggested that the labour shortage may be easing. A senior US Treasury official and the Chinese Treasury Department have both recently confirmed that US Treasury Secretary Janet Yellen will visit China from July 6 through July 9. Although the news appears to be good on the surface, the details are less impressive, as US Treasury Secretary Yellen is expected to raise concerns about the Uyghur Muslim minority’s human rights violations, China’s recent decision to forbid the sale of Micron Technology memory chips, and Chinese actions against foreign due diligence and consulting firms, according to Reuters.

It should be noted that the market’s risk-on sentiment was sparked by Friday’s weaker US inflation hints, which also supported the rise of the GBP/USD pair. Nevertheless, the Cable pair fell for the past two weeks in a row due to concerns about the UK recession. Nevertheless, according to the most recent readings, the UK’s first-quarter 2023 GDP was in line with 0.1% QoQ and 0.2% YoY forecasts. The US Personal Consumption Expenditure (PCE) Price Index, the Federal Reserve’s (Fed) preferred inflation indicator, poked hawkish expectations from the US central bank on Friday with the smallest yearly gain in six months. Following a flurry of Fed statements earlier in the past week, the same combined absence of any significant hawkish remarks from US central bank officials favoured the GBPUSD bulls. In this environment, S&P500 Futures continue to rise by tracking positive Wall Street performance, while US Treasury bond yields continue to rise. The final UK S&P Global/CIPS Manufacturing PMI readings for June will be released before the US ISM Manufacturing PMI readings for the same month, guiding intraday movements of the GBP/USD pair. The minutes from this week’s Federal Open Market Committee meeting on monetary policy and the US jobs report, however, will receive most of the attention.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Building approvals in Australia reached 20.6% as MoM’s May month report strengthened the AUD against the USD. China Caixin Manufacturing PMI was 50.5 instead of the predicted 50.0.

The Australian Dollar gained ground before falling back today as growth-oriented assets moved higher overall to start the week. Australian building approvals increased dramatically in May by a staggering 20.6% month-over-month, far exceeding the 3.0% expected and -8.1% prior. Although the probability of an RBA rate hike tomorrow is low according to interest rate markets, these numbers might add some zing to the monetary policy meeting. The news caused the Australian Dollar to jolt higher, but it had trouble keeping up. Following Wall Street’s significant gain on Friday, APAC stocks are a sea of green. In advance of a holiday-impacted start to the week there, some encouraging economic news out of North America gave markets the boost they needed. The improvement in mood was further aided by today’s Caixin PMI manufacturing data from China, which came in at 50.5 as opposed to the anticipated 50.0.

Another sign of a potential thawing in the occasionally icy relationship between the world’s two largest economies is the announcement by Washington that US Treasury Secretary Janet Yellen will visit China this week. Since testing lower last week, crude oil has had a relatively quiet session as it works its way back up. While the Brent contract is just over US$ 75 bbl, the WTI futures contract is close to that price. The price of spot gold, which is currently trading close to US$ 1,920, has also barely changed. In the event that higher Treasury yields continue, as they did on Friday, the precious metal may suffer. Looking ahead, a string of European PMI readings may capture the market’s interest before the US ISM manufacturing data.

Don Farrell, the minister of trade for Australia, stated that he anticipated more declarations on expanding trade with China soon. Australian Agriculture Minister Murray Watt stated that “relations between Australia and China have gradually warmed” in an interview with a regional public broadcaster ABC over the weekend. Watt made his remarks following his first encounter with his Chinese counterpart since 2019.

NZDUSD Analysis

NZDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Due to the US PCE index having a reading that was lower than anticipated last week, the NZD Dollar is likely to have risen from the support area. NZD gains from the US Dollar’s minor corrections from highs.

In response US bond yields retreated from daily highs as investors seemed to be betting on a less aggressive Fed. In that sense, the 2-year Bond yield peaked at 4.93%, its highest level since March 9, retreating to 4.85%, while the 5 and 10-year rates fell to 4.13% and 3.83%.

However, more evidence of inflation deceleration must be seen for the Fed to pivot from its hawkish stance. As for now, according to the CME FedWatch tool market is 86% sure of a 25 basis points (bps) hike on July 26 and still trying to figure out when the second hike Jerome Powell hinted will come.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/