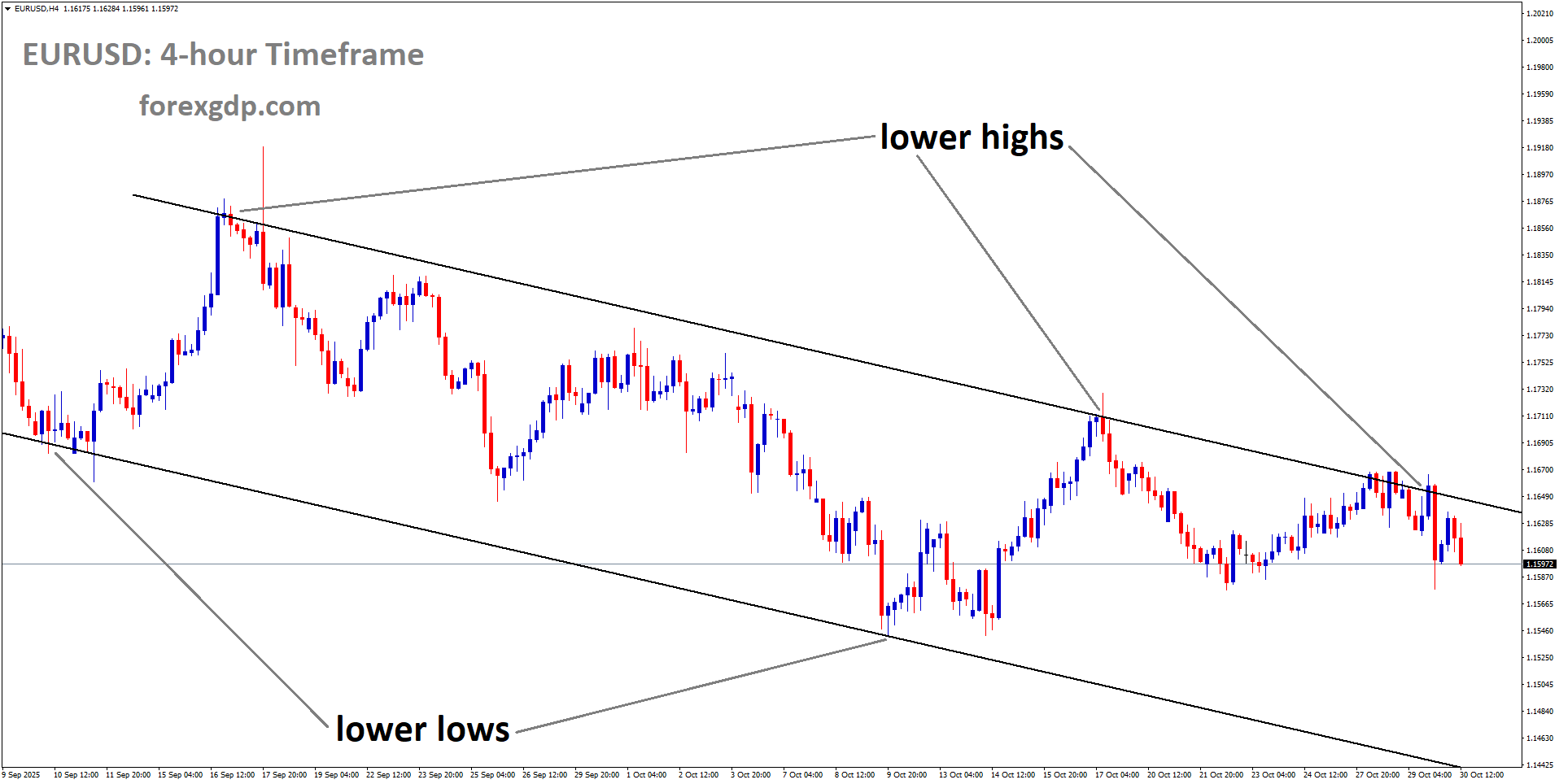

EURUSD is moving in a downtrend channel

EURUSD Climbs Gently as Eurozone Economic Momentum Lifts Market Mood

The euro has made a modest recovery against the US dollar, showing some signs of strength after a challenging week. Although it managed to bounce above the 1.1600 level, it still lacks strong upward momentum. Investors around the world are cautiously optimistic following positive developments in the Sino-US trade relationship, while also keeping a close watch on important Eurozone economic data and the European Central Bank’s (ECB) upcoming policy decision.

A Fresh Wave of Optimism: Trade Talks Bring Temporary Relief

The recent trade agreement between the United States and China has brought a sigh of relief to the global market. Investors have been waiting for months to see whether both nations could find common ground after years of tariffs, trade restrictions, and political tension. According to recent reports, US President Donald Trump described his meeting with Chinese President Xi Jinping as “amazing,” highlighting key agreements that could help stabilize trade relations between the two largest economies in the world.

Under this deal, the United States agreed to reduce tariffs on several Chinese imports, while China promised to increase purchases of American agricultural products and ensure that its rare earth exports continue uninterrupted. Moreover, China also committed to curbing the trade of fentanyl, a move welcomed by the US government.

Although President Xi Jinping’s comments were less enthusiastic, he confirmed that both sides reached a “consensus” on important economic and trade matters. This diplomatic progress helped boost investor confidence, even though the market response was moderate. Traders remain cautious, knowing that previous trade deals have seen similar optimism fade quickly due to renewed disputes or unfulfilled promises.

Eurozone Economic Data Brings Encouraging Signs

A Better-Than-Expected Growth Rate

In Europe, there’s a growing sense of optimism following the release of encouraging economic data. The latest preliminary GDP report for the Eurozone showed a 0.2% increase in the third quarter, surpassing the 0.1% growth that analysts had predicted. While the growth remains modest, the fact that it exceeded expectations gave the euro a small boost.

Compared to the previous quarter, the improvement is a positive sign that the European economy may be stabilizing after months of sluggish performance. Year-on-year, the region’s economy expanded by 1.3%, which, although slightly lower than the previous 1.5%, still beat projections of 1.2%.

Stronger Business Confidence Across Sectors

Confidence levels have also improved across the Eurozone. The European Commission’s Economic Sentiment Indicator climbed to 96.8 in October from 95.6 in September, indicating that businesses and consumers are becoming more optimistic about the economic outlook.

Industrial confidence rose significantly, suggesting that manufacturing firms are beginning to recover from previous supply chain issues and declining demand. The services sector also showed better results, with sentiment increasing as consumer activity gradually strengthens. Meanwhile, the unemployment rate remained steady at 6.3% in September, matching expectations and indicating a stable labor market despite global uncertainty.

Germany Shows Early Signs of Recovery

Germany, the Eurozone’s largest economy, has been struggling for much of the year due to weak exports and industrial output. However, new figures show that its GDP remained stable in the third quarter after contracting earlier in the year. On a yearly basis, Germany’s economy grew by 0.3%, a welcome rebound after a 0.2% contraction in the second quarter. This stabilization adds another layer of support for the euro, suggesting that the overall regional outlook might be improving gradually.

The US Federal Reserve’s Decision and Market Reaction

Interest Rate Cuts Create Mixed Reactions

Across the Atlantic, the United States Federal Reserve made a widely expected decision to cut interest rates by 25 basis points. However, what caught traders off guard was the tone of Chairman Jerome Powell’s comments following the announcement. Powell made it clear that the path ahead is uncertain, stating that future rate decisions would depend on how inflation and employment data evolve.

This cautious approach led many investors to question whether another rate cut could come in December. As a result, the US dollar gained strength against most major currencies, including the euro, immediately after Powell’s press conference. Despite the Fed’s effort to support economic growth, the mixed messaging about future policy moves caused some confusion in the market.

Investors Turn to Eurozone Outlook

The temporary strengthening of the US dollar pushed the euro down earlier in the week, but recent developments have allowed it to recover some ground. Investors are now turning their attention to the ECB’s next move. Many expect the ECB to keep its deposit facility rate unchanged, but the real focus will be on the central bank’s comments regarding the future of monetary policy.

Will the ECB signal the end of its tightening cycle, or will it hint at further rate adjustments in the coming months? The answer could shape the euro’s direction for the rest of the year.

Looking Ahead: What Could Influence the Euro Next

The euro’s performance in the coming weeks will depend heavily on how markets interpret the ECB’s decision and accompanying statements. If the central bank signals that it’s done with rate hikes, traders might anticipate a more stable period for the euro. However, if policymakers suggest there’s still room for tightening or express concerns about inflation, volatility could return.

In addition, global risk sentiment will continue to play a major role. Any setback in US-China relations or new trade tensions could once again push investors toward safe-haven assets like the dollar, which would weigh on the euro. Conversely, sustained cooperation and economic growth could help the common currency strengthen further.

It’s also important to note that energy prices, consumer confidence, and inflation trends across Europe will remain key indicators of how the economy is performing in the final quarter of the year. With growth showing signs of life and unemployment steady, the Eurozone may finally be on a path toward moderate recovery.

Final Summary

The euro has shown resilience despite global uncertainty. Positive progress in US-China trade relations and stronger Eurozone economic data have given it a temporary lift, even though it still struggles to gain strong upward momentum. The Federal Reserve’s cautious tone and the upcoming ECB decision have kept traders alert, as both central banks’ policies will heavily influence currency movements in the near future.

In simple terms, the euro’s outlook appears cautiously optimistic. Growth in the Eurozone, especially in Germany, along with improved business sentiment, points to a more stable environment ahead. However, global risks and central bank decisions continue to shape investor confidence. For now, the euro remains supported by improving fundamentals, though it still has a long way to go before reclaiming strong bullish ground.

GBPUSD Weakens as Dollar Rises on Fresh Hopes of Improved US-China Economic Ties

The Pound Sterling slipped lower against the US Dollar during Thursday’s European trading session after giving up its early gains. The move came as the US Dollar regained strength, reversing its earlier decline following encouraging developments between the United States and China.

The British Pound had managed a brief recovery earlier in the day but soon lost momentum as traders shifted back toward the Greenback. This shift happened after China confirmed it would resume rare earth exports to Washington, easing one of the long-standing tensions between the two major economies. At the same time, comments from both US President Donald Trump and Chinese President Xi Jinping after their recent meeting added optimism to the global market sentiment.

Investors closely watched how this renewed diplomatic tone between the two countries would affect global trade flows. As the Dollar stabilized, the Pound came under renewed pressure, reflecting how international trade developments can quickly influence currency trends.

US-China Trade Relations Take a Positive Turn

After a long period of uncertainty, the relationship between Washington and Beijing showed signs of improvement. Following his meeting with China’s President Xi Jinping, President Trump described the encounter as “amazing”, even rating it “a 12 out of 10.” He highlighted several key outcomes that boosted market confidence.

One of the biggest takeaways was China’s decision to ease tariffs and resume the export of rare earth materials to the US — a vital component for various American industries, including technology and defense. Trump also mentioned that tariffs on Chinese imports would be reduced, signaling progress toward easing the trade war that had rattled global markets for years.

China’s commerce ministry supported this sentiment by announcing it would suspend export control measures for a year and expand agricultural trade with the US, including immediate purchases of soybeans. These steps were viewed as an olive branch, indicating both nations were moving toward more stable trade relations.

Such developments naturally bolstered the US Dollar, as investors viewed the American economy as better positioned to benefit from smoother trade conditions. Meanwhile, the Pound struggled to maintain its footing as traders awaited key policy signals from the Bank of England.

The Fed’s Rate Cut Sparks Mixed Reactions

The Federal Reserve’s latest decision added another layer of complexity to the market dynamics. On Wednesday, the Fed cut interest rates by 25 basis points, marking its second rate reduction of the year. The move brought the benchmark range down to 3.75%–4.00%, aligning with expectations that the central bank would take a more cautious stance amid mixed economic indicators.

The rate cut came on the back of several economic challenges. The US labor market showed signs of cooling, job creation was slowing, and the prolonged federal government shutdown had impacted confidence. Moreover, the recent Consumer Price Index (CPI) data suggested that the inflationary pressure caused by tariffs was not as strong as initially feared.

Fed Chair Jerome Powell described the decision as an act of “risk management,” explaining that the Fed wanted to support growth while preventing further slowdown. However, what caught investors’ attention was Powell’s comment that further rate cuts were not guaranteed. He indicated that the Fed might hold rates steady in the coming months, as inflation still remained slightly above the desired level.

GBPUSD is breaking the lower low area of the downtrend channel

This unexpected shift in tone helped the US Dollar recover quickly. While lower rates generally weaken a currency, Powell’s firm stance reassured investors that the central bank was not rushing into aggressive monetary easing. As a result, traders reduced their expectations for another rate cut in December.

According to the CME FedWatch Tool, the probability of the Fed holding rates unchanged in December rose dramatically to around 70%, compared to just 9% earlier in the week. This shift reflected growing confidence that the Fed would take a “wait-and-see” approach before making further moves.

Investors Turn Focus Toward the Bank of England

While the US monetary policy took center stage, attention in the UK turned toward the upcoming Bank of England (BoE) meeting scheduled for next week. After the Pound’s sharp drop to near six-month lows, traders are now trying to gauge whether the BoE will follow in the Fed’s footsteps and cut interest rates.

According to analysts at Goldman Sachs, the BoE could announce a 25-basis-point rate cut, bringing rates down to 3.75%. The firm’s outlook turned dovish as the UK’s labor market softened and wage growth slowed in recent months. With inflation cooling and consumer spending showing weakness, Goldman Sachs believes the central bank may use this opportunity to support the economy through a modest rate adjustment.

However, not everyone agrees with that view. A recent Reuters poll of economists suggests that the BoE might hold rates steady for the rest of the year and delay any rate cuts until early 2026. Many economists expect the central bank to monitor global economic developments and domestic data before deciding on further policy actions.

The divided expectations highlight how uncertain the UK’s economic outlook remains. With inflation showing signs of easing but growth still fragile, the BoE faces a delicate balancing act between stimulating the economy and maintaining financial stability.

For the Pound, this uncertainty means volatility could persist in the short term. Traders are likely to respond sharply to any change in tone or policy hint from BoE officials.

Global Market Mood: A Tug of War Between Optimism and Caution

Overall, the financial markets remain caught between optimism over improved US-China relations and caution about the direction of global monetary policy. The Fed’s latest rate decision, combined with upbeat trade developments, initially supported the Dollar. However, investors remain alert to future policy shifts and economic indicators that could sway sentiment either way.

In the UK, all eyes are on next week’s BoE meeting, which could provide much-needed clarity on how policymakers plan to navigate slowing growth and persistent inflation pressures. Until then, the Pound is likely to remain sensitive to headlines from both Washington and Beijing, as global trade remains a dominant factor shaping currency movements.

Final Summary

The recent developments in global markets have once again highlighted how interconnected the world’s major economies are. The Pound’s struggle against the Dollar isn’t just about domestic economic factors—it’s about how trade relationships, interest rate decisions, and investor confidence interact on a global scale.

The US Dollar’s rebound after China’s trade-friendly gestures and the Fed’s balanced approach to rate cuts show how quickly sentiment can shift. For the Pound, the near-term focus will be on whether the Bank of England decides to ease its policy or wait for clearer signs of slowdown before acting.

As investors weigh these factors, one thing remains clear: the global economy is in a period of cautious optimism. With improved trade dialogue and measured policy moves, both the Dollar and the Pound are set to face a constantly changing landscape where every central bank decision and diplomatic statement can tip the balance.

USDJPY Surges as BoJ’s Ueda Sparks Fresh Wave of Yen Weakness

The Japanese Yen (JPY) has been facing tough times lately. After the Bank of Japan (BoJ) decided to maintain its current monetary stance, investors started rethinking their expectations about when the next rate hike might actually happen. On top of that, global optimism surrounding trade talks between the United States and China is taking away some of the Yen’s traditional safe-haven appeal. Together, these factors are pushing the currency lower and reshaping market sentiment around Japan’s economy.

BoJ’s Steady Hand Keeps Markets Guessing

When the BoJ announced that it would keep interest rates steady, it wasn’t a shock to anyone following the markets closely. What caught attention, however, were the remarks that followed from BoJ Governor Kazuo Ueda. During the post-meeting press conference, Ueda repeated that any future rate hikes would depend on how Japan’s economy and prices move relative to forecasts. But he avoided giving a clear timeline or hint about when that could happen.

That vague communication left traders and analysts uncertain. For months, speculation had been building that the BoJ might tighten policy sooner to curb inflation and stabilize the Yen. Instead, Ueda’s cautious tone suggested the central bank is in no rush. This indecision added pressure on the Yen as investors sought higher returns elsewhere.

Adding to the mix, Japan’s new Prime Minister Sanae Takaichi is expected to adopt an aggressive fiscal spending plan to boost growth. While that might support the domestic economy in the short term, it also increases government debt and delays expectations of a tighter monetary stance from the BoJ. This combination—cautious central banking and expansionary fiscal policy—has tilted the sentiment against the Yen.

Uncertainty Over Future Rate Hikes Fuels Yen Weakness

One of the main reasons behind the Yen’s decline is the uncertainty over when the next BoJ rate hike will happen. Markets dislike uncertainty, and right now, that’s exactly what Japan’s financial policy landscape offers. Investors are left to speculate whether the BoJ will move early next year or hold off even longer.

To make matters more complicated, external pressure is also coming into play. U.S. Treasury Secretary Scott Bessent recently encouraged Japan’s government to allow the BoJ more independence in managing currency stability. His remarks hinted that Washington may prefer a faster pace of monetary tightening to prevent extreme Yen weakness against the U.S. Dollar. But Tokyo’s policymakers seem more focused on avoiding sharp market shocks, which means they’re unlikely to act hastily.

All this has left the Yen vulnerable. With no clear signs of tightening and continued global risk appetite, traders have little reason to hold the JPY as a safe-haven asset.

Trade Optimism Dims the Yen’s Safe-Haven Glow

For decades, the Japanese Yen has been a go-to refuge during times of global uncertainty. Whenever tensions rose between major economies or financial markets stumbled, investors typically turned to the Yen as a safer bet. But lately, that reputation is fading.

The recent thaw in U.S.-China relations has lifted overall market sentiment. U.S. President Donald Trump and Chinese leader Xi Jinping are expected to meet to discuss trade relations after months of heated disputes. The possibility of improved cooperation between the world’s two largest economies is fueling investor optimism, driving funds back into riskier assets like equities and emerging market currencies.

USDJPY is moving in an uptrend channel, and the market has reached a higher high area of the channel

That shift in sentiment has reduced the appeal of the Yen as a safe haven. Simply put, when investors feel more confident, they’re less likely to park their money in low-yielding currencies like the Yen. As a result, the JPY finds itself under pressure not only from domestic policy uncertainty but also from changing global dynamics.

The Broader U.S. Influence: Fed Policy and Market Reactions

The Yen’s weakness is not happening in isolation. The U.S. Dollar (USD) plays a central role in determining how major currency pairs move, and recent developments in Washington have added another layer to the story.

The U.S. Federal Reserve recently signaled that it might hold off on additional rate cuts in the coming months. That decision strengthened the Dollar, as investors perceived it as a sign of confidence in the U.S. economy. Earlier rate cuts had been introduced to cushion against global economic slowdowns, but with signs of stability emerging, the Fed is adopting a more balanced stance.

Furthermore, the Fed announced it would end its balance sheet reduction program, a move that many see as the end of its quantitative tightening phase. This combination of policies has boosted confidence in the Dollar and attracted global capital flows back into the United States.

When the Dollar gains strength, it naturally puts downward pressure on the Yen. This dynamic, coupled with Japan’s internal uncertainty, makes it difficult for the JPY to recover momentum in the short term.

Political Shifts and Fiscal Policies Add More Complexity

The political landscape in Japan is also playing a part in shaping the Yen’s direction. With Prime Minister Sanae Takaichi’s pro-stimulus agenda, markets expect more government spending aimed at reviving economic growth. While such measures can help businesses and boost consumer demand, they also risk expanding Japan’s already large public debt.

For currency investors, this raises questions about Japan’s long-term fiscal health. A more aggressive spending approach, without corresponding monetary tightening, could keep inflation expectations low and the Yen weak. Traders are carefully watching how the BoJ balances its cautious approach with the government’s expansionary ambitions.

This policy tug-of-war—between the desire for stability and the need for growth—creates uncertainty, and as history shows, uncertainty rarely helps a currency strengthen.

Global Market Sentiment and Risk Appetite

Beyond Japan and the United States, global investors are responding to shifting risk sentiment. Optimism over trade talks, improving supply chains, and stronger corporate earnings have increased demand for riskier assets. This means money is flowing into equities, commodities, and emerging markets, rather than traditional safe havens like the Yen.

Even minor hints of progress in international relations can trigger big moves in the currency market. Right now, the general sense of optimism is dominating, leaving the Yen on the defensive. Unless new global tensions emerge or markets suddenly turn risk-averse, the JPY may continue to drift lower.

What Lies Ahead for the Japanese Yen

Looking forward, the Yen’s path will likely depend on three major factors:

-

BoJ Communication: Any shift in tone from Governor Ueda or other BoJ officials could influence market expectations about future rate hikes.

-

Government Policy Direction: How Prime Minister Takaichi implements fiscal stimulus will shape investor confidence in Japan’s long-term outlook.

-

Global Sentiment: If U.S.-China relations continue to improve, risk appetite will stay high, keeping pressure on safe-haven currencies like the Yen.

Investors are expected to stay cautious, closely analyzing every statement from policymakers for hints about what’s next.

Final Summary

The Japanese Yen’s recent weakness tells a larger story about the balance between domestic caution and global optimism. The Bank of Japan’s decision to hold rates steady, paired with vague signals about future tightening, has left traders uncertain. Meanwhile, optimism surrounding U.S.-China trade relations is driving risk-taking behavior across financial markets, further eroding the Yen’s safe-haven appeal.

At the same time, Japan’s new leadership is signaling a push for stronger government spending to stimulate the economy. While that may offer short-term support, it complicates the BoJ’s path toward policy normalization. In contrast, the U.S. Federal Reserve’s firmer stance is reinforcing the Dollar’s dominance, making it even harder for the Yen to find solid ground.

For now, the market’s message is clear: the Yen’s direction will depend on how quickly Japan’s central bank and government can align their strategies amid a rapidly changing global environment. Until then, uncertainty will remain the defining feature of the Japanese currency story.

USDCAD rebounds as the Greenback gains strength and sentiment improves

The US Dollar has regained momentum against the Canadian Dollar after bouncing back from a recent low point. This recovery reflects a mix of optimism around global trade relations and reactions to fresh comments from central banks on both sides of the border. Let’s take a deeper look at what’s happening and why the Greenback seems to be making a comeback.

A Strong Comeback for the US Dollar

After a brief dip, the US Dollar began to climb again against the Canadian Dollar. The currency’s recovery shows how sensitive global markets are to changes in both economic policy and international trade talks.

Investors appear more confident as new trade discussions between the United States and China hint at progress. At the same time, comments from the Federal Reserve have reassured markets that the US economy remains strong enough to handle tighter monetary policy if needed. Together, these developments have helped push the Dollar higher, reflecting a renewed sense of stability among traders.

Trade Talks Between the US and China Spark Market Interest

Global trade news has once again taken center stage. US President Donald Trump and Chinese President Xi Jinping have reportedly reached a mutual understanding that could ease tensions between the two largest economies in the world.

A Step Toward Better Trade Relations

As part of this agreement, the US and China are moving toward lowering tariffs on certain goods, especially products that have faced heavy duties in recent years. China, in turn, plans to resume purchases of US agricultural products, such as soybeans, and will continue to allow the export of critical materials like rare earth elements. Both sides also agreed to cooperate in addressing issues related to illegal drug trading, particularly the production and export of fentanyl.

While specific details remain limited, the announcement has been enough to spark optimism in global markets. Statements from both leaders suggest that the talks were productive. President Trump called the meeting “amazing,” while Chinese President Xi emphasized that both countries reached a “consensus on important economic and trade issues.”

Why This Matters for Currencies

Whenever there’s progress in trade relations, currencies often react quickly. For the US Dollar, reduced trade tensions can mean a stronger outlook for exports and growth. This tends to attract investors back to the Dollar, increasing its value. For Canada, which depends heavily on trade, these developments also influence the value of its currency, especially since both economies are closely connected through trade and energy markets.

Central Banks Take the Spotlight

Currency movements often follow the tone set by central banks, and this week was no exception. Both the US Federal Reserve and the Bank of Canada made decisions that caught the market’s attention.

Federal Reserve’s Confident Outlook

The Federal Reserve announced a small interest rate cut—something that markets had already expected. However, what stood out were the words of Fed Chair Jerome Powell. He suggested that another rate cut later this year is not guaranteed, emphasizing that the economy remains in relatively strong shape.

This statement was enough to strengthen the Dollar. Investors took it as a sign that the US central bank may soon pause its cycle of rate cuts. In simpler terms, Powell’s message signaled confidence in the economy, and that confidence gave traders a reason to buy back into the Dollar.

Bank of Canada’s Mixed Signals

On the other side, the Bank of Canada also lowered its interest rates by a quarter of a percent. But unlike the Fed, the Canadian central bank sent a slightly different message. Governor Tiff Macklem hinted that this might be the last rate cut for now, suggesting that Canada’s economy doesn’t need further stimulus at the moment.

USDCAD is moving in an uptrend channel

This mix of a rate cut and a positive outlook confused some investors. Initially, it gave the Canadian Dollar a brief boost, but as the US Dollar strengthened later in the day, the Loonie began to lose ground again.

Global Market Sentiment and What It Means for Investors

The recent movements in the US Dollar and Canadian Dollar are part of a larger global picture. Markets are currently driven by three main factors: central bank decisions, trade relations, and overall investor confidence.

1. Interest Rates Still Rule the Game

Even small changes in interest rates can have a big impact on currency values. When central banks cut rates, it often means they’re trying to boost economic growth. But if they hint that cuts are ending, it can strengthen the national currency as investors expect better returns in the future.

2. Trade Peace Brings Relief

After years of tension between the US and China, any sign of cooperation tends to lift investor spirits. Better trade relations can improve global economic stability, which supports stronger demand for major currencies like the Dollar.

3. Investors Seek Safety in the Greenback

The US Dollar is often seen as a safe haven during uncertain times. When investors aren’t sure how the global economy will perform, they tend to move their money into US assets. This consistent demand helps keep the Dollar strong, even when short-term events cause temporary dips.

How the Market Outlook Is Shaping Up

While daily market movements can seem unpredictable, the underlying trends are easier to understand. The US economy remains relatively stable, supported by a strong job market and steady consumer spending. Canada, on the other hand, continues to balance its energy-driven economy with global trade challenges and domestic policy adjustments.

Traders are watching for future statements from both the Federal Reserve and the Bank of Canada. Any sign of changing interest rate policy could quickly shift the direction of both currencies. At the same time, updates from US-China trade discussions will likely continue to influence global sentiment.

For now, the balance seems to favor the US Dollar. Investors are taking comfort in the Fed’s cautious confidence, and the recent trade optimism has only added to the Greenback’s strength.

Final Summary

In summary, the US Dollar’s recent rebound against the Canadian Dollar shows how global markets respond to both policy signals and international negotiations. The combination of a slightly hawkish tone from the Federal Reserve and renewed optimism around US-China trade discussions has helped push the Dollar higher.

While the Bank of Canada also made headlines with its own rate decision, the mixed message it delivered couldn’t outweigh the Dollar’s renewed strength. Investors appear to be betting that the US economy will hold steady even as the global landscape remains uncertain.

Overall, this week’s developments remind us that currency values aren’t just about numbers or charts—they’re reflections of global confidence, political decisions, and market psychology. The next few weeks will likely bring more clarity, but for now, the US Dollar is standing tall once again.

AUDUSD Slips After Early Rise as Dollar Strengthens on Renewed US-China Optimism

The Australian Dollar (AUD) faced a setback after briefly gaining against the US Dollar (USD). This shift came as the greenback regained strength on Thursday, following renewed optimism in trade relations between the United States and China and fresh remarks from Federal Reserve Chair Jerome Powell that hinted at no immediate rate cuts.

Let’s dive deep into what’s happening with the AUD/USD pair, why the US Dollar is finding renewed momentum, and how global trade developments continue to shape this dynamic currency relationship.

A Fresh Turn in the AUD/USD Journey

The AUD/USD pair initially showed strength in early trading but couldn’t hold onto those gains for long. By the European session, the Aussie dollar had lost ground as the US Dollar started recovering.

The turnaround in market sentiment came shortly after a significant meeting between US President Donald Trump and Chinese President Xi Jinping in South Korea. The two leaders reportedly discussed easing trade tensions, marking a notable improvement in diplomatic tone compared to the previous months of tariff disputes and trade restrictions.

Such high-level discussions often have a direct impact on the forex market because they influence investor confidence. When relations between the world’s two largest economies improve, the ripple effect is felt across global currencies — especially those closely tied to trade and commodities, like the Australian Dollar.

Why the US Dollar Rebounded So Strongly

Positive Trade Talks Boost Confidence

The key reason behind the US Dollar’s rebound was the improved tone of US-China trade relations. According to reports following the leaders’ meeting, China agreed to resume rare earth exports to the United States “openly and freely,” which was seen as a symbolic gesture of cooperation. Additionally, the US announced a reduction in tariffs on Chinese goods, another positive step that encouraged global markets.

These developments strengthened the US Dollar’s appeal because they reduced the risk of prolonged trade disruptions. A more stable global trade environment tends to attract investors toward the safe-haven US Dollar, especially when compared to riskier assets and currencies.

Federal Reserve Maintains a Firm Stance

Adding to the Dollar’s recovery was Federal Reserve Chair Jerome Powell’s statement that there is currently no plan to reduce interest rates at the upcoming December meeting. Powell emphasized that the US economy remains resilient, with inflation and employment levels supporting a cautious monetary policy approach.

For traders, this signals that the US interest rate may remain relatively higher for now, keeping the Dollar attractive to investors seeking better returns. When the Fed holds rates steady, it typically boosts demand for the US Dollar, as higher yields appeal to global investors.

The Australian Dollar’s Mixed Outlook

Trade Relations Offer Both Support and Pressure

While better US-China relations are broadly positive for the global economy, the Australian Dollar finds itself in a mixed position. On one hand, an improved trade environment benefits Australia, given its heavy reliance on exports to China — especially commodities like iron ore and coal.

On the other hand, the strengthening US Dollar often limits the upside potential for the Aussie. Since the AUD/USD pair moves inversely to the US Dollar, any significant rebound in the greenback tends to push the pair lower.

Essentially, while global trade optimism helps Australia indirectly, the Dollar’s dominant recovery still keeps the AUD under pressure.

Domestic Factors at Play

Back home, the Reserve Bank of Australia (RBA) faces its own challenges. The latest Consumer Price Index (CPI) data revealed that inflation is accelerating faster than expected. Prices rose 1.3% in the third quarter, up from 0.7% previously, signaling growing inflationary pressure.

Because of this, many traders now believe that the RBA will pause further interest rate cuts for the rest of the year. Cutting rates during a period of rising inflation could risk overheating the economy or weakening the currency further.

This expectation provides some underlying support to the Australian Dollar, even as external forces like the US Dollar’s strength weigh it down.

Global Market Sentiment and What Comes Next

The currency market remains highly sensitive to global political and economic developments. The AUD/USD exchange rate is particularly reactive to changes in trade sentiment, interest rate expectations, and macroeconomic indicators from both the US and Australia.

Right now, the mood in the market seems cautiously optimistic. The improvement in US-China relations has injected some relief into financial markets, reducing fears of an extended trade conflict. This has been good news for both Asian economies and commodity-linked currencies like the Australian Dollar.

AUDUSD is moving in an uptrend channel, and the market has rebounded from the higher low area of the channel

However, investors remain watchful. Any shift in tone between Washington and Beijing, or any surprise comments from the Federal Reserve, could quickly change the trend.

In short, while the current sentiment leans positive, volatility remains a key feature of this currency pair.

A Broader Perspective on AUD/USD Trends

The AUD/USD pair has long been seen as a barometer of global risk sentiment. When traders feel confident about economic growth, they tend to favor riskier currencies like the Australian Dollar. Conversely, when uncertainty rises — whether due to global conflict, inflation, or central bank policy — investors flock to the safety of the US Dollar.

Right now, this balance is shifting slightly in favor of the USD. Strong economic indicators from the US, coupled with Powell’s cautious tone, have reaffirmed confidence in the American economy. Meanwhile, Australia’s economy, though resilient, faces headwinds from global slowdowns and domestic inflation challenges.

This combination means the AUD/USD pair may continue to experience short-term fluctuations. However, traders will likely focus on upcoming data releases — such as employment reports, inflation numbers, and central bank statements — to gauge the next big move.

Final Summary

The recent moves in the AUD/USD pair highlight how interconnected global economies have become. What started as a rebound in the US Dollar due to improved US-China trade relations and firm Federal Reserve policy quickly translated into pressure on the Australian Dollar.

The Aussie’s struggle to hold gains shows the delicate balance between global optimism and domestic realities. While Australia benefits from better trade prospects with China, the stronger US Dollar and rising inflation back home create a challenging environment for sustained growth.

Looking ahead, the AUD/USD exchange rate will likely depend on two main factors: how the US-China trade relationship evolves and whether central banks maintain their current interest rate paths. If trade relations continue to improve and inflation remains manageable, the Australian Dollar may regain some ground. But if the US Dollar keeps strengthening on firm policy and investor confidence, the Aussie might continue to stay under pressure.

In essence, the coming weeks could bring more twists in this currency story — and traders should stay alert, as the balance between optimism and caution continues to define the AUD/USD market narrative.