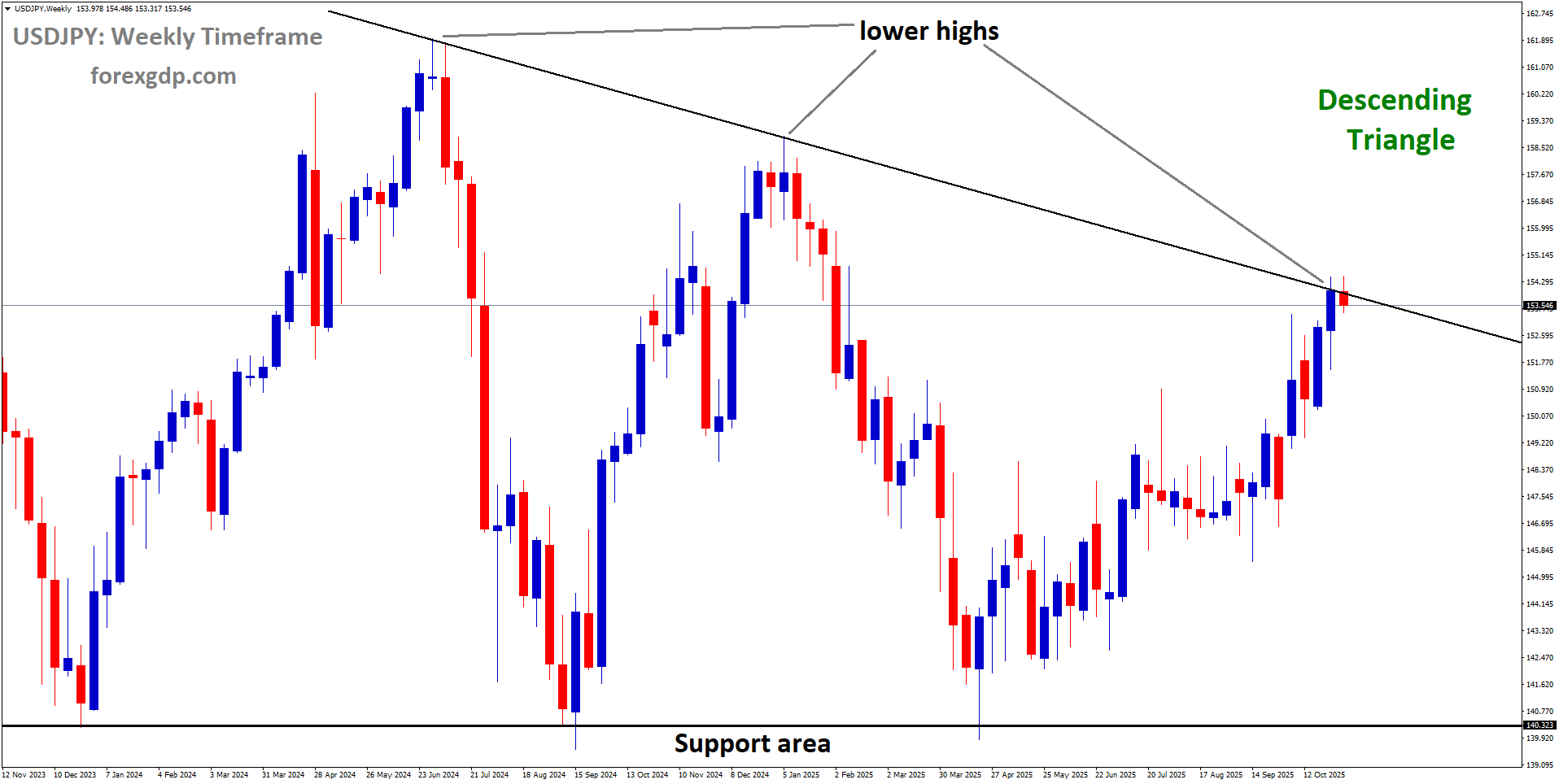

USDJPY is moving in a descending triangle pattern, and the market has reached the lower high area of the pattern

USDJPY Rises as Investors Seek Safety, But BoJ’s Next Move Keeps Traders Cautious

The Japanese Yen (JPY) has recently caught the attention of traders and investors around the world. With growing concerns about global market stability, central bank decisions, and intervention fears, the Yen has started to see renewed interest. Let’s take a closer look at what’s driving this movement and what it could mean in the coming days.

A Fresh Wave of Safe-Haven Demand for the Yen

In times of uncertainty, investors tend to move their money into assets that are considered safer — and the Japanese Yen is one of the top choices in that category. Recently, global markets have seen rising volatility due to political disputes, central bank decisions, and overall risk aversion. This shift in sentiment has encouraged traders to buy Yen, seeking protection against unpredictable market swings.

Why the Yen is Seen as a Safe-Haven Currency

The Yen’s safe-haven status comes from Japan’s stable economy, large foreign exchange reserves, and consistent trade surpluses. Even when other currencies weaken during market stress, the Yen tends to remain resilient. As fears of government intervention grow — especially after Japanese authorities hinted at potential action to stabilize the currency — more investors have moved toward the Yen to minimize their exposure to risk.

Additionally, a mild pullback in the US Dollar (USD) has added some strength to the Yen. With the USD slipping from its recent highs, traders are now looking for alternative currencies that offer short-term security and long-term potential.

BoJ’s Cautious Approach and Market Speculation

The Bank of Japan (BoJ) has been at the center of market discussions lately. After years of maintaining ultra-loose monetary policies, the BoJ has started signaling a possible shift. Comments from BoJ Governor Kazuo Ueda last week suggested that Japan may consider a rate hike in the near future — possibly as early as December or January. This statement alone was enough to cause ripples in the foreign exchange market.

Hints of a Possible Rate Hike

Governor Ueda indicated that Japan’s inflation outlook and economic performance are improving, and the central bank could gradually raise rates if these trends continue. Such a move would mark a major shift from the long-standing negative interest rate policy, which has been in place for years to support growth.

However, the BoJ’s cautious tone also reflects its concern about maintaining stability. While inflation in Tokyo has stayed above the 2% target for over three years, Japan’s new Prime Minister Sanae Takaichi has expressed interest in aggressive fiscal spending — something that could complicate the timing of any rate hike. The market, therefore, remains divided about when and how quickly Japan will tighten its policy.

Intervention Fears Loom Large

Another key factor influencing the Yen’s performance is the fear of intervention by Japanese authorities. If the Yen weakens too much against the Dollar, officials may step in to prevent excessive depreciation. These intervention threats have historically discouraged traders from taking overly bearish positions on the Yen, keeping it relatively stable even during periods of USD dominance.

The US Dollar’s Role in the Yen’s Movement

While the Yen has been gaining some ground, the US Dollar continues to play a significant role in shaping the USD/JPY pair’s direction. Last week, the US Federal Reserve maintained its firm stance, signaling that it’s not ready to lower interest rates anytime soon. Fed Chair Jerome Powell made it clear that while inflation is easing, the economy remains strong enough to justify keeping rates high.

This “hawkish” stance from the Fed helped the Dollar strengthen earlier, pushing the USD Index (DXY) to its highest level in three months. However, as the Dollar faced a mild correction this week, the Yen took advantage of the pullback. Investors looking to rebalance their portfolios began selling Dollars and buying back into the Yen.

Government Uncertainty and Market Reactions

Adding to the market’s nervousness is the ongoing US government shutdown, which has stretched on for more than a month. The deadlock between lawmakers over the funding bill has raised concerns about the economic impact of a prolonged closure. Investors are growing anxious, fearing that a continued shutdown could affect consumer confidence and slow economic growth in the United States.

Senate leaders have expressed hope of resolving the issue soon, but until an agreement is reached, uncertainty will remain high. This has created a complex environment where safe-haven currencies like the Yen benefit from the Dollar’s temporary weakness, even as underlying fundamentals still favor the US currency in the long run.

Balancing Risks: What Traders Should Keep in Mind

The current Yen movement highlights the delicate balance between optimism and caution in the global market. On one hand, safe-haven flows and intervention threats are supporting the Yen. On the other, Japan’s slow pace toward policy normalization and the Fed’s hawkish approach are limiting how much further the Yen can appreciate.

Short-Term Momentum vs. Long-Term Outlook

In the short term, traders may see fluctuations driven by news headlines, central bank comments, or political developments. However, for long-term investors, the broader trends — such as Japan’s inflation trajectory, BoJ policy decisions, and global risk appetite — will likely determine the Yen’s direction.

USDJPY is moving in an uptrend channel, and the market has reached a higher high area of the channel

Those betting on a stronger Yen should keep an eye on the BoJ’s next moves. If the central bank finally decides to raise rates, it could trigger a wave of appreciation for the Yen. Conversely, if the Fed maintains higher rates for longer while Japan continues its slow approach, the USD could regain momentum.

Final Summary

The Japanese Yen’s recent rise is a mix of safe-haven demand, intervention fears, and cautious optimism surrounding Japan’s monetary policy. As investors navigate a world filled with political and economic uncertainty, the Yen has once again proven its reputation as a dependable refuge.

While the BoJ’s next move remains uncertain, any hint of a rate hike could give the Yen more strength in the coming months. At the same time, the ongoing US government issues and the Fed’s policy stance will continue to influence market sentiment.

In short, the Yen’s journey is far from over — and traders should stay alert. As global markets shift between fear and confidence, the Japanese currency will remain at the heart of the action, balancing between domestic decisions and international developments.

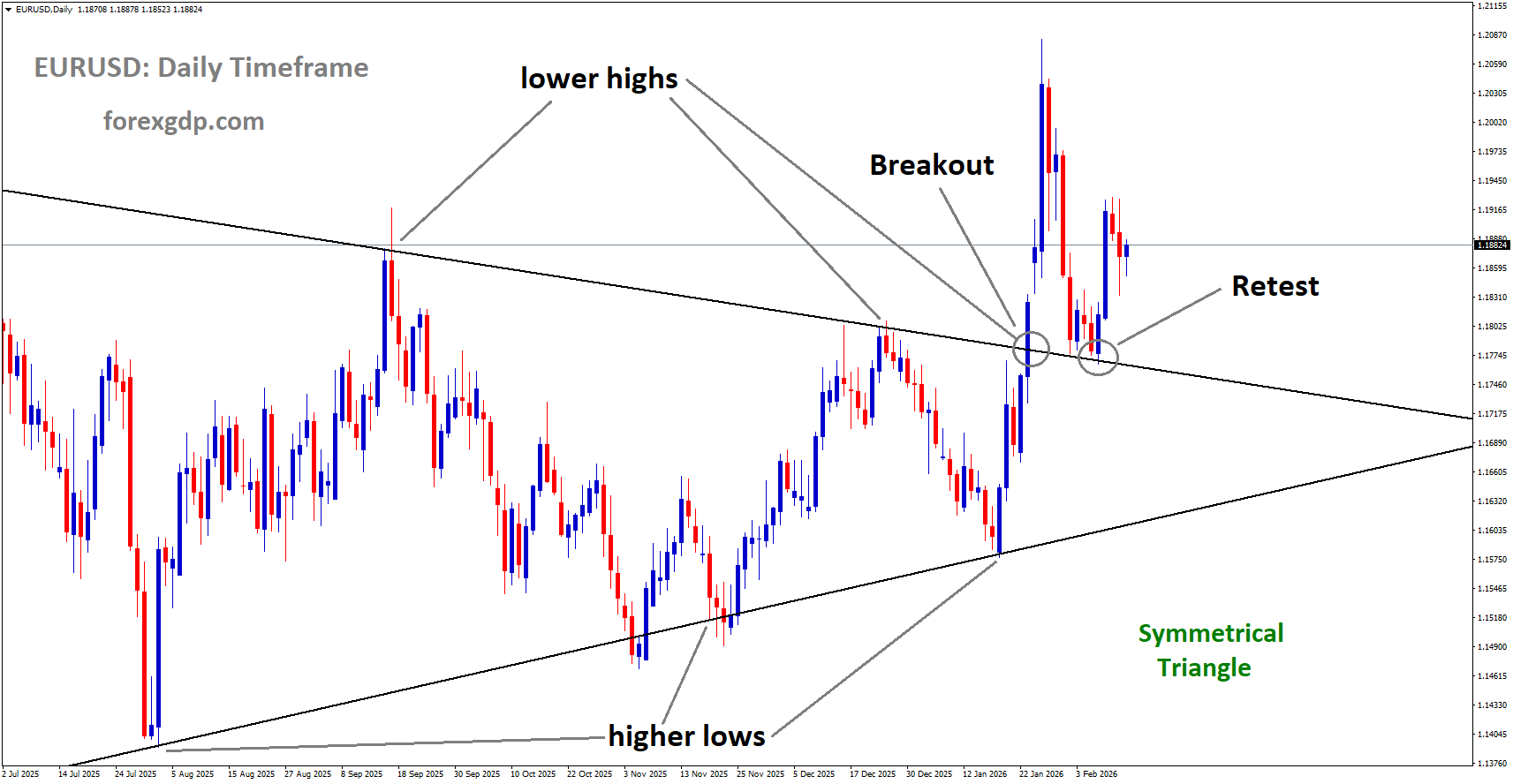

EURUSD struggles to rebound as Dollar dominance keeps pressure on the Euro

The Euro has been finding it tough to hold ground against the US Dollar, especially after its recent attempt to move higher was quickly rejected. With investors still uncertain about the Federal Reserve’s next move and ongoing concerns about global economic stability, the market has turned cautious once again. Let’s dive deeper into what’s going on behind the scenes and what’s driving the current mood in the forex market.

The Euro’s Struggle Against the Dollar

The EUR/USD pair has seen limited upward movement lately, losing momentum after a short-lived rally. Traders have been hesitant to take strong positions as the Dollar continues to gain strength. After a week of steady declines, the Euro remains under pressure, showing how market sentiment has shifted in favor of the Dollar.

EURUSD is moving in a downtrend channel, and the market has reached the lower low area of the channel

The recent weakness in the Euro comes after the US Dollar surged, driven by renewed expectations that the Federal Reserve may maintain its restrictive stance longer than expected. Despite softer manufacturing data from the United States, the Dollar has continued to attract demand as investors look for safer assets amid growing uncertainty.

This cautious behavior in the market is not surprising. Whenever global risks rise or economic data looks weak, traders often move back to the Dollar for safety. It’s a trend we’ve seen time and again, and it continues to shape market behavior today.

Why the US Dollar Is Holding Strong

Investor Caution and Fed Expectations

The key factor supporting the US Dollar right now is the market’s shifting expectation around Federal Reserve policies. Just a week ago, traders were betting heavily on rate cuts in the coming months. But that optimism has faded quickly.

Recent comments from various Fed officials have highlighted internal disagreement on how restrictive policy should remain. While some policymakers favor keeping rates steady to tackle inflation, others argue that policy might already be too tight and could risk slowing down the economy further.

Even so, inflation remains a major concern for the Fed. With price pressures still above the desired level, the central bank is hesitant to make aggressive moves toward rate cuts. As a result, investors are scaling back their expectations for policy easing in the near term, helping to keep the Dollar strong.

Mixed Economic Signals

The US economy continues to send mixed messages. The manufacturing sector, for instance, remains under stress. The latest data from the Institute for Supply Management (ISM) showed that manufacturing activity has contracted for eight consecutive months. Declining orders and reduced hiring have kept this sector weak.

However, the broader economy still shows resilience. Consumer spending has held up reasonably well, and job growth remains steady, even though some cracks are starting to appear. This balance between resilience and weakness keeps markets guessing about what the Fed will do next.

Market Sentiment: Playing It Safe

In times like these, investors tend to prioritize safety. When risk sentiment turns cautious, the Dollar often benefits as global traders seek a more stable asset. With tensions rising across multiple fronts — from geopolitical risks to economic slowdowns — this “risk-off” sentiment has once again pushed the Dollar higher against most major currencies.

What’s Happening in the Eurozone

Muted Market Reaction to ECB Comments

Across the Atlantic, the Eurozone isn’t offering much help to the Euro either. The European Central Bank (ECB) has been facing its own set of challenges. While inflation in the region has cooled compared to the previous year, growth remains weak and uneven across member countries.

ECB President Christine Lagarde recently addressed the public but didn’t introduce any major policy surprises. Her cautious tone reflected the ongoing dilemma faced by the central bank: inflation is falling, but the economic recovery remains fragile. Markets don’t expect the ECB to take any dramatic steps soon, which has limited the Euro’s ability to recover.

Signs of Stability, But No Real Growth

Recent Eurozone data offered a mixed picture. The region’s manufacturing activity managed to hold steady after months of contraction, which may be seen as a small relief. However, the improvement was marginal, suggesting that the industrial sector is merely stabilizing rather than expanding.

With sluggish economic momentum and cautious policymakers, the Euro has struggled to find strong support. Many investors are waiting for clear signs of recovery before betting on a stronger Euro in the coming months.

Global Focus Shifts to US Employment Data

With no major economic reports on Tuesday, attention has shifted toward the upcoming US ADP Employment Report. This report often provides early clues about the broader US labor market, which plays a key role in shaping Federal Reserve policy.

A strong jobs report could reinforce the idea that the US economy remains resilient, supporting the Fed’s decision to keep policy restrictive. That would likely give the Dollar another boost. On the other hand, weaker employment figures might revive expectations for earlier rate cuts, which could finally give the Euro a chance to bounce back.

Traders are also watching how the government’s partial shutdown in the US could affect upcoming data releases. The delay or cancellation of some reports, such as the JOLTS job openings or factory orders, has left investors with fewer clues to work with. This uncertainty is adding to the cautious tone across markets.

Market Outlook: What Traders Are Watching Next

Right now, both the Euro and the Dollar are at an important crossroads. The Dollar’s strength depends heavily on how economic data unfolds and how long the Fed decides to maintain its current stance. If inflation shows signs of easing further and job growth slows, the central bank may be forced to shift toward a more accommodative policy next year.

For the Euro, recovery will depend largely on whether the Eurozone can regain some economic momentum. A pickup in industrial activity or stronger consumer spending could help turn sentiment around. But for now, the lack of strong growth data keeps traders hesitant.

Investors will continue watching key indicators closely, including upcoming employment data, inflation reports, and any new statements from central bankers. Until the outlook becomes clearer, market volatility could remain high, with sudden shifts in sentiment driving short-term price movements.

Final Summary

In the current environment, the Euro’s weakness and the Dollar’s strength reflect a broader story about caution and uncertainty. Traders are looking for direction, but the global economy is sending mixed signals. While the Federal Reserve remains focused on inflation, its hesitation to signal clear policy changes keeps investors guessing. At the same time, the European Central Bank’s cautious approach leaves the Euro with little upward momentum.

The next few weeks could bring more clarity as new employment and inflation data come in. Until then, both currencies may continue to move within tight ranges, with sudden bursts of volatility whenever key data or policy comments hit the headlines. The balance between growth, inflation, and interest rates will continue to define the tone of global currency markets — and for now, the Dollar still has the upper hand.

GBPUSD Falls as UK Budget Concerns Rise Following Reeves’ Warning

The British Pound has been losing ground recently, slipping lower against the US Dollar as traders become cautious about what’s ahead for both the UK and US economies. From potential tax hikes in Britain to uncertainty about future interest rate moves by the US Federal Reserve, investors seem to be taking a more careful approach. Let’s break down what’s going on and why it matters.

UK Investors Brace for Possible Tax Increases

In recent days, the Pound has underperformed compared to most major currencies, and the reason is largely political and fiscal rather than technical. Reports suggest that the UK’s Chancellor of the Exchequer, Rachel Reeves, may soon announce tax hikes in her upcoming Autumn Budget to cover a £22 billion gap in the nation’s finances.

According to The Sunday Times, Reeves and her team have been reviewing over 100 potential tax and spending measures, with much of the focus placed on higher-income households. The goal appears to be closing the budget gap without placing additional strain on middle- and lower-income families, though the specifics are yet to be revealed.

GBPUSD is moving in a downtrend channel, and the market has reached the lower low area of the channel

This talk of tax rises has unsettled investors, who often view fiscal tightening as a potential drag on economic growth. When government spending slows or taxes increase, it can weigh on consumer confidence and reduce overall spending power—both of which can weaken a currency’s strength.

Why the Market Reacted So Strongly

Traders usually respond quickly to fiscal signals, especially when they suggest higher taxes or reduced government support. In this case, the fear is that increased taxation could slow down economic activity just as the UK is still recovering from the effects of inflation and rising borrowing costs.

The timing of this speculation is also critical—Reeves’ remarks came shortly before the Bank of England’s policy announcement, which has already divided opinions among economists. Some expect a rate cut to ease financial pressure, while others believe the central bank will hold off until inflation shows clearer signs of decline.

The Bank of England’s Balancing Act

The Bank of England (BoE) finds itself in a challenging position. Inflation in the UK has been slow to decline, and while the pace of price increases has cooled compared to last year, it remains higher than the central bank’s target.

During the previous meeting in September, the BoE decided to keep interest rates steady at 4%, reflecting a cautious stance amid economic uncertainty. However, officials also expressed optimism that inflation would peak soon, likely around 4%, suggesting that they may have reached the top of their tightening cycle.

Yet, recent comments from Chancellor Reeves have reminded everyone that inflation is still a problem. She stated that price pressures have been “too slow to come down,” which has exposed the economy to “rising borrowing costs.” Her message was clear—the upcoming Autumn Statement will prioritize bringing inflation lower, even if that means making some unpopular decisions.

This creates a tricky scenario for the BoE. If inflation remains sticky and the government increases taxes, the central bank must tread carefully to avoid stalling growth altogether. Rate cuts could help stimulate the economy, but they risk re-igniting inflation if done too early.

US Dollar Strength Keeps Pressure on the Pound

While domestic concerns weigh on the Pound, the US Dollar has been enjoying a burst of strength, making life even harder for the GBP/USD pair.

The Dollar’s rally comes from changing expectations about the Federal Reserve’s future moves. Just a week ago, markets were nearly certain that the Fed would cut rates again before the end of the year. But now, that confidence has dropped sharply after Fed Chair Jerome Powell suggested that a December rate cut is “far from a foregone conclusion.”

In other words, the Fed isn’t ready to commit to more rate cuts until incoming data justifies it. Powell mentioned that officials had “strongly different views” during the last meeting, showing that internal disagreements still exist about how much more easing is necessary.

Fed Officials Urge Caution

Adding to that cautious tone, Mary Daly, the President of the San Francisco Federal Reserve, recently noted that monetary policy must remain “modestly restrictive” since inflation is still above the 2% target. She emphasized that future decisions will depend on economic data, especially job market figures and consumer spending trends.

This stance has made investors rethink their earlier assumptions. The once-strong belief in a December rate cut has weakened, pushing the US Dollar higher as traders now see fewer chances of near-term monetary easing.

What’s Next for the GBP/USD Pair?

The next big test for the currency pair will come with the release of US employment data, particularly the ADP Employment Change report. Normally, markets also look at Nonfarm Payrolls (NFP) data, but that report remains unavailable due to the ongoing US federal shutdown.

Economists expect modest job growth, but any surprises—especially stronger-than-expected job numbers—could reinforce the idea that the US economy is still too robust for the Fed to justify more rate cuts. That would likely boost the Dollar further, making it harder for the Pound to recover.

Meanwhile, in the UK, traders will keep their eyes on both the Autumn Budget and the Bank of England meeting. Together, these two events will shape expectations for the Pound in the coming weeks. If Reeves introduces tax measures perceived as growth-restrictive, or if the BoE maintains a cautious tone without offering clear support for economic expansion, the GBP could remain under pressure.

Key Takeaways and Market Outlook

To sum it all up, the current weakness in the Pound Sterling is the result of a perfect storm—a mix of political uncertainty, fiscal tightening fears, and a resurgent US Dollar.

Here are the main drivers to watch in the near term:

-

UK Fiscal Policy: Potential tax hikes to address the £22 billion shortfall could weigh on investor sentiment.

-

Bank of England’s Decision: Whether the BoE maintains rates or hints at cuts will influence the Pound’s short-term direction.

-

US Economic Data: Strong US figures could strengthen the Dollar further, adding downward pressure on GBP/USD.

As things stand, traders are treading carefully. Both the UK and US economies face delicate balancing acts—one between fiscal responsibility and growth, the other between inflation control and monetary easing.

Final Summary

The Pound’s recent decline isn’t about short-term trading moves or technical levels—it’s about big-picture economic confidence. With talk of tax increases in the UK, persistent inflation, and an uncertain global monetary outlook, investors are moving cautiously. The Dollar’s strength adds another layer of pressure, leaving the Pound vulnerable in the near term.

However, markets are fluid. If the UK government presents a well-balanced fiscal plan that reassures investors while keeping inflation in check, confidence could return. Likewise, if US data starts showing signs of a slowdown, the Dollar’s dominance could fade, giving the Pound some breathing room.

For now, though, the story remains one of caution. Traders, policymakers, and analysts alike are waiting for clearer signals from both sides of the Atlantic before making their next big move.

AUDUSD Weakens Sharply as RBA Maintains Policy Hold and Inflation Persists

The Australian Dollar has taken a hit following the latest monetary policy announcement by the Reserve Bank of Australia (RBA). After holding interest rates unchanged, market sentiment shifted, pushing the AUD/USD pair to its weakest levels in recent days. Let’s take a closer look at what’s driving this movement, why the Australian Dollar is under pressure, and how global economic factors are shaping the outlook for both currencies.

RBA Keeps Interest Rates Steady – Why It Matters

The RBA decided to keep its official cash rate unchanged at 3.6%, matching expectations from analysts and investors. This marks the second consecutive meeting where the central bank chose not to adjust rates. The decision wasn’t surprising, but the reasoning behind it paints a picture of an economy still wrestling with persistent inflation.

Rising Inflation Remains a Concern

Recent data from the Australian Bureau of Statistics revealed that inflation is not easing as quickly as the RBA would like. The Consumer Price Index (CPI) rose faster than anticipated, showing that prices are still growing at a pace that could hurt household budgets and slow economic growth. Although inflation has come down from its peak, it’s still higher than the RBA’s comfort zone.

AUDUSD is moving in a downtrend channel

Governor Michele Bullock addressed this concern in her remarks following the announcement. She noted that core inflation above 3% remains “not ideal” and emphasized that the economy may still need “a little bit of tightness” to bring inflation back under control. This suggests the RBA isn’t ready to consider rate cuts anytime soon, preferring to wait for clearer signs of stable price growth before making any move.

No Clear Guidance on Future Moves

One key takeaway from the RBA’s statement was its uncertainty about the timing of future rate changes. Bullock avoided offering a timeline for when rates might come down, explaining that inflation remains unpredictable due to both domestic and global factors. For now, the RBA’s cautious stance is aimed at balancing economic stability with inflation control, but investors were left with limited clues about what comes next.

The US Dollar’s Strength Adds Pressure on the Aussie

While the Australian Dollar weakened, the US Dollar found renewed strength. The primary reason behind this shift is the changing sentiment around the Federal Reserve’s interest rate policy. Markets had been betting on multiple rate cuts by the Fed this year, but those expectations have started to cool down. With fewer rate cuts now anticipated, the US Dollar has gained momentum, drawing investors away from riskier currencies like the AUD.

Fed Policy Outlook Shifts

According to the CME FedWatch Tool, the probability of a 25 basis point rate cut in December has dropped significantly compared to last week. This change in expectations reflects a stronger US economy, where inflation, although easing, remains sticky, and growth indicators continue to hold up. When investors believe the Fed will keep rates higher for longer, the US Dollar tends to benefit, as it offers better returns compared to other currencies.

This broader dollar strength has weighed heavily on the Australian Dollar. Since Australia’s economy is closely tied to global trade and commodity exports, any shift in global monetary policy can have an immediate impact on the Aussie’s performance.

What’s Next for the Australian Dollar?

The next few days could bring more clarity on where the Australian Dollar is headed. One key piece of data to watch is Australia’s upcoming trade balance report, which is due later this week. Strong export figures could offer temporary support to the currency, but weak numbers may reinforce the bearish tone that has dominated since the RBA’s announcement.

Global Factors to Watch

Beyond domestic data, global sentiment toward the US Dollar and commodities will continue to shape the direction of AUD/USD. The pair often reflects the difference in economic outlook between the US and Australia, making it sensitive to global risk trends and interest rate expectations.

If the Fed maintains its hawkish stance while the RBA remains cautious, the interest rate gap between the two countries could widen, keeping the Australian Dollar under pressure. On the other hand, if upcoming US economic data shows signs of slowing down, traders might start betting again on future Fed rate cuts — a move that could give the Aussie some breathing room.

Investor Sentiment and Market Behavior

Market reactions following central bank decisions often depend not only on what’s said, but on how investors interpret the tone and direction of policy. In this case, even though the RBA didn’t surprise anyone by holding rates steady, its tone was seen as slightly cautious, reinforcing the view that Australia’s economy might not be strong enough to handle further tightening.

Meanwhile, the Fed’s tone has been more resilient, with policymakers emphasizing the need to keep monetary conditions restrictive until inflation convincingly moves toward the 2% target. This contrast has made the US Dollar more attractive, especially for investors looking for safe-haven assets during uncertain times.

For short-term traders, this environment creates volatility in the AUD/USD pair. Movements can be sharp, driven by economic headlines or even small changes in global risk sentiment. For long-term investors, however, the focus will be on inflation trends, job data, and the RBA’s evolving stance.

Final Summary

The AUD/USD slide reflects a mix of domestic caution and international confidence. The RBA’s decision to hold interest rates steady, combined with its cautious tone on inflation, signaled that Australia’s central bank prefers patience over risk. On the other hand, the Federal Reserve’s stronger position and reduced expectations of near-term rate cuts have boosted the US Dollar, tipping the balance further against the Aussie.

As markets digest these developments, the next few weeks will be crucial for the Australian Dollar. Key data such as trade performance and global economic updates will determine whether the currency can rebound or continue its downward trend.

In simple terms, the story of AUD/USD right now is one of two economies moving at different speeds — one taking a careful, wait-and-see approach, and the other showing resilience and holding firm. Traders and investors will be watching closely to see which central bank blinks first in this ongoing monetary policy tug of war.

NZDUSD Under Pressure as China’s Economic Woes and Fed Stance Strengthen USD

The New Zealand Dollar (NZD) has been struggling recently, losing ground against the US Dollar as weak Chinese manufacturing data and cautious comments from the Federal Reserve dampen investor sentiment. The currency’s slide reflects broader worries about global economic growth and the uncertain path of US monetary policy.

Why the New Zealand Dollar Is Falling

The New Zealand Dollar’s recent decline is tied closely to disappointing economic data coming out of China. Since China is one of New Zealand’s largest trading partners, any slowdown in Chinese manufacturing or demand has a direct impact on New Zealand’s economy.

Recent reports show that China’s manufacturing activity is cooling off. The Manufacturing Purchasing Managers’ Index (PMI), a key measure of industrial health, dropped more than expected. This signals that factories are producing less and that overall demand is weakening. For a country like New Zealand, which relies heavily on exporting goods such as dairy, meat, and raw materials to China, this slowdown raises concerns about future trade revenue.

NZDUSD is breaking the lower low area of the downtrend channel

Investors often respond to such developments by moving their money into safer assets. That means they sell risk-sensitive currencies like the NZD and buy safer ones like the US Dollar. This shift adds more downward pressure on the New Zealand Dollar, making it one of the weaker performers among major currencies lately.

The Role of the US Federal Reserve and Its Impact on NZD/USD

Another key factor driving the New Zealand Dollar’s weakness is the tone coming from the United States Federal Reserve. Recently, the Fed decided to cut interest rates for the second time this year in an effort to support growth. However, Fed Chair Jerome Powell’s remarks following that decision created uncertainty in the market.

Powell made it clear that another rate cut in December is “not a foregone conclusion.” This means the central bank might not continue easing policy as aggressively as some traders had hoped. His comments were interpreted as hawkish, suggesting that the Fed could slow or even pause further rate reductions.

This kind of stance tends to strengthen the US Dollar. When the Fed signals confidence in the economy and holds off on additional cuts, investors see the USD as a safer and more attractive investment. As a result, currencies like the NZD, which are more sensitive to global risk sentiment, often weaken.

Adding to this dynamic is the ongoing political tension in the United States. The prolonged government shutdown, which has now stretched into several weeks, is creating an additional layer of uncertainty. Normally, a government shutdown would hurt the Dollar because it disrupts economic activity and raises fears about fiscal instability. However, in this case, the Dollar remains supported—mainly because of the Fed’s steady approach and the lack of appealing alternatives among other global currencies.

Global Sentiment and Its Ripple Effects

When global investors start worrying about growth, their first move is usually to avoid risk. This means they steer clear of currencies and assets tied to global trade and commodities. Unfortunately for New Zealand, its economy depends heavily on exports and agricultural products, both of which are influenced by external demand.

The recent decline in factory output and business activity in China has also fueled fears that global trade might slow further. In such a climate, traders prefer to hold currencies from countries with strong, stable economies and high interest rates—like the US.

The uncertainty surrounding US fiscal policy adds another dimension to market behavior. While the prolonged budget deadlock in Washington may cause temporary economic hiccups, investors are still drawn to the Dollar because of its traditional role as a safe-haven currency during times of turmoil.

This combination—weak Chinese demand, cautious Fed language, and ongoing US political gridlock—creates a perfect storm for the New Zealand Dollar. It’s a reminder that even though domestic economic data in New Zealand can influence the NZD, global events often play a far bigger role.

What Traders and Investors Are Watching Next

After several weeks of steady decline, market participants are now watching upcoming New Zealand economic reports closely. Labor market data and the next round of PMI readings are expected to shed more light on how the domestic economy is holding up.

Strong employment numbers or signs of resilience in New Zealand’s private sector could help stabilize the currency in the short term. On the other hand, if the data confirms further weakness, the NZD could face additional pressure.

For investors, the key is not only the data itself but also how it compares to expectations. In foreign exchange markets, surprises matter more than actual numbers. If New Zealand’s economic indicators outperform forecasts, traders might see a rebound in the Kiwi. But if the reports disappoint again, the downward trend could easily continue.

Meanwhile, all eyes remain on the Federal Reserve. Any new statement from US policymakers about interest rates or inflation could shift sentiment quickly. Since global markets are interconnected, even small changes in tone from the Fed can ripple across major currency pairs, including NZD/USD.

How the Broader Economic Climate Influences Currency Movements

Currency markets are a reflection of global confidence. When investors believe that economic growth will continue, they tend to buy currencies linked to trade and commodities, such as the New Zealand and Australian Dollars. But when fear or uncertainty enters the picture, they flock to safer options like the US Dollar, the Swiss Franc, or the Japanese Yen.

In today’s environment, most of the world’s major economies are showing signs of cooling. Manufacturing growth is slowing, inflation remains uncertain, and central banks are divided about whether to cut rates further. These factors make markets extremely sensitive to every piece of data or central bank comment.

For New Zealand, which relies on foreign investment and international trade, this means that global trends matter as much—if not more—than local conditions. Even if New Zealand’s economy performs reasonably well, a slump in China or a strong US Dollar can still drag the Kiwi down.

Final Summary

The recent fall in the New Zealand Dollar reflects a mix of global and domestic pressures. Weak Chinese manufacturing data has reduced demand for New Zealand’s exports, while a cautious Federal Reserve has kept the US Dollar strong. Add to that the uncertainty from the ongoing US government shutdown, and it’s easy to see why traders are favoring safer assets.

Moving forward, the market will be watching closely for signs of stability in both New Zealand and China. Any improvement in trade sentiment or positive data could help the Kiwi recover some ground. But as long as global uncertainty remains high and the US Dollar stays firm, the New Zealand Dollar may continue to face an uphill battle.

In short, the story of the NZD right now is one of global dependency. The currency’s fortunes are tied not just to local performance but to the broader health of the global economy—and that means volatility could remain a key feature in the weeks ahead.