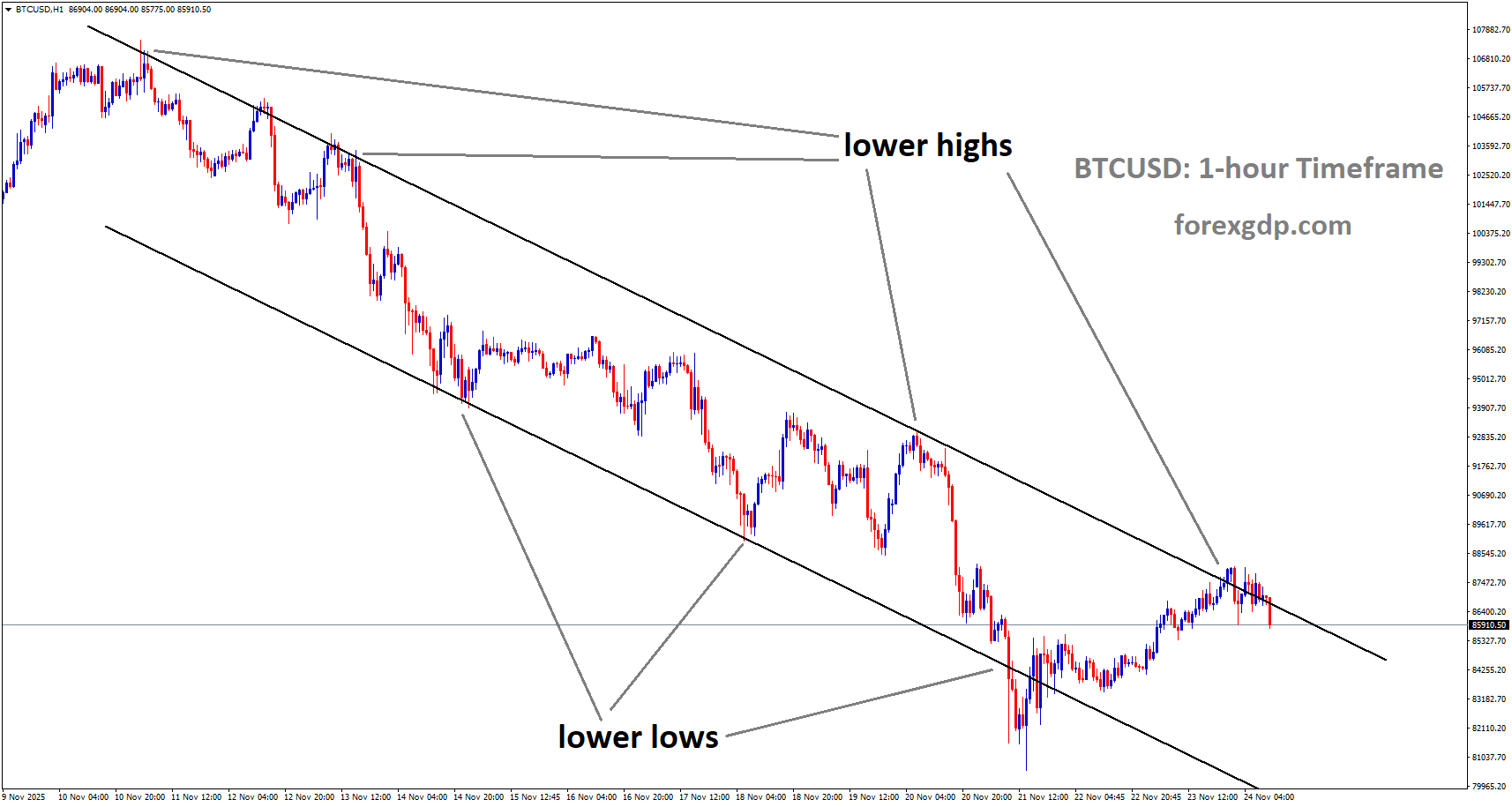

BTCUSD is moving in a descending channel, and the market has reached the lower high area of the channel

BTCUSD Climbs Sharply as Powell Hints at a Year-End Fed Rate Reduction

Bitcoin has shown a powerful recovery in recent days, lifted by growing confidence that the U.S. Federal Reserve may lower interest rates at its upcoming December meeting. After slipping earlier in the week, the digital asset quickly regained momentum as traders reacted to shifting expectations within the Fed and signs that monetary policy could soon become more accommodative.

As speculation builds, attention is turning toward the internal debate among Fed officials and the role Chair Jerome Powell may play in steering a divided committee toward a rate reduction. This debate, combined with improving sentiment across the broader crypto market, is helping fuel renewed interest and activity among investors.

Fed Officials Split on Policy Direction

Inside the Federal Reserve, views on interest rates appear sharply mixed. Several governors have signaled support for easing monetary conditions, pointing to slowing economic indicators and a belief that the economy could benefit from a modest reduction. Others, however, remain cautious and prefer to maintain current rate levels until more data offers clearer guidance.

A group of policymakers—including those known for prioritizing caution—are leaning toward holding rates steady. Their hesitation reflects concerns that inflation may not be cooling fast enough and that lowering rates too soon could reignite upward pressure on prices. This camp prefers to wait for more consistent economic signals before making further adjustments.

Meanwhile, another group of officials appears open to additional cuts if upcoming data suggests that inflation continues to ease and growth remains stable. These members are neither fully committed nor opposed to a rate decrease, choosing instead to allow data in the weeks ahead to influence their final position.

This division increases the likelihood that Powell’s leadership could be pivotal. If he believes a rate cut is necessary, he may need to use his influence to build consensus among colleagues who remain hesitant.

Chair Powell’s Potential Influence

Powell’s role in guiding the Federal Reserve’s decisions has always been central, but in moments of division, his ability to unify the committee becomes even more important. Analysts suggest that, if he chooses to advocate for a small interest rate reduction, he may need to speak more forcefully than usual to persuade those on the fence.

This scenario aligns with rising market expectations. Tools used to measure interest rate forecasts now show a significantly higher chance of a rate cut compared to just days earlier, indicating how quickly sentiment has shifted. Market observers believe Powell may emphasize the importance of flexibility and responsiveness, especially given recent signs of moderation in inflation and consumer demand.

Supporting this view, remarks from Treasury Secretary Scott Bessent have helped calm fears about inflationary pressures. He recently stated that rising service-sector activity is not linked to imported goods or tariffs, reducing concern that external factors are driving costs higher. This has reinforced the belief that inflation risks may be more contained than previously thought.

Bitcoin’s Market Momentum Strengthens

Bitcoin’s rebound reflects more than just speculation about interest rates. The cryptocurrency continues to benefit from a mix of underlying factors that have strengthened the digital asset market throughout the year.

Trading activity has expanded noticeably, suggesting renewed engagement from both retail and institutional participants. Rising demand for Bitcoin-focused investment products, as well as increasing activity among larger market holders, has added to the sense of optimism. Observers believe these trends may continue if the Federal Reserve confirms a more accommodative stance in December.

The potential for a rate cut often influences interest in alternative assets. When borrowing costs decrease and traditional yields soften, investors frequently explore other ways to pursue returns. Bitcoin, despite its volatility, has repeatedly shown that it attracts heightened attention during periods of monetary easing.

Divided Fed Signals an Uncertain Path Ahead

Although the market is leaning toward expectations of lower rates, the internal disagreement within the Federal Reserve highlights the uncertainty that still surrounds the economic outlook. Some officials worry that inflation could fluctuate if policy becomes too loose too soon, while others see enough moderation to justify adjusting the target range now rather than later.

This clash of perspectives often appears when the economy is transitioning from one phase to another. Recent indicators show a mix of strengths and weaknesses: the job market remains resilient, consumer activity has softened in some areas, and inflation—though easing—still sits above the Fed’s long-term target.

This environment makes monetary policy harder to calibrate. A cautious path may limit economic risk but could also slow momentum. A faster shift toward easing could support growth but carries the risk of misjudging inflation’s trajectory. Powell’s response, therefore, will be essential in shaping the final decision.

Broader Forces Supporting Bitcoin’s Revival

Beyond monetary policy, Bitcoin’s recent momentum is reinforced by several positive forces. Renewed interest in Bitcoin-based investment funds continues to bring fresh liquidity into the market. Large holders—sometimes called “whales”—have been increasing their accumulation, which reduces available supply and reinforces market stability.

Additionally, rising participation in certain derivatives markets, such as call options, reflects growing confidence among traders that Bitcoin may still have room to climb. These elements combined create a strong foundation for ongoing market strength, even if short-term fluctuations persist.

Institutional participation, in particular, has played a key role in expanding the digital asset ecosystem this year. The introduction of regulated investment pathways has opened the door for larger firms to participate more actively, adding credibility and long-term support.

What Market Participants Are Watching Next

With the December Federal Reserve meeting approaching, traders, analysts, and investors are paying close attention to incoming economic data. Reports on employment, consumer spending, and inflation will likely shape the final tone of the discussion inside the Fed.

A clearer signal from Powell could also influence expectations. If he emphasizes caution, markets may temper their outlook. If he signals readiness to support easing, excitement around alternative assets—including Bitcoin—could strengthen further.

Analysts also note that seasonal dynamics heading into the end of the year tend to bring increased activity across financial markets. This period can amplify trends already in motion, especially when combined with heightened public attention and shifting macroeconomic narratives.

Summary

Bitcoin’s recent rebound reflects a combination of improving sentiment, rising trading activity, and growing expectations that the Federal Reserve may choose to lower interest rates in December. While Fed officials remain divided on the best path forward, Chair Powell’s leadership may ultimately influence the final decision. At the same time, broader market forces such as institutional adoption and increased participation continue to support Bitcoin’s momentum. As the year draws to a close, all eyes remain on economic data and the Fed’s next move, both of which could shape the trajectory of the cryptocurrency market in the weeks ahead.

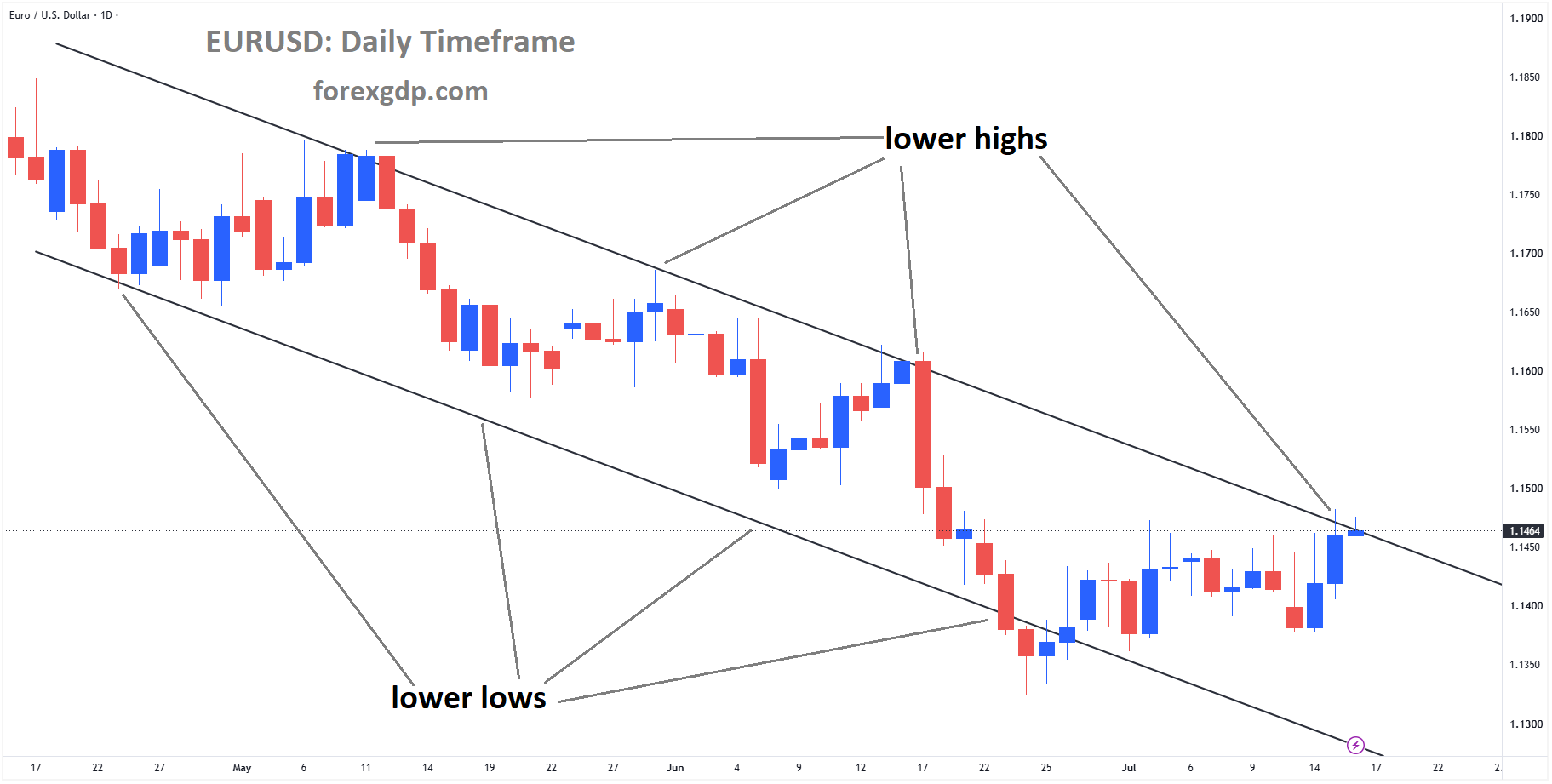

EURUSD pushes ahead as the Dollar softens on shifting market mood

The Euro began the week on a stronger note, building momentum against the US Dollar after last week’s drop. The currency pair moved toward the 1.1540 level, recovering from Friday’s dip near 1.1490. This improvement came during a quiet start to the week, supported by a mild appetite for risk across global markets. Although fresh data from Germany showed a decline in business confidence for November, the news had only a limited effect on the Euro’s performance.

Investors continued to respond to reassuring remarks from New York Federal Reserve President John Williams, whose comments encouraged expectations of future rate cuts. His outlook helped weaken the US Dollar from its recent highs and offered support to the Euro’s recovery.

Market Drivers Supporting the Euro

The general tone of the market has remained upbeat, encouraged by the possibility of easier monetary policy ahead. Williams’ statements on Friday suggested that the Federal Reserve still has room to lower interest rates without jeopardizing its goal of keeping inflation under control. This perspective eased concerns of a more aggressive policy stance and drew investors toward assets perceived as riskier, benefiting the Euro.

EURUSD is moving in a box pattern, and the market has reached the resistance area of the pattern

Risk sentiment was also lifted by renewed hopes for progress toward a peace agreement in Ukraine. European equity markets opened with gains, adding to the risk-friendly environment and helping the common currency regain lost ground.

German and Eurozone Data Present a Mixed Picture

Business Climate Weakens in Germany

Despite the overall positive market tone, economic indicators from Germany offered less encouraging news. The latest reading of the German IFO Business Climate Index fell to 88.1 in November, slipping from 88.4 in October. Analysts had anticipated a slight improvement, making the decline a mild disappointment. Although the assessment of the current economic situation remained stable, expectations for the future worsened noticeably, reflecting ongoing uncertainty in Europe’s largest economy.

Eurozone PMIs Show Manufacturing Contraction

Manufacturing activity across the Eurozone also softened. Preliminary figures for November revealed a surprise contraction in the sector, dropping to 49.7. Analysts had expected a move above the 50 mark, which separates contraction from expansion. While the services sector showed a slight improvement, the overall composite index edged lower, signaling that the region’s economy is struggling to gain momentum.

Germany’s manufacturing sector posted a similar trend, with its PMI falling further to 48.4. The sharp drop in the services reading, which slipped from 54.6 to 52.7, emphasized the challenges facing Europe’s economic engine.

US Data and Fed Comments Influence Dollar Direction

US Economic Reports Offer Modest Strength

Across the Atlantic, the United States released a set of economic indicators that painted a mixed but generally positive picture. The preliminary Manufacturing PMI eased slightly but remained above the 50 level, showing ongoing expansion in the industry. The services sector outperformed expectations with a reading of 55.0, helping lift the composite index.

Consumer confidence also improved, with the Michigan Consumer Sentiment Index rising to 51 in November. Expectations for the future move higher as well, suggesting that US consumers may feel more optimistic heading into the end of the year.

Dovish Signals from the Fed Weigh on the Dollar

Despite these encouraging numbers, the US Dollar weakened as markets focused on comments from Federal Reserve President Williams. His message signaled openness to further rate cuts in the near future, which investors interpreted as a more growth-friendly and less restrictive stance. This shift reduced demand for the Dollar, supporting the Euro’s upward trajectory.

Looking Ahead: ECB Remarks on the Horizon

Later in the day, European Central Bank President Christine Lagarde is scheduled to speak at a forum in Slovakia. While the topic centers on artificial intelligence and education, investors will still pay close attention for any unexpected remarks that could hint at the future direction of monetary policy in the Eurozone.

Summary

The Euro regained strength at the start of the week, supported by a brighter market mood and expectations of more flexible monetary policy in the United States. While economic data from Germany and the broader Eurozone showed signs of softness, the impact on the currency was limited. In contrast, the US Dollar eased as investors reacted to dovish comments from the Federal Reserve. As markets await remarks from ECB President Christine Lagarde, the Euro continues to benefit from a mix of improving sentiment and shifting central-bank expectations.

GBPUSD drifts lower beneath 1.3100 while a stronger USD and UK fiscal concerns pressure sentiment

The new trading week opens with the GBP/USD pair moving slightly lower, reflecting a stronger US Dollar and ongoing uncertainty in the United Kingdom. While the currency pair remains above last week’s low, it struggles to build on the modest progress made in recent sessions. Several key developments on both sides of the Atlantic are shaping sentiment, making this an important week for anyone watching the movement of the British Pound against the US Dollar.

The Dollar Finds Support as Fed Expectations Shift

The US Dollar begins the week with a noticeable advantage, supported by expectations that the Federal Reserve may not be as inclined toward further interest rate cuts as previously thought. Recent economic data out of the United States has helped fuel this view. The delayed release of September’s Nonfarm Payrolls report showed that hiring remained resilient, offering a sign that the economy continues to hold up despite broader concerns.

GBPUSD is moving in a descending channel, and the market has reached the lower high area of the channel

The longest-ever US government shutdown had raised fears that economic momentum could falter, but the strong labor report helped ease those worries. As a result, investors now see fewer reasons for the Fed to deliver another rate cut in December. This shift in expectations has lifted the US Dollar Index to its highest levels since late spring, giving the Greenback an edge over several major currencies, including the Pound.

With the Dollar strengthening, the GBP/USD pair is finding it difficult to push higher. Although declines remain limited for now, the broader tone favors the USD, and traders are watching closely to see whether upcoming US data reinforces this momentum.

UK Budget Uncertainty Pressures the Pound

While the US Dollar benefits from stronger economic signals, the British Pound continues to face its own challenges. One of the biggest sources of uncertainty is the upcoming UK budget, which will be announced by Chancellor Rachel Reeves. Markets remain cautious as they wait to see how the government plans to manage spending, taxes, and economic priorities in the face of ongoing financial pressures.

This uncertainty has encouraged expectations that the Bank of England could cut interest rates as soon as next month. With inflation easing from its peak and economic growth still sluggish, some investors believe the BoE may see room to lower borrowing costs. These rate-cut expectations have weighed on the Pound, contributing to its underperformance against the Dollar and other major currencies.

For now, traders appear hesitant to take strong positions in either direction. With major announcements ahead, many prefer to wait for clearer signals before committing to a more decisive view on the Pound’s trajectory.

What to Watch in the UK This Week

All eyes in the UK will be on the Autumn Budget announcement. The decisions laid out on Wednesday may influence the Pound’s tone in the days and weeks ahead. Investors will be looking for clarity on fiscal strategy, growth plans, and potential policy changes that could affect economic confidence.

If the budget reassures markets, the Pound could find some support. However, any signs of increased financial strain or limited room for stimulus may strengthen the argument for an upcoming rate cut, which could keep the currency under pressure.

Key US Data Releases Likely to Drive Market Moves

The United States also has a packed economic calendar this week, and each release will play a role in shaping expectations for the Fed’s next steps. Among the most important reports are the Producer Price Index, Retail Sales, and the Consumer Confidence Index, all scheduled for release on Tuesday.

Later in the week, the focus will shift to the preliminary estimate of third-quarter GDP and the closely watched Personal Consumption Expenditure Price Index. The PCE report is the Fed’s preferred measure of inflation, making it especially important for markets. If the data suggests inflation is easing steadily, it could revive calls for rate cuts in the coming months. If it remains stubborn, the Dollar may find even more support.

These releases are expected to bring fresh momentum to the GBP/USD pair. Stronger-than-expected US data would likely keep the Dollar in control, while softer figures could open the door for the Pound to recover some ground.

Market Sentiment Remains Cautious

With both the UK and US facing significant economic events, traders appear cautious in the early part of the week. The Pound remains under pressure, but not dramatically so, as investors wait for clearer direction. Meanwhile, the Dollar continues to benefit from a solid backdrop of improving data and reduced expectations for rapid monetary easing.

In this environment, the GBP/USD pair is likely to stay sensitive to any shifts in expectations for interest rates, government policy, and overall economic performance. Each new piece of information could sway market sentiment, creating potential swings in either direction.

Final Summary

The GBP/USD pair enters the week on weaker footing, influenced by a stronger US Dollar and ongoing uncertainty surrounding the upcoming UK budget. Shifting expectations for Federal Reserve policy have supported the Dollar, while speculation about a possible Bank of England rate cut has weighed on the Pound. With significant economic reports due from both countries, traders are bracing for a busy week that could set the tone for the currency pair’s next major move.

USDJPY Edges Higher as Yen Weakness Persists and Momentum Stalls

The Japanese Yen opened the new week weaker as investors reacted to rising concerns around the country’s financial health and ongoing uncertainty about the future path of monetary policy. Although the Yen managed a modest recovery against a slightly softer US Dollar, it continued to trade with a negative tone during the Asian session. The mood in the market remained cautious, and the Yen struggled to shake off the pressures that have been building over recent weeks.

One of the key forces weighing on the currency is the perception that Japan’s fiscal position is becoming more fragile. At the same time, expectations that the Bank of Japan will delay raising interest rates have added another layer of pressure. This combination has kept the Yen from gaining meaningful traction despite moments of temporary relief.

Government Spending Sparks Fresh Fiscal Concerns

On Friday, Japan’s cabinet approved a large economic stimulus package worth ¥21.3 trillion. This marks the first major policy initiative under Prime Minister Sanae Takaichi and signals a commitment to supporting the economy through government spending. The plan includes ¥17.7 trillion in general account outlays—significantly higher than last year’s spending—as well as tax cuts totaling ¥2.7 trillion.

USDJPY has broken the uptrend channel on the upside

While the intention is to strengthen the economy, the scale of the package has raised eyebrows among investors. Concerns are growing that the new spending will add to Japan’s already heavy debt load. The possibility of increased government borrowing has pushed Japan’s borrowing costs toward their highest level in decades. This renewed strain on public finances has made investors more cautious about holding the Yen.

Economic data released last week added to the worry. Japan’s economy contracted in the third quarter for the first time in six quarters, suggesting that growth momentum is weakening. This setback increases pressure on the Bank of Japan to avoid tightening monetary policy too soon, reinforcing the belief that a rate hike may not come as quickly as previously expected.

Mixed Signals Keep Markets on Edge

Beyond Japan’s domestic challenges, global market sentiment also played a role in shaping Yen movements. Investors have generally been more willing to take on risk, and this has reduced demand for safe-haven currencies like the Yen. Trading conditions were relatively light due to a holiday in Japan, giving the market fewer catalysts to shift the currency’s direction.

Meanwhile, the US Dollar has been hovering near levels last seen in late May. Traders have scaled back expectations for another interest rate cut from the US Federal Reserve in December, giving the Dollar underlying support. Minutes from the Fed’s October meeting suggested that policymakers remain cautious about easing monetary policy too soon, fearing that premature action could allow inflation pressures to stick around longer.

A stronger-than-expected US jobs report for September further reduced concerns about weakening labor conditions and supported the view that the Fed may not need to act quickly. These developments limited the Yen’s ability to recover against the Dollar, even as the greenback experienced a small dip.

Policymakers Offer Cautious Messages on the Yen

Amid these market dynamics, Japanese officials have been voicing their concerns about the weakening currency. Bank of Japan Governor Kazuo Ueda warned that a falling Yen could increase import costs and add upward pressure to prices at home. Although inflation has remained above the BoJ’s 2% target, the central bank has resisted making abrupt changes to its policy stance. Still, a recent poll from Reuters showed that a slim majority of economists believe the BoJ could raise rates in December.

Finance Minister Satsuki Katayama issued one of the strongest signals yet that the government is prepared to act if currency movements become too volatile. He emphasized that authorities would take action as needed to address disorderly market behavior. The possibility of intervention has helped limit the Yen’s losses, as traders remain wary of triggering a response from policymakers.

Adding to this, an adviser to Prime Minister Takaichi noted that Japan has ample foreign reserves and could use them to support the Yen if necessary. Such comments suggest that Tokyo is closely monitoring the situation and is willing to step in if the currency weakens too quickly.

A Market Waiting for Clearer Direction

The tug-of-war between domestic pressures, global trends, and policy signals has created a complex outlook for the Japanese Yen. On one hand, fiscal concerns, a cautious central bank, and stronger global risk appetite continue to weigh on the currency. On the other, intervention warnings and lingering expectations of eventual policy tightening help prevent sharp declines.

For now, traders appear hesitant to make bold moves in either direction. The path forward may depend on upcoming economic data, clarity from the Bank of Japan, and whether the government continues to expand fiscal support. Shifting expectations for US monetary policy will also play a major role in shaping the Dollar-Yen dynamic.

Summary

Japan’s currency began the week under pressure as investors reacted to rising fiscal risks and uncertainty over the Bank of Japan’s next steps. A large new stimulus package and signs of economic weakness have raised doubts about the country’s financial stability. At the same time, mixed messages from the US Federal Reserve and stronger global risk appetite have influenced the Dollar-Yen balance. While warnings of possible intervention have limited deeper losses, the market remains cautious, waiting for clearer signals from policymakers and economic indicators.

GBPJPY edges higher while traders brace for upcoming UK fiscal plans

The British Pound is having trouble gaining strong momentum against the Japanese Yen, even though the Yen remains under pressure. After dipping to 204.30 late last week, the Pound has managed a modest recovery but continues to stall around the 205.00 mark. Traders appear hesitant to commit to larger positions as they wait for important political and economic developments in the United Kingdom and Japan.

Budget Expectations Shape Sentiment

With the UK Autumn Budget set to be unveiled next Wednesday, many investors are choosing caution over confidence. The upcoming budget is expected to introduce meaningful tax increases as the government looks for ways to reduce the country’s growing fiscal deficit.

GBPJPY is moving in an uptrend channel, and the market has reached a higher high area of the channel

Chancellor Rachel Reaves had earlier hinted at raising income taxes before pulling back on the idea, but pressure on public finances suggests that tax measures are still likely. These expectations are influencing market behavior, prompting investors to remain careful until the details are made public.

The possibility of higher taxes also affects the broader economic outlook. Increased tax burdens could create additional pressure on household spending and business activity. This may leave the Bank of England in a position where it needs to soften monetary conditions in the coming months to help cushion the economy.

Some recent data from the UK has already pointed toward slower growth, raising concerns that the country may be heading toward a more noticeable economic downturn. This combination of softer economic indicators and expectations of tighter fiscal policy makes future rate cuts more likely, adding another layer of uncertainty for the Pound.

Japan Faces Its Own Headwinds

Takaichi’s Major Spending Plan Weighs on the Yen

While the Pound’s struggle is partly tied to domestic uncertainty, the Yen is also under notable pressure due to developments within Japan. Prime Minister Sanae Takaichi’s government recently approved a large stimulus package worth 21 trillion Yen. The plan aims to support the economy, but it has sparked fresh concerns about Japan’s already strained public finances.

Large-scale spending programs can provide short-term economic benefits, but they often raise fears about debt sustainability. For Japan, where public debt is already among the highest in the world, another round of heavy spending adds to these worries. As a result, the Yen has continued to weaken, unable to gain meaningful support even when the Pound softens.

Intervention Rumors Stir Market Anxiety

Signs of discomfort from Japanese authorities have grown in recent days. The government issued a strong warning late last week, signaling that it might step in to limit excessive volatility in foreign exchange markets. Such warnings are typically designed to discourage traders from pushing the Yen too low too quickly.

Despite the stern language, investors are still betting against the Yen for now. Many believe the Bank of Japan will wait before taking any direct action. Historically, the Bank tends to intervene when market activity is quieter, allowing any move to have a stronger impact. With the US preparing for the Thanksgiving holiday on Thursday, trading volumes are expected to thin out, making late-week intervention a plausible scenario.

A Market Searching for Direction

Both currencies are caught in a push-and-pull between competing economic signals and policy expectations. The Pound is struggling to build upward momentum as traders wait for clarity on the UK’s fiscal plans. Meanwhile, the Yen is weighed down by concerns over government spending and speculation about whether and when Japan will intervene.

This has left the GBP/JPY pair drifting without a clear direction. Traders appear comfortable holding smaller positions while they wait for key developments. The combination of a major UK budget announcement and the possibility of Japanese intervention later in the week may lead to more decisive moves once the picture becomes clearer.

What Traders Are Watching Now

UK Budget Details

The Autumn Budget is expected to set the tone for the Pound in the short and medium term. Investors will look closely at how aggressive the tax measures are and whether the government provides any signals about its long-term economic priorities. Any hint that the fiscal outlook may weaken further could deepen concerns about economic growth, making future rate cuts even more likely.

Bank of England Signals

Although no immediate action is expected, the Bank of England’s message in the coming weeks will be essential in shaping expectations. If policymakers suggest that tax increases may require monetary easing to support the economy, the Pound could face additional pressure.

On the other hand, if the Bank signals confidence in the resilience of the UK economy, investors may become more comfortable taking on larger positions.

Possible Japanese Intervention

Many traders will keep an eye on the Yen as the week progresses. Japanese officials have shown increasing concern about rapid currency movements. If the Yen weakens further or if volatility picks up, authorities may feel compelled to act sooner rather than later. The timing of any intervention—especially around periods of lighter trading—could significantly influence market reactions.

Summary

The Pound is struggling to gain ground against the Japanese Yen as investors weigh upcoming fiscal decisions in the UK and rising speculation of currency intervention in Japan. With the UK expected to introduce tax increases to address its fiscal challenges, and Japan pushing forward with a large stimulus package that raises debt concerns, both currencies are facing pressures from different directions. Markets remain cautious, watching closely for key developments in the week ahead that may shape the next major move in the GBP/JPY exchange rate.