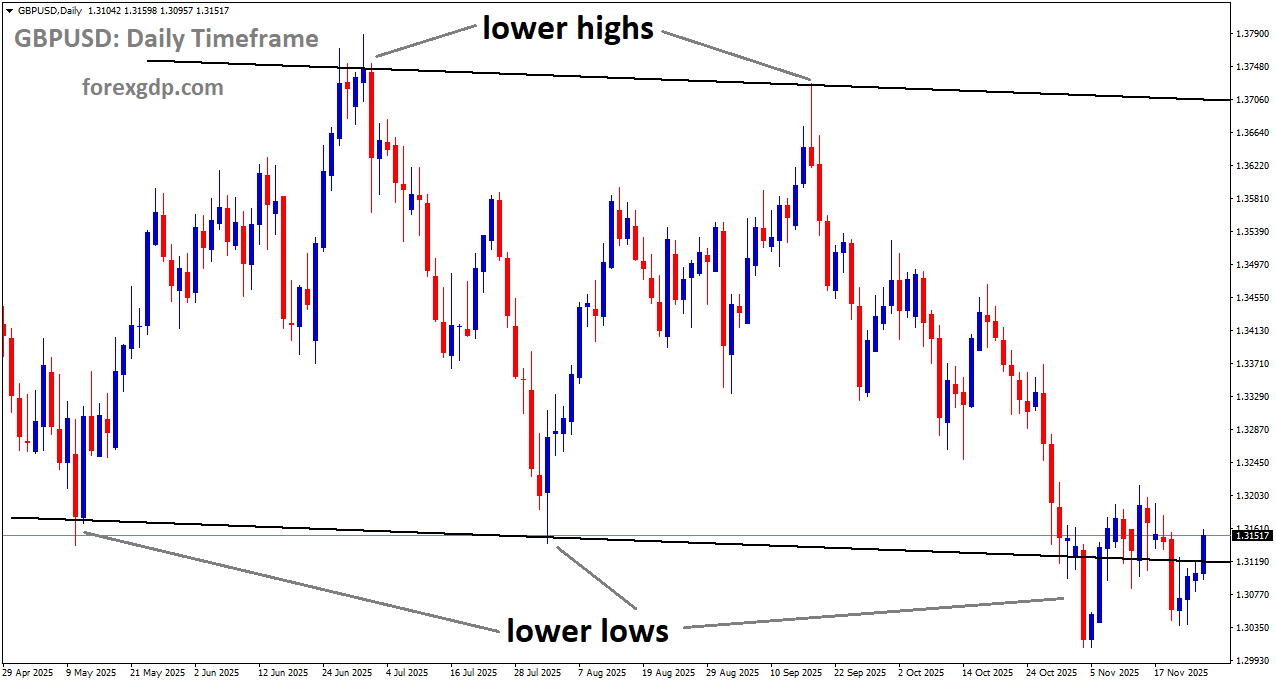

GBPUSD is moving in a downtrend channel, and the market has reached the lower low area of the channel

GBPUSD edges down to the 1.3100 zone as UK debt markets weaken

The British Pound has been facing renewed pressure, slipping after several days of gains as investors react to softer economic signals coming out of the United Kingdom. One of the key drivers behind the latest pullback is the drop in UK 10-year Gilt yields. As yields move lower, they often reflect fading confidence in the broader economic outlook or expectations of easier monetary policy.

This shift comes at a crucial moment, with the UK government preparing for the upcoming November 26 budget. Investors are paying close attention to how the new fiscal plan will attempt to balance spending goals with existing fiscal rules. Finance Minister Rachel Reeves is widely expected to search for significant cost-saving measures—potentially tens of billions of pounds—to stay within the government’s financial framework.

Adding to the cautious tone, the Office for Budget Responsibility is preparing to update its growth and productivity outlook. Early indications suggest these projections may be downgraded, creating another layer of uncertainty for markets watching the relationship between government spending and future economic potential.

Softer UK Inflation Pushes BoE Rate Cut Expectations Higher

Another major weight on the Pound is the shift in expectations around Bank of England policy. October’s inflation numbers revealed a slowdown to 3.6%, offering fresh evidence that price pressures in the UK are continuing to ease. While cooler inflation can be a sign of economic stabilization, it also increases the likelihood that the Bank of England may move toward cutting interest rates sooner rather than later.

Markets are now leaning heavily toward the possibility of a rate cut in December, with bets rising sharply in recent days. Many investors see an 80% chance of a 25-basis-point reduction. Lower interest rates tend to make a currency less attractive to global investors, which helps explain the Pound’s recent weakness against the US Dollar.

As the budget approaches and inflation cools, the atmosphere surrounding UK monetary policy has noticeably shifted. The combination of subdued yields, softer economic data, and the prospect of easier policy is creating a challenging environment for the Pound in the short term.

US Dollar Rebounds Despite Expectations for a Fed Rate Cut

On the other side of the Atlantic, the US Dollar has been showing signs of renewed strength, even as expectations build that the Federal Reserve may cut rates at its December meeting. This may seem counterintuitive, but the Dollar’s performance reflects a complex mix of economic data, central bank communication, and global risk sentiment.

Many traders had initially expected the Dollar to weaken as speculation about a rate cut increased. Instead, the currency has recovered some of its earlier losses, suggesting that investors may still see the United States as a relatively stable and resilient economy compared with other major markets.

Recent comments from Federal Reserve officials have contributed to shifting expectations. Fed Governor Christopher Waller noted that inflation has become less of a pressing concern, especially given the softer tone in US employment data. He highlighted signs of a weakening labour market and suggested that previous job figures, including the September payrolls report, may even be revised lower.

Waller also expressed concern about hiring becoming concentrated in only a few sectors, which he described as “not a good sign” for broader economic health. These remarks reinforce the idea that the Fed may consider reducing rates to support the labour market, a view that has gained momentum in financial markets.

Rising Market Probability of a Fed Rate Cut

Market tools tracking investor expectations are now signalling a strong likelihood of a policy shift in December. Many traders are pricing in an 81% probability of a 25-basis-point cut at the upcoming Federal Reserve meeting. This is a notable increase from just a day earlier, when expectations stood at 71%.

GBPUSD is breaking the lower high area of the downtrend channel

Such rapid adjustments show how sensitive markets have become to changes in economic data and central bank messaging. Even with rate cut expectations rising, the Dollar’s ability to remain firm hints at underlying confidence in the US economy or, alternatively, concern about the outlook for other major currencies—including the Pound.

How These Shifts Affect the GBP/USD Pair

The GBP/USD pair has been struggling to hold recent gains, drifting lower during Asian trading hours. The exchange rate’s movements reflect a tug-of-war between UK-specific pressures and US economic developments.

On one hand, weakening Gilt yields, softening inflation, and heightened expectations of a Bank of England rate cut have weighed heavily on the Pound. On the other hand, the US Dollar has been supported by cautious comments from Federal Reserve officials, even in the face of growing speculation around near-term rate reductions.

Together, these factors create a landscape in which the Pound finds it difficult to build momentum against a Dollar that continues to draw investor demand.

Final Summary

The recent decline in GBP/USD highlights the impact of changing economic expectations in both the UK and the US. In the UK, falling bond yields, a softer inflation reading, and anticipation of the November 26 budget have pushed investors to price in an upcoming Bank of England rate cut. These developments have combined to create downward pressure on the Pound.

Meanwhile, the US Dollar has regained strength despite higher odds of a Federal Reserve rate cut in December. Comments from Fed officials about labour market weakness and softer employment data have influenced market expectations, but the Dollar remains resilient.

As both central banks navigate uncertain economic landscapes, the GBP/USD pair is likely to remain sensitive to shifts in policy tone, economic data releases, and broader market sentiment in the weeks ahead.

EURUSD Holds Steady as Traders Await Key US Spending and Price Reports

The Euro is showing small gains in the latest European trading session, yet it continues to struggle within a narrow range. Market participants are paying close attention to economic news from both sides of the Atlantic as they look for clues about the next moves in global monetary policy. With mixed signals coming from the Eurozone and growing expectations of policy easing in the United States, traders are navigating an environment filled with uncertainty, shifting sentiment, and cautious optimism.

The Euro’s Modest Performance Amid Limited Support

The Euro’s recent movement has been modest, reflecting a currency caught between weak regional data and a softer US Dollar. While the Euro has managed to inch slightly higher, it remains unable to break through the upper boundary of its recent trading zone. This limited upward momentum is linked to the lack of encouraging economic signals from Europe’s largest economy, Germany.

EURUSD is moving in an uptrend channel, and the market has reached a higher high area of the channel

Fresh data out of Germany confirmed that the economy did not expand in the most recent quarter. This follows a decline in the previous quarter, reinforcing concerns that growth remains fragile. Despite a small improvement in the yearly rate, the stagnant quarterly performance has done little to lift confidence among investors who are already wary of the broader Eurozone outlook.

German Indicators Highlight Ongoing Economic Challenges

Germany continues to face significant economic hurdles. The latest figures show that growth has stalled, matching earlier estimates and leaving the country stuck between weak industrial activity and slow consumer demand. Although annual growth has shown a slight improvement, the current pace still falls short of what would be considered healthy for Europe’s economic engine.

Further signs of strain emerged from recent business sentiment surveys. The latest reading of a well-known business climate index slipped again, missing expectations of a slight improvement. While the assessment of current conditions showed a small uptick, expectations for the months ahead declined noticeably. This drop in confidence underscores concerns that companies are becoming more pessimistic about the near-term economic environment.

Taken together, these reports paint a picture of an economy struggling to regain momentum. Investors are mindful that Germany’s difficulties often spill over into the wider Eurozone, creating headwinds for the currency.

Growing Expectations of US Policy Easing

Across the Atlantic, the story is different. Several officials from the Federal Reserve have recently voiced support for additional monetary easing. Their remarks have fueled speculation that the US central bank may move forward with another interest rate cut in the near future.

One high-profile official emphasized signs of a weakening labor market and expectations that inflation will continue to slow. These comments echoed earlier remarks from another senior figure at the central bank, reinforcing the sense that policymakers are increasingly open to reducing borrowing costs again. Market-based measures now indicate a strong probability of such a move, a notable jump from expectations just a week earlier.

A softer US Dollar has been one of the immediate effects of this shift in sentiment. With traders anticipating a potential rate cut, pressure has built on the currency, giving the Euro some breathing room despite its own regional challenges.

Geopolitical Developments Add Another Layer of Influence

Beyond economic data and central bank communication, global politics also helped shape the atmosphere this week. The US President reported positive developments in diplomatic relations with China following a conversation with the Chinese leader. Shortly afterward, a call to Japan’s prime minister signaled an effort to soothe tensions between two major Asian powers.

While these gestures are not directly tied to currency movements, improvements in geopolitical stability can reduce risk aversion in financial markets. This, in turn, can influence the way traders position themselves, particularly in periods of heightened economic uncertainty.

Anticipation Builds Ahead of Key US Releases

Although several European Central Bank officials are scheduled to speak later, the primary focus remains on upcoming US economic releases. Investors are awaiting new inflation data from the business sector, consumer spending figures, and an update on consumer confidence. These reports were originally delayed and are now set for release later in the day, increasing the level of anticipation.

Inflation as measured by producer prices is expected to show faster monthly growth compared to previous readings, with the annual rate also projected to rise. However, core inflation—an important measure that strips out volatile components—is expected to cool slightly. Meanwhile, retail sales are forecast to expand but at a slower pace than the previous month, both overall and when excluding vehicle purchases.

These releases will offer fresh insights into the health of the US economy and could influence expectations for the Federal Reserve’s next steps. Stronger inflation or robust consumer spending could complicate the case for easing, while weaker data may reinforce current expectations of a rate cut.

The Euro Holds Steady as Markets Await Clarity

With mixed signals coming from economic data and central bank commentary, the Euro is holding steady near a middle ground. It reflects a currency waiting for a clearer direction, caught between domestic stagnation and shifting US monetary expectations.

The Zone’s largest economy is not showing signs of meaningful improvement, and business sentiment continues to face headwinds. At the same time, the potential for further US policy easing has reduced some of the upward pressure on the Dollar, creating a more balanced dynamic in the currency pair.

Investors are eager to see whether the upcoming US data will strengthen or weaken the argument for additional monetary support. For now, the focus remains heavily geared toward the Federal Reserve and the broader direction of the US economy.

Summary

The Euro is trading within a tight range as traders navigate a combination of weak German data, cautious business sentiment, and anticipation of key US economic figures. Germany’s stalled growth and declining expectations continue to weigh on the currency, while dovish comments from Federal Reserve officials have softened the US Dollar. Geopolitical signals and upcoming US inflation and retail sales reports add further complexity to an already uncertain environment. Until new data provides clearer direction, both the Euro and the broader market remain in a holding pattern, watching closely for the next major shift in economic momentum.

USDJPY retreats with Japan’s warning tones rising and major US data on the horizon

The USD/JPY pair slipped slightly, hovering near 156.50 as the Japanese Yen struggled to gather strong buying interest. Even though the possibility of action from Japanese authorities is helping prevent a deeper drop, the Yen continues to face a mix of economic and policy challenges that limit its ability to recover.

USDJPY is moving in a box pattern, and the market has reached the resistance area of the pattern

Recent comments from senior officials have put markets on alert. Finance Minister Satsuki Katayama stated that the government is prepared to act if currency swings become too extreme. Takuji Aida, a member of an influential government advisory panel, also pointed to the potential need for direct intervention to soften the economic strain caused by a weaker Yen. Together, these statements have slowed the pace of USD/JPY’s upward movement, as traders remain cautious about pushing the pair too high.

Fiscal Concerns Continue to Weigh on the Yen

Japan’s broader fiscal picture remains a significant hurdle for the currency. The government recently approved a stimulus package worth ¥21.3 trillion, marking one of the largest spending efforts since the pandemic. While the measure aims to support growth, it has raised fresh concerns about the country’s already heavy public debt burden.

These worries have shown up in bond markets, where yields on super-long Japanese government bonds have climbed to record levels. Investors are increasingly uneasy about the long-term sustainability of Japan’s financial strategy, and this skepticism is contributing to ongoing pressure on the Yen.

Economic Weakness Complicates the Bank of Japan’s Next Moves

The latest economic data adds another layer of uncertainty. Japan’s economy contracted in the third quarter, increasing speculation that the Bank of Japan may hold off on additional policy tightening. Although Governor Kazuo Ueda has not ruled out a potential rate adjustment in December, he continues to face a delicate balance.

On one hand, the weak Yen is contributing to higher inflation, which has stayed above the 2% target for more than three years. On the other hand, slower economic growth makes it harder for the central bank to move too quickly. This tension has kept investors guessing about the BoJ’s next steps, and the ongoing uncertainty is another reason the Yen has struggled to regain ground.

US Policy Expectations Influence Market Sentiment

Across the Pacific, the US Dollar has eased slightly as investors look ahead to key economic releases and update their expectations for Federal Reserve policy. Several Fed officials have spoken recently, and their remarks suggest growing support for further monetary easing.

Fed Governor Christopher Waller noted that the labor market is showing signs of cooling, a factor that could strengthen the case for a rate cut. His comments came shortly after New York Fed President John Williams suggested that current policy settings may not be restrictive enough to push inflation decisively lower. Markets now see a strong likelihood of a rate reduction at the Fed’s December meeting.

While this shift in expectations has limited the Dollar’s short-term strength, the broader environment still favors USD/JPY resilience. If the Bank of Japan proceeds cautiously and interest rate differences remain wide, the pair could stay supported.

Key US Data Could Shape the Next Market Move

Looking ahead, traders are watching several upcoming US economic indicators that could influence USD/JPY. Reports on the Producer Price Index, Retail Sales, and various housing and manufacturing metrics may inject new volatility into the market.

These data points will help shape expectations for Federal Reserve policy and may set the tone for the pair’s direction in the days to come. With both the US and Japan at critical points in their economic cycles, the next round of information could play an important role in determining whether USD/JPY continues to hold steady or shifts toward a new trend.

Summary

The USD/JPY pair has softened slightly as traders navigate conflicting signals from Japan and the United States. Japan’s warnings about potential intervention have slowed the Yen’s decline, but concerns about government debt, weak growth, and uncertain central bank policy continue to weigh heavily. In the US, expectations of a December rate cut have taken some momentum out of the Dollar, yet overall conditions still support the currency against the Yen. With several major US data releases on the horizon, market sentiment could shift quickly, making the coming days important for understanding where USD/JPY is headed next.

AUDUSD slips toward 0.6450 as traders brace for Australia’s expanded CPI release

The AUD/USD pair has eased after recent strength, reflecting a cautious mood among traders as they wait for Australia’s newly expanded monthly inflation report. This upcoming data release is viewed as an important indicator of how consumer prices are evolving, even though the Reserve Bank of Australia (RBA) has not yet made it a central tool in its decision-making. Instead, the focus remains on areas like housing and services, which often provide clearer signals about longer-term price pressure.

AUDUSD is moving in a downtrend channel, and the market has reached the lower high area of the channel

Despite the pair’s pullback, the broader sentiment around the Australian Dollar has shown signs of support. Investors believe the RBA may maintain a careful, steady approach to interest rates, avoiding quick moves and watching economic conditions closely. Minutes from the RBA’s recent policy meeting reinforced this idea, showing policymakers are prepared to hold rates steady for a period while evaluating progress toward their inflation target.

RBA’s Cautious Stance Offers Underlying Support for the Australian Dollar

Expectations surrounding the RBA have been a key factor in shaping the direction of the Australian Dollar. With officials signaling patience, traders see less urgency for policy changes in the near term. This sense of stability has helped limit downside pressure on the currency, especially as Australia prepares for more detailed inflation information.

The central bank’s preference for a careful, measured approach reflects uncertainty about how quickly inflation will return to its desired range. Housing costs and service prices remain areas of close attention, as they tend to be slower to adjust and can provide insight into whether price pressures are easing or persisting.

While financial markets previously speculated about future rate changes, the most recent commentary from the RBA emphasized the value of waiting for stronger evidence before making adjustments. This message has reduced expectations for any immediate shift in policy, helping the Australian Dollar avoid a deeper retreat even as global market dynamics evolve.

Fed Rate-Cut Expectations Weigh on the US Dollar

On the other side of the currency pair, the US Dollar has been struggling under growing expectations that the Federal Reserve could lower interest rates in the near future. Recent comments from multiple Fed officials have pointed toward concerns over weakening labor conditions rather than inflation, which has shown signs of easing.

Market indicators suggest that investors now believe there is a strong likelihood of a rate cut at the Fed’s upcoming meeting. This shift in expectations has softened the appeal of the US Dollar, as lower interest rates typically reduce demand for the currency.

The tone from policymakers has played a big role in this adjustment. One senior Fed official noted that the labor market is showing signs of cooling, and that inflation no longer appears to be the primary challenge. He also indicated that past employment figures may be revised lower, reinforcing the view that the economy is losing momentum. Concerns about hiring being concentrated in only a few sectors added to the sense that the job market may not be as healthy as earlier reports suggested.

These factors have strengthened the case for a near-term rate cut, which has in turn limited the downside risk for the Australian Dollar and contributed to the recent pullback in the US Dollar.

What Traders Are Watching Next

With both central banks in a cautious mode, the next key driver for the AUD/USD pair will be Australia’s expanded inflation report. Traders will be watching closely to see whether the data points to easing price pressures or signals lingering cost growth in certain sectors. Housing and services inflation, in particular, will likely have the most influence on market sentiment.

In the United States, market participants will continue monitoring economic indicators such as employment and consumer spending, which play major roles in shaping the Federal Reserve’s decisions. Any signs of further cooling in the US labor market could reinforce expectations of a rate cut and put additional pressure on the US Dollar.

Final Summary

The AUD/USD pair has softened slightly as traders wait for new Australian inflation data and reassess the policy paths of both the RBA and the Federal Reserve. The Australian Dollar remains supported by expectations that the RBA will maintain a steady approach, while the US Dollar faces pressure from rising speculation about a potential Fed rate cut. Shifting economic signals from both countries continue to guide sentiment, making upcoming data releases especially important for determining the next move in the currency pair.

NZDUSD steadies near 0.5600 as traders await the RBNZ’s next move

The New Zealand Dollar has been struggling to gain momentum, staying near the 0.5600 level for a second straight day. This steady hesitation reflects a market that feels uncertain and cautious. Recent daily price movements show long wicks on the charts, a sign that buyers and sellers are pulling in different directions without clear conviction.

NZDUSD is moving in a downtrend channel

Much of this hesitation comes from investors preferring to stay on the sidelines ahead of a major announcement from the Reserve Bank of New Zealand. With the central bank preparing to release its latest monetary policy decision, market participants are reluctant to take large positions in the Kiwi. At the same time, the US Dollar has been retreating slightly against several major currencies, adding another layer of complexity to the NZD’s performance.

Expectations for the RBNZ’s Policy Decision

The Reserve Bank of New Zealand is expected to cut its Official Cash Rate by 25 basis points, bringing it down to 2.25%. While the size of the cut is widely anticipated, investors are far more interested in what the bank plans to do next.

The central question is whether policymakers see a need for additional easing as the country moves into 2026. New Zealand’s economic growth has shown signs of strain, and hints of more rate cuts could signal deeper concerns about the country’s financial outlook. Such a move would likely put extra pressure on the New Zealand Dollar, as investors typically react negatively when a central bank leans toward looser monetary policy.

However, there is also the possibility of what some analysts call a “hawkish cut.” In this scenario, the RBNZ may reduce rates now but firmly suggest that this could be the final adjustment for a while. If Governor Adrian Orr indicates that interest rates have reached their lowest point for the foreseeable future, it could boost confidence in the New Zealand Dollar. Traders often view such comments as a sign that the currency may be undervalued or that economic conditions may soon stabilize.

The US Dollar’s Weakness Adds Another Layer

While the New Zealand Dollar sits in pause mode, the US Dollar is experiencing its own challenges. Comments from Federal Reserve officials have encouraged expectations that the Fed will ease monetary policy further in the coming months. These remarks have fueled growing speculation that the central bank may cut interest rates in December.

Just a month ago, the odds of such a cut were around 40%. Now, market expectations have surged past 80%. With so much anticipation building around upcoming policy shifts, the US Dollar has weakened against several other major currencies. Investors are shifting their focus toward data releases that could provide clearer direction.

Upcoming US Data Could Influence Market Mood

Two important pieces of economic data will be released soon in the United States, both of which could influence how global markets behave. The first is Retail Sales, a key indicator of consumer spending. Economists expect the September report to show slower growth compared to the previous month, but still a positive rise of around 0.4%. That would follow August’s growth of 0.6%.

Consumer spending plays a central role in the US economy. Even small changes in this data can shift expectations around how aggressively the Federal Reserve may act on interest rates. If spending shows strong resilience, the Fed may take a more cautious approach to rate cuts. If it softens significantly, calls for easing could grow louder.

The second major piece of information is the Producer Price Index, which tracks the cost of goods at the wholesale level. Forecasters expect the headline number to increase to 2.7% annual growth in September, up slightly from 2.6% in August. However, the core PPI—which excludes more volatile items—is expected to slip to 2.7% from the prior 2.8%.

These figures matter because inflation remains the key factor shaping central bank decisions worldwide. Any sign that inflation is cooling could encourage the Fed to advance with more supportive monetary policies, further weighing on the US Dollar.

What This Means for the New Zealand Dollar

The New Zealand Dollar is currently caught in a delicate balance between local and global forces. On the domestic front, the RBNZ’s upcoming policy decision carries the potential to shape the currency’s path over the coming months. A signal of further rate cuts could keep the NZD under pressure, while a more confident tone from policymakers might provide a lift.

Globally, the New Zealand Dollar is influenced by the trajectory of the US Dollar. If US inflation data cools and expectations for Fed easing rise even further, the American currency could weaken, indirectly giving the Kiwi some room to breathe. On the other hand, any unexpected strength in US data could limit the NZD’s ability to recover.

Final Summary

The New Zealand Dollar remains under strain as traders wait for clarity from the Reserve Bank of New Zealand’s next policy decision. Expectations of a rate cut are already priced in, but the central bank’s comments about future moves will likely determine the currency’s direction. Meanwhile, the US Dollar is pressured by rising expectations of Fed easing and upcoming economic data that could shift market sentiment yet again. As both countries approach key economic moments, investors continue to navigate an environment marked by uncertainty and anticipation.