EURUSD is moving in a Symmetrical Triangle pattern, and the market has reached the lower high area of the pattern

EURUSD Edges Lower Before Key US Flash PMI Updates Hit the Market

The EUR/USD pair has been moving in a tight range as the week comes to an end, staying just under the 1.1750 level while keeping recent highs within reach. After touching a three-week peak near 1.1768, the pair eased slightly on Friday but still managed to protect most of its earlier gains.

Even with a small pullback, EUR/USD is on track to record its strongest weekly performance since June. That says a lot about what has been driving the market lately—not just economic data, but also shifting global relationships and political headlines that have shaken confidence in the US Dollar.

A Calm Friday Move After a Strong Week for the Euro

By Friday, EUR/USD was trading around the mid-1.17 area, showing moderate losses on the day. Still, the bigger picture remains positive for the Euro this week.

The pair’s ability to stay close to recent highs is especially notable because the latest economic updates from the Eurozone did not provide a major boost. Normally, weaker data could have pushed the Euro lower. Instead, traders seem more focused on what’s happening on the US side, where political developments have weighed heavily on the Dollar.

In short, the Euro hasn’t been winning because it looks incredibly strong. It has been holding up well because the Dollar has struggled to attract buyers.

Eurozone Business Surveys Fail to Impress, But the Euro Stays Steady

The Eurozone’s flash Purchasing Managers’ Index (PMI) readings for January were closely watched, but they didn’t deliver a clear reason for Euro bulls to celebrate.

The Services PMI showed the sector expanding at a steady pace, but it didn’t improve. Meanwhile, the Manufacturing PMI did rise slightly, which sounds encouraging at first, but it still remained below the key 50 mark that separates growth from contraction.

Services Remain Stable

The services sector, often considered a major engine for the Eurozone economy, continued to grow at a modest pace. However, the lack of improvement suggested the region isn’t gaining strong momentum at the start of the year.

Manufacturing Shows Small Progress, Still Not in Growth Mode

Manufacturing activity improved compared to the previous month, but the number remained below 50. That signals the factory sector is still shrinking overall, even if the pace of decline is slowing.

This mix of “not great, but not terrible” data is one reason the Euro didn’t surge higher on its own. Still, EUR/USD remained supported because traders weren’t rushing back into the US Dollar.

Germany Offers a Brighter Spot in the Eurozone Picture

While the broader Eurozone PMI numbers were underwhelming, Germany’s results were more encouraging. German business activity improved more than expected, especially in services.

Germany is the Eurozone’s largest economy, so any signs of stability or improvement there tend to attract attention. Better German data helped reduce worries about the region’s growth outlook, even if the manufacturing sector is still not fully back on its feet.

Stronger Services Activity

Germany’s services PMI increased, pointing to healthier demand and more resilience in areas like consumer spending, business services, and travel-related activity.

Manufacturing Still Struggling, But Improving

Germany’s manufacturing PMI also climbed and beat expectations. Yet, like the broader Eurozone number, it remained below 50—meaning the sector is still contracting, just less sharply than before.

Overall, Germany’s PMI results offered a mild lift to sentiment, but they weren’t strong enough to become the main driver of EUR/USD.

US Dollar Slides as Politics and Global Trust Take Center Stage

The biggest story of the week wasn’t a chart pattern or a surprise interest rate shift. It was the sudden focus on US-European tensions and what that could mean for global confidence in the United States.

Reports and headlines about strained transatlantic relations helped push the US Dollar lower, sending the Dollar Index toward multi-week lows. Investors tend to dislike uncertainty, and when political tensions rise between major partners, markets often respond quickly.

One key topic grabbing attention was the situation involving Greenland and comments made by US President Donald Trump.

Trump stated on social media that he had secured “total and permanent access” to Greenland through an agreement with NATO. The statement came after his appearance at the Davos World Economic Forum, where his tone reportedly softened compared to earlier remarks.

Why These Headlines Matter to Currency Traders

Currencies often reflect trust, stability, and long-term confidence. When markets sense that relationships between major allies are deteriorating, it can create doubts about leadership, cooperation, and global trade stability.

That kind of uncertainty can hurt a currency even when economic data looks fine—and that’s exactly what happened to the US Dollar this week.

US Economic Data Was Solid, But Traders Looked Past It

Under normal conditions, the US economic updates released this week could have helped support the Dollar. Several reports came in at levels that typically signal strength and stability.

But the market response was muted. Investors largely ignored the numbers, keeping their attention on geopolitics and broader risk sentiment.

Here’s what stood out in the latest US data:

US GDP Revised Higher

The US economy’s third-quarter growth rate was revised upward, showing stronger expansion than previously estimated. A stronger growth figure often supports a currency because it suggests the economy is performing well.

Inflation Pressures Remain Present

The Personal Consumption Expenditures (PCE) Price Index, a key inflation measure watched by the Federal Reserve, showed inflation ticking higher compared to the previous month. The core reading, which excludes volatile items, showed a similar trend.

This supports the idea that inflation hasn’t fully cooled, which can strengthen the argument for keeping interest rates steady rather than cutting quickly.

Jobless Claims Still Low

Weekly jobless claims rose slightly but remained lower than expected, pointing to continued resilience in the labor market.

Taken together, these data points align with the Federal Reserve’s preference to stay cautious. They support the view that the central bank can afford to keep interest rates steady for now.

But despite the supportive backdrop, the Dollar didn’t benefit much—showing how powerful political risk can be when it dominates the narrative.

Traders Shift Focus to US S&P Global PMIs

As the week ends, attention turns toward the next major set of business activity readings from the United States: the S&P Global preliminary PMIs.

These reports matter because they offer a snapshot of how US companies are performing in both services and manufacturing. If the numbers show stronger momentum, they can help restore confidence in the Dollar—at least temporarily.

What Markets Expect

The services PMI is expected to edge higher compared to the previous month. While that’s not a dramatic change, even small improvements can shape market mood, especially when traders are looking for reasons to reassess the Dollar’s weakness.

Why EUR/USD May Stay Sensitive to Headlines

Right now, EUR/USD is being pulled by two competing forces:

-

The Eurozone outlook is steady but not exciting

-

The US Dollar is struggling under the weight of political tension and shifting sentiment

That combination keeps EUR/USD supported near recent highs, even when European data doesn’t shine.

At the same time, the pair is unlikely to move in a straight line. Traders are reacting quickly to any updates about US-EU relations, global trade risks, and comments from political leaders.

If tensions ease further, the Dollar could stabilize. If they flare up again, the Euro may remain well-supported even without major improvements in Eurozone growth data.

Summary: A Strong Week for EUR/USD Driven by More Than Data

EUR/USD remains close to multi-week highs as the market wraps up a volatile week. Eurozone PMI numbers were mixed and didn’t provide strong support, though Germany showed some improvement. On the US side, economic data was generally positive, but it failed to lift the Dollar as traders focused instead on political tensions between the US and Europe. With more US business activity data ahead, the pair is likely to stay sensitive to both headlines and shifting market confidence.

GBPUSD Pushes Up as UK Economic Reports Spark Fresh Pound Demand

The Pound Sterling has started to look much stronger again, especially against the US Dollar. In the latest trading sessions, the British currency moved higher after the UK released a set of economic updates that surprised many investors in a positive way. Two key reports stood out: UK Retail Sales for December and the flash S&P Global Purchasing Managers’ Index (PMI) readings for January.

GBPUSD is moving in a descending channel, and the market has reached the lower high area of the channel

Together, these numbers suggest the UK economy may be holding up better than expected. That matters because when growth looks healthier, markets often scale back expectations for quick interest rate cuts. And when rate cut bets drop, the currency often gets a boost.

At the same time, the US Dollar is not showing the same strength. While it has not collapsed, it has struggled to find steady support as investors weigh global political tensions, shifting trade relationships, and what the Federal Reserve might do next.

Strong UK Data Helps the Pound Stand Out

The Pound rose sharply against several major currencies, with GBP/USD climbing toward the 1.35 area. That move came as traders reacted to upbeat UK business activity data and a clear improvement in consumer spending.

Both reports point to something important: demand inside the UK is still alive. Businesses are seeing more activity, and shoppers are spending again after a weak period. For a currency like the Pound, that combination is often a positive sign because it supports growth expectations and can influence how the Bank of England approaches interest rates.

UK PMI Report Shows Faster Business Growth

The flash PMI data for January delivered a stronger message than many expected. The overall business output number moved higher, showing that the UK economy may be starting the year with better momentum.

The Composite PMI, which combines both manufacturing and services, jumped to 53.9 in January, up from 51.4 in December. It also beat market expectations, which were much lower. A number above 50 signals expansion, so this rise suggests the UK economy is growing at a faster pace than it was late last year.

Services Sector Leads the Way

The services side of the economy was especially strong. Services matter a lot for the UK because they make up a large share of overall economic activity.

The Services PMI came in at 54.3, higher than the previous reading and well above what markets expected. This tells investors that businesses like retailers, restaurants, transport firms, and other service providers are seeing improved demand.

Manufacturing Also Shows Improvement

Manufacturing was another bright spot. The Manufacturing PMI rose to 51.6, up from 50.6. While manufacturing is smaller than services in the UK economy, it still plays an important role, especially when it comes to exports, business confidence, and job creation.

This rise is meaningful because it shows the factory side of the economy is not falling behind. Instead, it appears to be gaining traction at the same time as services.

Retail Sales Return to Growth and Surprise the Market

Alongside the PMI data, UK Retail Sales offered another positive surprise. After shrinking for two months in a row, consumer spending bounced back in December.

The Office for National Statistics reported that Retail Sales rose 0.4% month-on-month. That might not sound huge at first glance, but it was much better than expected. Markets had forecast a small decline instead.

This matters because consumer spending is one of the biggest drivers of economic growth. When people spend more, businesses earn more, hiring can improve, and overall confidence tends to rise.

Annual Retail Sales Growth Looks Even Better

Even more impressive was the yearly number. Retail Sales grew 2.5% year-on-year, beating expectations by a wide margin. It was also stronger than the previous month’s reading, which had already been revised higher.

This kind of growth suggests that households are still willing and able to spend, even after a period of pressure from higher interest rates and the cost of living.

What This Means for the Bank of England

When UK data comes in strong, it often changes how investors think about interest rates. If the economy is holding up well, the Bank of England has less pressure to cut rates quickly.

That’s important because rate cuts usually reduce a currency’s appeal. Lower rates can mean lower returns for investors holding assets in that currency. So when traders believe the Bank of England might stay cautious and avoid rushing into cuts, the Pound tends to benefit.

Right now, stronger Retail Sales and improved business activity could reduce the market’s confidence that rate cuts are coming soon. It doesn’t mean cuts are off the table, but it does suggest the central bank may take more time before making big moves.

A Quiet UK Data Calendar Could Keep Focus on BoE Expectations

Looking ahead, the UK economic calendar is expected to be relatively light next week. That means there may not be many major UK reports to reshape the narrative in the short term.

Because of that, market attention may shift toward expectations for the Bank of England’s next policy meeting in February. Without a steady flow of new data, traders often rely more heavily on broader sentiment, central bank signals, and how global events affect risk appetite.

The US Dollar Struggles to Build Strength

While the Pound has been gaining support from better UK data, the US Dollar has not been enjoying the same kind of momentum. Even though the Dollar has shown small moves higher at times, it has generally stayed under pressure.

The US Dollar Index, which measures the Greenback against a basket of major currencies, has been hovering near recent lows. That suggests traders are not fully confident about the Dollar’s direction, especially with global headlines creating uncertainty.

Trade and Political Tensions Add Pressure to the Dollar

One reason the Dollar has looked less stable is growing caution around the United States’ long-term trade relationships. Investors have been watching how Washington interacts with major global partners, especially after tariff-related moves aimed at addressing trade imbalances.

When trade relations become unpredictable, markets can become nervous. That nervousness can impact currency flows, especially if investors worry about global growth or sudden shifts in policy.

At the same time, global geopolitical issues remain a factor. Relations between major powers can influence market confidence, and uncertainty often pushes traders to rethink their positions in major currencies.

Federal Reserve Decision Is the Next Big Event

The biggest near-term driver for the GBP/USD pair may be the Federal Reserve’s next interest rate decision. Investors are waiting for the Fed’s policy announcement next Wednesday.

Right now, the expectation is that the Fed will keep interest rates unchanged. Markets are widely pricing in a steady decision, meaning no hike and no cut at this meeting.

Even if the Fed holds rates, the tone of its messaging will matter. Traders will pay close attention to how policymakers describe inflation, the job market, and the broader economy. Any hint about future rate moves could quickly shift the Dollar’s direction.

Why the Fed Matters for GBP/USD

GBP/USD is shaped by the story on both sides of the Atlantic. If UK data stays strong and the Bank of England looks less eager to cut rates, the Pound can remain supported.

But if the Federal Reserve signals that US rates will stay high for longer, the Dollar could regain strength. That could limit the Pound’s upside or even push GBP/USD lower again.

In other words, the pair is being pulled by two major forces:

-

The UK’s improving economic signals and shifting BoE expectations

-

The US Dollar’s response to global uncertainty and Fed policy guidance

What Traders May Watch Next

In the coming days, investors are likely to keep a close eye on a few key themes that could shape the Pound’s performance:

UK Economic Momentum

If future reports confirm that the UK economy is strengthening, it could support the Pound further and reduce pressure on the Bank of England to cut rates quickly.

Central Bank Expectations

Even without major UK data releases, traders will watch how expectations evolve for the BoE and the Fed. Currency markets often move based on what investors think will happen next, not just what is happening now.

Global Headlines and Risk Mood

Trade disputes and geopolitical tensions can quickly change market sentiment. If uncertainty rises, currencies can move sharply as investors shift toward or away from risk.

Summary: Pound Supported by Better UK Growth Signals and Steady Fed Outlook

The Pound Sterling has moved higher after the UK delivered stronger-than-expected Retail Sales and flash PMI figures. The data suggests the economy may be gaining momentum, with services and manufacturing both expanding and consumer spending returning to growth.

These positive signals could reduce near-term expectations for Bank of England rate cuts, giving the Pound extra support. Meanwhile, the US Dollar remains under pressure as investors weigh global trade concerns and wait for the Federal Reserve’s next policy decision, which is expected to keep rates unchanged.

With UK data light next week, attention may shift toward central bank expectations and global developments, both of which could shape the next move for GBP/USD.

USDJPY Retreats to 158.00 as Markets Buzz Over Japan’s Next Move

The USD/JPY pair is trading close to the 158.00 area after giving back earlier gains, as traders digest a sharp and unexpected swing in the Japanese Yen. The move came after the US Dollar briefly pushed higher during the session, only to reverse direction quickly. By the time markets settled, the Dollar was still down on the day, and the Yen was back in the spotlight.

USDJPY is moving in an uptrend channel, and the market has reached a higher low area of the channel

What made the session especially interesting was the speed of the shift. There was no single major headline that clearly explained the size of the Yen’s sudden jump and pullback. Instead, the market reaction appeared to be driven by a mix of central bank messaging, growing speculation about official action from Japan, and broader weakness in the US Dollar.

This kind of rapid back-and-forth price movement is sometimes described as a “whipsaw,” and that’s exactly what many traders experienced. It was the type of volatility that can catch both buyers and sellers off guard, especially when it happens without an obvious trigger.

A Fast Reversal Leaves USD/JPY Near 158.00

Earlier in the day, the US Dollar moved higher against the Yen and climbed above 159.20. But the strength didn’t last long. Momentum shifted quickly, and the pair dropped back toward 158.00, where it has been hovering as markets reassess the situation.

Moves like this often reflect uncertainty. When traders are confident about a trend, price action tends to look smoother. But when the market is unsure—especially around central bank decisions or potential government involvement—price can swing sharply as positions are adjusted in real time.

In this case, the Yen’s sudden movement raised eyebrows because it seemed to happen without a clear economic report or major breaking news at that exact moment. That has fueled speculation that something may have happened behind the scenes.

Speculation Grows Around a Possible “Rate Check” in Japan

One of the biggest talking points from Friday’s trading has been growing chatter about a possible “rate check” by Japanese authorities.

A rate check is not the same thing as direct currency intervention, but it can be a warning sign that officials are paying close attention to market moves. It usually involves calls from authorities in Tokyo to major commercial banks, asking for quotes on the Yen. Traders watch this closely because it can sometimes happen shortly before Japan steps in more forcefully to influence the currency market.

Why a Rate Check Matters to Traders

Even though a rate check is technically just an information-gathering step, the market often reacts strongly because it suggests Japan may be preparing to act. Traders know that when authorities become uncomfortable with the pace of Yen weakness, they may choose to respond quickly.

That possibility alone can trigger sudden shifts in positioning. Investors who were betting on further Yen weakness may rush to reduce exposure, while others may take the opportunity to buy the Yen in anticipation of possible official support.

The result can be exactly what markets saw on Friday: sharp moves, sudden reversals, and a sense that the Yen is being watched more closely than usual.

Bank of Japan Keeps Rates Steady, as Expected

Before the volatility picked up, the Japanese Yen had already been weakening more broadly. That earlier softness followed the Bank of Japan’s decision to keep interest rates unchanged at 0.75%, a move that markets largely expected.

When a central bank holds rates steady, the market reaction depends heavily on what traders were expecting going in. If the decision matches forecasts, attention immediately shifts to the language and tone of the central bank’s message.

In Japan’s case, many investors are still trying to understand how quickly the Bank of Japan may continue tightening policy in the future. That uncertainty keeps the Yen sensitive to any hint of what could come next.

Governor Ueda Sends a Cautious but Slightly Hawkish Message

Bank of Japan Governor Kazuho Ueda delivered comments that many interpreted as moderately hawkish, even though the bank did not change rates at this meeting.

Ueda noted that inflation is moving closer to the BOJ’s 2% target, which could support further tightening over the medium term. That matters because Japan has spent years fighting low inflation, and reaching the target in a stable way could change how the central bank approaches interest rates going forward.

At the same time, Ueda also emphasized caution. He said the BOJ needs to fully understand the impact of previous rate hikes before deciding to tighten again. That suggests the bank is not in a rush, even if inflation trends are moving in the right direction.

This combination—acknowledging progress on inflation while still urging patience—creates a tricky message for markets. Traders are left balancing two ideas at once:

-

The BOJ may still raise rates again later on

-

But the timing may depend on how the economy responds to what has already been done

That uncertainty can keep the Yen unstable, especially when the market is already nervous about potential government action.

The US Dollar Struggles Under Political and Economic Pressure

While Japan’s side of the story grabbed most of the attention, the US Dollar has also been dealing with its own problems.

The US Dollar Index is on track for its worst weekly performance since June, weighed down by concerns linked to rising tensions between the United States and the European Union. Reports of friction connected to Greenland have added to the uneasy mood, and markets generally don’t like political uncertainty—especially when it risks turning into a broader diplomatic dispute.

When investors feel uncertain about international relations, they often reduce risk or shift capital into assets they believe may be more stable. That kind of shift can weaken the Dollar, even when US economic data looks solid.

Strong US GDP and Inflation Data Didn’t Help the Dollar Much

On Thursday, the United States released strong GDP figures along with inflation numbers that remained stubborn. Under normal circumstances, data like that could support the Dollar because it suggests the economy is holding up and inflation pressures remain.

But this time, the Dollar didn’t gain much from it.

That’s a reminder that currency markets don’t move based on data alone. The US Dollar can still struggle if traders believe political tensions, global uncertainty, or changing expectations about future policy will outweigh economic strength.

It also shows how market focus can shift quickly. Even solid economic performance may not be enough to lift the Dollar if investors are worried about the bigger picture.

All Eyes Turn to US Flash PMI Data

As Friday continues, traders are paying close attention to the upcoming US Flash PMI reports. These surveys provide an early look at business activity and can influence expectations about economic momentum.

Markets are currently expecting a moderate improvement, which could offer the Dollar some short-term support if the numbers surprise to the upside. However, if the data disappoints, it may reinforce the idea that the Dollar is losing strength at a time when political concerns are already weighing on sentiment.

For USD/JPY, this matters because the pair is being pulled in two directions:

-

The Yen is sensitive to possible official action and BOJ policy expectations

-

The Dollar is reacting to political headlines and shifting confidence in US momentum

When both currencies are being influenced by major themes at the same time, volatility can rise quickly.

What This Means for USD/JPY Traders and Market Watchers

The current situation around USD/JPY is a clear example of how fast currency markets can change when uncertainty is high.

On one side, Japan is dealing with renewed attention on its currency and questions about whether authorities may step in if moves become too extreme. On the other side, the US Dollar is facing pressure from international tensions and a market mood that has become less supportive, even with solid economic data.

For traders, it’s a reminder that sudden swings can happen even without a clear headline, especially when the market is already on edge. For long-term watchers, it highlights how the Yen remains highly sensitive to both central bank signals and any hint of government involvement.

Summary

USD/JPY has drifted near 158.00 after a sharp reversal from earlier highs, as the Japanese Yen saw sudden and unusual volatility. Speculation about a possible rate check by Japanese authorities added fuel to the move, while the Bank of Japan kept rates steady and delivered a message that sounded cautious but slightly hawkish. At the same time, the US Dollar remains under pressure, weighed down by US-EU tensions and a weak weekly performance despite strong US economic data. With US Flash PMI reports in focus, traders are watching closely for the next catalyst that could shape the pair’s direction.

BTCUSD Downtrend Still Intact While the Recent Upswing Loses Strength

Bitcoin has been moving in a softer direction since October 2025, and that shift has changed the mood across the crypto market. After months of strong momentum, the price action started to lose strength, and what followed looks like a clear change in trend.

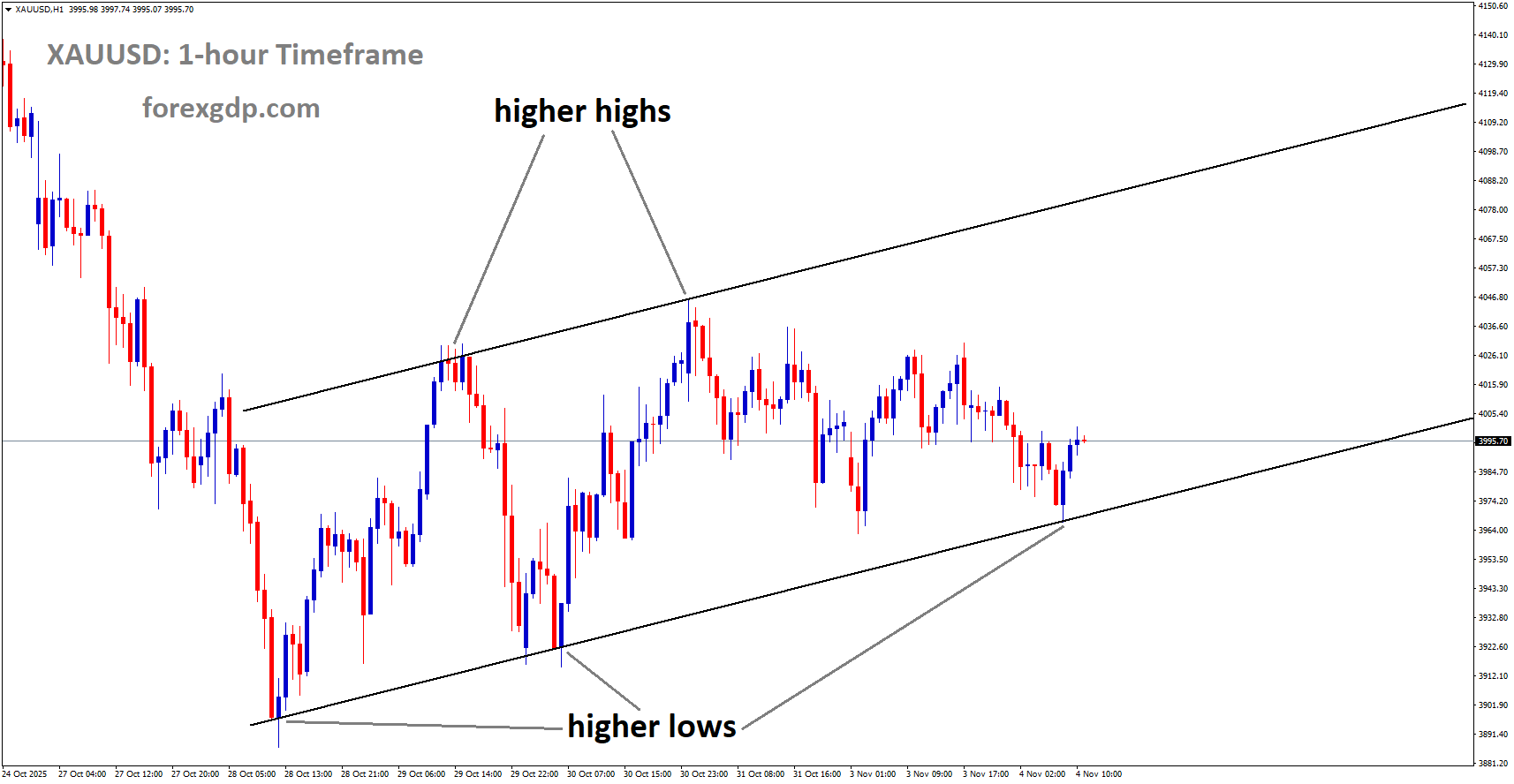

BTCUSD is moving in an Ascending channel, and the market has reached the higher low area of the channel

Instead of continuing to climb, Bitcoin began forming a pattern that many traders and long-term observers recognize as a sign of weakness: each rebound has struggled to reach a new high, and each drop has pushed into fresh lows. When this happens consistently, it usually suggests that sellers are still in control.

This doesn’t mean Bitcoin is “done” forever or that crypto is going away. It simply means the market may be going through one of its natural cooling phases—something Bitcoin has experienced many times before. The bigger question now is how deep this phase could go, and what kind of behavior might signal that a real bottom is finally forming.

A Shift in Momentum After the October Peak

The key turning point appears to have happened in October 2025. That period marked what many believe was the late stage of a larger bull cycle. In long market cycles, it’s common to see strong rallies near the end, followed by a noticeable reversal once buyers begin to run out of energy.

Since then, Bitcoin has been moving in a way that suggests the trend is still leaning bearish. Instead of sharp back-and-forth swings that overlap heavily, the movement has been cleaner and more directional. In many cases, a market that continues to trend without major overlap is showing that one side—buyers or sellers—is still firmly in charge.

Right now, the structure points toward continued weakness rather than a stable recovery.

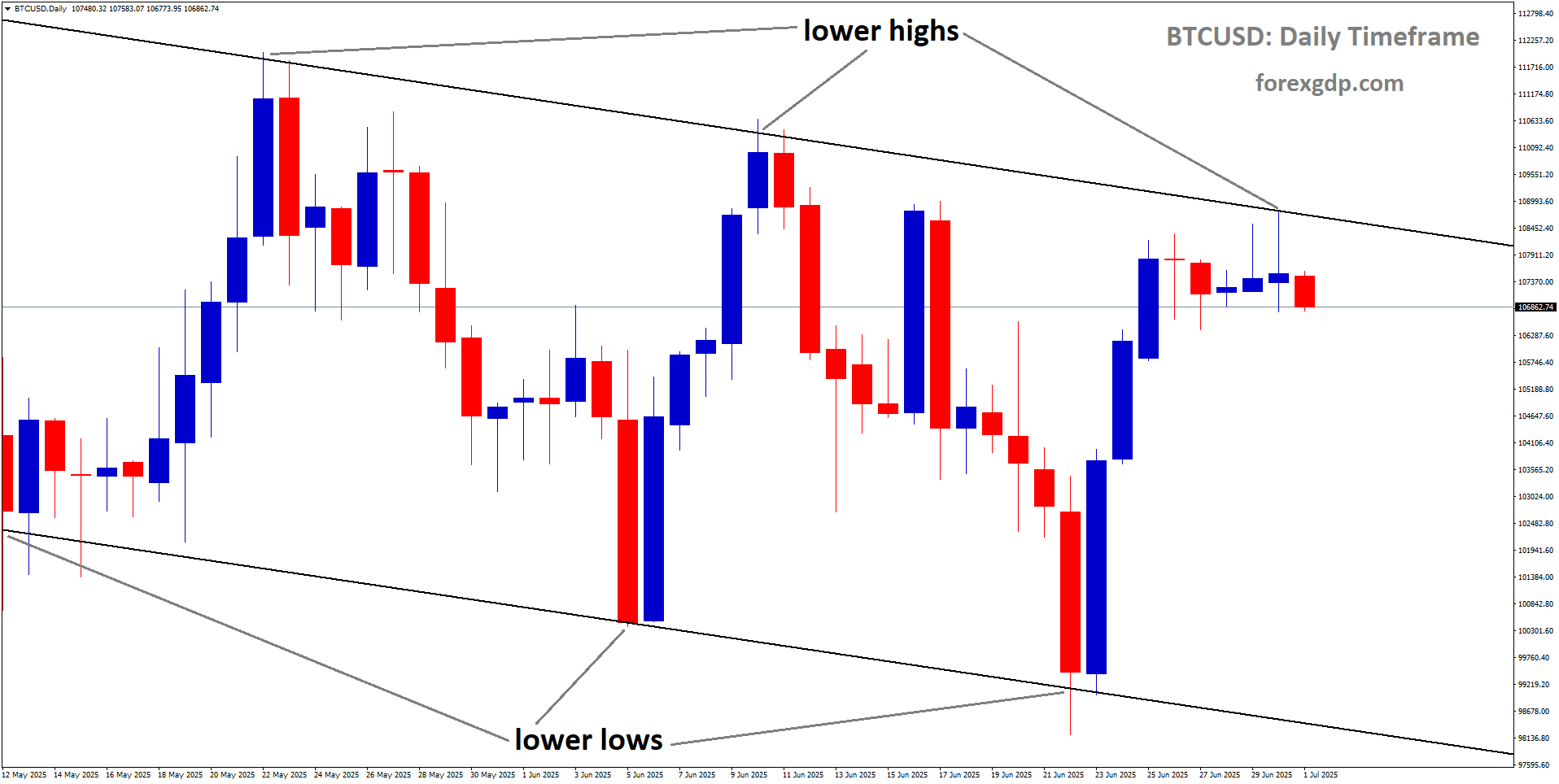

Lower Highs and Lower Lows: A Classic Bearish Setup

One of the most important things happening in this cycle is the formation of lower highs and lower swing lows.

That might sound simple, but it’s one of the clearest signs that the market is not yet ready to move back into a strong uptrend. Each time Bitcoin tries to recover, it runs into selling pressure sooner than before. And when it drops again, it breaks below the previous low instead of finding strong support.

This type of steady decline often reflects a market that is slowly unwinding optimism. It’s not always a dramatic crash. Sometimes it’s a grinding move lower that slowly wears people down.

And in crypto, those slow declines can be just as emotionally difficult as sudden drops—because they keep hope alive while still draining confidence over time.

Why the November Bounce May Not Have Been Enough

After Bitcoin hit its November lows, there was a recovery attempt. That bounce brought some relief, and it likely encouraged many people to believe the worst was over.

But there’s a detail that stands out: the recovery unfolded in what looked like only three waves of movement.

In wave-based market theories, a strong recovery that signals a trend change often develops in a more complete structure. A three-wave rise, on the other hand, is frequently seen as corrective. That means the market is not starting a new bullish phase—it’s simply taking a break before continuing the broader downtrend.

This kind of rebound can feel convincing in the moment. It can bring positive headlines, renewed social media excitement, and even a wave of new buyers stepping in. But if it’s only a temporary correction, it may end up setting the stage for another push lower.

The Area Where Corrections Often End

The recovery from the November lows appears to have stalled in a zone that is commonly associated with countertrend moves ending.

In many market cycles, corrections often stop around a mid-range recovery area rather than fully reversing the decline. This zone tends to attract sellers who missed earlier opportunities, along with traders who see the bounce as a chance to exit positions at a better price.

When Bitcoin fails to push past this kind of recovery range, it can signal that the downtrend is still the main story.

At that point, the market may be preparing for another leg lower—especially if buyers begin to lose confidence again.

What Would Confirm Another Drop?

A major signal for trend continuation would be a clear break out of the recovery structure.

When markets recover inside a controlled channel or range, they can appear stable even while remaining weak. The real confirmation comes when that structure breaks and the market starts slipping again.

If Bitcoin breaks down from that corrective move, it could open the door for further weakness over the next several weeks. That would likely bring a fresh wave of fear into the market, especially among traders who bought during the rebound expecting a bigger recovery.

Why this matters psychologically

This kind of move often creates a frustrating trap:

-

Early sellers feel “right” again

-

Recent buyers feel stuck

-

Long-term holders start questioning their patience

-

New investors begin to panic

And once panic grows, markets can drop faster than people expect.

Long-Term Holders Still Haven’t Felt Maximum Pain

One interesting detail in this cycle is how long-term Bitcoin holders are behaving.

In past major market lows—such as those seen around 2012, 2015, 2019, and even 2022—long-term holders reached a point where many were sitting on heavy losses. That kind of pain often forces people to sell, even if they originally planned to hold for years.

But in the current cycle, long-term holders are not showing the same level of stress yet.

That suggests something important: there may still be a large group of holders who are not truly worried about downside risk. Many might still feel confident that Bitcoin will bounce back quickly, or that any dip is just another buying opportunity.

And when too many people remain comfortable, markets sometimes have a way of pushing further down until that confidence breaks.

If Bitcoin Drops Again, Liquidations Could Increase

If Bitcoin sees another strong move lower, it could trigger more forced selling.

In crypto markets, liquidations happen when traders use leverage and the price moves against them. When the market falls quickly, leveraged positions can be wiped out, creating even more selling pressure.

This can lead to a chain reaction:

-

Price drops

-

Liquidations kick in

-

More selling hits the market

-

Price drops further

-

Panic spreads

This kind of event doesn’t just impact traders. It often shakes the entire market, including altcoins, crypto-related stocks, and sentiment across the industry.

Extreme Pessimism Can Be a Sign a Bottom Is Near

Here’s the strange part about crypto cycles: the worst emotional moments often come close to major turning points.

When pessimism reaches an extreme level, it can mean the market is nearing exhaustion on the downside. That’s because most of the people who were going to sell have already sold, and fewer sellers remain.

In wave-based thinking, this is often associated with the final stage of a decline—sometimes called the “last push down.” It’s the phase where the market tries one more time to break confidence completely.

This is also the phase where meaningful bottoms often form.

Not because the news improves or because everyone suddenly becomes optimistic—but because the selling pressure finally runs out.

What it can look like in real life

A final downside phase often comes with:

-

Very negative headlines

-

Traders calling for endless downside

-

People giving up on the idea of a recovery

-

Low excitement and low participation

Ironically, that’s often when long-term opportunities begin to quietly return.

What Investors and Traders Should Watch Next

Bitcoin’s current behavior suggests the downtrend may not be finished. The recovery attempt from November appears more like a pause than a full reversal, and long-term holders haven’t experienced the kind of deep pain that often appears near major cycle lows.

That doesn’t guarantee a major collapse, but it does mean the market may still need to “clear out” remaining optimism before a durable bottom forms.

For traders, the coming days and weeks could be important. If Bitcoin breaks down from its recovery structure, the next move may be sharper and more emotional than the slow decline that came before.

For long-term investors, this may be a time to stay patient and realistic. Crypto cycles tend to punish impatience, and they often test conviction before rewarding it.

Final Summary

Bitcoin has been trending lower since October 2025, showing a consistent pattern of lower highs and lower lows that still favors a bearish outlook. The rebound from the November lows appears corrective rather than a strong reversal, which may increase the risk of another leg down. At the same time, long-term holders have not reached the deep loss levels seen in past major cycle bottoms, suggesting that the market may still need a stronger wave of fear and forced selling before a lasting bottom can form.

ETHUSD: Ethereum Activity Jump After Fusaka Might Not Last, JPMorgan Reports

Ethereum has been busy lately. After the Fusaka upgrade launched last December, the network saw a sharp rise in transactions and active addresses. At the same time, fees on Ethereum dropped to some of the lowest levels seen in a long time. For many crypto watchers, this combination looks like a win: more usage, lower costs, and a network that feels more alive.

ETHUSD is moving in an Ascending Triangle, and the market has reached the higher low area of the pattern

But according to a new note from JPMorgan analysts led by Nikolaos Panigirtzoglou, the recent burst of activity may not be a long-lasting trend. The bank’s message is simple: Ethereum upgrades often create short-term excitement, but history shows that network growth tends to cool down after the initial rush.

That doesn’t mean Ethereum is failing. It means the ecosystem is changing fast, and the way value flows through Ethereum today is very different from how it worked in earlier years.

Ethereum’s Fusaka Upgrade Boosted Activity, but Fees Fell Hard

Ethereum’s Fusaka upgrade introduced changes that made the network better at handling more activity, especially for Layer 2 systems. In the weeks after the upgrade went live, usage started climbing.

Recent data shows that weekly active addresses and daily transactions reached record highs after steadily increasing over the past month. Some people have welcomed this as proof that Ethereum is still growing and attracting users.

However, there’s also debate about what is really driving these numbers. Some critics suggest the spike may be partly influenced by things like address poisoning and other behavior that can inflate activity metrics without representing real user growth.

Even so, the bigger story is what happened alongside the growth: Ethereum fees dropped sharply. While low fees can be great for users, they also reduce the amount of revenue Ethereum captures on its main network, also known as Layer 1.

Why JPMorgan Thinks Ethereum Struggles to Keep Long-Term Growth

JPMorgan’s analysts say Ethereum has seen this pattern before. Major upgrades often lead to a surge in activity, but the boost tends to fade as the market adjusts and users spread out across different platforms.

The bank points to several reasons why Ethereum has struggled to turn upgrade-driven excitement into lasting, sustained growth.

Layer 2 Networks Are Pulling Activity Away From Ethereum’s Main Chain

One of the biggest shifts in Ethereum’s world today is the rise of Layer 2 networks. These are systems built on top of Ethereum that help process transactions faster and at a lower cost.

Fusaka introduced improvements designed to help Layer 2 networks scale even more. Features such as Peer Data Availability Sampling (PeerDAS), higher gas limits, and expanded blobspace made it easier for Layer 2 networks to handle more throughput.

That sounds like a positive development, and in many ways it is. But JPMorgan argues that there’s a tradeoff: as Layer 2 networks grow, they take more activity away from Ethereum’s Layer 1.

In simple terms, more users may still be “in the Ethereum ecosystem,” but fewer of their transactions are happening directly on the main chain where the base layer collects the most fees.

Competitive Blockchains Are Taking Market Share

Ethereum is no longer the only major destination for developers and users. JPMorgan notes that rival blockchains have been capturing meaningful market share, with Solana mentioned as a strong example.

Competing networks often focus on high throughput and low fees, which can be attractive for everyday users and app builders. When people can get faster and cheaper transactions elsewhere, they may not feel as tied to Ethereum as they once did.

This is one of the biggest changes in crypto over the last few years. Ethereum used to be the default place for many new apps. Now, the ecosystem is more competitive, and users have more choices than ever.

Speculative Trends Aren’t Driving Ethereum Like They Used To

In previous crypto cycles, Ethereum benefited from huge waves of speculative activity. Things like memecoins, NFTs, and ICOs brought massive attention, trading volume, and network usage.

JPMorgan says that kind of activity has either cooled down or moved elsewhere. The excitement that once fueled constant Ethereum traffic isn’t as strong today, and many speculative communities have migrated to other chains that offer cheaper and faster transactions.

This matters because Ethereum’s network activity has historically been closely tied to speculation cycles. When hype slows down, usage often follows.

The Rise of App-Specific Chains Is Fragmenting Liquidity

Another major point from JPMorgan is that crypto activity is no longer concentrated in one place. Instead, liquidity and users are being spread across more specialized environments.

App-specific chains are designed to support one platform or one type of application. They can offer more control, custom features, and sometimes better performance.

JPMorgan highlights this fragmentation as a key reason Ethereum has been capturing fewer fees. When apps and liquidity move to separate chains, Ethereum’s Layer 1 becomes less central to day-to-day activity.

Examples of Major Platforms Shifting the Landscape

The analysts pointed to examples such as Uniswap and dYdX, which represent important parts of the decentralized finance world.

Uniswap has historically been a major contributor to Ethereum network usage and ETH burn. But as liquidity spreads across different networks and scaling solutions, Ethereum’s base layer may not benefit as much as it once did.

The bigger picture is that Ethereum is still powering a huge ecosystem, but the economic value is being shared across many layers and chains rather than flowing into Layer 1 alone.

Lower Fees Mean Less ETH Burn, Which Changes Supply Dynamics

Ethereum’s fee model has an important feature: part of the transaction fees can be burned, meaning removed from circulation. This has been one of the key reasons many investors have viewed ETH as having strong long-term potential.

But when fees drop, the amount of ETH being burned also drops.

JPMorgan explains that because Ethereum is now capturing fewer fees on Layer 1, there is less burning happening. This can increase the circulating supply over time, which may create downward pressure on ETH’s price.

This doesn’t automatically mean ETH will fall. It simply means the supply-and-demand balance may not be as supportive as it was during periods when Ethereum was collecting high fees and burning large amounts of ETH.

Ethereum Still Has a Big Opportunity in Tokenization

While JPMorgan focuses on the challenges of maintaining long-term network activity, not everyone is pessimistic about Ethereum’s future.

BlackRock, one of the world’s largest asset managers, highlighted in its 2026 thematic outlook that Ethereum could be well-positioned to benefit from the growth of tokenized assets.

Tokenization is the process of putting real-world assets onto blockchain rails. This could include things like funds, bonds, real estate exposure, and other financial instruments that become easier to trade, settle, or manage through blockchain technology.

BlackRock pointed out that Ethereum currently holds a strong position in this sector, with an estimated 65% market share of tokenized assets. That’s a major lead, and it suggests Ethereum still plays a central role in where serious institutional blockchain activity is heading.

What This Means for Ethereum’s Next Phase

Ethereum’s recent activity spike after the Fusaka upgrade shows the network is still capable of scaling and attracting attention. But JPMorgan’s view is that upgrades alone may not be enough to create long-term growth on Layer 1, especially as crypto becomes more fragmented.

Ethereum’s challenge today isn’t survival. It’s value capture.

Layer 2 networks, app-specific chains, and rival blockchains are all growing quickly. Many of them still rely on Ethereum or connect back to it in some way, but they don’t always feed the same level of fees and revenue into Ethereum’s base layer.

At the same time, Ethereum continues to hold a powerful position in areas that matter for long-term adoption, including tokenization and institutional use cases. That could become a major driver of future demand, especially if more real-world financial products move onto blockchain infrastructure.

Summary: Ethereum Is Growing, but the Ecosystem Is Shifting

Ethereum has seen a fresh burst of network activity after the Fusaka upgrade, with transactions and active addresses climbing while fees fell to new lows. JPMorgan believes this kind of post-upgrade surge often fades over time, and it points to several reasons why sustained growth has been difficult.

Layer 2 networks are expanding rapidly and pulling activity away from Ethereum’s main chain. Competitive blockchains are attracting users with faster and cheaper experiences. Speculative trends like NFTs and memecoins no longer drive Ethereum usage the way they once did, and liquidity is spreading across app-specific chains.

As Ethereum captures fewer fees, ETH burn slows down, which can affect supply dynamics. Still, Ethereum remains a leader in tokenization, and major institutions like BlackRock see it as well-positioned for the next wave of blockchain adoption.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!