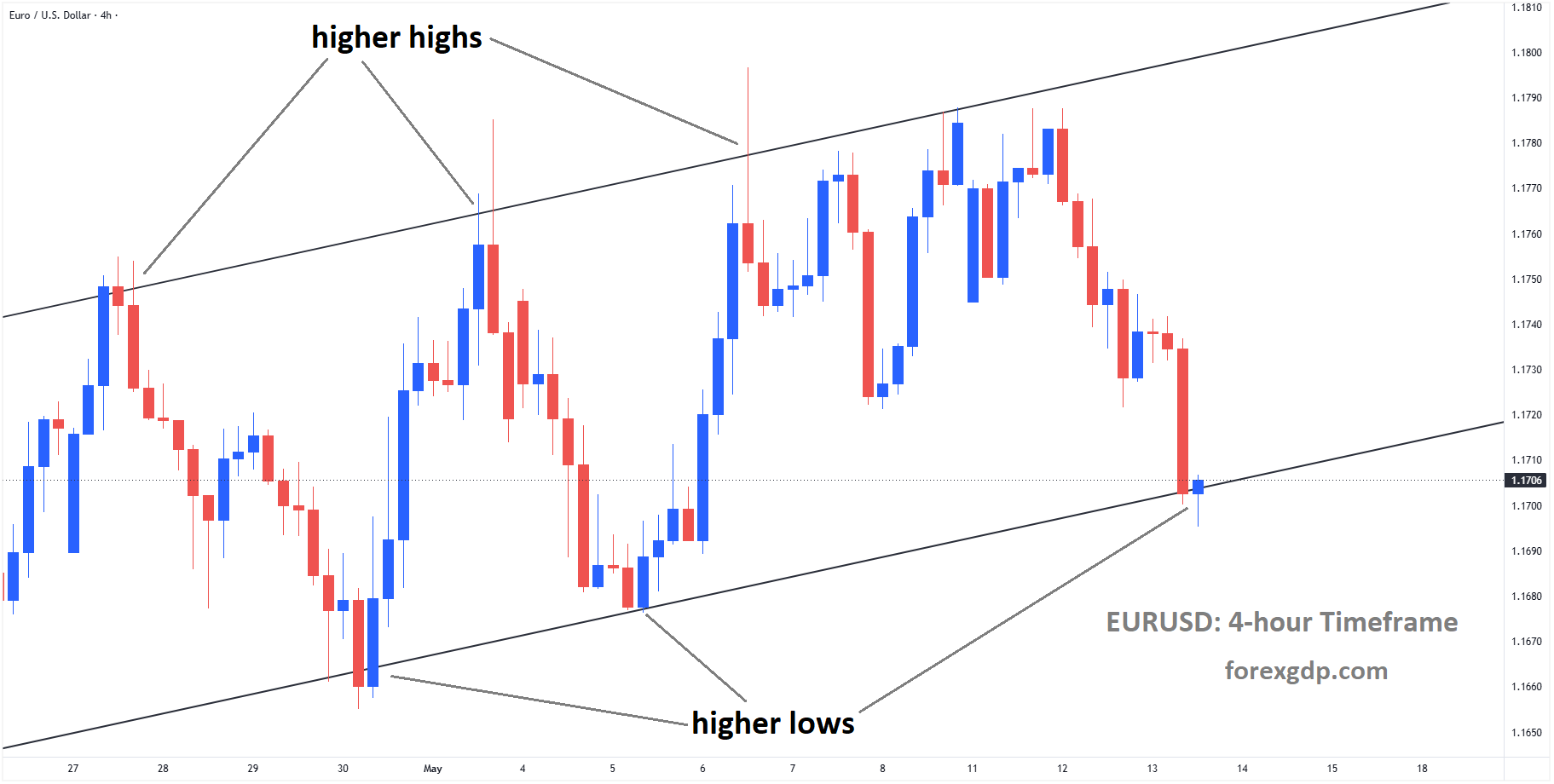

EURUSD reached a higher low area of the ascending channel

EURUSD Under Pressure While Weak European Data Boosts Dollar Strength

The EUR/USD currency pair continued to move lower on Wednesday, slipping below the 1.1700 level after failing to hold gains near 1.1790 earlier in the week. The decline reflects growing pressure on the Euro as fresh economic data from the Eurozone painted a weaker picture of regional growth and industrial activity.

At the same time, the US Dollar remained strong after recent inflation data from the United States reduced expectations that the Federal Reserve could lower interest rates anytime soon. Global uncertainty and ongoing geopolitical tensions also continued to support demand for the safe-haven Dollar.

Euro Struggles After Weak Economic Reports

The Euro came under renewed selling pressure after the latest Eurozone economic figures failed to impress investors. One of the key reports released was the updated Gross Domestic Product (GDP) data for the region.

According to the latest estimate, the Eurozone economy grew by only 0.1% during the first quarter of the year. While the figure confirmed earlier expectations, it still highlighted the slow pace of economic recovery across the region. On a yearly basis, economic growth slowed to 0.8%, compared to 1.2% recorded during the previous quarter.

The numbers reinforced concerns that the Eurozone economy is losing momentum. Many businesses and consumers across Europe continue to face pressure from high borrowing costs, weak demand, and slower industrial activity.

Industrial Production Adds to Market Concerns

Another major factor behind the Euro’s weakness was disappointing Industrial Production data from the Eurozone.

Factory output in March increased by only 0.2%, falling short of market expectations for a 0.3% rise. In addition, February’s production figures were revised lower, showing weaker performance than previously reported.

The yearly data was even more concerning. Industrial Production contracted by 2.1% compared to the same period last year, showing a much sharper decline than February’s 0.8% drop.

These figures suggest that Europe’s manufacturing sector continues to struggle with lower demand and ongoing economic uncertainty. Industries across the region have faced challenges linked to slower global trade, higher energy costs, and weaker consumer spending.

Strong US Inflation Supports the Dollar

While the Euro faced pressure from weak domestic data, the US Dollar gained strength from stronger-than-expected inflation numbers released earlier this week.

The latest Consumer Price Index (CPI) report showed inflation rising to its highest yearly level in nearly three years. The data surprised markets and immediately changed expectations surrounding future Federal Reserve policy decisions.

Before the inflation report, some investors believed the Fed could begin cutting interest rates later this year. However, stronger inflation has made that possibility less likely in the near term.

As expectations for rate cuts faded, US Treasury yields moved higher. Higher yields tend to attract global investors toward Dollar-based assets, which increases demand for the US currency.

The Dollar’s strength against major currencies, including the Euro, has largely been driven by this shift in market sentiment.

Federal Reserve Outlook Remains a Key Driver

Investors are now paying close attention to future comments from Federal Reserve officials and upcoming economic reports from the United States.

The Fed has repeatedly stated that inflation remains one of its biggest concerns. If price pressures continue to stay elevated, policymakers may decide to keep interest rates higher for longer than previously expected.

A higher interest rate environment generally supports the US Dollar because it offers better returns for investors holding Dollar-denominated assets.

Meanwhile, the European Central Bank faces a different challenge. The Eurozone economy is showing signs of slowing growth, which could increase pressure on policymakers to consider easing measures in the future.

This widening gap between the economic outlooks of the United States and Europe has become an important factor influencing the EUR/USD exchange rate.

Geopolitical Tensions Increase Demand for Safe-Haven Assets

Apart from economic data, geopolitical developments have also played a role in supporting the US Dollar.

Ongoing tensions in the Middle East continue to create uncertainty in global financial markets. During periods of geopolitical instability, investors often move money into safe-haven assets, and the US Dollar is widely viewed as one of the safest currencies in the world.

Reports that US President Donald Trump is seeking diplomatic support from Chinese President Xi Jinping regarding the Iran conflict have added another layer of uncertainty to the market environment.

As long as geopolitical risks remain elevated, demand for the Dollar could continue to stay strong.

Market Focus Turns to Upcoming Economic Data

Looking ahead, traders will closely monitor additional economic reports from both the United States and the Eurozone.

In Europe, investors will be searching for signs that economic activity can stabilize after recent disappointing data. Any further weakness in manufacturing, consumer spending, or business activity could continue to weigh on the Euro.

In the United States, inflation data, labor market figures, and Federal Reserve comments are expected to remain the main market drivers. Stronger-than-expected US economic data could reinforce expectations that interest rates will stay elevated for a longer period.

At the same time, any improvement in Eurozone economic conditions or signs of easing inflation in the US could influence the direction of the EUR/USD pair in the coming weeks.

Summary

The EUR/USD pair remained under pressure as weak Eurozone GDP and Industrial Production figures hurt confidence in the European economy. Slower growth and continued weakness in manufacturing have increased concerns about the region’s economic outlook.

Meanwhile, the US Dollar stayed strong after higher US inflation reduced expectations for Federal Reserve interest rate cuts. Rising Treasury yields and ongoing geopolitical tensions also added support to the Greenback.

With investors closely watching economic data and central bank signals, the outlook for EUR/USD will likely continue to depend on the contrast between the economic performance of the Eurozone and the United States.

GBPUSD Slides Lower With Markets Eyeing Upcoming US PPI Report

The GBP/USD currency pair moved lower on Tuesday as growing political uncertainty in the United Kingdom and stronger-than-expected inflation data from the United States increased pressure on the British Pound. The pair fell by around 0.7% during the day, dropping from highs near 1.3650 before testing the important 1.3500 level. Although the Pound managed to recover slightly later in the session, it still remained near the bottom of its recent trading range.

GBPUSD reached a higher low area of the ascending channel

Investors are now closely watching several major economic events that could influence the next move for the Pound and the US Dollar. These include upcoming US inflation-related data, comments from Bank of England policymaker Catherine Mann, and the release of UK economic growth figures later this week.

Political Uncertainty Weakens the British Pound

The British Pound faced strong selling pressure after political tensions increased in Westminster. More than 70 Labour MPs publicly called for Prime Minister Keir Starmer to step down following disappointing local election results. The sudden rise in political instability created concerns among investors about the future direction of the UK government and its economic policies.

Financial markets reacted quickly to the growing uncertainty. UK government bonds, commonly known as gilts, saw heavy selling activity across different maturities. The yield on the 30-year UK gilt briefly climbed to 5.81%, marking its highest level since 1998.

Higher bond yields often reflect investor concerns about inflation, government borrowing, or fiscal stability. In this case, traders worried that any possible leadership change could lead to looser government spending policies at a time when inflation risks are already elevated.

The political situation has added another layer of pressure on the Pound, which was already struggling with concerns about inflation and economic growth.

Bank of England in Focus

Attention is now turning toward Catherine Mann, one of the more hawkish members of the Bank of England’s Monetary Policy Committee. Mann has repeatedly signaled that she remains concerned about long-term inflation risks in the UK economy.

She previously stated that she would support higher interest rates if inflation expectations continue rising through 2027. Her upcoming speech could provide important clues about how the Bank of England may respond to ongoing inflation pressures.

The central bank has already warned that inflation could move above 5% later this year. Much of this concern comes from rising energy costs linked to tensions in the Middle East and disruptions affecting global oil supply routes.

If Mann delivers another strong anti-inflation message, markets may begin expecting the Bank of England to maintain tighter monetary policy for longer. That could offer temporary support for the Pound, although political uncertainty may continue limiting gains.

UK GDP Data Could Influence Market Sentiment

Another important event for the British economy is the release of preliminary first-quarter Gross Domestic Product (GDP) data. Economists currently expect the UK economy to expand by 0.6% quarter-on-quarter.

The GDP report will provide investors with a clearer picture of how the UK economy is performing amid high inflation, political instability, and global uncertainty.

A stronger-than-expected GDP figure could help ease some concerns about economic weakness and support the Pound in the short term. However, weaker growth numbers may increase fears that the UK economy is slowing while inflation remains high, creating a difficult environment for policymakers.

Strong US Inflation Data Supports the Dollar

While the Pound struggled, the US Dollar gained strength after the latest US inflation report came in above expectations.

According to the April Consumer Price Index (CPI) report, headline inflation rose 3.8% compared to the previous year. Core inflation, which excludes volatile food and energy prices, increased 2.8% annually. Both readings exceeded market forecasts.

Monthly core inflation also climbed by 0.4%, showing that price pressures remain strong across several sectors of the economy.

Housing and energy costs continued to play a major role in keeping inflation elevated. Rising oil prices and ongoing disruptions linked to the Strait of Hormuz situation have contributed to increased energy costs globally.

The stronger inflation numbers boosted demand for the US Dollar because investors now believe the Federal Reserve may keep interest rates higher for a longer period.

Upcoming US Data Remains Important

Markets are now waiting for additional US economic reports that could shape expectations for Federal Reserve policy.

The upcoming Producer Price Index (PPI) report will show whether inflation pressures are also increasing at the wholesale level. If producer prices rise faster than expected, it could strengthen concerns that inflation remains difficult to control.

In addition to PPI data, investors are also preparing for US retail sales figures and weekly jobless claims data scheduled for release later this week.

Strong economic data from the United States would likely continue supporting the Dollar, especially if inflation remains elevated. On the other hand, weaker reports could reduce some of the recent momentum behind the US currency.

GBP/USD Faces a Sensitive Short-Term Outlook

The GBP/USD pair is currently being influenced by a mix of political and economic developments from both sides of the Atlantic.

In the UK, political uncertainty and concerns about fiscal policy are weighing heavily on investor confidence. At the same time, the Bank of England continues facing inflation risks that may require tighter monetary policy.

In the United States, stronger inflation data has reinforced expectations that interest rates could stay elevated for longer. This has provided fresh support for the US Dollar against major global currencies.

The next few days could prove especially important for the direction of GBP/USD as traders react to comments from Bank ofEngland officials, UK GDP figures, and additional US inflation-related reports.

Summary

GBP/USD moved sharply lower as political tensions in the UK and stronger US inflation data shifted market sentiment in favor of the US Dollar. Concerns surrounding Prime Minister Keir Starmer’s leadership created pressure on the British Pound, while rising US inflation strengthened expectations of higher interest rates in the United States.

Investors are now focusing on upcoming speeches from Bank of England policymakers, UK economic growth figures, and additional US economic reports for clearer direction. With both political and inflation risks remaining high, the Pound and the Dollar may continue experiencing increased volatility in the near term.

USDJPY Surges While Japanese Yen Struggles Under Growing Rate Hike Expectations

The Japanese Yen continued to lose ground against the US Dollar during Wednesday’s European trading session as investors reacted to stronger-than-expected inflation data from the United States. The USD/JPY currency pair climbed close to 157.70, supported by growing confidence that the US Federal Reserve could still raise interest rates later this year.

USDJPY is moving in an ascending channel, and the market has rebounded from the higher low area of the channel

The latest inflation figures from the United States have changed market sentiment significantly. Traders and investors are now paying closer attention to the possibility of tighter monetary policy from the Federal Reserve, which has boosted demand for the US Dollar while putting pressure on the Japanese Yen.

Strong US Inflation Data Boosts the Dollar

The main reason behind the Dollar’s recent strength is the latest Consumer Price Index (CPI) report from the United States. The April inflation data came in higher than economists had expected, signaling that price pressures in the country remain stubbornly strong.

According to the report, headline CPI increased by 3.8% year-over-year, beating market expectations of 3.7%. The previous reading stood at 3.3%, showing that inflation accelerated instead of cooling down.

This unexpected rise in inflation has fueled speculation that the Federal Reserve may need to keep interest rates higher for longer. Some investors even believe another rate hike could happen before the end of the year if inflation continues to remain elevated.

Higher interest rates generally support the US Dollar because they attract investors seeking better returns on US-based assets. As a result, the Dollar strengthened against several major currencies, including the Japanese Yen.

Federal Reserve Rate Hike Expectations Rise

Following the CPI release, market expectations around Federal Reserve policy shifted quickly. Investors are now reassessing the chances of additional tightening by the central bank.

Data from the CME FedWatch tool showed that the probability of at least one Fed rate hike by the end of the year increased sharply after the inflation report. Before the CPI release, the chances stood at around 23.5%. After the data, those odds jumped to 35.3%.

This rise in expectations has had a direct impact on currency markets. The Japanese Yen, which typically struggles when US interest rates rise, came under renewed pressure.

The gap between US and Japanese interest rates also continues to influence the market. While the Federal Reserve maintains a relatively aggressive stance to control inflation, the Bank of Japan remains cautious with monetary tightening. This difference in policy direction has helped support the Dollar against the Yen for an extended period.

Investors Await US Producer Price Data

Market participants are also closely watching the upcoming US Producer Price Index (PPI) data for April. The report is expected to provide more insight into inflation trends at the wholesale level.

The PPI figures are important because they can indicate whether businesses are facing rising production costs, which could eventually be passed on to consumers. If the data shows stronger inflationary pressure again, it may further strengthen expectations for tighter Federal Reserve policy.

Investors are likely to remain cautious ahead of the release, as any surprise in the data could create additional movement in the currency market.

Trump-Xi Meeting Becomes Key Market Focus

Beyond economic data, global investors are also paying close attention to geopolitical developments. One of the biggest upcoming events for financial markets is the meeting between US President Donald Trump and Chinese President Xi Jinping during Trump’s visit to Beijing this week.

The meeting is expected to attract significant attention because of the important economic relationship between the United States and China. Any comments related to trade, tariffs, or economic cooperation could influence market sentiment worldwide.

Currency traders are particularly sensitive to developments involving the world’s two largest economies because changes in trade relations can affect global growth expectations and investor confidence.

If the discussions between Trump and Xi lead to signs of improving relations, market sentiment could improve. However, any indication of renewed tensions may increase uncertainty and volatility across global markets.

Japanese Yen Remains Under Pressure

The Japanese Yen has struggled to recover despite comments from US Treasury Secretary Scott Bessent regarding cooperation with Japan on currency market stability.

Bessent confirmed that the United States and Japan are working together to address excessive volatility in currency markets. His remarks briefly influenced the USD/JPY pair earlier in the week, causing a short-term reaction.

However, the impact did not last long, as broader market forces continued to favor the US Dollar.

The Yen often faces pressure when US Treasury yields rise and investors expect tighter Federal Reserve policy. In contrast, Japan’s central bank continues to maintain relatively loose monetary conditions compared to other major economies.

This policy difference remains one of the biggest drivers behind the Yen’s weakness against the Dollar.

Global Markets Watch for the Next Direction

Financial markets are currently balancing multiple factors at the same time. Strong US inflation data has increased expectations of further Federal Reserve action, while geopolitical events are adding another layer of uncertainty.

Investors are carefully monitoring economic reports, central bank signals, and political developments to understand where markets could move next.

The US Dollar has benefited from stronger economic data and rising rate expectations, while the Japanese Yen continues to struggle under pressure from widening policy differences between the Federal Reserve and the Bank of Japan.

At the same time, the outcome of high-level talks between the United States and China could influence global risk sentiment and shape the direction of financial markets in the coming days.

Final Summary

The Japanese Yen weakened further against the US Dollar as stronger US inflation data boosted expectations of another possible Federal Reserve rate hike this year. Rising inflation has strengthened the Dollar and increased investor demand for US assets.

Markets are now focused on upcoming US PPI data and the highly anticipated meeting between Donald Trump and Xi Jinping, both of which could influence global market sentiment. Meanwhile, the Yen remains under pressure as policy differences between the US and Japan continue to favor the Dollar.

EURJPY Trades Sideways While Global Uncertainty Pressures the Euro

The EUR/JPY currency pair remained mostly unchanged during Wednesday’s Asian trading session after posting small losses a day earlier. The pair traded near the 185.00 level as weakness in the Euro was balanced by a softer Japanese Yen. Investors stayed cautious due to growing global uncertainty, especially after fading optimism surrounding peace efforts in the Middle East.

EURJPY is moving in Ascending channel and market has reached higher high area of the channel

Even though the Euro faced pressure from risk-averse market sentiment, the Japanese Yen also struggled to attract strong demand. This balance between both currencies helped keep the EUR/JPY pair relatively stable.

Risk Aversion Weighs on the Euro

The Euro came under pressure as investors turned more cautious in global markets. Concerns surrounding geopolitical tensions in the Middle East have reduced confidence among traders, pushing many investors toward safer positions.

Market participants had earlier hoped for progress toward peace in the region, but those expectations weakened. As uncertainty increased again, traders became more defensive, which affected the Euro’s momentum.

However, the decline in the Euro was not severe enough to create major losses against the Japanese Yen. The Yen itself remained under pressure because of expectations tied to future monetary policy changes in Japan.

Bank of Japan Signals More Rate Hikes Ahead

Attention has increasingly shifted toward the Bank of Japan (BOJ) after the release of its April Summary of Opinions. The report showed that policymakers are becoming more open to additional interest rate hikes, possibly as early as the next policy meeting.

Rising inflation remains a major concern for Japanese officials. Higher oil prices are adding pressure to consumer costs, and this may push the BOJ toward tightening monetary policy further.

For many years, Japan maintained extremely low interest rates to support economic growth. But inflation trends are now changing the outlook. Policymakers appear more willing to move away from ultra-loose monetary settings if price pressures continue rising.

OECD Expects Higher Japanese Interest Rates by 2027

The Organisation for Economic Co-operation and Development (OECD) also shared its outlook on Japan’s economy and monetary policy. According to the OECD, the Bank of Japan is expected to gradually raise short-term policy rates to 2% by the end of 2027.

This projection reflects expectations that inflation in Japan could remain elevated over the coming years. A move toward higher rates would mark a significant shift for Japan after decades of low borrowing costs.

The OECD also suggested that Japan should rely more heavily on consumption tax increases to strengthen government revenue. Japan continues to face long-term fiscal challenges, including high public debt and an aging population, making tax reforms an important topic for policymakers.

At the same time, the OECD warned that the BOJ must stay flexible with its bond-buying strategy. Financial markets could become unstable if policy adjustments happen too quickly, so officials may need to carefully manage the pace of future changes.

ECB Officials Hint at Possible Rate Increases

While Japan’s monetary outlook is changing, the Euro is also receiving support from growing expectations that the European Central Bank (ECB) could maintain a hawkish stance.

Bundesbank President Joachim Nagel warned that rising energy prices linked to the Iran conflict are increasing the possibility of future ECB interest rate hikes. Higher energy costs can fuel inflation across the Eurozone, making it more difficult for the central bank to ease policy aggressively.

Nagel’s comments suggest that inflation risks remain a serious concern for European policymakers despite recent efforts to stabilize prices.

Adding to the discussion, ECB Governing Council member Martin Kocher stated earlier this week that there is little reason to delay interest rate hikes if energy prices continue climbing rapidly.

These comments have supported the Euro by reinforcing expectations that the ECB may continue focusing on inflation control rather than shifting quickly toward easier monetary policy.

Japan’s Current Account Surplus Reaches Record High

Fresh economic data from Japan also attracted market attention. Japan reported a current account surplus of JPY 4,681.5 billion in March, significantly higher than the JPY 3,625.3 billion recorded during the same period last year.

The figure also exceeded market expectations, which had projected a surplus of JPY 3,879 billion. The latest reading marked the highest current account surplus ever recorded for the country.

A strong current account surplus generally reflects healthy export performance and overseas investment income. This can sometimes support the Japanese Yen because it indicates steady demand for Japanese assets and exports.

The stronger-than-expected data offered some support to the Yen, although broader market sentiment and central bank expectations remained the dominant drivers for the currency.

Investors Focus on Upcoming Eurozone Economic Data

Traders are now closely watching upcoming economic releases from the Eurozone. The market is waiting for first-quarter 2026 Gross Domestic Product (GDP) figures along with Employment Change data.

These reports could provide fresh insight into the strength of the Eurozone economy and influence expectations surrounding future ECB policy decisions.

If economic growth and employment figures come in stronger than expected, the Euro could receive additional support. On the other hand, weaker data may increase concerns about slowing economic momentum across the region.

For now, investors remain cautious as they assess both geopolitical developments and central bank signals from Europe and Japan.

Market Sentiment Keeps EUR/JPY in Balance

The EUR/JPY pair continues to trade in a narrow range as opposing forces keep the market balanced. Weakness in the Euro due to global uncertainty has been offset by expectations that Japan may continue raising interest rates gradually.

At the same time, support for the Euro remains tied to concerns about rising energy prices and the possibility of further policy tightening by the ECB.

With major economic data releases and central bank decisions still ahead, traders are likely to remain cautious in the short term. The balance between risk sentiment, inflation concerns, and monetary policy expectations will continue shaping the direction of EUR/JPY in the coming sessions.

Summary

EUR/JPY stayed relatively stable as weakness in both the Euro and Japanese Yen balanced each other out. Investors remained cautious because of geopolitical tensions and uncertainty surrounding global inflation. The Bank of Japan is increasingly open to further interest rate hikes, while ECB officials continue signaling concern about rising energy prices and inflation risks. Strong Japanese economic data and upcoming Eurozone GDP figures are also keeping traders focused on future market direction.

AUDUSD Gains Momentum With Traders Expecting Tougher RBA Policy

The Australian Dollar has been gaining strength against several major currencies as investors increase their expectations for another interest rate hike by the Reserve Bank of Australia (RBA). Strong economic signals from Australia, combined with global political developments and renewed strength in the US Dollar, are shaping the direction of the currency market this week.

AUDUSD is moving in an ascending channel, and the market has rebounded from the higher low area of the channel

The AUD is trading steadily against the US Dollar near the 0.7240 level during the European session on Wednesday. While the US Dollar remains firm overall, the Australian currency has managed to hold its ground due to growing confidence in the Australian economy and expectations of tighter monetary policy from the RBA.

Rising Expectations for an RBA Rate Hike

One of the biggest drivers behind the Australian Dollar’s recent strength is the growing belief that the Reserve Bank of Australia could raise interest rates again during its August policy meeting.

This shift in expectations comes after the Australian government released its 2026 federal budget. The budget introduced new tax relief measures that are expected to increase household spending power across the country.

Australian Treasurer Jim Chalmers announced that citizens earning between $18,201 and $45,000 will benefit from a lower tax rate beginning in July 2026. The tax rate for this income group will be reduced from its previous level to 15%.

The move is designed to help households manage living costs and improve disposable income. However, stronger consumer spending can also increase inflationary pressure in the economy. Since Australia is already dealing with elevated inflation levels, investors believe the central bank may need to respond with higher interest rates to keep price growth under control.

Higher interest rates generally support a currency because they can attract foreign investment seeking better returns. This is one reason why traders have become more optimistic about the Australian Dollar in recent sessions.

Budget Changes Could Boost Consumer Spending

The latest budget announcement has become a major talking point in financial markets because of its potential impact on inflation and economic growth.

Tax reductions often leave consumers with more money to spend on goods and services. While that can support economic activity, it may also create stronger demand across the economy, which can push prices higher.

For the RBA, controlling inflation remains a top priority. If consumer demand rises too quickly after the tax cuts take effect, policymakers may feel additional interest rate increases are necessary to maintain stability.

Investors are now watching future economic reports closely, especially inflation and employment data, to determine whether the central bank will continue its hawkish approach.

A hawkish central bank is one that favors tighter monetary policy, including higher interest rates, to fight inflation. Markets currently believe the RBA may maintain that stance longer than previously expected.

Trump-Xi Meeting Draws Global Attention

Another major event influencing the Australian Dollar is the upcoming meeting between United States President Donald Trump and Chinese President Xi Jinping.

The two leaders are expected to meet during Trump’s visit to Beijing between May 13 and May 15. Global investors are paying close attention because the outcome of these talks could affect trade relations between the world’s two largest economies.

Australia has strong economic ties with China, particularly through exports of commodities and raw materials. China remains one of Australia’s biggest trading partners, meaning any major change in US-China relations can quickly influence the Australian economy and its currency.

If the meeting results in improved cooperation and reduced trade tensions, market confidence could improve, which may support risk-sensitive currencies like the Australian Dollar.

On the other hand, if the talks create uncertainty or lead to new trade concerns, investors could become more cautious. That would likely place pressure on currencies connected to global trade and economic growth.

Why China Matters So Much to Australia

Australia’s economy depends heavily on exports to China. Products such as iron ore, coal, and agricultural goods make up a significant portion of Australian trade.

When China’s economy performs well, demand for Australian exports often increases. This can strengthen Australia’s economy and support the value of the Australian Dollar.

Because of this close relationship, developments involving China often have a direct impact on the AUD. Even political discussions between China and other major nations can affect investor sentiment toward the Australian currency.

The Trump-Xi meeting therefore carries added importance for Australian markets. Investors will look for any signs of progress on trade, investment, or economic cooperation between the two global powers.

US Dollar Remains Strong on Fed Expectations

While the Australian Dollar has shown resilience, the US Dollar continues to trade strongly due to changing expectations around the Federal Reserve.

Markets are increasingly pricing in the possibility that the Fed could raise interest rates at least once more this year. These expectations have supported demand for the Greenback across currency markets.

The US Dollar Index, which measures the strength of the US Dollar against a basket of major currencies, climbed around 0.3% and reached its highest level of the month near 98.58.

Strong economic data from the United States has contributed to the shift in market sentiment. Investors now believe the Federal Reserve may keep interest rates elevated for longer in an effort to control inflation and maintain economic stability.

A stronger US Dollar can create challenges for other currencies because it increases demand for USD-denominated assets. However, the Australian Dollar has managed to stay relatively stable thanks to rising RBA rate hike expectations.

Global Central Banks Continue to Influence Currency Markets

Currency markets remain highly sensitive to decisions made by central banks around the world. Investors constantly compare interest rate expectations between countries to decide where capital may flow next.

At the moment, both the Federal Reserve and the Reserve Bank of Australia are seen as leaning toward tighter monetary policy. This has created an interesting balance between the US Dollar and the Australian Dollar.

Traders are now focused on upcoming inflation reports, labor market data, and comments from policymakers for clues about future interest rate decisions.

Any surprise changes in economic conditions could quickly shift expectations and lead to increased volatility in currency markets.

Summary

The Australian Dollar has gained support from growing expectations that the Reserve Bank of Australia could raise interest rates again following the government’s latest budget announcement. Tax cuts aimed at boosting household spending have also increased concerns about inflation, strengthening the case for tighter monetary policy.

At the same time, investors are closely watching the meeting between Donald Trump and Xi Jinping, as the outcome could influence global trade sentiment and Australia’s export-driven economy.

Meanwhile, the US Dollar remains strong due to rising expectations that the Federal Reserve may still increase interest rates this year. With both central banks maintaining a firm stance on inflation, currency markets are likely to remain active in the coming weeks.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!