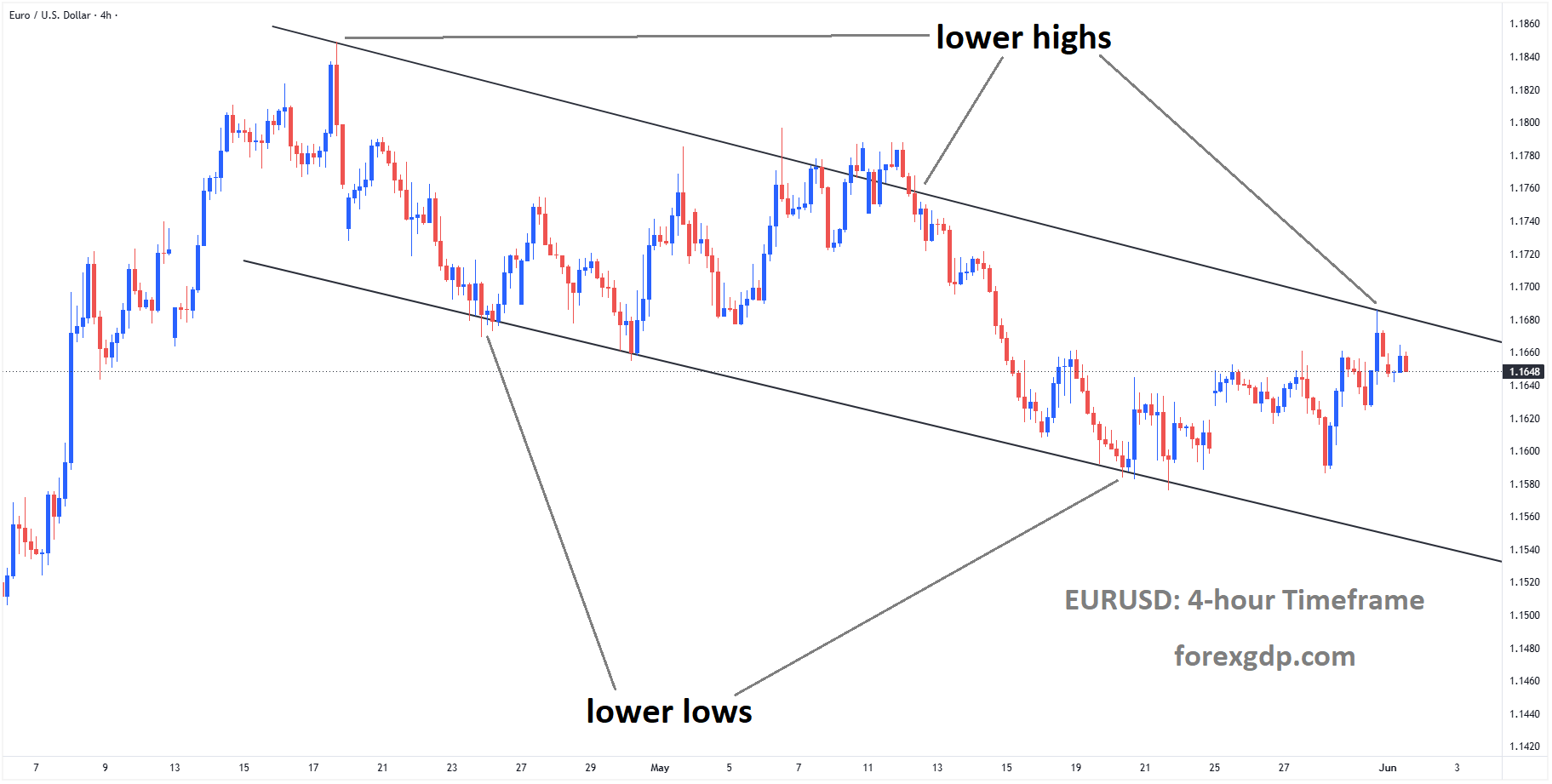

EURUSD is moving in a descending channel, and the market has fallen from the lower high area of the channel

EURUSD Remains Under Pressure While Eurozone Growth Slows and Global Risks Rise

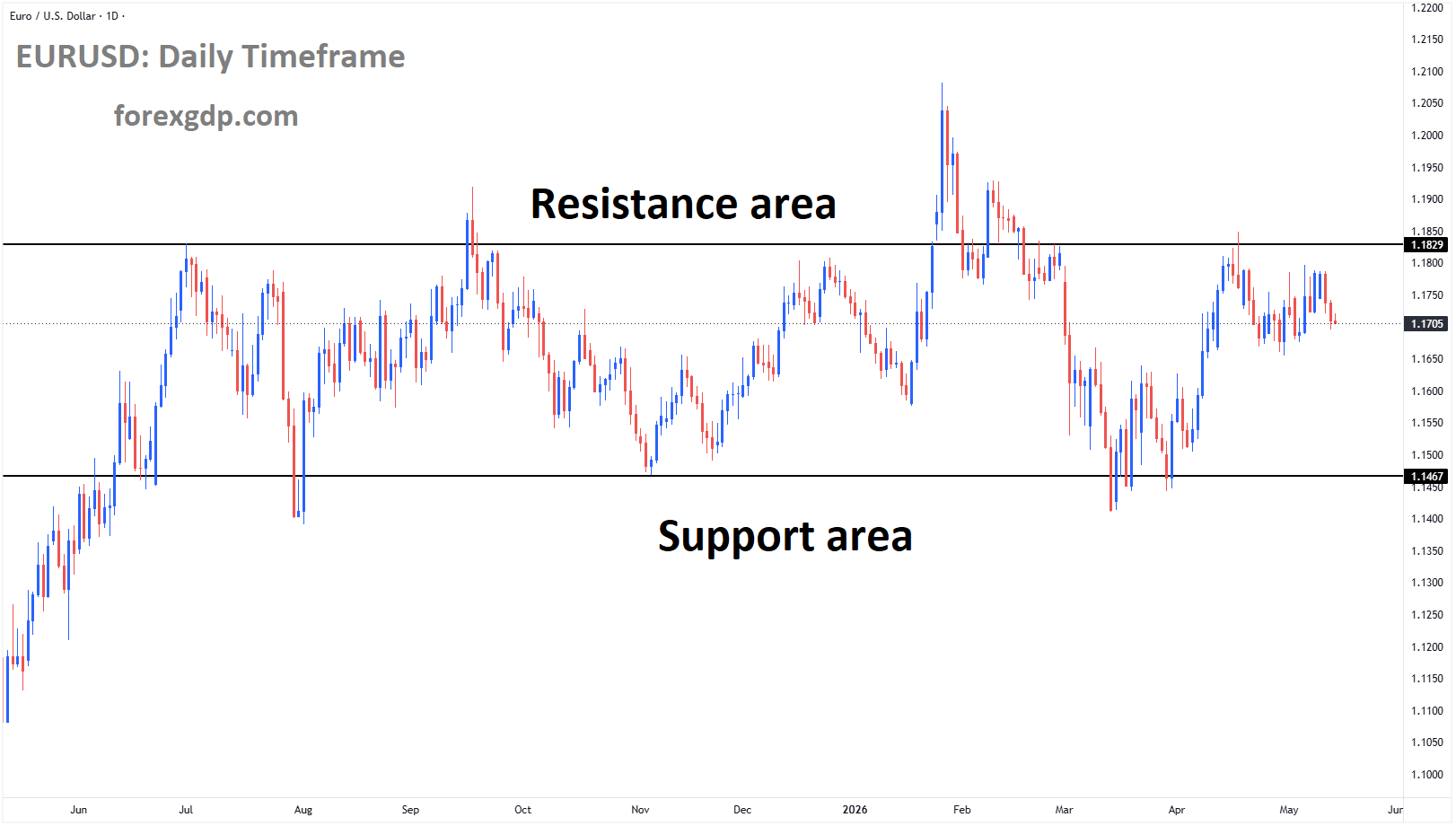

The Euro remained under mild pressure against the US Dollar on Monday, with the EUR/USD currency pair struggling to move beyond recent highs. Despite maintaining a relatively stable position, the pair continued to trade just below the upper boundary of the range that has held for the past two weeks.

A combination of mixed economic data from the Eurozone and growing geopolitical tensions in the Middle East has influenced investor sentiment. These developments have reduced risk appetite in global markets and created additional challenges for the common European currency.

Euro Remains Under Pressure Despite Stability

The EUR/USD pair showed limited movement during Monday’s trading session. While the Euro managed to avoid significant losses, it also lacked enough momentum to break higher and establish a stronger upward trend.

Market participants remain cautious as they assess a variety of economic and geopolitical factors. Investors are balancing concerns about slowing economic activity in Europe with expectations surrounding upcoming economic reports from the United States.

This cautious approach has kept the currency pair confined within a familiar trading range, preventing major directional moves.

Middle East Tensions Weigh on Investor Confidence

One of the main factors affecting market sentiment is the renewed escalation of tensions in the Middle East.

Reports indicated that the United States and Iran exchanged strikes earlier in the day, placing additional strain on an already fragile ceasefire agreement. At the same time, Israel intensified its military operations in Lebanon, adding another layer of uncertainty to the regional situation.

Geopolitical conflicts often lead investors to become more risk-averse. During periods of heightened uncertainty, traders typically move funds toward assets considered safer, which can impact currency movements and overall market sentiment.

Uncertainty Surrounding Ceasefire Efforts

Efforts to maintain peace in the region remain ongoing but face significant challenges.

US President Donald Trump is expected to sign a memorandum aimed at extending the current ceasefire arrangement for an additional 60 days. However, tensions remain elevated as officials on both sides continue to exchange warnings.

Iranian Parliament Speaker Mohammad Bagher Ghalibaf publicly criticized what he described as American noncompliance with ceasefire commitments and warned of potential retaliation. Such statements have increased concerns that the situation could worsen, keeping financial markets on edge.

Eurozone Manufacturing Growth Slows in May

Economic data released from the Eurozone provided a mixed picture of the region’s economy.

The latest HCOB Manufacturing Purchasing Managers’ Index (PMI) was revised slightly higher to 51.6 in May from the initial estimate of 51.4. Although the revision was positive, the reading remained below April’s level of 52.2.

A PMI reading above 50 generally signals expansion in manufacturing activity. Therefore, the sector continues to grow, but the slower pace suggests that momentum has weakened compared to previous months.

For investors, this slowdown raises questions about the strength of the Eurozone’s economic recovery. While manufacturing remains in growth territory, declining momentum can influence expectations regarding future economic performance.

Unemployment Rate Remains Unchanged

Additional data from Eurostat showed that the Eurozone unemployment rate remained steady at 6.3% in April.

Market expectations had pointed to a slight decline to 6.2%, which would have indicated further improvement in labor market conditions. The unchanged reading suggests that employment conditions are stable but not improving as quickly as some economists had hoped.

Labor market performance is closely watched because it serves as an important indicator of economic health. Stable unemployment can be viewed positively, but a lack of further improvement may limit optimism about future economic growth.

Together, the manufacturing and employment figures paint a picture of an economy that continues to expand but faces signs of slowing momentum.

Focus Shifts to Key US Economic Reports

Attention is also turning toward important economic releases from the United States.

The latest Institute for Supply Management (ISM) Manufacturing PMI is expected to indicate continued expansion in US manufacturing activity. A strong reading would reinforce perceptions that the American economy remains resilient despite global uncertainties.

However, the most significant market events of the week are likely to come from a series of labor market reports.

Nonfarm Payrolls Report in the Spotlight

Friday’s Nonfarm Payrolls report is expected to be the key focus for investors. The report provides valuable insights into job creation, wage growth, and overall labor market conditions in the United States.

Employment data plays a crucial role in shaping expectations about future decisions by the Federal Reserve. Strong labor market performance could support the view that the US economy remains healthy, while weaker numbers may lead investors to reassess monetary policy expectations.

As a result, traders are likely to remain cautious until more clarity emerges from these upcoming releases.

Why Investors Are Watching Closely

Several important themes are influencing market behavior at the moment:

- Slowing but still expanding manufacturing activity in the Eurozone.

- Stable unemployment levels that failed to show the expected improvement.

- Rising geopolitical tensions involving the United States, Iran, and Israel.

- Upcoming US economic reports that could influence Federal Reserve policy expectations.

These factors are creating a complex environment where traders are hesitant to make aggressive moves in either direction.

Summary

The Euro remained slightly weaker against the US Dollar on Monday, with EUR/USD continuing to trade near the upper end of its recent range. Mixed economic data from the Eurozone highlighted slower manufacturing growth and unchanged unemployment levels, while escalating tensions in the Middle East added to market uncertainty.

At the same time, investor attention is shifting toward key US economic releases, particularly employment data and Friday’s Nonfarm Payrolls report. With geopolitical risks rising and important economic indicators still ahead, market participants are likely to remain cautious as they search for clearer signals about the direction of the global economy and future monetary policy.

GBPUSD Strengthens While BoE Keeps Flexible Approach Toward Inflation Risks

The British Pound started the week on a positive note, gaining ground against several major currencies despite cautious remarks from Bank of England (BoE) Governor Andrew Bailey. While the UK currency showed strength against many of its peers, it remained relatively stable against the US Dollar during Monday’s European trading session.

GBPUSD is falling from the retest area of the broken ascending channel

Investors are carefully balancing comments from central bank officials, ongoing geopolitical concerns, and an important week of economic data from the United States. With major employment figures and manufacturing data due soon, financial markets are waiting for clearer signals about the future direction of monetary policy on both sides of the Atlantic.

BoE Governor Signals Patience on Interest Rates

One of the key developments influencing the British Pound is the latest message from Bank of England Governor Andrew Bailey. Speaking at a conference in Reykjavik on Friday, Bailey suggested that policymakers do not need to rush into tightening monetary policy.

According to Bailey, the UK economy is currently facing a combination of softer economic conditions and heightened uncertainty caused by tensions in the Middle East. These factors make policy decisions more challenging, particularly when inflation remains above the central bank’s target.

The governor indicated that allowing inflation to remain temporarily above the target level may be a reasonable approach under current circumstances. This reflects the difficult balance policymakers must strike between controlling inflation and supporting economic growth.

His comments suggest that the Bank of England is willing to be patient rather than react aggressively to short-term inflation pressures.

Inflation Risks Remain on the Radar

Although Bailey expressed a cautious approach toward raising interest rates, he also emphasized that the Bank of England is not ignoring inflation risks.

The governor explained that the central bank’s tolerance for above-target inflation would diminish if there are signs of so-called “second-round effects.” These occur when higher prices begin influencing wages, business costs, and broader inflation expectations across the economy.

If inflation becomes more deeply embedded and starts spreading through different sectors, policymakers may need to reconsider their stance and take stronger action.

This message highlights that while the Bank of England is not currently signaling an urgent need for higher rates, it remains ready to respond if inflationary pressures become more persistent.

Energy Concerns Add Pressure to the UK Economy

Another factor shaping the outlook for the United Kingdom is the ongoing uncertainty surrounding energy markets.

The UK relies heavily on imported oil and energy supplies. As a result, any disruption linked to geopolitical tensions can create challenges for businesses, households, and policymakers.

Concerns about energy supply shocks have increased due to instability in the Middle East. Such developments can push up energy costs, increase inflationary pressures, and slow economic activity at the same time.

For the Bank of England, this creates a difficult policy environment. Raising interest rates too quickly could weaken economic growth, while remaining too cautious could allow inflation pressures to linger longer than desired.

The central bank therefore faces a delicate balancing act as it monitors both domestic economic conditions and global developments.

British Pound Shows Resilience

Despite the cautious tone from the Bank of England governor, the British Pound managed to gain strength against several major currencies.

This resilience suggests that investors remain relatively confident in the UK’s economic outlook and believe the central bank still has flexibility to respond if inflation risks intensify.

At the same time, the Pound’s performance against the US Dollar was more restrained. The currency pair remained broadly stable around the 1.3455 area as traders avoided making significant moves ahead of important economic releases from the United States.

The lack of major movement reflects a wait-and-see approach among market participants who are looking for clearer guidance from upcoming data.

US Dollar Steady Ahead of Busy Economic Week

Across the Atlantic, the US Dollar began the week with little movement as investors prepared for a series of important economic reports.

The US Dollar Index (DXY), which measures the value of the Greenback against a basket of six major currencies, traded close to the 99.00 level. This relatively calm performance indicates that traders are holding back from taking large positions before key economic updates are released.

The upcoming data could play a major role in shaping expectations for future Federal Reserve policy decisions.

Market participants are particularly interested in understanding whether the US economy continues to show resilience or whether signs of slowing growth are beginning to emerge.

Focus Turns to US Nonfarm Payrolls Report

The most anticipated event of the week is the release of the US Nonfarm Payrolls (NFP) report for May, scheduled for Friday.

The employment report is one of the most closely watched economic indicators because it provides insight into the health of the labor market. Strong job growth can signal a robust economy, while weaker figures may raise concerns about slowing economic momentum.

Investors will study the report carefully for clues about future Federal Reserve policy decisions. Employment data often influences expectations regarding interest rates and the broader economic outlook.

As a result, both currency and financial markets are likely to react strongly once the figures are published.

Manufacturing Data Also in Spotlight

Before the employment report arrives, investors will also focus on US manufacturing activity.

The Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index (PMI) for May is scheduled for release on Monday. This report offers a snapshot of conditions within the manufacturing sector and can provide early signals about the direction of the broader economy.

A stronger reading could support confidence in economic growth, while a weaker result may reinforce concerns about slowing activity.

Because the manufacturing sector often reflects shifts in business confidence and demand, the report is expected to receive close attention from traders and economists alike.

Summary

The British Pound started the week with modest gains against major currencies, even as Bank of England Governor Andrew Bailey signaled there is no immediate need to tighten monetary policy. While the central bank remains willing to tolerate temporarily elevated inflation, officials are closely watching for signs that inflation pressures may become more widespread.

Meanwhile, ongoing geopolitical tensions and energy market uncertainty continue to present challenges for the UK economy. Despite these concerns, the Pound has remained resilient.

On the US side, the Dollar traded in a narrow range as investors awaited a series of important economic reports. The upcoming ISM Manufacturing PMI and Friday’s Nonfarm Payrolls report are expected to provide valuable insight into the strength of the US economy and the future path of Federal Reserve policy. As these data releases approach, market participants are likely to remain cautious while looking for fresh direction.

USDJPY Moves Higher as Escalating Regional Conflict Boosts US Dollar Appeal

The USD/JPY currency pair started the week on a stronger note, with the US Dollar gaining ground against the Japanese Yen. Growing geopolitical tensions in the Middle East have increased uncertainty across global financial markets, leading investors to seek safer assets. As a result, demand for the US Dollar has risen, helping the pair move higher.

USDJPY is rebounding from the higher low area of the ascending channel

At the same time, concerns about rising energy costs and their impact on Japan’s economy have continued to weigh on the Japanese Yen. With several important economic reports scheduled in the United States this week, market participants are closely monitoring developments that could influence the future direction of monetary policy.

Rising Geopolitical Risks Boost Demand for the US Dollar

The US Dollar has received support from a renewed wave of safe-haven demand. Investors often move funds into the Dollar during periods of global uncertainty because it is widely viewed as one of the world’s most reliable reserve currencies.

Recent developments in the Middle East have increased concerns about regional stability. Tensions involving the United States and Iran have raised questions about whether the current ceasefire can hold, while military activity involving Israel and Lebanon has added to fears of further escalation.

These geopolitical risks have weakened overall market sentiment and encouraged investors to reduce exposure to riskier assets. In this environment, the US Dollar has benefited from increased demand, helping USD/JPY move higher at the start of the week.

Higher Energy Costs Create Challenges for Japan

While the US Dollar has found support from global uncertainty, the Japanese Yen has faced pressure from concerns surrounding rising oil prices.

Japan relies heavily on imported energy to meet its domestic needs. This dependence makes the country particularly vulnerable to disruptions in global energy supply chains. Any threat to major shipping routes, especially those linked to oil transportation, can increase concerns about higher import costs and slower economic growth.

As energy prices rise, investors worry about the potential impact on Japanese businesses, consumers, and overall economic performance. These concerns have contributed to weakness in the Yen, keeping it close to its lowest levels in several weeks against the US Dollar.

Japanese Economic Data Fails to Support the Yen

Fresh economic data released in Japan offered little encouragement for Yen bulls.

Corporate Capital Spending remained unchanged during the first quarter of the year. This followed a strong annual increase of 6.5% in the previous quarter. The flat reading suggests that business investment activity may be losing momentum after a period of stronger growth.

Business investment is often viewed as a key indicator of economic confidence. When companies reduce or delay spending plans, it can signal caution about future economic conditions. The latest figures therefore added to concerns that Japan’s economic recovery may be facing new challenges.

As a result, the data did little to strengthen demand for the Japanese currency.

Bank of Japan Maintains Focus on Policy Normalization

Despite recent economic concerns, policymakers at the Bank of Japan continue to support a gradual shift away from the ultra-loose monetary policies that have defined the country’s financial landscape for years.

The latest Summary of Opinions from the Bank of Japan’s April policy meeting showed that many officials believe further interest rate increases may be appropriate in the near future. Policymakers also highlighted ongoing inflation risks, suggesting that price pressures remain an important factor in decision-making.

Market expectations have increasingly shifted toward the possibility of another rate increase at the Bank of Japan’s upcoming meeting. Investors believe there is a strong chance that policymakers could move forward with a modest quarter-point rate hike.

While expectations of higher rates would normally support a currency, the impact on the Yen has been limited due to broader concerns about economic growth and rising energy costs.

Investors Await Key US Economic Reports

Attention is now turning toward a busy week of economic data releases in the United States.

One of the first major reports on the calendar is the Institute for Supply Management (ISM) Manufacturing Purchasing Managers’ Index. The report will provide insight into the health of the US manufacturing sector and could influence expectations for economic growth.

However, the primary focus for investors remains the US labor market.

Several employment-related reports are scheduled throughout the week, culminating in the closely watched Nonfarm Payrolls report on Friday. This data is considered one of the most important indicators of economic strength in the United States.

Strong employment figures could reinforce confidence in the US economy and influence expectations regarding future decisions by the Federal Reserve. On the other hand, weaker-than-expected data could lead investors to reassess the outlook for interest rates and economic growth.

What Could Influence USD/JPY Going Forward?

The current environment continues to favor the US Dollar over the Japanese Yen. Safe-haven demand linked to geopolitical uncertainty remains supportive for the Dollar, while concerns over Japan’s energy costs and economic outlook continue to pressure the Yen.

At the same time, upcoming US economic reports have the potential to create additional volatility in the currency pair. Investors will be closely analyzing every major release for clues about the strength of the US economy and the future direction of Federal Reserve policy.

One factor that could limit further gains in USD/JPY is the possibility of intervention by Japanese authorities. In the past, officials have stepped into currency markets when Yen weakness became excessive. Any signs that authorities are becoming uncomfortable with the pace of the Yen’s decline could slow the pair’s upward momentum.

Summary

USD/JPY began the week on a stronger footing as escalating geopolitical tensions increased demand for the US Dollar. Concerns over rising oil prices and their impact on Japan’s import-dependent economy have continued to weigh on the Japanese Yen, while recent domestic economic data offered limited support.

Although the Bank of Japan remains open to further policy normalization, broader economic concerns have kept the Yen under pressure. Meanwhile, investors are preparing for a series of important US economic reports, particularly labor market data, which could play a major role in shaping expectations for Federal Reserve policy and the future direction of USD/JPY.

AUDUSD Under Pressure While Regional Tensions Weigh on Market Confidence

The Australian Dollar came under pressure at the start of the week, with the AUD/USD currency pair falling toward the 0.7180 level during early European trading on Monday. A combination of rising geopolitical uncertainty in the Middle East and changing expectations around Australian interest rates contributed to the weakness of the Aussie against the US Dollar.

AUDUSD is moving in an ascending channel, and the market has rebounded from the higher high area of the channel

Investors remain cautious as global developments continue to shape market sentiment. At the same time, upcoming US economic data releases are expected to play an important role in determining the next direction for the US Dollar.

Middle East Conflict Fuels Demand for Safer Assets

One of the key factors weighing on the Australian Dollar is the growing tension in the Middle East. As geopolitical risks increase, investors often move money away from risk-sensitive assets and into safer alternatives.

The Australian Dollar is generally considered a risk-linked currency because Australia’s economy is closely tied to global trade and economic growth. When uncertainty rises around the world, traders tend to reduce their exposure to currencies like the AUD.

Recent reports highlighted escalating security concerns in the region. Kuwait’s military announced that its air defense systems were actively intercepting missile and drone attacks after emergency alerts and air raid sirens were triggered across the country. Such developments have added to fears of a wider regional conflict and increased investor caution.

The ongoing situation has strengthened demand for safer investments, which has supported the US Dollar while putting additional pressure on the Australian currency.

US-Iran Developments Remain in Focus

Investors are also paying close attention to relations between the United States and Iran. Over the weekend, Iranian Foreign Minister Abbas Araghchi stated that discussions and exchanges of messages with the United States were continuing.

However, he noted that it was still too early to assess the progress of negotiations until a clearer outcome emerged. This uncertainty has left markets waiting for further developments before making stronger directional moves.

Any significant changes in the relationship between the two countries could have a broader impact on global markets, influencing investor confidence and currency movements.

Upcoming US Economic Data Could Drive the Dollar

While geopolitical tensions remain a major focus, traders are also preparing for important economic data from the United States.

The US ISM Manufacturing Purchasing Managers Index (PMI) report is scheduled for release later on Monday. The report is widely followed because it provides insights into the health of the manufacturing sector and overall economic activity.

Beyond Monday’s data, attention is already shifting toward the highly anticipated US employment report due later in the week.

Focus on Nonfarm Payrolls

Friday’s Nonfarm Payrolls (NFP) report is expected to be one of the most important economic releases of the week. Economists forecast that the US economy added around 96,000 jobs in May.

Meanwhile, the unemployment rate is expected to remain unchanged at 4.3%.

Strong employment figures could reinforce confidence in the resilience of the US economy. On the other hand, weaker-than-expected numbers may raise questions about the pace of economic growth.

The report is particularly important because Federal Reserve officials have indicated that inflation risks remain a concern. Some policymakers have suggested that further action may be needed if geopolitical developments contribute to higher inflationary pressures.

US Dollar Influenced by Both Data and Geopolitics

Market participants recognize that the US Dollar is currently being driven by a mix of economic and geopolitical factors.

According to Joseph Capurso, Head of Foreign Exchange at Commonwealth Bank of Australia, the US Dollar’s direction will largely depend on developments related to the US-Iran conflict as well as the upcoming May employment report.

This combination creates a complex environment for traders. Positive economic data may strengthen the Dollar, while any escalation in geopolitical tensions could further increase demand for safe-haven assets.

As a result, investors are closely monitoring both headlines and economic indicators for clues about future market direction.

Australian Economic Data Reduces RBA Rate Hike Expectations

On the Australian side, domestic economic developments have also contributed to the Australian Dollar’s weakness.

Recent inflation figures came in below expectations, suggesting that price pressures may be easing faster than previously thought. At the same time, Australia recorded an unexpected increase in its unemployment rate.

These developments have significantly changed market expectations regarding future action by the Reserve Bank of Australia (RBA).

Sharp Drop in Rate Hike Expectations

Before the latest employment report was released, markets had assigned a modest probability that the RBA might raise interest rates at its upcoming meeting. However, those expectations have fallen sharply following the weaker labor market data.

According to pricing data cited by Westpac, the probability of an interest rate increase at the next RBA meeting dropped to just 3%, down from 13% before the employment figures were published.

Lower expectations for future rate increases generally reduce support for a currency because investors often seek higher returns in markets where interest rates are expected to rise.

As a result, the Australian Dollar has faced additional selling pressure as traders reassess the outlook for Australian monetary policy.

Market Sentiment Remains Fragile

The combination of geopolitical uncertainty and softer domestic economic indicators has created a challenging environment for the Australian Dollar.

Investors remain cautious as they assess the impact of Middle East tensions, monitor ongoing diplomatic developments involving Iran and the United States, and prepare for key US economic reports.

At the same time, reduced expectations for tighter monetary policy in Australia have weakened support for the Aussie, leaving it vulnerable to further shifts in global sentiment.

Summary

The AUD/USD pair moved lower near 0.7180 as investors reacted to growing tensions in the Middle East and changing expectations for Australian interest rates. Rising geopolitical risks boosted demand for the US Dollar, while weaker Australian inflation and labor market data reduced the likelihood of a near-term rate increase from the Reserve Bank of Australia.

Looking ahead, traders will closely watch US economic releases, particularly the ISM Manufacturing PMI and the Nonfarm Payrolls report. Together with developments in the Middle East, these events are expected to play a major role in shaping the outlook for both the US Dollar and the Australian Dollar in the days ahead.

NZDUSD Extends Decline While Investors Overlook Encouraging China PMI Report

The New Zealand Dollar continued to face pressure against the US Dollar at the start of the week, with the NZD/USD pair trading near 0.5975 during the early Asian session on Monday. While investors assessed the latest economic data from China, market attention gradually shifted toward important economic releases from the United States that could influence currency movements in the coming days.

NZDUSD reached a lower high area of the symmetrical triangle pattern

Global financial markets are entering a busy period, with several major economic reports scheduled for release. These reports are expected to provide fresh insight into the health of the US economy and could play a significant role in shaping investor sentiment.

Chinese Manufacturing Data Offers Mixed Signals

China released its latest Manufacturing Purchasing Managers’ Index (PMI) data on Monday, providing an update on the country’s industrial activity. According to the report from RatingDog, the manufacturing PMI eased to 51.8 in May from 52.2 in April.

Although the reading showed a slight slowdown compared to the previous month, it still exceeded market expectations of 51.4. A PMI figure above 50 generally indicates expansion in the manufacturing sector, suggesting that Chinese factories continue to experience growth despite some moderation.

China’s economic performance is often closely watched by investors because of its strong trade relationship with New Zealand. As one of New Zealand’s largest trading partners, changes in Chinese economic activity can influence demand for New Zealand exports and impact the value of the New Zealand Dollar.

However, despite the better-than-expected PMI result, the data did not provide meaningful support for the Kiwi. The currency remained relatively weak, indicating that traders are focusing on broader global factors rather than a single economic report.

Market Attention Turns to US Manufacturing Data

While Chinese economic figures attracted some attention early in the day, traders are primarily preparing for the release of the US ISM Manufacturing PMI report later on Monday.

This report is widely followed because it provides valuable information about business conditions within the US manufacturing sector. Investors often use it to gauge the strength of economic activity and potential future trends.

A stronger reading could reinforce confidence in the resilience of the US economy, while a weaker result may raise concerns about slowing growth. Either outcome has the potential to influence demand for the US Dollar and affect major currency pairs, including NZD/USD.

Geopolitical Developments Remain in Focus

Beyond economic data, geopolitical events continue to influence market sentiment. Investors are keeping a close watch on developments in the Middle East, particularly the ongoing interactions between the United States and Iran.

Periods of heightened geopolitical uncertainty often encourage investors to move toward assets perceived as safer, while reducing exposure to currencies and investments considered risk-sensitive. The New Zealand Dollar is commonly viewed as a risk-linked currency, meaning it can come under pressure when market uncertainty increases.

Iranian Foreign Minister Abbas Araghchi recently stated that discussions and message exchanges with Washington remain ongoing. However, he also noted that it is still too early to draw conclusions about the outcome of the negotiations.

As long as uncertainty remains, traders are likely to remain cautious, and any escalation in tensions could influence broader financial markets.

Federal Reserve Independence Remains a Talking Point

Investors are also paying attention to comments regarding the independence of the US Federal Reserve.

Former Federal Reserve Chair Jerome Powell recently emphasized the importance of maintaining public trust in the central bank. According to reports, Powell stated that allowing political leaders to dismiss Federal Reserve officials over policy disagreements could weaken confidence in the institution.

Central bank independence is considered an important foundation for maintaining economic stability and credibility. Comments related to the Federal Reserve often attract attention because monetary policy decisions have a direct impact on interest rates, inflation management, and overall economic conditions.

Although Powell’s remarks were not directly tied to immediate policy changes, they contributed to ongoing discussions about the role and independence of the US central bank.

All Eyes on Friday’s Employment Report

The most anticipated economic event of the week is likely to be the release of the US Nonfarm Payrolls (NFP) report on Friday.

The NFP report is one of the most influential indicators of labor market health in the United States. It measures the number of jobs added or lost across the economy, excluding farm workers, government employees, and a few other categories.

Economists currently expect the US economy to have added approximately 96,000 jobs in May. At the same time, the unemployment rate is projected to remain unchanged at 4.3%.

The results could have a significant impact on market expectations regarding future economic conditions and monetary policy. A stronger-than-expected employment report would suggest continued resilience in the labor market and could support demand for the US Dollar.

On the other hand, weaker employment figures could raise concerns about slowing economic momentum and potentially alter investor expectations.

What Traders Are Watching Next

As the week progresses, market participants will be balancing several important themes. Economic data from both China and the United States, geopolitical developments in the Middle East, and discussions surrounding Federal Reserve policy are all contributing to market uncertainty.

For the NZD/USD pair, upcoming US economic releases remain the primary focus. The ISM Manufacturing PMI and Friday’s Nonfarm Payrolls report could provide crucial clues about the direction of the US economy and influence currency market sentiment.

Summary

The New Zealand Dollar started the week on a weaker footing against the US Dollar, with NZD/USD trading near 0.5975. Although China’s manufacturing sector delivered better-than-expected growth data, it failed to provide meaningful support for the Kiwi. Investors are now concentrating on upcoming US economic reports, particularly the ISM Manufacturing PMI and the highly anticipated Nonfarm Payrolls release. At the same time, geopolitical tensions and discussions about Federal Reserve independence continue to shape overall market sentiment, making the days ahead especially important for currency traders.

Don’t trade all the time, trade forex only at the confirmed trade setups

Get more confirmed trade signals at premium or supreme – Click here to get more signals, 2200%, 800% growth in Real Live USD trading account of our users – click here to see , or If you want to get FREE Trial signals, You can Join FREE Signals Now!