USDCAD Retreats While Canadian Dollar Bounces Back After Recent Weakness

The USD/CAD currency pair moved lower on Tuesday, ending a four-day streak of gains after reaching its highest level in roughly two months. The pullback came as investors reassessed global risk conditions, shifting their attention toward geopolitical developments in the Middle East and upcoming economic events in both the United States and Canada.

Although the US Dollar had recently benefited from safe-haven demand, improving hopes for a reduction in regional tensions led some traders to reduce defensive positions. At the same time, uncertainty surrounding the situation in the Middle East continues to keep markets cautious.

USD/CAD Loses Momentum After Reaching Multi-Month High

After climbing steadily over the previous several sessions, USD/CAD eased back following its rise to a two-month peak. The retreat reflected a softer US Dollar as investors responded to signs of reduced tensions between Iran and Israel.

The recent rally in the pair had been supported by demand for safe-haven assets amid fears of a broader regional conflict. However, sentiment improved after reports indicated that both Iran and Israel had agreed to halt direct attacks against one another. The development followed diplomatic efforts and calls for restraint from international leaders.

The possibility of a pause in hostilities encouraged investors to take on slightly more risk, reducing the appeal of traditional safe-haven assets such as the US Dollar.

Middle East Uncertainty Continues to Influence Market Sentiment

Despite signs of de-escalation, traders remain far from confident that the situation has fully stabilized. Fresh warnings from Israeli officials have highlighted the fragile nature of the ceasefire and the potential for renewed tensions.

Reports indicated that residents of the Lebanese city of Tyre were instructed to evacuate certain areas ahead of expected military operations. The warning added another layer of uncertainty to an already complex regional situation.

Israeli Prime Minister Benjamin Netanyahu also emphasized that military operations connected to Iran and Hezbollah are not fully over, even while stating that both groups have been significantly weakened. His remarks came shortly after Iran’s military confirmed that it had stopped launching attacks against Israel.

These mixed signals have left investors balancing optimism about a possible diplomatic solution with concerns that the conflict could reignite. As a result, financial markets remain highly sensitive to headlines from the region.

Strong US Economic Data Shapes Federal Reserve Expectations

Beyond geopolitical developments, investors are also closely monitoring the outlook for US monetary policy.

Recent employment data from the United States came in stronger than expected, reinforcing the view that the American economy remains resilient. A strong labor market can contribute to ongoing inflation pressures by supporting consumer spending and wage growth.

Because of this, traders have adjusted their expectations regarding future Federal Reserve decisions. Market participants increasingly believe policymakers could maintain a cautious stance toward lowering borrowing costs if inflation remains persistent.

The focus now turns to upcoming inflation reports, which are expected to provide fresh clues about the direction of US monetary policy.

Inflation Reports in Focus

Two major economic releases are drawing significant attention this week:

")

- The Consumer Price Index (CPI)

- The Producer Price Index (PPI)

These reports offer insight into price pressures across the economy and can influence expectations about future Federal Reserve actions.

If inflation shows signs of remaining elevated, policymakers may choose to keep interest rates higher for longer. On the other hand, evidence of cooling inflation could support a more flexible policy outlook.

Because the Federal Reserve’s decisions have a major impact on the US Dollar, traders are watching these reports closely.

Canadian Data and Bank of Canada Decision Take Center Stage

On the Canadian side, investors are preparing for several important developments.

One key release is Canada’s International Merchandise Trade data, which provides information about the country’s exports and imports. Trade performance is an important indicator of economic health, particularly for Canada, whose economy relies heavily on international commerce.

However, the primary event for Canadian markets is the upcoming Bank of Canada policy announcement.

Bank of Canada Expected to Hold Rates Steady

Economists and market participants largely expect the Bank of Canada to leave its benchmark interest rate unchanged at 2.25%.

A decision to maintain current policy settings would signal that policymakers are still evaluating economic conditions before making further adjustments. The central bank has been balancing the need to support economic growth while ensuring inflation remains under control.

Investors will not only focus on the rate decision itself but also on any comments from policymakers regarding the future path of monetary policy. Guidance about inflation trends, economic growth, and labor market conditions could influence expectations for the months ahead.

For the Canadian Dollar, the tone of the central bank’s statement may prove just as important as the actual rate decision.

Markets Enter a Critical Week

The combination of geopolitical uncertainty, major inflation reports, and a central bank meeting has created a busy and potentially volatile week for currency markets.

While hopes for reduced tensions in the Middle East have eased demand for the US Dollar, lingering uncertainty continues to limit investor confidence. At the same time, upcoming economic data from the United States could reshape expectations for Federal Reserve policy.

In Canada, traders are waiting to hear how the Bank of Canada views the economic outlook and whether policymakers see any need for future policy adjustments.

Summary

USD/CAD stepped back after reaching a two-month high, ending a four-day winning streak as safe-haven demand for the US Dollar weakened. The move followed reports of a halt in direct attacks between Iran and Israel, although concerns remain due to ongoing uncertainty in the Middle East.

Investors are also focused on important economic events, including US inflation reports and Canada’s trade data. Meanwhile, the Bank of Canada is widely expected to keep interest rates unchanged, making its policy statement a key event for markets. With geopolitical risks and central bank decisions both in focus, traders are preparing for a week that could shape the direction of the US and Canadian currencies.

EURUSD Gains Momentum as Traders Eye ECB Move and Dollar Eases

The EUR/USD currency pair continued its upward movement on Tuesday, building on gains from the previous session. After finding support near the 1.1500 area on Monday, the Euro strengthened against the US Dollar for a second consecutive day, helping recover part of the losses recorded last week.

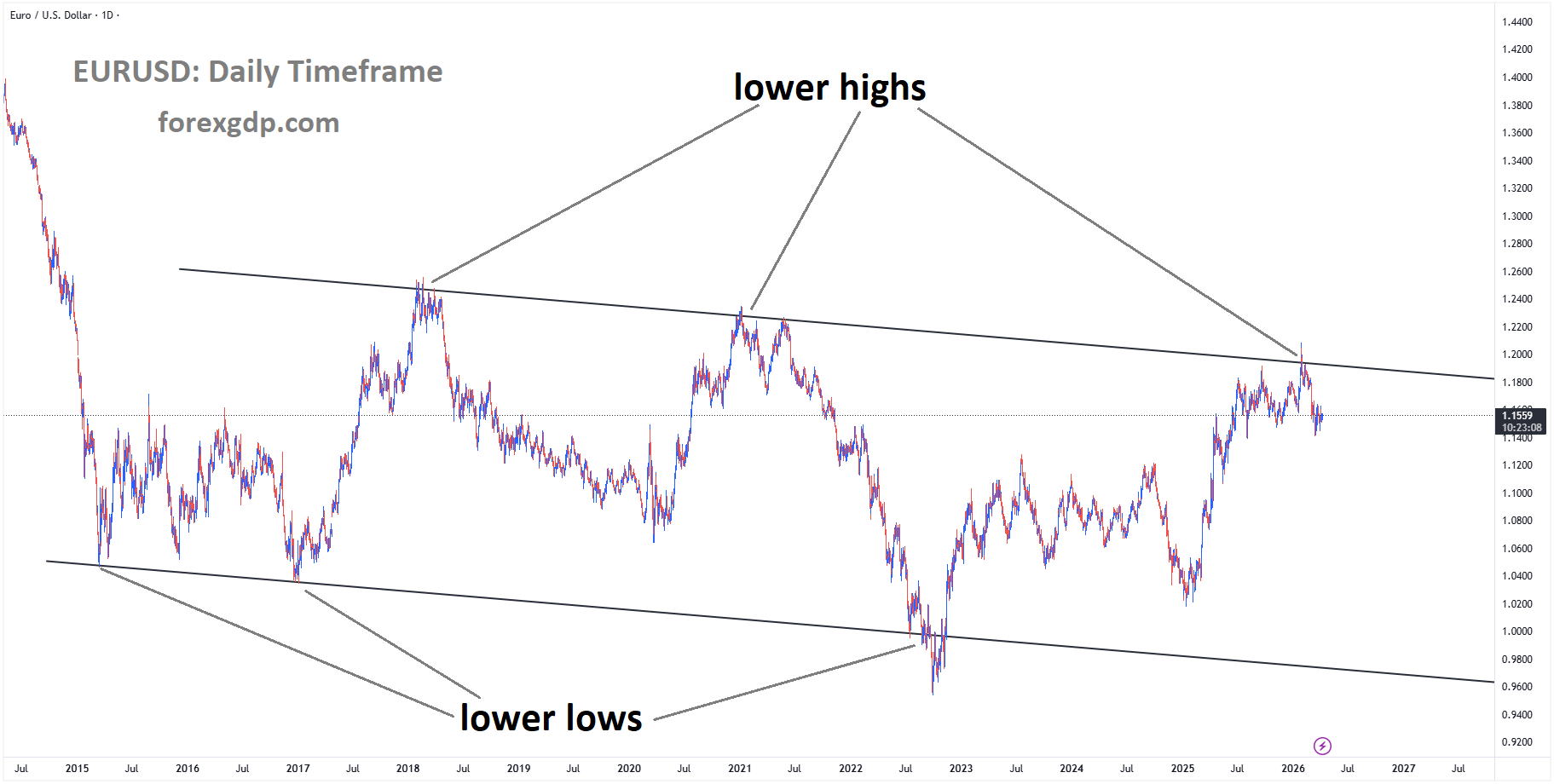

EURUSD is moving in a descending channel, and the market has rebounded from the lower low area of the channel

The pair climbed to around 1.1555 during the session, supported by growing expectations that the European Central Bank (ECB) will raise interest rates at its upcoming meeting. At the same time, a more positive mood in global markets reduced demand for the traditionally safe-haven US Dollar.

German Economic Data Offers Mixed Signals

Fresh economic reports from Germany provided investors with additional insights into the health of the Eurozone’s largest economy.

Industrial Production in Germany showed a modest improvement in April, rising by 0.4%. The figure matched market expectations and followed a revised decline of 0.1% in March. Earlier data had also shown a larger contraction of 0.5% in February, making the latest increase a welcome sign of stabilization in the manufacturing sector.

However, Germany’s trade figures painted a slightly less encouraging picture. The country recorded a trade surplus of €14.5 billion in April, lower than the €14.7 billion reported in March. The result also came in below analysts’ expectations of €15 billion.

While the industrial output data suggested some resilience in economic activity, the softer trade balance indicated that challenges remain for Germany’s export-driven economy.

ECB Rate Increase Remains the Main Focus

A major driver behind the Euro’s recent strength is the growing belief that the ECB will raise interest rates at its policy meeting later this week.

Market participants widely expect the central bank to increase its deposit rate by 25 basis points, taking it to 2.25%. Policymakers continue to face pressure from elevated inflation levels across the Eurozone, making further policy tightening likely.

Why Investors Expect a Cautious Approach

Although a rate increase is largely anticipated, many analysts believe the ECB may signal a more cautious stance for future meetings.

Economic growth across the Eurozone has remained relatively weak, and concerns about slowing business activity continue to influence policy discussions. Because of these growth challenges, investors expect the ECB to avoid committing to a series of aggressive rate hikes after this week’s decision.

As a result, traders will pay close attention not only to the rate announcement itself but also to any guidance regarding the central bank’s future plans.

Improving Global Sentiment Reduces Dollar Demand

Another factor helping the Euro is the improvement in overall market sentiment.

The US Dollar often benefits during periods of uncertainty because investors view it as a safe place to store capital. When confidence improves and risk appetite increases, demand for the Dollar can weaken as investors move toward assets perceived as offering higher returns.

Recent geopolitical developments contributed to a modest improvement in investor confidence.

Middle East Developments Remain in Focus

Tensions in the Middle East continue to attract significant attention from financial markets.

Reports indicated that an Israeli strike on the Lebanese city of Tyre resulted in multiple fatalities despite calls from US President Donald Trump for Israeli Prime Minister Benjamin Netanyahu to halt military actions.

At the same time, Trump expressed optimism about the possibility of reaching an agreement with Tehran. These comments helped support hopes that diplomatic progress could reduce regional tensions over time.

While the situation remains uncertain, the possibility of improved relations has encouraged a moderate risk-on environment across financial markets, reducing some of the demand for safe-haven assets such as the US Dollar.

Federal Reserve Expectations Limit Dollar Weakness

Despite the Euro’s recent gains, losses for the US Dollar have remained relatively limited.

Strong US economic data released last week reinforced expectations that the Federal Reserve could maintain a firm stance on monetary policy. Investors believe that resilient economic performance may give policymakers room to keep interest rates elevated or even consider additional tightening if inflation remains stubbornly high.

This outlook continues to provide underlying support for the Dollar, preventing a deeper decline against major currencies.

Attention Turns to US Inflation Data

The next major event for currency markets is the release of the US Consumer Price Index (CPI) report.

Inflation data is closely monitored because it plays a key role in shaping Federal Reserve policy decisions. A stronger-than-expected reading could reinforce expectations for tighter monetary policy, potentially supporting the Dollar. Conversely, signs of easing inflation could reduce pressure on the Fed to maintain a restrictive stance.

As a result, traders are likely to remain cautious until the inflation figures provide a clearer picture of the direction of US monetary policy.

What Traders Are Watching Next

Several important developments are expected to influence EUR/USD in the coming days:

- The ECB’s interest rate decision and policy guidance.

- Updates on inflation trends across Europe and the United States.

- Geopolitical developments in the Middle East.

- The latest US CPI report and its implications for Federal Reserve policy.

- Broader shifts in investor sentiment and risk appetite.

With both central banks remaining in focus and geopolitical risks still present, volatility in the currency market could remain elevated.

Summary

The Euro continued to recover against the US Dollar, supported by expectations of an ECB interest rate increase and improving market sentiment. Economic data from Germany delivered mixed results, but investors remained focused on the upcoming ECB meeting and its policy outlook. Meanwhile, optimism surrounding diplomatic efforts in the Middle East reduced demand for the safe-haven Dollar. However, strong US economic data and expectations for continued Federal Reserve policy firmness helped limit the Dollar’s losses. The upcoming US inflation report and ECB decision are expected to play a major role in determining the next direction for EUR/USD.

GBPUSD Climbs as Softening US Dollar Boosts Pound Despite UK Economic Concerns

The GBP/USD currency pair climbed toward the 1.3390 level on Tuesday, gaining momentum as the US Dollar weakened following signs of reduced geopolitical tensions in the Middle East. While the British Pound benefited from the softer Dollar, several economic and political concerns in the United Kingdom continued to limit stronger gains.

GBPUSD is moving in an ascending triangle pattern, and the market has rebounded from the higher low area of the pattern

Investors are also closely monitoring changing expectations for Bank of England policy, with markets now anticipating a possible interest rate increase before the end of the year. At the same time, upcoming economic data from both the UK and the United States could play a major role in determining the pair’s next direction.

Weaker US Dollar Lifts GBP/USD

One of the main drivers behind Tuesday’s move was a decline in demand for the US Dollar. The Greenback came under pressure after reports confirmed that direct attacks between Israel and Iran had stopped, easing fears of a broader regional conflict.

During periods of global uncertainty, investors often move money into assets considered safer, including the US Dollar. However, when geopolitical risks begin to fade, demand for these safe-haven assets typically decreases. As a result, the Dollar lost some of its recent strength, helping GBP/USD move higher.

The calmer geopolitical environment encouraged investors to take on more risk, benefiting currencies such as the British Pound and contributing to the pair’s upward movement.

Bank of England Rate Expectations Have Shifted Dramatically

Another important factor influencing the Pound is the significant change in market expectations regarding Bank of England interest rates.

Earlier this year, many investors expected the central bank to cut interest rates twice as economic growth concerns weighed on the outlook. However, the situation has changed considerably. Markets are now pricing in the possibility of a 25-basis-point rate increase before the end of the year.

In theory, expectations of higher interest rates often support a currency because they can attract foreign investment seeking better returns. This shift would normally be viewed as positive for the Pound.

However, the reaction in currency markets has been relatively restrained, suggesting that investors remain cautious about the broader economic picture.

Inflation Concerns Are Driving the Hawkish Outlook

The reason behind the change in rate expectations is particularly important.

Rather than reflecting stronger economic growth, the possibility of higher interest rates is largely linked to ongoing inflation concerns. Rising energy costs and persistent price pressures continue to challenge policymakers.

This creates a difficult situation for the Bank of England. On one hand, higher inflation may require tighter monetary policy. On the other hand, raising borrowing costs could put additional pressure on an economy that is already showing signs of weakness.

As a result, investors are not viewing potential rate hikes as an entirely positive development. Instead, they are concerned that tighter policy could arrive during a period of sluggish economic activity.

Growth Risks Continue to Weigh on the Pound

Despite the recent support from a weaker US Dollar, concerns about the UK economy remain a major obstacle for the British currency.

Several analysts believe that the UK faces the risk of slow economic growth combined with persistent inflation pressures. This combination is often viewed as a challenging environment for both policymakers and investors.

Financial institution BBH has highlighted that the Pound could remain vulnerable against the US Dollar despite higher rate expectations. According to its assessment, increasing interest rates in an economy facing stagnation and inflation does not automatically create a strong bullish case for the currency.

While tighter monetary policy may help prevent significant declines in the Pound, it may not be enough to generate sustained strength if economic growth continues to disappoint.

Political Uncertainty Adds Another Layer of Pressure

Beyond economic concerns, political developments in the UK are also influencing investor sentiment.

Prime Minister Keir Starmer has faced growing pressure after a series of government resignations weakened confidence in the administration. Political uncertainty often creates hesitation among investors, as it can make future policy decisions less predictable.

When political stability comes into question, investors may become more cautious about holding a country’s assets or currency. This appears to be one of the reasons why the Pound has struggled to make stronger gains despite the shift toward a more hawkish interest rate outlook.

The combination of political uncertainty and economic challenges has encouraged market participants to remain careful when assessing the Pound’s prospects.

Divided Opinions Within the Bank of England

The future direction of monetary policy remains another key area of focus.

Some members of the Bank of England’s Monetary Policy Committee have reportedly expressed support for raising interest rates in the near term. Their concerns are primarily linked to inflation remaining higher than desired.

However, not all policymakers share the same view. Analysts at Société Générale believe that those advocating immediate tightening are likely to remain a minority within the committee.

The bank expects the central bank to proceed carefully and avoid rushing into aggressive policy changes. This suggests that while rate hike expectations have increased, the final decision is far from certain.

As a result, investors continue to evaluate every new piece of economic data and every statement from policymakers for clues about the Bank of England’s next move.

Key Economic Reports Could Determine the Next Move

Attention is now turning toward several important economic releases that could influence both the British Pound and the US Dollar.

In the United Kingdom, investors are awaiting the latest Gross Domestic Product (GDP) figures. The report will provide valuable insight into the health of the economy and help determine whether growth concerns are justified.

Meanwhile, in the United States, inflation data will be closely watched for clues about the Federal Reserve’s future policy decisions. Strong inflation could support expectations for higher US interest rates, while softer data could further weaken the Dollar.

These reports are expected to play a crucial role in shaping market expectations for both central banks and could ultimately determine the next major move in GBP/USD.

Summary

GBP/USD moved higher as easing tensions between Israel and Iran reduced demand for the US Dollar, providing support for the British Pound. At the same time, financial markets have dramatically shifted their expectations for Bank of England policy, with a rate increase now viewed as a possibility before year-end.

Despite this supportive backdrop, the Pound continues to face challenges. Persistent inflation, weak economic growth prospects, political uncertainty, and differing views within the Bank of England are all limiting bullish sentiment. With important UK GDP and US inflation data approaching, investors are preparing for fresh signals that could shape the future path of the GBP/USD pair in the weeks ahead.

USDJPY Remains Resilient as Ceasefire Reduces Market Fear While Japan Defends the Yen

The USD/JPY currency pair remained close to its strongest level since the end of April on Tuesday, trading near the 160.15 mark. While price movement during the session was relatively calm, the pair continued to show resilience, supported by expectations that US interest rates may stay elevated for longer.

USDJPY is moving in an ascending channel, and the market has fallen from the higher high area of the channel

At the same time, several factors are limiting further gains. Improved global sentiment following a ceasefire between Israel and Iran has reduced demand for safe-haven assets, placing some pressure on the US Dollar. Meanwhile, Japanese officials have renewed warnings about excessive currency fluctuations, increasing speculation that authorities could step in if the Yen weakens too much.

Ceasefire Eases Safe-Haven Demand for the US Dollar

Investor sentiment improved after Israel and Iran confirmed a halt to direct military attacks. The move followed diplomatic efforts led by US President Donald Trump, who urged both sides to reduce hostilities.

As concerns over an immediate escalation eased, demand for traditional safe-haven assets weakened. The US Dollar, which often attracts investors during periods of global uncertainty, lost some of its recent support against several major currencies.

This shift in market mood prevented the Dollar from extending its recent gains, even as expectations for restrictive US monetary policy continued to provide a supportive backdrop.

Geopolitical Risks Continue to Influence Markets

Although the ceasefire has brought some relief, tensions in the Middle East remain a major concern for investors.

Reports indicated that Israel ordered evacuations in parts of the Lebanese city of Tyre ahead of additional military operations. According to regional media reports, casualties were recorded following airstrikes in southern Lebanon.

These developments highlight that the broader geopolitical situation remains fragile despite the pause in direct conflict between Israel and Iran. As a result, investors continue to monitor the region closely, and lingering uncertainty is helping prevent a significant decline in the US Dollar.

The ongoing risks also contribute to cautious trading conditions across global financial markets, as traders assess the potential impact of further escalation on economic growth and energy supplies.

Japanese Authorities Step Up Verbal Intervention Warnings

On the Japanese side, the Yen has received support from renewed comments by government officials regarding currency stability.

Japan’s Finance Minister Satsuki Katayama stated that authorities remain prepared to take appropriate measures if foreign exchange movements become excessive. Such remarks are often interpreted by markets as warnings that intervention remains a possibility.

These comments are particularly important because USD/JPY continues to trade above the psychologically significant 160.00 level. Historically, Japanese authorities have shown concern when the Yen weakens rapidly, especially when exchange rate moves are viewed as speculative or disconnected from economic fundamentals.

As a result, traders remain cautious about aggressively pushing the pair higher, fearing that stronger government action could be taken if volatility increases.

Bank of Japan Policy Expectations Support the Yen

Another factor helping the Japanese currency is the growing expectation that the Bank of Japan may continue adjusting its monetary policy in the months ahead.

Investors increasingly believe that the central bank could introduce additional interest rate increases as inflation remains a key focus. Market participants are also watching for signs that the Bank of Japan may further reduce its bond-buying activities as part of its ongoing policy normalization process.

These expectations have provided underlying support for the Yen, even as the currency continues to face challenges from the significant interest rate gap between Japan and the United States.

A gradual tightening approach from the Bank of Japan could help strengthen the domestic currency over time, although the pace and timing of future policy decisions remain uncertain.

Energy Supply Concerns Limit Yen Strength

Despite receiving support from intervention concerns and central bank expectations, the Japanese Yen has struggled to build stronger momentum.

One reason is the continued uncertainty surrounding energy markets. Japan relies heavily on imported energy, making it particularly sensitive to disruptions in global supply chains.

Investors remain concerned about potential risks to shipping routes in the Middle East, especially through the Strait of Hormuz, a critical passage for global oil transportation. Any disruption in this region could lead to higher energy costs and place additional pressure on Japan’s economy.

President Donald Trump recently suggested that an agreement with Iran could be reached within days. He also stated that the Strait of Hormuz would be fully accessible once a deal is finalized. These comments provided some reassurance to markets, although traders remain cautious until concrete progress is confirmed.

Focus Shifts to Key US Inflation Reports

Looking ahead, market attention is increasingly turning toward upcoming US inflation data, which could play a major role in shaping expectations for Federal Reserve policy.

The Consumer Price Index (CPI) report is scheduled for release on Wednesday, followed by the Producer Price Index (PPI) on Thursday. Together, these reports will offer valuable insight into inflation trends across the US economy.

Investors will carefully analyze the data for clues about the Federal Reserve’s next policy steps. Stronger inflation readings could reinforce expectations that interest rates will remain elevated for longer, potentially supporting the US Dollar. On the other hand, softer inflation figures could strengthen hopes for future policy easing and weigh on the currency.

Because monetary policy expectations remain one of the biggest drivers of exchange rate movements, the inflation releases are expected to have a significant impact on the direction of USD/JPY in the coming days.

Summary

USD/JPY remains near its highest level in several weeks as traders weigh competing forces affecting both currencies. Expectations of relatively tight US monetary policy continue to support the pair, but gains are being limited by reduced safe-haven demand for the US Dollar and growing concerns about possible intervention by Japanese authorities.

At the same time, expectations for additional policy tightening by the Bank of Japan are offering support to the Yen, while ongoing geopolitical uncertainties and energy supply concerns continue to influence market sentiment. With crucial US inflation reports approaching, investors are preparing for fresh signals that could determine the next major move for USD/JPY.

EURJPY Moves Higher as Germany’s Manufacturing Recovery Lifts the Euro

The EUR/JPY currency pair continued its upward movement for a second straight session, with the Euro gaining strength against the Japanese Yen. Strong economic data from Germany helped boost confidence in the Euro, while a more stable Japanese Yen limited the pace of further gains.

EURJPY is moving in an ascending channel, and the market has rebounded from the higher low area of the channel

During Tuesday’s Asian trading session, EUR/JPY traded near the 184.90 level, reflecting continued investor optimism toward the Euro following the latest industrial production and trade figures from Germany.

Germany’s Industrial Production Returns to Growth

One of the key factors supporting the Euro was the latest industrial production report from Germany, the largest economy in the Eurozone.

According to data released by Germany’s federal statistics office, Destatis, industrial output increased by 0.4% in April compared to the previous month. The result matched market expectations and marked a recovery from March, when production had declined by 0.1%.

The improvement suggests that Germany’s manufacturing and industrial sectors are showing signs of resilience despite ongoing economic challenges. A return to positive monthly growth is often viewed as an encouraging signal because industrial activity plays a major role in Germany’s overall economic performance.

On a yearly basis, however, industrial production remained lower than the same period last year, falling by 0.5%. While this annual decline indicates that some challenges persist, the monthly rebound offered investors a reason to remain optimistic about the country’s economic outlook.

Trade Figures Paint a Mixed Picture

Germany also released its latest trade balance data, which provided a broader view of economic activity.

The country recorded a trade surplus of €14.5 billion in April, slightly lower than the revised €14.7 billion surplus reported in March. The figure also came in below analysts’ expectations of €15.0 billion.

Although the trade surplus narrowed, the underlying details were more encouraging than the headline number suggested.

Exports Continue to Improve

German exports rose by 0.9% during April, reaching approximately €136.6 billion. This marked the highest export level in nearly three and a half years.

The growth in exports exceeded expectations by a wide margin. Economists had anticipated a decline, but instead, overseas demand for German goods remained strong. The increase also represented an acceleration from March’s modest export growth.

Strong export performance is particularly important for Germany because the country relies heavily on international trade. Higher exports can support business activity, employment, and overall economic growth.

Imports Reach Highest Level Since 2022

Imports also increased during April, climbing 1.2% to €122.1 billion.

While imports grew at a slower pace than in March, they reached their highest level since November 2022. Rising imports can often indicate healthy domestic demand, as businesses and consumers purchase more goods from abroad.

However, imports grew faster than exports during the month, which contributed to the smaller trade surplus.

Overall, the trade report highlighted a dynamic economy where both international demand and domestic consumption remain active, despite some ongoing uncertainties.

Euro Benefits From Improved Economic Sentiment

The combination of stronger industrial production and resilient trade activity helped improve market sentiment toward the Euro.

Investors generally favor currencies backed by economies showing signs of growth and stability. Germany’s latest figures reinforced the view that the Eurozone’s largest economy continues to navigate challenges while maintaining important areas of strength.

As a result, demand for the Euro remained firm, providing support for EUR/JPY and helping the pair extend its recent gains.

Japanese Yen Finds Stability

While the Euro has been benefiting from positive economic news, the Japanese Yen has also shown signs of stabilization.

One important factor has been the recent decline in global oil prices. Lower energy costs have helped ease concerns about a sharp rise in inflation driven by expensive fuel imports.

Japan imports a significant portion of its energy needs, making oil prices an important factor for inflation and economic policy decisions. As energy prices ease, fears of rapidly accelerating inflation have also moderated.

This has reduced market expectations for extremely aggressive monetary tightening, helping the Yen maintain a steadier footing against major currencies.

Bank of Japan Still Expected to Tighten Policy

Despite the recent relief from lower oil prices, the Bank of Japan continues to face inflation-related challenges.

Policymakers remain focused on underlying price pressures that have persisted across the economy. As a result, financial markets still expect the central bank to move toward tighter monetary policy in the near future.

Many investors believe the Bank of Japan could implement further policy adjustments later this month as it seeks to manage inflation while supporting economic stability.

In addition to potential interest rate decisions, attention is also centered on the central bank’s asset purchase program.

Reports suggest that Japanese policymakers may review their bond-buying strategy and could reduce the pace of monthly asset purchases. Such a move would represent another step toward normalizing monetary policy after years of ultra-loose financial conditions.

Investors Watch Key Government Bond Auction

Market participants are now closely monitoring the upcoming 30-year Japanese Government Bond (JGB) auction scheduled for Wednesday.

The auction is expected to provide valuable insight into investor demand for long-term Japanese debt in an environment where yields have been gradually moving higher.

Strong demand could signal confidence in Japan’s financial outlook, while weaker demand might raise questions about market sentiment and future policy adjustments.

The results of the auction may influence expectations surrounding the Bank of Japan’s next moves and could affect the direction of the Japanese Yen in the short term.

Summary

EUR/JPY continued to rise as stronger economic data from Germany boosted confidence in the Euro. Germany’s industrial production returned to growth in April, while exports reached their highest level in several years, highlighting resilience in the country’s economy. Although the trade surplus narrowed, the overall data supported positive sentiment toward the Euro.

At the same time, the Japanese Yen found some stability as falling oil prices eased concerns about inflation-driven policy tightening. However, expectations remain that the Bank of Japan will continue moving toward tighter monetary conditions, including possible adjustments to its bond purchase program. Investors are now turning their attention to the upcoming Japanese government bond auction for further clues about the future path of monetary policy and the Yen.

AUDUSD Gains Momentum as Geopolitical Fears Fade and China Exports Surprise Higher

The Australian Dollar strengthened against the US Dollar on Tuesday, recovering part of the losses it suffered last week. While the currency remains close to its lowest levels in nearly two months, improving global sentiment and stronger-than-expected economic data from China helped boost confidence in the Australian currency.

AUDUSD is moving in a descending channel, and the market has rebounded from the lower low area of the channel

A combination of easing geopolitical concerns in the Middle East and encouraging trade figures from China created a more positive environment for the Australian Dollar, which is often viewed as a currency closely tied to global trade and economic growth.

Relief in Global Markets Lifts Risk Sentiment

One of the key factors supporting the Australian Dollar was the reduction in tensions between Israel and Iran. News that both countries had halted hostilities brought a sense of relief to financial markets that had been concerned about the possibility of a wider regional conflict.

When geopolitical risks rise, investors typically move money into assets considered safer, such as the US Dollar. On the other hand, currencies linked to global growth and commodity demand, including the Australian Dollar, often come under pressure during periods of uncertainty.

The latest developments in the Middle East helped calm investor fears and encouraged a shift back toward risk-sensitive assets. As a result, the Australian Dollar managed to regain some ground against its US counterpart.

Although the rebound was relatively modest, it reflected an improvement in market sentiment after a period of heightened caution.

Strong Chinese Trade Data Provides Additional Support

Another important driver behind the Australian Dollar’s recovery was a surprisingly strong trade report from China.

Official figures released by Chinese authorities showed that the country’s trade surplus expanded significantly in May. The surplus reached $105.43 billion, marking the highest level recorded since January and exceeding expectations from economists.

The latest figure represented a substantial increase from April, when the trade surplus stood at $84.82 billion. The stronger performance suggested that Chinese exports remained resilient despite ongoing challenges in the global economic environment.

For Australia, China’s economic performance is especially important. China is Australia’s largest trading partner and a major buyer of Australian exports, including iron ore, coal, natural gas, and agricultural products.

When Chinese trade activity improves, it often signals stronger demand for raw materials and commodities, which can benefit the Australian economy. This relationship means that positive Chinese economic news frequently provides support for the Australian Dollar.

Why China Matters So Much to Australia

The close economic ties between Australia and China have made Chinese data a major influence on the Australian currency for many years.

Australia supplies a significant amount of the resources that help power China’s industrial sector. As a result, any indication that Chinese manufacturing, exports, or trade activity is strengthening tends to be viewed positively by investors holding Australian assets.

The latest trade numbers suggested that China’s export sector remains active and capable of generating strong revenue despite a complex global backdrop. This has encouraged expectations that demand for Australian exports could remain stable, offering a supportive outlook for Australia’s trade sector.

Investors often monitor Chinese economic releases carefully because they can provide early clues about broader trends in commodity demand and regional economic growth.

Australian Dollar Still Faces Challenges

Despite Tuesday’s gains, the Australian Dollar remains under pressure compared with levels seen earlier in the year.

The currency is still trading near its weakest point in approximately eight weeks, highlighting the challenges it has faced recently. Global uncertainty, shifting expectations for interest rates, and periods of strong demand for the US Dollar have all weighed on the Australian currency.

While the latest rebound reflects improving sentiment, market participants remain cautious about the broader economic outlook. Factors such as global growth prospects, trade developments, and central bank policies continue to play a significant role in shaping currency movements.

For now, investors appear encouraged by the combination of reduced geopolitical risks and stronger economic signals from China, but they are also keeping a close watch on future developments that could influence market direction.

Focus Turns to Upcoming Economic Developments

Looking ahead, traders and investors will continue monitoring economic data from both China and Australia for signs of sustained strength.

Chinese trade performance will remain a key area of interest because of its direct impact on Australian exports. Additional evidence of stable demand from China could help maintain support for the Australian Dollar in the weeks ahead.

At the same time, broader global developments, including geopolitical events and economic indicators from major economies, are likely to influence investor sentiment and currency markets.

The Australian Dollar’s recent recovery demonstrates how quickly market attitudes can change when uncertainty eases and economic data exceeds expectations.

Summary

The Australian Dollar moved higher against the US Dollar on Tuesday, benefiting from two major developments. First, news that Israel and Iran had stopped hostilities helped reduce geopolitical concerns and improved investor confidence. Second, China reported a much stronger-than-expected trade surplus for May, highlighting resilience in the world’s second-largest economy.

Because China is Australia’s most important trading partner, stronger Chinese trade data often supports the Australian economy and its currency. While the Australian Dollar remains near multi-week lows, the combination of easing global tensions and encouraging economic data has provided a welcome boost and renewed optimism in the market.