AUD: RBA Minutes: No Interest Rate Rise Considered

The RBA Meeting minutes happened today, outcome is no rate hike or cut in near term. It is difficult situation for taking one decision in monetary policy settings, Inflation is slight higher, it will come down once productivity increased, then Labour unit cost get down, really House hold suffered from higher rates. Consumption is lower due to higher inflation, it will be arrested soon by our policy settings.

The Reserve Bank of Australia (RBA) released the detailed Minutes of its March monetary policy meeting on Tuesday, revealing that the Board members opted not to entertain the possibility of increasing interest rates. Further insights from the RBA Minutes indicate a nuanced perspective on potential future adjustments to the cash rate.

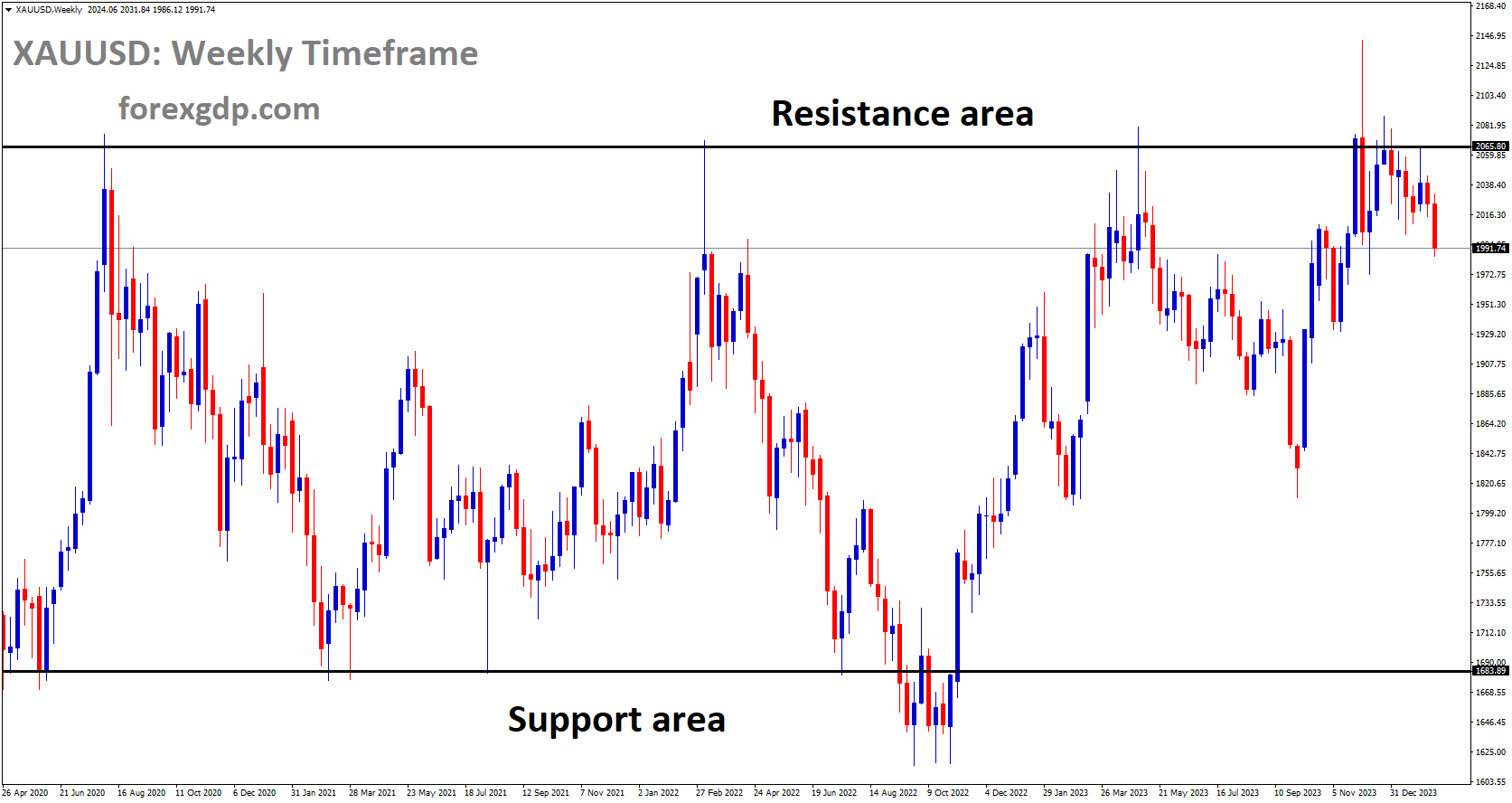

AUDUSD is moving in Descending channel and market has rebounded from the lower low area of the channel

Key Highlights:

– The minutes conspicuously lacked any mention of the board contemplating the prospect of raising rates.

– The Board reached a consensus that assessing forthcoming changes to the cash rate presented considerable challenges.

– Despite an uncertain economic outlook, risks appeared to be evenly distributed.

– The Board acknowledged that it would require a significant amount of time before they could confidently anticipate a return of inflation to the target level.

– While inflation rates were elevated, there were no immediate signs of upward pressure, with consumer spending notably subdued.

– Despite inflation trending gradually towards the target, there was evidence of a softening labor market.

– The gap between demand and supply in the economy was noted to be narrowing swiftly.

– The Board assessed that demand would likely outpace supply for the foreseeable future, leading to a marginally tighter labor market.

– Although wage growth may have peaked, a rapid decline was not anticipated.

– A recovery in productivity was deemed necessary to counterbalance the persistently high unit labor costs.

– Overall, financial conditions were observed to be restrictive, particularly impacting households.

AUD: RBA Meeting Minutes: No Further Rate Hikes Discussed

The RBA Meeting minutes happened today, outcome is no rate hike or cut in near term. It is difficult situation for taking one decision in monetary policy settings, Inflation is slight higher, it will come down once productivity increased, then Labour unit cost get down, really House hold suffered from higher rates. Consumption is lower due to higher inflation, it will be arrested soon by our policy settings.

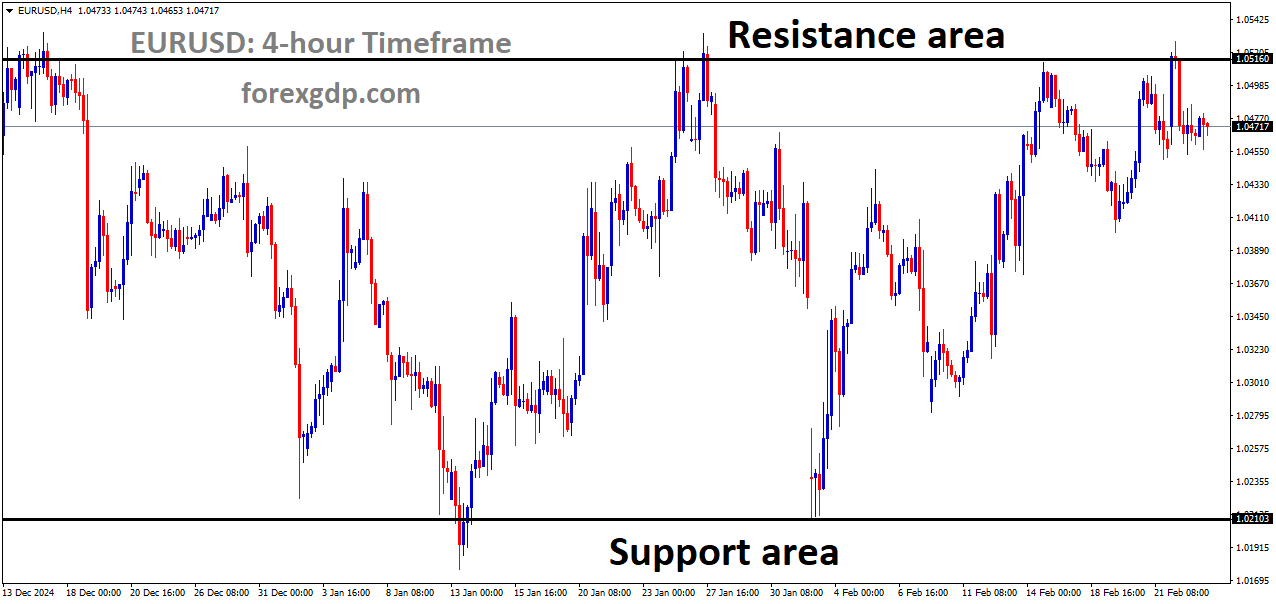

GBPAUD is moving in the Symmetrical triangle pattern and the market has reached the top area of the pattern

The latest decision by the Reserve Bank board, as revealed in the minutes of its March 18-19 meeting, indicated a departure from considering an additional increase to interest rates. Instead, the board opted to maintain the cash rate at 4.35 per cent, marking a shift from its previous stance of contemplating rate hikes at every meeting since May 2022, during which the bank implemented a series of 13 rate increases.

The minutes highlighted that the risks to the economic outlook had become more balanced, leading to a characterization of the policy outlook as one where predicting future changes in the cash rate target was challenging. While many economists and investors anticipate a rate cut as the next move, with markets fully pricing in a 25 basis point easing at the RBA’s September 23-24 meeting, the board noted that inflation had continued to moderate, albeit with services inflation remaining high and some temporary factors influencing recent trends.

Despite the board’s priority of bringing inflation back within the 2 to 3 per cent target band by December 2025, they acknowledged the complexities of this task, drawing lessons from the experiences of other countries in managing disinflationary pressures. Preserving gains in the labor market was deemed important, with the board agreeing that maintaining the current cash rate was the optimal strategy to support the gradual return of inflation to target and the labor market to full employment.

Notably, the minutes conveyed a shift towards a more dovish stance, signaling increased confidence in addressing inflation concerns. However, analysts such as Commonwealth Bank’s Gareth Aird suggested that while the board may lean towards future rate cuts, it is premature to adopt an easing bias. Similarly, Marcel Thieliant from Capital Economics indicated that rate cuts might not materialize until later in the year, citing historical precedents where the RBA deliberated on rate cuts over several months before implementation.

The minutes also shed light on the financial strain experienced by households under the backdrop of “restrictive” financial conditions, with rising scheduled household debt payments and challenges in meeting essential expenses. Despite this, defaults remained low, and banks had revised their forecasts of potential loan losses downwards.

In response to the minutes, Treasurer Jim Chalmers welcomed the relief they could bring to household borrowers, emphasizing the six-month gap since the last interest rate increase and its potential to alleviate financial pressure for homeowners and mortgagees.

Looking ahead, the RBA is scheduled to convene again on May 6-7, with expectations leaning towards maintaining interest rates at current levels.

AUD: RBA Monetary Policy Meeting Minutes

The RBA Meeting minutes happened today, outcome is no rate hike or cut in near term. It is difficult situation for taking one decision in monetary policy settings, Inflation is slight higher, it will come down once productivity increased, then Labour unit cost get down, really House hold suffered from higher rates. Consumption is lower due to higher inflation; it will be arrested soon by our policy settings.

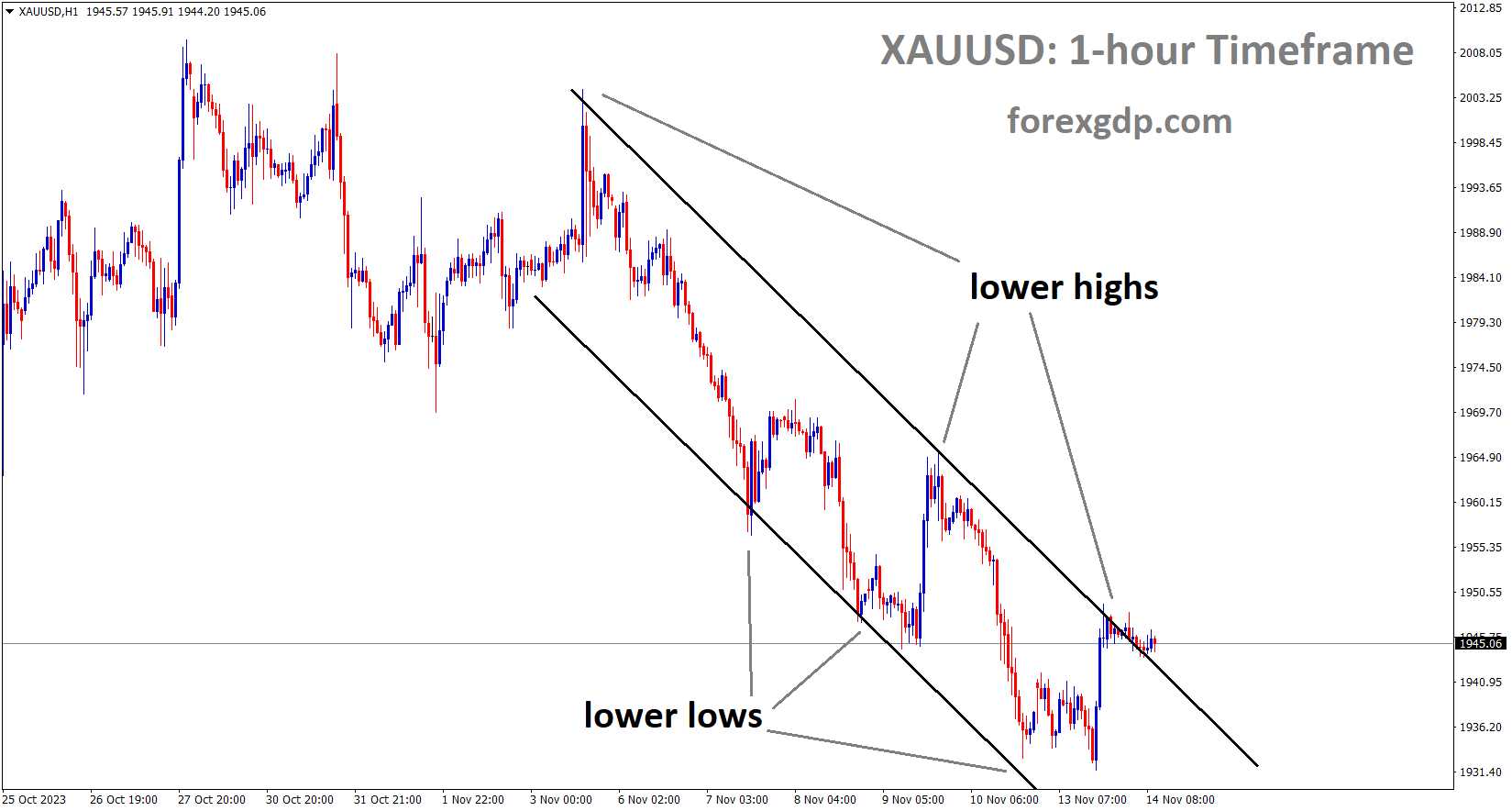

AUDUSD has broken Ascending channel in downside

Assessment of Domestic Economic Conditions:

Members of the Reserve Bank began their discussion by evaluating recent data regarding output growth in the domestic economy. They noted a further deceleration in growth during the December quarter, aligning with expectations. Throughout 2023, aggregate demand received support from robust growth in business investment and public spending. However, concerns arose regarding weak household consumption growth, especially on a per capita basis, attributed to factors such as high inflation, rising interest rates, and increased tax payments, which compressed real incomes. Nevertheless, members observed a positive trend in real household disposable income, anticipated to strengthen further as the impact of high inflation subsides and pre-announced tax cuts take effect. Members engaged in a thorough discussion on various factors influencing the likelihood of an upturn in consumption growth.

Housing Market Dynamics:

Regarding the housing market, members noted brisk demand surpassing supply, contributing to escalating prices and rents. Factors such as sustained population growth and lingering preferences for spacious housing, stemming from the pandemic, continued to exert pressure despite worsening affordability. Supply-side constraints persisted due to ongoing capacity limitations, particularly in finishing trades, alongside substantial increases in construction costs. Advertised rents surged notably across most capital cities.

Labor Market Conditions:

Labor market conditions underwent further moderation owing to slower output growth, resulting in a slackening in labor demand. Indicators such as a rise in the unemployment rate in January underscored this trend. Despite this, overall labor market conditions remained relatively tight, albeit slightly below levels consistent with sustained full employment and target inflation.

Wages and Productivity:

Wage growth exhibited resilience in the December quarter, with signs indicating a potential peak in wages growth. However, the decline was not expected to be immediate. Members highlighted persistent high labor costs per unit of output, although a slight moderation was evident due to improved productivity growth in the latter half of 2023. Yet, uncertainties lingered regarding the sustainability of this trend, with structural factors potentially impeding productivity growth.

Inflationary Trends:

Underlying inflation persisted at elevated levels, albeit moderating in line with forecasts. Notably, while monthly inflation slowed, high services inflation endured. Members anticipated a rebound in inflation in subsequent quarters, considering transient factors such as fuel price declines and legislative expiration of electricity rebates. Overall, data indicated ongoing, albeit diminishing, excess demand and robust domestic cost pressures.

Assessment of International Economic Developments:

Members noted a trend of inflation moderation in advanced economies, nearing central banks’ targets. However, disparities persisted across components, with housing and core services inflation remaining elevated. Notably, the United States witnessed a modest inflation uptick in recent data. Concerns were raised regarding persistent non-tradables inflationary pressures in some economies.

Financial Conditions:

Market expectations regarding central bank policy rates in advanced economies slightly rose, reflecting stronger-than-anticipated economic data. Members highlighted a diverse outlook, with Japan expected to diverge from other economies. Despite global stability, risks persisted, necessitating ongoing vigilance.

Assessment of Financial Stability:

Discussion centered on the resilience of the global financial system amid high inflation and tight monetary policies. While pressures existed, particularly concerning the Chinese property sector and commercial real estate markets, most Australian households and businesses maintained robust financial positions, mitigating immediate systemic risks.

Monetary Policy Considerations:

Given the data’s alignment with expectations, the Board decided to maintain the cash rate target at 4.35 percent and the interest rate on Exchange Settlement balances at 4.25 percent. Emphasizing a commitment to returning inflation to target, members acknowledged the complexities in predicting future rate adjustments, underscoring the need for ongoing monitoring of economic developments.

Conclusion:

The decision reflected the Board’s view that recent data did not substantially alter the economic outlook. Acknowledging significant uncertainties, members maintained a balanced stance on future rate adjustments, emphasizing adaptability to evolving economic conditions.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/