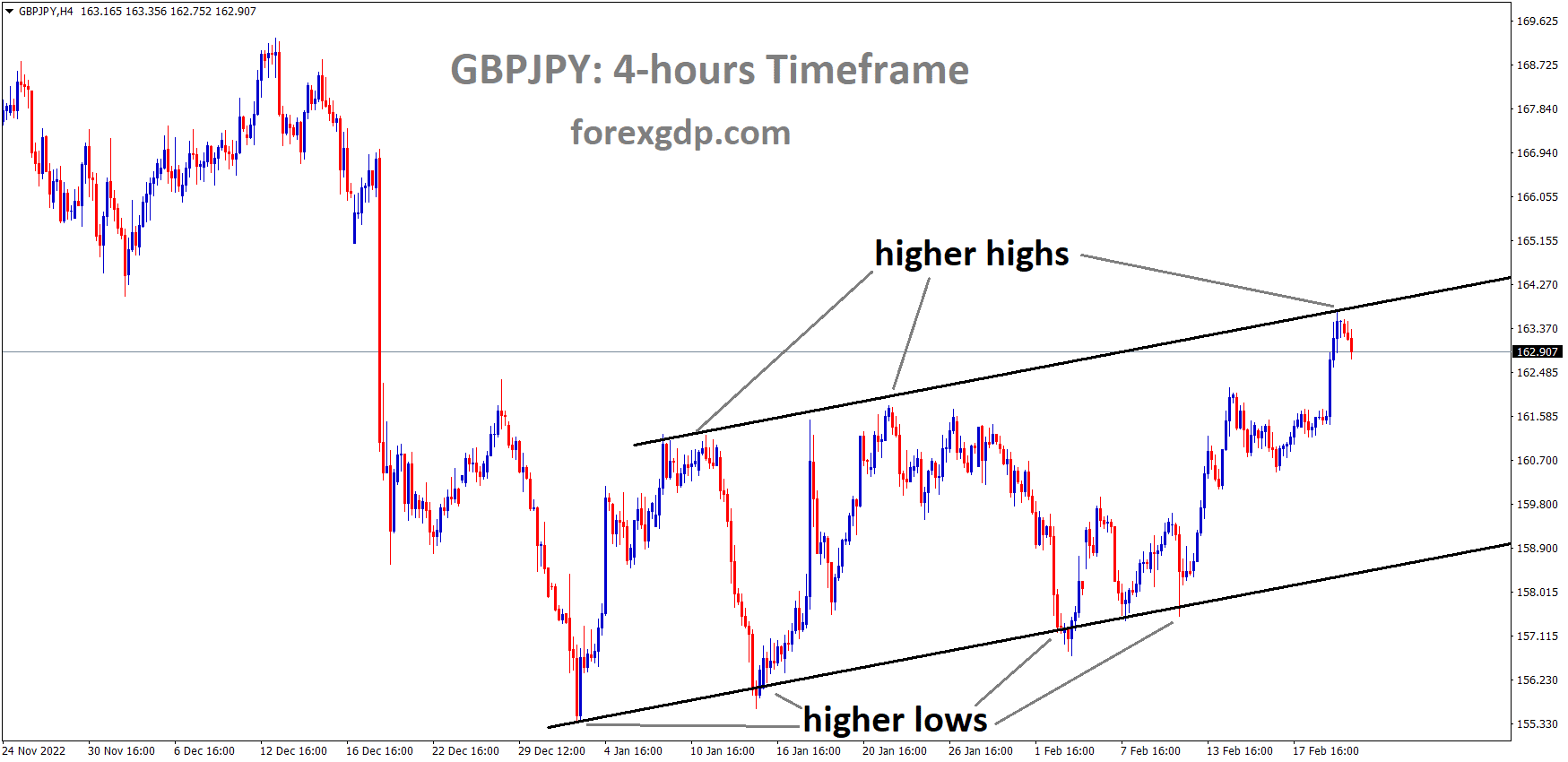

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

The global slowdown and recession have had a greater impact on Japan’s manufacturing sector, resulting in reduced production levels. The Tankan Manufacturing Index for the current period was recorded at -5.0, compared to the previous month’s -6.0, indicating a slightly better situation. On the other hand, the Non-Manufacturing Index for the current period was recorded at 17.0, down from the previous period’s 20.0, indicating a slight decline in the non-manufacturing sector.

The latest monthly Reuters Tankan survey revealed that Japan’s manufacturers are feeling pessimistic due to the global slowdown. The survey, which closely tracks the Bank of Japan’s quarterly tankan survey, was conducted from February 8 to 17 and canvassed 493 big non-financial Japanese firms, of which 244 replied, according to Reuters.

The survey results come after the manufacturing and services gauges both declined in the previous two months. In February, the Reuters Tankan Manufacturing Index for Japan was -5.0, an improvement from January’s -6.0. Similarly, the Tankan Non-Manufacturing Index eased to 17 for the same month, down from 20.0 in the previous period.

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel.

According to US Secretary of State Anthony Blinken, both the West and China have indirectly supported Russia’s military campaign against Ukraine, leading to heightened geopolitical tensions. As a result, the price of gold has become more volatile, with the upcoming release of the FOMC meeting minutes expected to have a significant impact on gold prices.

During early trading on Wednesday, the price of gold (XAU/USD) remains in a trading range of about $30.00 within the past week and is currently hovering around $1,835. The Federal Open Market Committee’s (FOMC) Monetary Policy Meeting Minutes are eagerly awaited by traders, and geopolitical fears, along with a lackluster US Dollar movement near a multi-day top, are affecting XAU/USD trading.

The preliminary US S&P Global PMIs for February have boosted the US Dollar Index’s strength, along with hawkish Fed bets, and restricted XAU/USD momentum lately. However, the lack of significant movement in the US Treasury bond yields around the three-month high previously set seems to have limited the Gold traders’ reactions. Additionally, the hawkish bias surrounding the US Federal Reserve (Fed) and looming policy pivot chatters will likely affect Gold traders.

SILVER Analysis

XAGUSD Silver Price has broken the Descending channel in upside and the market is moving in an minor Ascending channel and the market has reached the higher low area of the channel.

US Secretary of State Antony Blinken and Russian President Vladimir Putin’s recent comments, suggesting increased tension between Moscow and Kyiv, which also includes indirect participation of the West and China, have impacted market sentiment and the Gold price. However, an absence of major updates in Asia has eased the risk-off mood.

Although the US 10-year and two-year treasury bond yields are fluctuating near three-month highs, and the S&P 500 Futures is experiencing mild gains, Wall Street’s negative closing might limit the upside potential of XAU/USD.

Looking ahead, XAU/USD could remain uncertain and cautious as traders await the FOMC Minutes. The signals for a Fed policy pivot may encourage Gold buyers, but the mixed mood could keep the price of gold on a volatile floor.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

On Tuesday, the DXY index, which measures the US dollar, increased moderately and remained near a six-week high due to risk-off sentiment and rising U.S. Treasury yields. Traders had previously thought that the Fed would pause its hiking cycle in the first quarter and start cutting rates later in the year, but this changed due to strong employment numbers and sticky CPI data.

The US labor market proved to be more resilient than expected, which increased the risk of wage pressures remaining skewed to the upside. Meanwhile, the inflation outlook has become less favorable than projected, particularly with stubbornly high prices in the services sector. As a result, the Fed may have no choice but to continue raising interest rates in the coming months, making it unlikely for a monetary policy pivot soon.

USDCAD Analysis

USDCAD is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern.

The Canadian Dollar weakened against its counterparts yesterday, following a mixed bag of economic data. The Canadian Consumer Price Index (CPI) dropped to 5.9%, while the Canadian Retail Sales data came in at 5.0%. Additionally, the backdrop of the CAD was affected by a drop in oil prices to $75, as Canada is the largest exporter of oil items to the US. A decrease in oil prices typically shows weakness in the CAD.

The USD/CAD pair went through an inventory adjustment process near the 1.3550 resistance level during the Asian session. As the Federal Reserve (Fed) is expected to raise rates and oil prices continue to decline, the Loonie asset is anticipated to surpass the resistance level. In the Tokyo session, S&P500 futures display gains after a bearish Tuesday, thanks to positive United States S&P PMI data, which has increased hawkish Fed bets. Despite a general risk-off mood, there is a minor sense of optimism, and investors should not build aggressive long positions in perceived-risk assets.

Due to the risk aversion theme, the US Dollar Index (DXY) is expected to break through the 103.90 resistance level. The upbeat US PMI data indicates strong consumer spending, supporting further policy tightening by Fed Chair Jerome Powell. Although many signs suggest more restrictions on monetary policy, investors await further guidance from the Federal Open Market Committee (FOMC) minutes.

On Tuesday, the Canadian Dollar was active following the release of the Consumer Price Index (CPI) and Retail Sales data. The headline and core CPI figures were lower than their estimates at 5.9% and 5.0%, respectively, suggesting that the Bank of Canada’s (BoC) higher interest rates are effectively curbing inflation. BoC Governor Tiff Macklem has paused policy tightening for now, stating that the current monetary policy is restrictive enough to control inflation.

In contrast to the CPI, monthly Retail Sales (Dec) data increased by 0.5%, higher than the consensus estimate of 0.2%. Increased consumer spending could counteract the softening price pressures. Oil prices are declining towards $75.50 as the demand recovery in China falls short of expectations. It should be noted that Canada is a significant oil exporter to the United States, and lower oil prices could weaken the Canadian Dollar.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

If the inflation report indicates higher inflation, the ECB may increase the rate hike this month. However, the manufacturing sector continues to be sluggish, possibly due to the lagging effects of ECB monetary policy settings. Yesterday, Russia announced the suspension of the START treaty, which could have an impact on both the Euro and the US Dollar.

Commerzbank economists predict that the Eurozone’s January inflation data may slightly support the Euro, but the lower end of the Euro is likely to remain weak. Although ECB officials have recently expressed a restrictive tone, higher inflation results could increase rate expectations for the Eurozone and provide short-term support for the Euro. However, yesterday’s PMIs for the Eurozone’s manufacturing sector showed a potential slowdown due to concerns that the ECB’s monetary policy may be hindering the industry.

This development may pressure the Euro further down. Additionally, the increasing tension between the US and Russia, following Russia’s announcement of the suspension of the nuclear disarmament (START) treaty, may also impact the Euro. It is important to monitor this situation as it could impact the Euro’s performance.

GBPUSD Analysis

GBPUSD is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern.

According to Northern Ireland leader Jeffrey Donaldson, UK Prime Minister Rishi Sunak is scheduled to hold discussions with the European Union to resolve the issue of the Northern Ireland Protocol and make arrangements for border issues. Meanwhile, positive UK domestic data released yesterday has strengthened the Pound against its counterparts.

UK S&P Global/CIPS data for February showed that the Manufacturing PMI rose to 49.2, while the Services PMI jumped to a seven-month high of 53.3.

Furthermore, Brexit concerns continue to loom as the Eurosceptic Conservatives challenge UK Prime Minister’s talks with the European Union (EU) over the Northern Ireland (NI) border issue

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has reached the higher high area of the channel.

Today, the RBNZ increased the interest rate to 50 bps, causing the NZD Dollar to rise. The NZ Prime Minister, Chris Hipkins, stated that cyclones hitting New Zealand are the most significant natural disasters in a decade. Inflation in NZ is at 7.2%, which is above the RBNZ’s target range of 1-3%. Unemployment levels are at multi-year lows, currently at 3.4%. The RBNZ also mentioned that increased immigration and labor pressures could contribute to further inflationary pressures.

The recent cyclone Gabrielle has caused widespread damage, and Prime Minister Chris Hipkins has described it as the most damaging natural disaster in at least a generation. Despite this, the RBNZ remains committed to reducing price pressures. Inflation in NZ stands at 7.2%, which is above the RBNZ’s target band of 1-3%. In the post-decision press conference, RBNZ Governor Adrian Orr stated that the bank sees the impact of the severe weather event as adding to inflation, and they anticipate that the rebuild will add 1% to GDP over the coming years.

The RBNZ is concerned about labor pressures, as the tight labor market is above the RBNZ’s own measure of the maximum sustainable level of employment. The unemployment rate is at multi-generational lows of 3.4%. While the RBNZ believes that increased immigration may alleviate some labor pressures, it may also lead to broad-based inflationary pressures.

Finally, the RBNZ has been proactive in dealing with the pandemic, being one of the first central banks to cut rates at the beginning of the pandemic and among the leaders in hiking to combat inflation. Despite this, the S&P/NZX 50 equity index in New Zealand has continued to decline following losses seen earlier this week.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has reached the lower low area of the channel.

The Swiss Franc did not experience a boost despite comments from SNB Vice Chairman Martin Schlegel stating that the central bank is still actively intervening in currency markets to achieve the goal of price stability for the Swiss Franc.

The preliminary United States S&P PMI data for February indicates expansionary economic activity, likely due to an increase in consumer spending. This has caused a decline in risk-perceived assets, supporting a hawkish stance from the Federal Reserve (Fed).

Although S&P500 futures show slight gains in the early Tokyo session, the overall sentiment remains risk-off. The US Dollar Index (DXY) is finding it difficult to extend gains above 103.90, but it is likely to rise due to the high volatility expected in the FX market before the release of the Federal Open Market Committee (FOMC) minutes. The increasing possibility of the Fed announcing more rate hikes at its March monetary policy meeting is boosting US treasury yields, with the return on 10-year bonds nearing 4%.

Regarding the Swiss Franc, comments from Swiss National Bank (SNB) Vice Chairman Martin Schlegel failed to strengthen the currency. Schlegel stated that the SNB is “still willing” to intervene in foreign currency markets to achieve price stability.

AUDNZD Analysis

AUDNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The Australian Dollar continues to weaken against the US Dollar as the Federal Reserve’s plan for rate hikes in March and May by 25 basis points is causing the US Dollar to dominate. Fed Chair Powell has already stated that inflation needs to be controlled before rate hikes can be considered. Weaker-than-expected domestic data in Australia is also contributing to the AUD’s weakness. With the FOMC meeting minutes scheduled for today, the path for both the USD and AUD is becoming clearer.

The Reserve Bank of New Zealand has increased the official cash rate target by 50 basis points to 4.75% from 4.25%, causing the New Zealand Dollar to surge. This move was anticipated and less than the previous increase of 75 bp in November. The OIS market had priced in 45 bp prior to the decision, and most economists surveyed by Bloomberg had forecast a 50 bp increase. The RBNZ believes that the cash rate will peak at 5.5%, while the OIS market predicts a peak of around 5.40% later this year.

Moreover, several FOMC members, including Fed Chair Jerome Powell, recently emphasized the need to raise rates gradually to gain control of inflation. The release of the latest FOMC monetary policy meeting minutes, later during the US session, will provide investors with clues about the Fed’s rate-hiking path and drive the USD’s direction, which will, in turn, impact the AUD/USD pair. In addition, looming recession risks, along with geopolitical tensions, have contributed to a bearish outlook for the AUD/USD pair as the market continues to favor the safe-haven buck. In light of the fundamental backdrop, the major’s path of least resistance is to the downside.

Don’t trade all the time, trade forex only at the confirmed trade setups.

🎁 80% NEW YEAR OFFER for forex signals. LIMITED TIME ONLY Get now: forexgdp.com/offer/