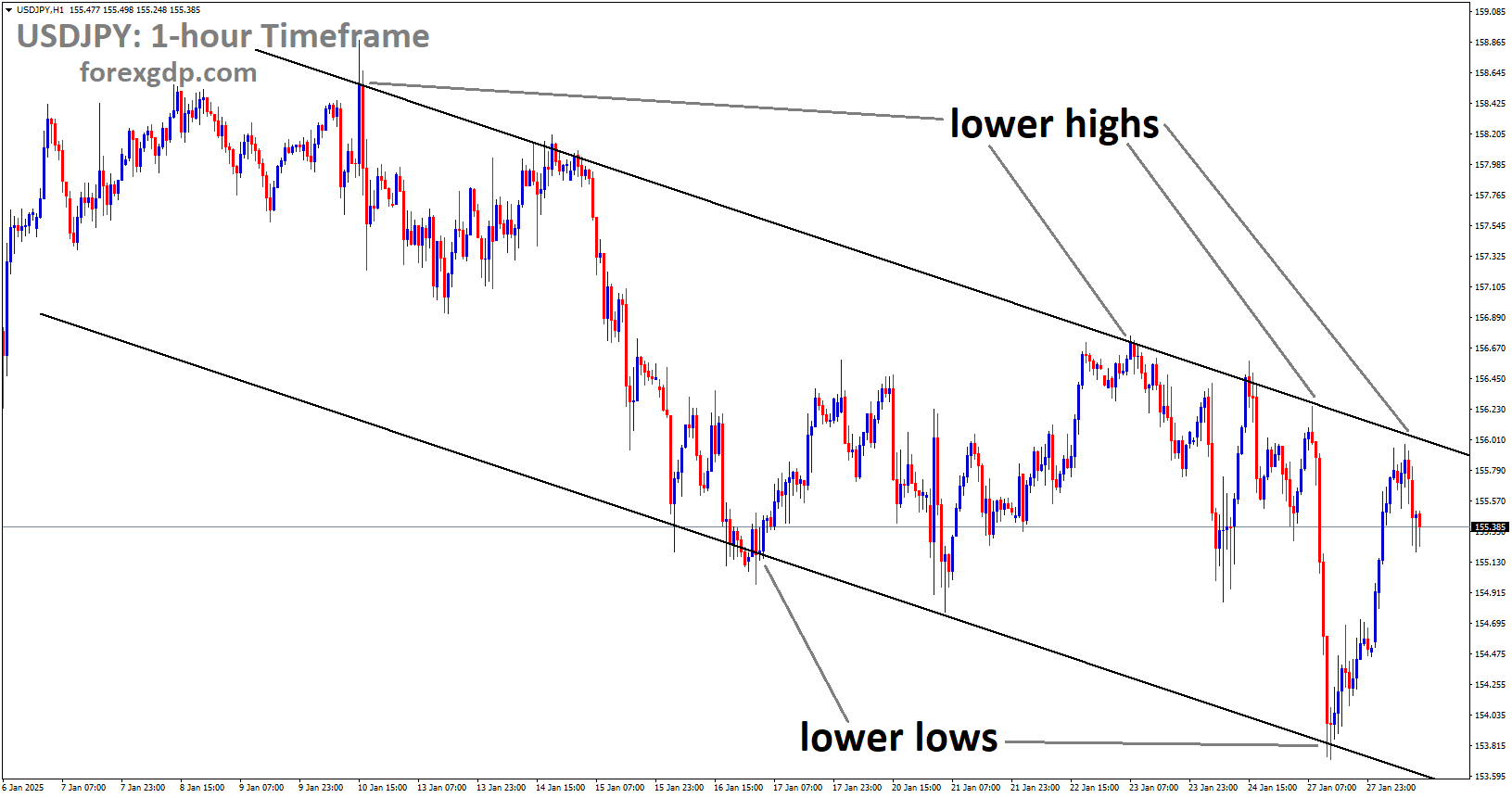

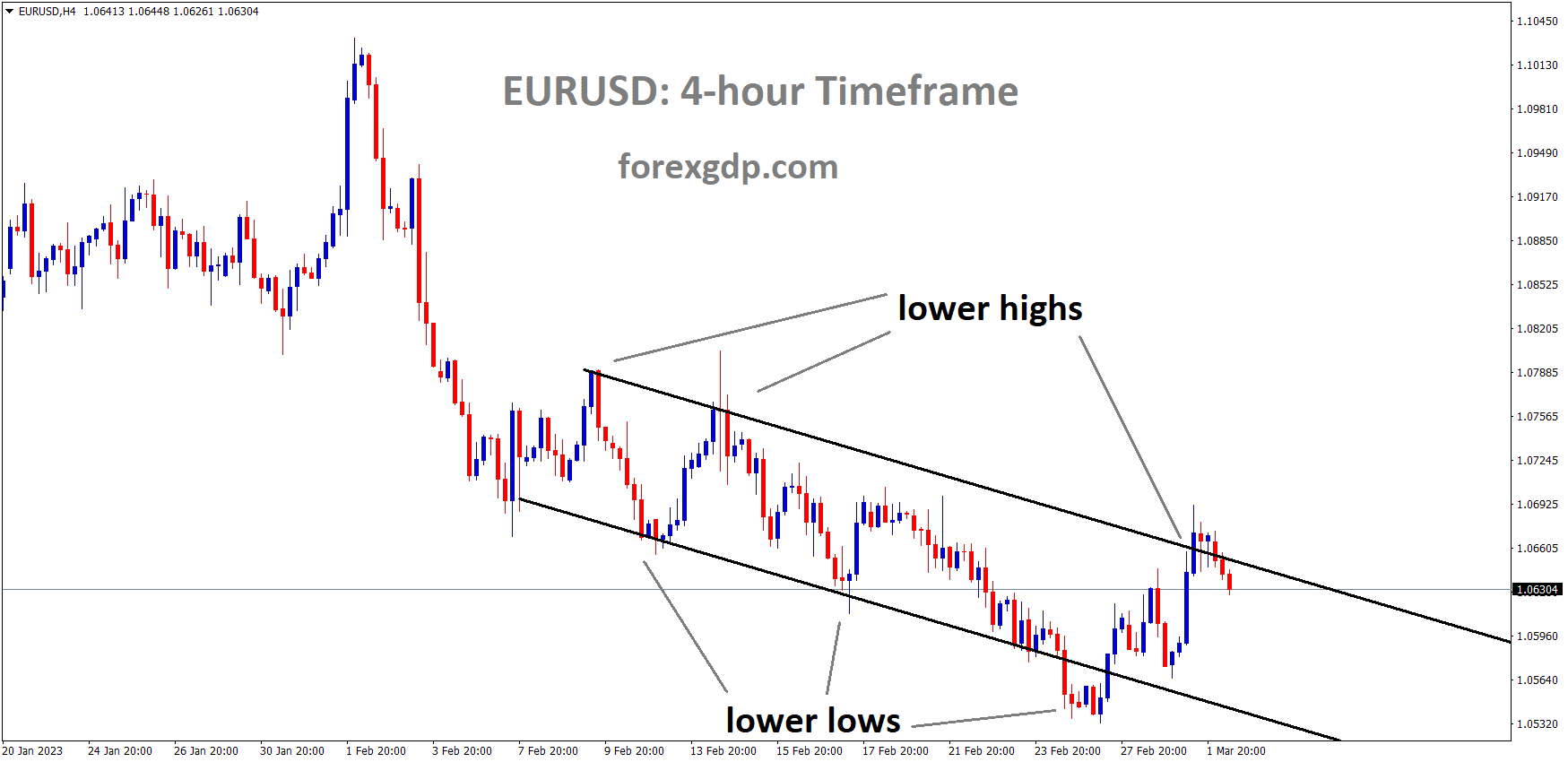

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

The German consumer price index for March showed inflation of 8.7%, which was above the forecasted 8.5%. Consumers are paying 9.3 percent more overall now that they have to account for the rising prices of food and energy.

This month, the ECB will increase rates by 50 basis points, and some experts forecast that we could reach our 4% goal by the end of July.

Higher inflation is causing consumers to spend less in France, Spain, and Germany, so these countries have raised interest rates.

The German CPI figures for February have been released, with both the annual and monthly figures exceeding expectations. As the year-over-year inflation rate remains unchanged at 8.7%, the harmonised inflation rate (which includes food and energy) has increased to 9.3%. The data that measures the change in prices of products and services over a predetermined time period suggests that price pressures may persist for a longer period of time.

While the ECB (European Central Bank) intended to raise rates by an additional 50 basis points later this month (16 March), recent readings from Spain, France, and Germany pose an additional risk to the growth outlook for Europe. In “normal” conditions, higher interest rates reduce consumer expenditure, thereby lowering inflation. However, in the wake of the Coronavirus pandemic, ballooning balance sheets and the Ukraine conflict have compelled policymakers to adopt a more aggressive stance. Monetary policy for the central bank remains centred on attaining “full employment” while maintaining price stability.

Moreover, as a result of Christine Lagarde’s reiteration of the ECB’s commitment to tame inflation through additional rate increases, market participants now anticipate that the terminal rate will reach 4% by July (it is currently 2.75%). In anticipation of Eurozone inflation (to be published on 2 March at 10:00 GMT), the repricing of information has boosted German yields, propelling the two-yield to its highest level since 2008. In reaction to the most recent forecasts, EUR/USD has risen, as investors anticipate that the ECB will remain more hawkish than the Federal Reserve for an extended period of time.

GOLD Analysis

XAUUSD Gold price has broken the Descending channel in Upside.

Yesterday, gold prices increased as a result of US ISM manufacturing activity readings that were below expectations, with 47.7 instead of the expected 48. These figures indicate the escalating cost of data manufacturing in the United States. Analysts anticipate that the United States will raise interest rates and that the level will reach 5.5% in September.

Gold prices attempted a recovery on Wednesday, but it may be challenging for the yellow commodity to sustain its recent gains. This is the third straight day that XAU/USD has risen, and it most likely wouldn’t have happened without a weaker US Dollar. The 1.35 percent increase in gold’s price this week is the largest such increase since early January. Traders probably started the day thinking about the optimistic Chinese factory PMI numbers. The latter hit 52.6 in February, well above the median 50.6 forecast in a poll by Bloomberg. This was an increase from the 50.1 reading in January. When taken as a whole, it’s consistent with a picture of an industry that has been making progress towards full recovery since the recent Covid lockdowns.

Data from the US Institute for Supply Management’s Manufacturing Index did, however, make its way across the lines later that day. While the headline gauge’s reading of 47.7 was below expectations of 48.0, the rates paid index rose to a surprising 51.3 from a reading of 44.5. This is in contrast to the predicted value of 46.5%. For the first time since September, the number indicated increasing expenses. The United States is the world’s largest economy, and the latest CPI and PCE figures have shown that the country’s battle against inflation is likely to continue for some time. Soon after the ISM numbers were released, Fed Funds Futures showed that markets had priced in a peak policy rate of 5.5% in September. The yield on the 2-year Treasury note rose above 5%, approaching its all-time peak set in 2007.

Gold prices fell during Wednesday’s Asia-Pacific trading period as the US dollar recovered some of its earlier losses. The XAU/USD pair could be in for more trouble in the future. Traders’ focus will shift to the latest US jobless claims statistics and a speech on the economy from Christopher Waller, a member of the Federal Reserve Board.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel.

The Swiss Franc stays weaker against the US dollar as Swiss retail sales fell 2.2% year on year, compared to the 2.2% expected. The Swiss SVME Purchasing Manager Index was 48.9, down from 49.3 earlier. Swiss GDP was 0.0%, compared to 0.30% anticipated and 0.20% reported in the third quarter.

Following a disappointing start to the month of March, the USD/CHF is licking its wounds around 0.9400, as the Swiss currency pair takes up bids during early Thursday. As a result, the quotation justifies the country’s grim statistics versus firmer details of US data, strong Treasury bond yields, and hawkish Fed talks, which could jolt US Dollar bulls. However, Swiss Real Retail Sales fell 2.2% year on year in January, compared to the 2.2% expected growth, and the prior reading of -3.0% was revised down. In the same vein, the Switzerland SVME Purchasing Managers’ Index for February came in at 48.9, compared to 49.3 previously. It should be mentioned that the Swiss GDP (GDP) reached 0% in the fourth quarter (Q4) of 2022, compared to an expected growth of 0.3% and 0.2% in the third quarter.

The US ISM Manufacturing PMI details, on the other hand, renew inflation fears as the headline measure increased to 47.7 from 47.4 previously, versus the 48.0 anticipated, but the Prices Paid and New Orders figures were the highest in five and four months, respectively. The statistics and hawkish Federal Reserve (Fed) talks also put the previous day’s US Dollar weakness and USD/CHF pullback into question. “Wage growth is now too strong to be consistent with 2% inflation,” Minneapolis Federal Reserve (Fed) President Neel Kashkari said. The policymaker also added and observed that it is concerning that the Federal Reserve’s rate hikes so far have not brought down service inflation.

However, the earlier softer US data dump, China-inspired risk-on mood, and month-start consolidation appeared to have teased the USD/CHF bears. In the midst of these moves, US 10-year Treasury bond yields surpassed the 4.0% mark for the first time since early November 2022, while the two-year equivalent surpassed the 4.90% mark for the first time since June 2007. The rise in US Treasury bond yields indicates the market’s fear of inflation and recession, which has recently probed bulls on Wall Street and weighed on S&P 500 Futures, implying a probable rebound in the US Dollar.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

The Bank of Governor Bailey’s speech indicates that another round of rate hikes is likely in the coming meetings due to higher inflation costs.

Despite the fact that domestic data provides good results when compared to previous ones, the UK Manufacturing PMI was higher than expected, printing 49.3 instead of 49.2.

Following the release of Data, the UK Pound gained ground against the Japanese yen.

GBPCAD Analysis

GBPCAD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Following a two-day downtrend, the GBP/JPY pair teases investors while building up bids to 163.80 early Thursday, as firmer yields join monetary policy divergence between the Bank of England (BoE) and the Bank of Japan (BoJ). The recent rebound in the cross-currency pair may also be linked to market anxiety ahead of the Group of 20 (G20) meeting, as recent headlines from the New York Times (NYT) indicate a possible rift between the US and China at the key event. “China is urging the start of peace talks, and some Group of 20 nations may support that idea when they meet in India,” according to the news. “However, US officials contend Russia will not engage in good faith,” according to the news.

In other news, US 10-year Treasury bond yields surpassed the 4.0% mark for the first time since early November 2022, while the two-year equivalent surpassed the 4.90% mark for the first time since June 2007. The increase in US Treasury bond yields indicates the market’s dread of inflation and recession, which has recently probed bulls on Wall Street and weighed on S&P 500 Futures. It should be mentioned that the Japanese yen frequently tracks the yields on US Treasury bonds.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

It should be observed that the hawkish remarks of BoE Governor Andrew Bailey contrast with those of BoJ board member Junko Nakagawa, providing additional support to the GBP/JPY recovery. According to Reuters, BoE Governor Bailey stated on Wednesday that a further increase in bank rates may be suitable, but that nothing has been decided. On the other hand, the Bank of Japan’s Nakagawa stated that an easy monetary policy is necessary for the time being because it helps the economy.

Talking about the data, February’s Jibun Bank Manufacturing Japan and S&P/CIPS Manufacturing PMI for the UK improved a bit from their initial forecasts but stayed below the 50.0 level differentiating the growth from the otherwise in activities. Japan’s capital spending increased 7.7% in the fourth quarter (Q4), compared to 9.8% in the previous quarter and 2.8% expected by the market. Moving on, G20 updates could join central bankers’ remarks to keep GBP/JPY traders entertained on what is likely to be a slow day due to the light schedule.

EURAUD Analysis

EURAUD is moving in an Ascending channel and the market has reached the higher high area of the channel.

In an interview with Spanish television, ECB President Lagarde stated that a rate rise of 50 basis points is possible. In Europe, inflation rates are excessively high, and we have set a target of 2%, which can only be reached by reducing consumer expenditure; only an increase in the interest rate will bring inflation back to normal levels.

We do not compare our inflation and interest rates with those of the United States and Europe. We will implement rate increases, but we do not yet know the maximum increase, and the interest rate will vary depending on the circumstances.

In an interview with Spanish television on Thursday, European Central Bank President Christine Lagarde discusses the economic effect of the Ukraine war, rising prices, and interest rate hikes.

The case for a 50 bps rate increase this month is still on the table as inflation is still too high. To reduce inflation, we must employ all available instruments. The future rate path will be determined by statistics. We will do everything possible to reduce inflation to our 2% goal.

It would be a mistake to compare the price scenario in Europe to that of the United States. We still need to seek higher interest rates; we don’t know when the peak will be. We’ll have to remain at higher levels for a while. The ECB does not have the authority to set mortgage terms.

EURNZD Analysis

EURNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The New Zealand Dollar rose as a result of higher China Caixin manufacturing data and lower Australian GDP data.

If China recovers from the Covid-19 slowdown, New Zealand’s commodity shipments to China will increase.

Another plus for the New Zealand Dollar is the RBA’s decision to slow the pace of rate increases.

A rebound in Chinese demand, which boosted commodity prices. This followed a poor performance in the Australian data, in which 4 Gross Domestic Product growth slowed to 0.5% QoQ, down from 0.7% previously, and falling short of consensus forecasts of a 0.8% increase. The data raised the possibility of an earlier pause in rate hikes by the Reserve Bank of Australia, which originally weighed in on both currencies.

However, the kiwi profited from speculative buying after China’s non-manufacturing activity expanded faster in February, and the Caixin/S&P Global manufacturing PMI reading for last month also exceeded. The offshore yuan increased 1.3% to 6.8683 per dollar, marking its biggest one-day rise since late November. The Kiwi also outperformed most peers and did well on crosses, most notably NZD/AUD, according to ANZ Bank analysts. “The Euro was a strong performer following the strong German CPI print, and the Kiwi followed suit, possibly exacerbated by NZD/AUD stop-loss buying, as there was no obvious NZD catalyst. As a result, price action may be muted in the future days.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

The Australian Dollar depreciated against its counterparts due to the release of weaker GDP figures for the fourth quarter. The RBA is expected to raise rates by 25 basis points at its meeting next week; a slowdown in the pace of rate increases will be negative for the Australian dollar.

China’s Comeback from Covid-19 is beneficial for Australian Exports of Iron Ore, which are Australia’s primary exports to China.

Despite strong US Treasury bond yields and mostly positive US data, the Aussie pair battles to explain the softer US Dollar and China-linked market optimism. Nonetheless, after robust China activity data for February, the Aussie pair managed to reverse the Aussie GDP and inflation-induced pessimism. The risk barometer pair also benefited from remarks made by China Finance Minister Liu He, who indicated a willingness to increase the country’s fiscal spending. The policymaker also stated that the basis of China’s economic recovery is unstable, posing a challenge to the AUD/USD bulls.

In other news, the headline US ISM Manufacturing PMI increased to 47.7 from 47.4 the previous month, versus the 48.0 expected. Prices Paid and New Orders, on the other hand, were the greatest in five and four months, respectively. “Wage growth is now too strong to be consistent with 2% inflation,” Minneapolis Federal Reserve (Fed) President Neel Kashkari said ahead of the data. The policymaker also added and observed that it is concerning that the Federal Reserve’s rate hikes so far have not brought down service inflation.

It should be noted that US 10-year Treasury bond yields surpassed the 4.0% mark for the first time since early November 2022, while the two-year equivalent surpassed the 4.90% mark for the first time since June 2007. The rise in US Treasury bond yields reflects the market’s dread of inflation and recession, putting the risk-barometer AUD/USD pair under pressure. Nonetheless, Wall Street ended mixed, with the S&P 500 Futures struggling to find a clear direction. Looking ahead, Australia’s January Building Permits may provide immediate guidance ahead of the US Weekly Initial Jobless Claims. However, the US ISM Services PMI on Friday will be closely watched due to concerns about high service inflation.

Crude Oil Analysis

Crude Oil has broken the Descending channel in Upside.

The Canadian dollar is falling in markets due to the consolidation of oil prices, which is the country’s primary export item.

If the CAD stays stronger than its counterparts, the Governor of the Bank of Canada must consider slowing the rate of interest.

USD/CAD is trading near 1.3600, having fallen to its lowest level in three weeks, as traders battle to interpret mixed catalysts during Thursday’s sluggish Asian session. The quote’s sharp drop on Wednesday could be attributed to the market’s upbeat mood, as well as positive Canadian activity data. The firmer oil price, Canada’s primary export item, bolstered the downside bias. Market sentiment brightened after contrasting Tuesday’s soft US data with Wednesday’s strong China PMIs for February. On the same topic, China Finance Minister Liu He expressed willingness to increase the country’s fiscal spending while also noting that the basis of China’s economic recovery is still shaky.

It’s worth mentioning that the price of oil has risen in the last two days to the highest level since February 17, reaching $77.80 at the most recent round. As a result, the black gold is struggling to justify the earlier upbeat sentiment, as US oil inventories increased more than anticipated, according to weekly data from the US Energy Information Administration (EIA). In other news, Canada’s S&P Global Manufacturing PMI for February increased to 52.4 from 50.1 expected and 51.0 previously, challenging USD/CAD buyers even as US data renewed inflation fears. Nonetheless, the US ISM Manufacturing PMI details renew inflation fears, with the headline index rising to 47.7 in February from 47.4 the previous month, versus the 48.0 anticipated. However, the PMI data show that Prices Paid and New Orders were at their greatest levels in five and four months, respectively. However, the hawkish Fed bets and firmer US Treasury bond yields, combined with higher Oil inventories, look to test the USD/CAD bears later.

“Wage growth is now too strong to be consistent with 2% inflation,” Minneapolis Federal Reserve (Fed) President Neel Kashkari said on Wednesday. The policymaker also added and observed that it is concerning that the Federal Reserve’s rate hikes so far have not brought down service inflation. Furthermore, US 10-year Treasury bond yields surpassed the 4.0% mark for the first time since early November 2022, while the two-year equivalent surpassed the 4.90% mark for the first time since June 2007. The rise in US Treasury bond yields indicates the market’s dread of inflation and recession, which has recently probed bulls on Wall Street and weighed on S&P 500 Futures, indicating a recovery in the US Dollar. The USD/CAD bears held the reins amidst these plays, but they are likely to suffer as the calendar is light and a change in sentiment looms.

Don’t trade all the time, trade forex only at the confirmed trade setups.

🎁 80% NEW YEAR OFFER for forex signals. LIMITED TIME ONLY Get now: forexgdp.com/offer/