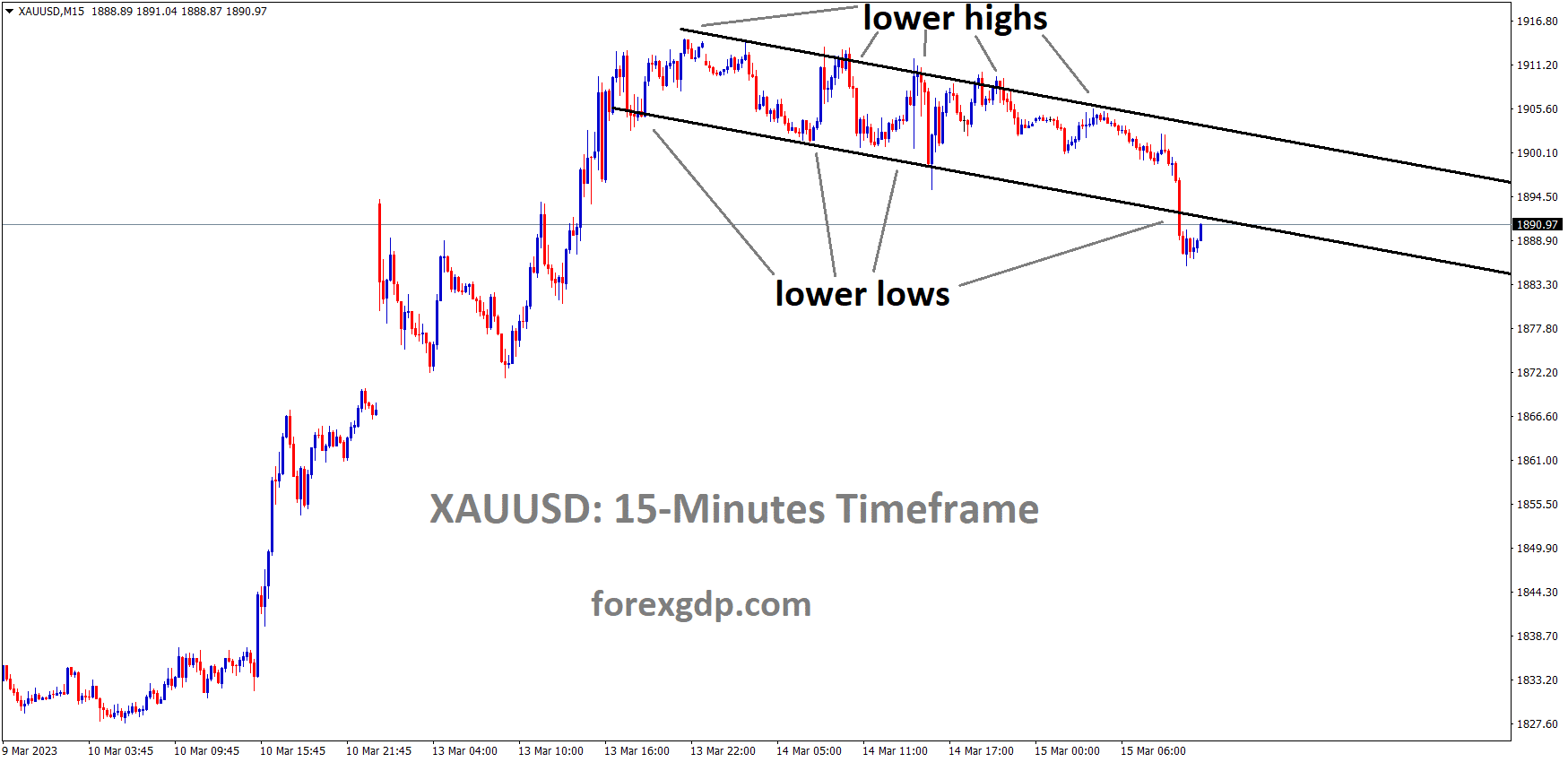

GOLD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower low area of the channel.

Due to the failure of SVB and other banks last week, gold values were driven up to higher levels. The US 2 Year and 10 Year Bond rates yesterday decreased as a result of this news. Non-yielding investments like Gold make shines against US Dollar. Next week’s FED rate increase could be postponed, in which case the gold rally will be strong against the US dollar.

USD Index Analysis

DXY Index has broken the Ascending channel in downside.

Yesterday’s US CPI statistics showed that the housing index contributed 70% of CPI numbers, fuel prices were down, and the food price index increased 0.4% over the previous month. This decline in inflation forces the US FED to consider halting rate increases; if inflation rises, the rate hike tool must be used.

The US inflation rate declines but remains elevated. Fears of banking contagion continue to haunt the market. In February, headline inflation (y/y) in the United States decreased by 0.4% to 6%, in accordance with analyst expectations, while core inflation decreased by 0.1% to 5.5%. According to the Bureau of Labor Statistics of the United States. The index for shelter contributed the most to the monthly increase for all items, accounting for over 70 percent. The indexes for food, recreation, domestic furnishings and operations also contributed. The food index increased by 0.4% month-over-month, while the food at home index rose by 0.3%. The energy index decreased by 0.6% month-over-month as both the natural gas and fuel oil indices fell.

SILVER Analysis

XAGUSD Silver price has broken the Descending channel in upside.

The recent dread of banking contagion, sparked by the failure of Silicon Valley Bank, will remain at the forefront of the Fed’s mind when they announce their most recent monetary policy decision on March 22. While the actions of the central bank in reimbursing depositors have alleviated concerns, the fear that smaller banks are sitting on unrealized bond losses will persist, particularly if the Fed continues to raise interest rates. Market expectations for further rate hikes have been pared back sharply in the last few days, but if inflation remains high then chair Powell and his colleagues will have to decide whether to continue to push down on inflation by tightening monetary conditions or to wait and see if prior rate hikes start passing through the system and dampen price pressures. After the release, the US dollar fell 15 pips before recovering these minor losses and trading flat. The US dollar is presently contending with opposing forces, including fears of banking contagion and declining US Treasury yields, and it remains highly volatile.

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel.

Risk-Reducing money JPY fell as US banking sector turbulence subsided and public concern over the collapse of SVB subsided. After the debt businesses were properly acquired by profit-growth companies, the US dollar began to recover. The ECB’s monetary policy conference is still scheduled for this week; if a rate increase of 50 basis points occurs, the euro appreciates against the yen.

Tuesday saw the Japanese Yen perform worse than its key competitors. Following a relief rally in banking stocks amid increased uncertainty following Silicone Valley Bank’s collapse last week, this was a day when global market volatility carefully decreased. The S&P 500 and the heavily tech-weighted Nasdaq Composite both increased on Wall Street by 1.68% and 2.14%, respectively. At the same time, the market’s “fear gauge,” the VIX, reversed sharply downward, falling 10.45%, suggesting that the worst of the turmoil may have subsided. Front-end Treasury rates spiked sharply higher as traders began pricing in expected rate cuts later this year as a result of the failure of SVB. In reality, the outlook for the next six months has been revised upward by about 30 basis points over the last 24 hours.

The Japanese Yen plays a role in this, which is why it fared poorly. To begin with, the JPY is frequently regarded as a risk-averse currency, occasionally acting like the US Dollar during uncertain market conditions. The currency was affected by the increase in risk appetite. Then there is the impact of increasing Treasury yields in light of the Bank of Japan’s ongoing dovishness. The allure of JPY versus USD would decrease if the Fed adopted a more hawkish stance. The US inflation estimate for February was released, speaking of which. The headline indicator came in as predicted, but the Core measurement surprised higher on a month-to-month basis. This indicates that underlying inflation is still persistent, which presents a challenge for the Fed. Looking at the Wednesday’s Asia-Pacific trading period, China will present a significant economic event risk. These comprise information on regional retail sales and industrial output. In addition, if markets remain calm in the coming hours, traders might keep re-adding expectations for a Fed rate increase. That may be the formula for the USD/JPY to rise further.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

As a result of the SVB Collapse, investors are pouring into tech stocks and non-bank related equities from the Banking Sector, which has a positive effect on the Swiss Franc.

FED is less likely to raise rates by 50 basis points at its meeting next week, and there is little possibility that it will raise rates by 25 basis points.

The USDCHF has seen a modest recovery over the past day and today, following a brief period of market investor concern.

Wednesday marks the second consecutive day of gains for the USD/CHF pair, as fresh buying follows an early decline to the 0.9115 region and the pair turns positive for the second consecutive day. During the early European session, the pair climbs back above the mid-0.9100s and seeks to extend its recovery from a six-week low reached on Monday. A further increase in US Treasury bond yields provides some support for the US Dollar, which is expected to act as a tailwind for the USD/CHF currency pair. Despite uncertainties surrounding the US banking system, investors appear confident that the Federal Reserve will proceed with a 25 basis point rate increase at its March 21-22 policy meeting. Tuesday’s release of US consumer inflation data boosted wagers and continues to drive US bond yields higher.

In addition, indicators of stability in the financial markets appear to weaken the safe-haven Swiss Franc (CHF) and provide additional support for the USD/CHF pair. In response to diminishing fears of a broader systemic crisis stemming from the abrupt collapse of Silicon Valley Bank, investors poured back into stocks, resulting in a relief rally on Wall Street. (SVB). The spillover effect continues to support the equity markets’ prevailing optimism. The aforementioned fundamental environment favors USD investors and supports the likelihood of a significant USD/CHF appreciation move. The US economic calendar features the publication of the Producer Price Index (PPI), monthly Retail Sales data, and the Empire State Manufacturing Index later in the early North American session. Market participants are now focusing on these events. In addition, US bond yields may influence the USD’s price dynamics.

The technical picture is more bearish, implying that long holders should exercise caution. The decline from the March 8 highs has temporarily bottomed, and the price has entered a consolidation phase. This appears to be a continuation pattern of a bear flag rather than a reversal. A break below the February lows of 0.9065 would corroborate the flag pattern’s activation and likely lead to an extension to a target near 0.8850, the 61.8% Fibonacci extension of the flagpole. A two-day FOMC monetary policy meeting, commencing next Tuesday, will drive the USD in the near term and determine the next leg of a directional move for the major currency.

USDCAD Analysis

USDCAD is moving in the Descending channel and the market has reached the lower high area of the channel.

Market weakness for the Canadian Dollar led Bank of Canada governor Tiff Macklem to state that no rate change is anticipated in the near future; if inflation increased, watch for changes in the inflation rate; if not, rates will stay the same. In Moody’s opinion, the FED will raise rates, but banks with higher debt loads will struggle. Based on market behavior observed by CAD, US retail sales and US PPI data are planned for release this week.

Today’s decline in the USD/CAD pair has reached the top of the range breakout that eventually happened last week. However, the loonie’s attempts to record further gains against the dollar may be hampered by falling WTI oil prices. The US Dollar is still trending higher, but this week’s apprehension and uncertainty have made that route less straightforward. Despite recent developments, I still believe that the Fed will raise rates at its meeting next week, so the general fundamental picture is still in favor of the bulls going forward. The market expectations now all but rule out the likelihood of a 50bps hike, leaving the issue of whether it will be 25bps or not at all. Today, Moody’s also spoke to us, stating that their basic scenario is for the US Fed’s monetary tightening to continue, which might make some US banks’ difficulties worse.

In the meantime, the Bank of Canada (BoC) reiterated its conviction that the present monetary policy stance is constraining enough to control inflation. BoC Governor Macklem did, however, leave the possibility of additional rate increases open in the event that inflation picks back up. Fears that inflation may rise once more have been rekindled in response to recent increases in employment statistics and a higher employment cost index. This has not yet happened, but the Canadian inflation data that will be released on Tuesday of next week should make things clear for the BoC going forward. We still have a lot of US statistics coming out for the rest of the week, including tomorrow’s release of Retail Sales and PPI. The Canadian inflation print, which is due on Tuesday of next week, is the primary data point that could have a significant effect on USDCAD.

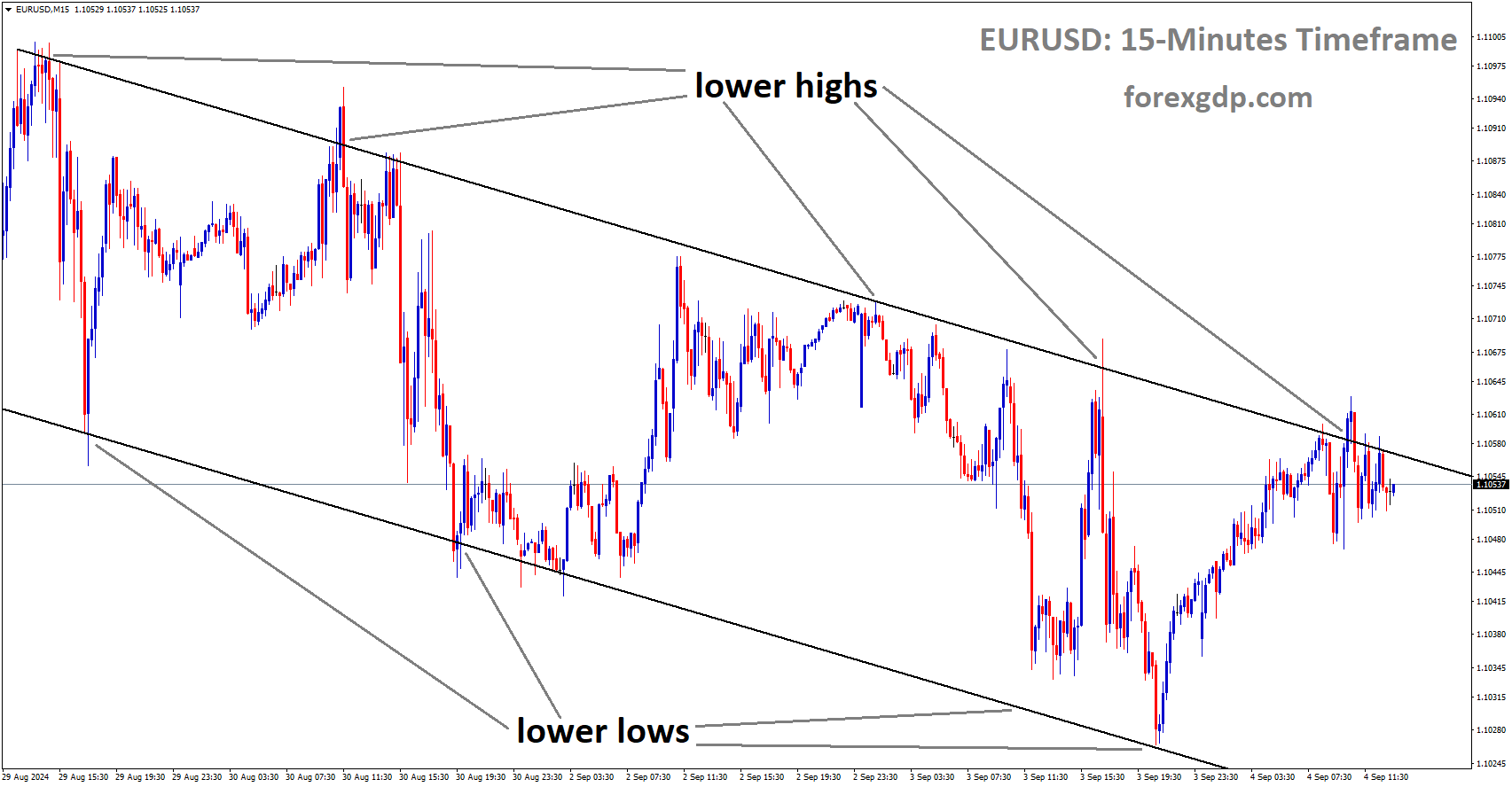

EURUSD Analysis

EURUSD is moving in the Rising wedge pattern and the market has reached the higher low area of the pattern.

The US CPI data came in as anticipated at 6.0% YoY and 0.40% MoM, which caused the US dollar to weaken against the Euro and dashed expectations that the FED would raise interest rates at its meeting next week.

The US FED paused rate increases in upcoming meetings to inject more liquidity into the banks after the US SVB and Signature banks already collapsed and the US CPI printed at lower numbers.

Tomorrow’s ECB monetary policy conference will result in a rate increase of 50 basis points, which will strengthen the euro relative to the US dollar.

Chinese data published today is mixed: retail sales are in line with expectations, industrial production is slightly below expectations, but fixed investments in EX-Rural come in higher than anticipated, strengthening the Chinese economy.

As the market considers the wider effects of the failure of three US banks and the following government rescue of them, the euro has risen again today. Despite this, the US Dollar is still under attack, and the EUR/USD exchange rate is heading above 1.0750, toward a 4-week high. After a turbulent week that saw wild fluctuations in many asset classes, financial markets generally stabilized on Wednesday. The changes in the 2-year Treasury paper were noteworthy. The MOVE indicator reached its highest level since 2008 as a result. Similar to how the VIX index measures implied volatility in the S&P 500, the MOVE indicator measures volatility in the bond market.In the US session, Treasury yields increased across the curve; however, moving into the European session, they have slightly decreased from 5 years and beyond.

Headline According to forecasts, the US CPI was 6.0% year over year and 0.4% month over month. Although the annual figure of 5.5% was in line, the monthly core CPI was slightly higher at 0.5% as opposed to the forecasted 0.4%. In light of the recent chaos, this has intensified the emphasis on next week’s Federal Open Market Committee (FOMC) meeting for the rate path ahead.

Following Wall Street’s positive lead, APAC equities are all up today to different degrees as the calm seems to have returned. After mixed Chinese statistics, the Hong Kong Hang Seng Index (HSI) took the lead and increased by more than 1%. Retail sales were in line for the same period at 3.5%, while industrial output had a slight miss of 2.4% YoY to the end of February as opposed to the expected 2.6%. For the same time, fixed assets excluding rural areas beat expectations, coming in at 5.5% versus the forecast of 4.5%. Additionally, the People’s Banks of China (PBoC) added more liquidity than anticipated at the 1-year medium-term lending facility (MLF).After declining once more yesterday, crude oil has since rebounded. At the moment of publication, the Brent futures contract is trading around US$ 78.50 bbl and the WTI futures contract is close to US$ 72.50 bbl. Going into the Euro period, gold is steadily trading around US$ 1,900. More CPI statistics will be released today across Europe, which could influence tomorrow’s European Central Bank (ECB) meeting expectations. A 50 bp increase there is what the interest rate market is moving toward.

EURGBP Analysis

EURGBP is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Today will see the presentation of the UK’s Spring Budget; a reduction in gasoline taxes is the most anticipated significant point, and the Bank of England would like to pause rate hikes due to the collapse of the SVB bank in the United States.

EURGBP rose advance of the ECB Meeting the following day, the Bank of England is scheduled for March 23, UK wages are currently cooling, and bonuses were reduced from 6.7% to 6.5%. Therefore, the British Pound may strengthen if the US Dollar continues to decline.

The EUR/GBP cross rises for a second consecutive day on Wednesday and seeks to build on yesterday’s solid rebound from the 0.8775 region, or over a one-week low. In the early European session, the cross trades with a slight positive bias and is presently located around 0.8830, up less than 0.05% on the day. The British Pound’s relative underperformance is largely attributable to expectations that the Bank of England (BoE) will halt its rate-hiking cycle next week, which provides support for the EUR/GBP exchange rate. Amid indications of a decline in UK wages, the markets are now pricing in a 40% chance that the BoE will leave interest rates unchanged on March 23. The bets decreased after the UK Office for National Statistics reported on Tuesday that annual growth in average total pay, including bonuses, declined to 5.7% in the three months leading up to January, down from 6% in the preceding month. The growth in pay, excluding incentives, slowed from 6.7% to 6.5%.

However, a number of European Central Bank (ECB) policymakers recently defended the need for extra jumbo rate increases after the March meeting. This, in turn, continues to support the shared currency and appears to boost the EUR/GBP exchange rate. Ahead of Thursday’s crucial ECB monetary policy meeting, however, bullish traders appear reluctant to place aggressive wagers and prefer to sit on the sidelines. In the absence of pertinent macro data, the presentation of the UK government’s new budget on Wednesday could influence the Sterling Pound and provide some impetus for the cross.

Nevertheless, the above-mentioned fundamental environment bolsters the EUR/GBP cross’s upside potential. Even from a technical standpoint, the overnight recovery reaffirmed strong support close to the 100-day Simple Moving Average (SMA) at 0.8770, which should now serve as a transition point and a solid base for spot prices in the near future. A convincing break below, on the other hand, will negate the bullish outlook and move the bias in favor of bearish traders, paving the way for an extension of the recent pullback to a potential target near 0.8680, where the 200-day simple moving average and a major trendline intersect.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

Chinese statistics for today were mixed, but growth in fixed assets, which represents investments in construction projects, jumped to 5.5%. This is a modest effort to promote Australian exports to China, which is Australia’s top commodity importer.

In addition, today’s US PPI, scheduled retail sales data, and yesterday’s US CPI weaken the US Dollar against the AUD and raise questions about FED rate increase predictions.

Early this morning, the Australian dollar looked to Chinese activity figures, which were rather mixed but ultimately positive for the Chinese economy. In particular, fixed asset investment increased to 5.5%, demonstrating a significant improvement in investments in building projects. The Australian dollar received support from the data’s small upbeat slant thanks to optimism surrounding commodity exports. Being a pro-growth currency, the Australian dollar (AUD) reacts favorably to positive development data coming from China, which is Australia’s biggest commodity importer.

The PPI and retail sales reports for February will be the only US statistics on the economic calendar later today. Both are predicted to be lower than previous releases, which could cause the U.S. dollar to decline even more should actual figures match forecasts. Despite this, markets remain uncertain about the Fed’s future course because yesterday’s US CPI gave little indication. In addition, the systemic effects of the failures of the Silicon Valley Bank (SIVB) and the Signature Bank are still being considered.

NZDUSD Analysis

NZDUSD is moving in the Box Pattern and the market has reached the horizontal support area of the pattern.

According to S&P Global Ratings, as New Zealand’s current account deficit widens, imports exceed exports of services and commodities.

If these imports increase in the future, the NZ Currency’s AA+ rating could be in jeopardy and deterioration is conceivable. New Zealand has placed a greater emphasis on the importation of a variety of materials and the reconstruction industry.

In June of last year, S&P predicted that the deficit would be 6.7% and would decline to 5.7% by mid-2023; however, 8.9% has been recorded in recent months. It depicts the primary risk of the New Zealand current account deficit widening.

Bloomberg reported early Wednesday morning in Europe that New Zealand’s credit ratings with S&P Global Ratings could come under pressure if the nation’s current account deficit remains too large. Anthony Walker, director of sovereign ratings for Australia, New Zealand, and the Pacific at S&P, is quoted in the news as saying that the deficit “is at an exceedingly high level and is much larger than we anticipated.

The persistently weak and deteriorating current account position of the New Zealand government is attracting our attention, especially given that it has been quite weak over the past year or two and our projections call for it to narrow. S&P assigns New Zealand AA+ foreign currency and AAA local currency ratings, but has always highlighted the country’s external imbalances as a major concern. As the nation imported more goods and services than it exported, the current account deficit ballooned to 8.9% of gross domestic product (GDP) in 2022, according to data released on Wednesday.

In June of last year, S&P predicted the deficit would be 6.7% and decline to 5.8% by mid-2023. If the current account deficit does not decline within the next 12 to 18 months, the AA+ rating will come under increasing pressure. New Zealand imports a great deal of materials, and reconstruction will necessitate additional imports, so this could also contribute to the country’s weakened external position.

Crude oil Analysis

Crude oil is moving in the Descending channel and the market has reached the horizontal support area of the minor Box pattern under the channel.

In a recent interview with Energy Intelligence, the energy minister of Saudi Arabia, Prince Abdul-Aziz bin Salman, stated that the OPEC+ alliance should adhere to its production limits until the end of 2023.

Those who wish to modify the agreement with us must do so before the end of 2023.

Tuesday, Saudi Arabia’s Energy Minister Prince Abdulaziz bin Salman stated in an interview with Energy Intelligence that the OPEC+ alliance will adhere to production limits until the end of 2023. There are still those who believe we will modify the agreement… He added that until Friday, December 29, 2023, we will demonstrate our commitment to the current agreement.

Don’t trade all the time, trade forex only at the confirmed trade setups.

🎁 80% NEW YEAR OFFER for forex signals. LIMITED TIME ONLY Get now: forexgdp.com/offer/