USDCAD Analysis

USDCAD is moving in the Symmetrical triangle pattern and the market has rebounded from the bottom area of the pattern.

This Wednesday’s FED monetary policy meeting has a 25 basis point rate hike planned; this is the highest rate since 2007. Any rate delay will result in the US Dollar falling back. By providing money to Banks that have defaulted, the FED is preserving investor trust. This time, borrowing is more expensive, so money will be called. So the FED reconsiders its choice to set interest rates this week.

The steep decline in U.S. bond yields, which was exacerbated by traders repricing down the Federal Reserve’s tightening path in the face of extreme turmoil in the banking sector, put pressure on the U.S. dollar this week, which fell by about 0.8% to settle just below the 104.00 level. After the failure of two mid-sized U.S. regional banks stoked concerns about a financial Armageddon and prompted the Fed to take emergency action to support depository institutions experiencing liquidity problems, bets on the outlook for monetary policy changed in a dovish way. Despite Jerome Powell’s hawkish speech to Congress, the chart below shows how much Treasury yields and Fed terminal rate forecasts have dropped since last Wednesday. It also demonstrates how the dollar’s decline has coincided with that of those commodities. Given recent events, the path of least resistance for the U.S. dollar is likely to be lower, given that the current situation doesn’t get out of hand and trigger a major financial crisis, as that would benefit defensive currencies.

After the Fed releases its March policy decision on Wednesday, traders will have more information with which to evaluate the future of the dollar. Although forecasts have fluctuated, market pricing now favors an interest rate increase of one-quarter point, which would increase borrowing costs to 4.75%–5.00%, the highest level since 2007. Anyway, there is still a possibility of a pause and it shouldn’t be entirely thrown out because a lot could occur between now and Wednesday. Recent events have demonstrated that negative news can appear out of nowhere and without warning. Nevertheless, any new financial strain might prompt officials to proceed cautiously and take a wait and see stance. Whatever the Fed chooses to do next week, everything is in place for dovish guidance. The FOMC is likely to stress the significance of maintaining financial stability and its preparedness to take action to stop the development of systemic risks. The ramifications of this message might cause the US currency to decline even more.

GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Inflation in developed countries is significantly influenced by gold in these times. When yield rates are reduced, gold seems to be the ideal hedge; even during the 2008 Financial Crisis, gold prices skyrocketed. Due to the failure of SVB and Signature Banks, the same situation will occur again in 2023.

Energy crisis in Europe was caused by the Russia and Ukraine Wars, and after 2014, trade relations between the US and China were not as good as they had been for the previous 30 years. Investors now anticipate the same calm era to return. This week, the FED will decide whether to raise or hold its interest rate. If neither is altered, gold prices fall.

Gold is enduring a challenging year for an asset that is frequently hailed as the ultimate safe haven or inflation hedge. If the metal is truly what so many of its followers perceive it to be, then these are some of its best days in years. Inflation has, after all, reemerged across the globe. And that after decades of such obedient submission, an entire trading generation will have never experienced price increases of the current magnitude. Accustomed to a world in which even 2% inflation targets frequently proved elusive, the year 2022 has imparted difficult lessons. However, gold’s downward trend is still very much in force. Likewise, the need for a safe-haven asset is not difficult to discern. The invasion of Ukraine by Russia has crippled the European economy, which is still completely dependent on Putin’s regime for its energy requirements. Tensions between China and the United States imperil the last thirty years of largely peaceful globalization, to the extent that many analysts are prepared to declare its demise. Covid has also played a negative role, stifling global development and forcing a rethinking of supply chains. Priority is now placed on resiliency where price once held influence. China’s neighbors are becoming increasingly concerned about its Taiwan ambitions. Regional military budgets are increasing. And gold continues to decline.

In reality, the metal has spent the majority of time since March acting more like a traditional ‘risk asset’ than a safe refuge. Since March, gold and stock markets have been declining roughly in tandem, which seems counterintuitive if gold is truly a safe haven or inflation hedge. Clearly, as shown in the preceding graph, prices do increase when a natural disaster occurs or when inflation increases. However, it is also evident that these gains have been short-lived and that neither has come close to reversing the current downward trend. In reality, gold reacts to inflation via the transmission channel of interest rate expectations. The metal is notoriously worthless beyond the possibility of price increases or, possibly, capital preservation. There is no yield or dividend offered to gold holders. Basically, there are no benefits. Since 2009, years of historically low interest rates in the United States and throughout the globe have benefited the asset. When yields are low or even negative, the opportunity cost of holding a non-yielding asset decreases.

Now, the situation is in reverse. As global interest rates rise significantly, the allure of non-yielding gold diminishes. In reality, the most significant factor affecting the price of gold is the anticipated path of interest rates, particularly in real terms. The lower the expected real rate, the more attractive a non-yielding asset becomes. Once prices begin to rise, gold appears to lack merit. There may be one or two caveats to add here. Gold’s fortunes may yet improve if the substantial firepower currently employed by central banks to combat inflation begins to appear ineffective. The US Federal Reserve appears to be achieving some success in taming prices, but it is far too early to be optimistic. Other monetary authorities have yet to increase their efforts, and the likelihood of their success is uncertain. Remember that inflation targeting has never been tested in quite this manner before. Recent interest rate increases have been moderate and relatively painless for central banks. They are no longer. Increases in interest rates will be extremely painful for businesses and consumers.

USDJPY Analysis

USDJPY has broken the Box pattern in Downside.

The Bank of Japan should continue its ultra-loose monetary policy and address the negative impacts of economic problems, according to the outlook for the March month BoJ policy meeting.

After a long time, the Japanese economy is now showing signs of improvement. Members of the Bank of Japan have stated in Reuters that any adjustments to monetary policy will have a much greater impact on the economy.

There is now a public version of the Bank of Japan’s Summary of Opinions. According to a Reuters summary of views from their March policy meeting released on Monday, the board members saw the need to maintain ultra-loose monetary policy for the time being, even as some warned of the need to scrutinize its side effects, such as deteriorating market functions.

An upswing in Japan’s economy appears to be on the horizon. One of the members was quoted as saying that any change in monetary policy should be carefully discussed because of the effect on markets and other economic entities. The BOJ’s predictions for inflation and GDP growth are included in this analysis. Eight times a year, roughly every 10 days after the publication of the Monetary Policy Statement, there will be a meeting of this kind.

USD Index Analysis

US Dollar Index is moving in the Descending channel and the market has fallen from the lower high area of the channel.

In a combined statement, US FED Powell and US Treasury Secretary Janet Yellen stated that US Banks are secure, have enough liquidity, and funds are still robust.

They also admired SNB’s efforts to defend Credit Suisse and restore investor and public faith in banks. If any banks default, loans are available and funds will be provided, according to ECB president Christine Lagarde.

The head of the US Federal Reserve, Jerome Powell, and the secretary of the Treasury, Janet Yellen, said in a joint statement on Sunday that “the US banking system’s capital and liquidity situations are robust and the financial system is resilient. We applaud the Swiss authorities’ statements made today to support financial stability. The US banking system has strong capital and liquidity situations, and its financial system is robust.

To assist in their implementation, we have maintained constant communication with our foreign partners. Christine Lagarde, president of the European Central Bank, stated that the bank expects the Swiss-brokered rescue of Credit Suisse will bring calm to the financial markets shortly after Powell and Yellen released their joint statement. If necessary, Lagarde continued, the ECB is still prepared to provide loans to assist Eurozone institutions.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Ville Roy, a member of the ECB, stated that because French banks are more reliable than those in the US and Switzerland, France should escape recession in 2023.

The June month should see a decline in agricultural prices thanks to the ECB’s ongoing implementation of policies to contain inflation. As opposed to other global nations, Europe has well-funded banks and stricter regulations.

Francois Villeroy de Galhau, governor of the Bank of France and a member of the European Central Bank’s Governing Council, said on Monday that France should escape recession. Villeroy argued that the United States’ regulation of financial institutions was inferior to that of France and Europe.

The liquidity and capital of French institutions are very healthy. This statement restates the ECB’s commitment to reducing inflation. French financial institutions are unconcerned about the crisis in the banking sector witnessed in the United States and Switzerland.

Cautious in the face of rising food and electricity costs. We can’t let inflation become systemic. Have high hopes that June brings lower food costs. approves of UBS’s decision to acquire Credit Savio.

EURCHF Analysis

EURCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Due to the failure of Credit Suisse Bank and SNB protection, Swiss Franc may experience modest loses through June 2023.

Therefore, SNB cannot raise rates again until bank problems are resolved.

Due to the well-funded nature of European banks, ECB will continue to implement large rate increases, such as those of 50 basis points. SNB intervention on the foreign exchange market will moderately increase the CHF and put inflation under control.

Commerzbank economists predict that the ECB will act more restrainedly generally and that the Franc will weaken against the EUR over the course of the year. The latest inflation development in Switzerland may prompt the SNB to intervene in the foreign exchange market if the Franc weakens too much. Therefore, EUR/CHF may temporarily trade below parity in the near future.

However, we anticipate a moderate weakening of the CHF over the medium run. The reason for this is that the SNB should permit the Franc to weaken moderately against the EUR because the ECB is likely to increase its key rate more than the SNB by the middle of the year and because price pressures in Switzerland are likely to ease at the same time.

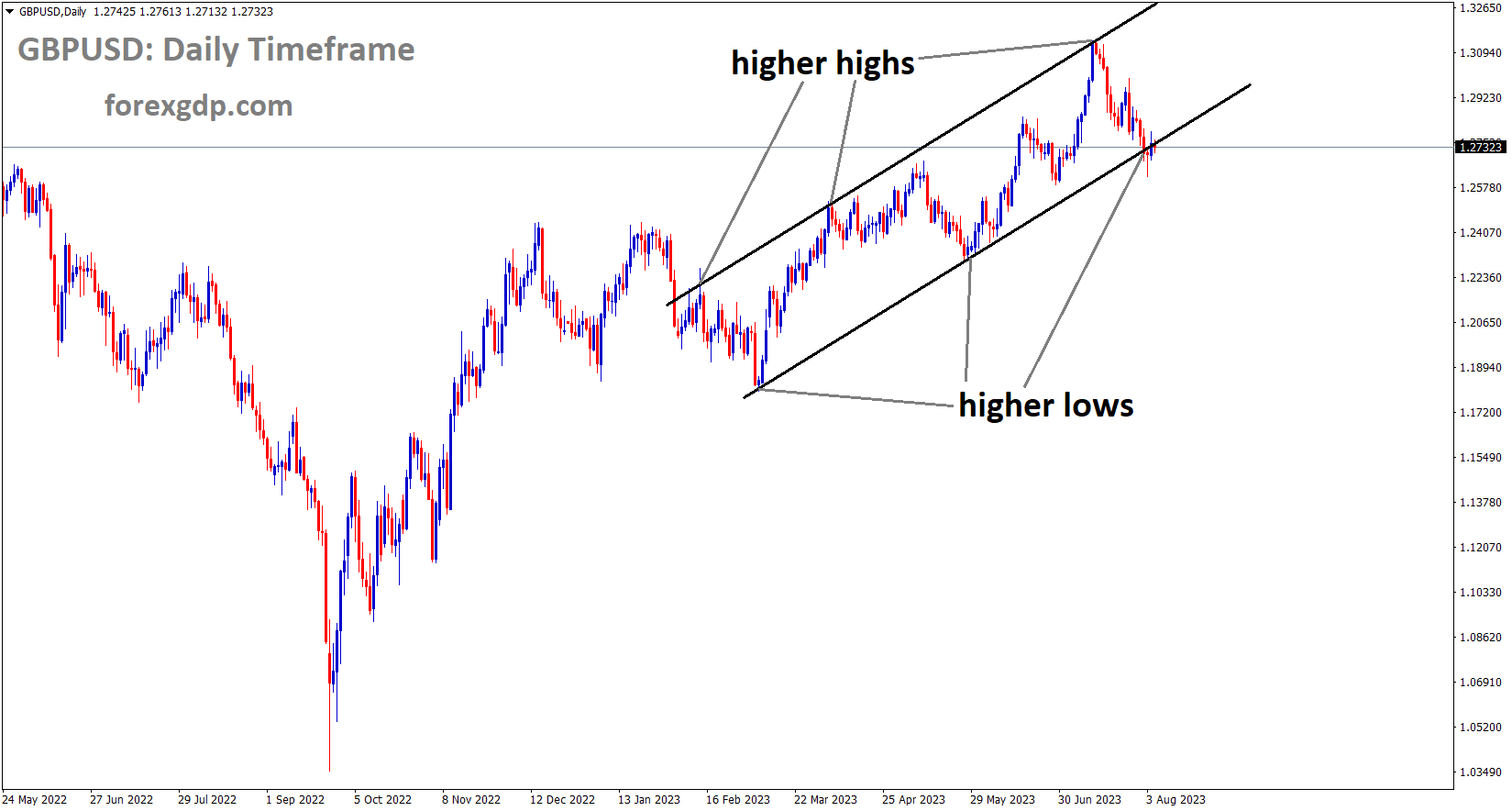

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

The lifetime pension savings were eliminated, the corporate tax rate was increased to 25%, and there were incentives for early retirees in the UK Chancellor’s spring statement, which was given last week. It also included the $2500 Energy Price Guarantee.

Although the UK CPI is still in the double digits, according to Jeremy Hunt’s remark, it may reach 2.9% in November 2023. Any increase in interest rates from the Bank of England this week will impact the values of the GBPUSD pair. When compared to the November expansion of the previous year, a small contraction of the UK GDP of 0.20% is anticipated.

Despite the optimistic projections, the underlying data for the pound sterling, with the exception of PMI data, have not really changed all that much. After the smallest of expansions in Q3 (0.1%), GDP growth for Q4 showed a contraction. Inflation is still in the double digits. The extremely difficult task of the Bank of England raising rates while banking stocks try to fend off a selling frenzy as concerns of systemic risk spread throughout global banks after the failure of three midsized US banks is considered in the bearish outlook for this forecast. On the surface, the pound sterling appeared to have a good week. The week ended with a gain for Cable, EURGBP fell, and GBPCHF was about 2% stronger for the week going into the weekend.

The chancellor opened Jeremy Hunt’s Spring Statement with a strong prediction that the UK will escape a technical recession and that inflation will more than halve, from 10.7% in November to 2.9% by the end of 2023. This prediction was made by the Office for Budget Responsibility (OBR). As opposed to the previous November number, a minor contraction of 0.2% is now anticipated. The budget proposal included a three-month extension of the $2500 energy price guarantee, a 25% corporate tax rate increase, the complete elimination of the lifetime allowance for pension savings, as well as financial incentives to entice early retirees, the chronically ill, and new parents back to the workforce.

For the month of February, UK core inflation is predicted to stay flat and not alter year over year. With prices predicted to have risen 9.8% from February of last year, headline inflation is forecast to fall into the single digits. In particular when energy costs have fallen significantly, core inflation the measure of inflation that excludes volatile food and fuel prices is a better indicator of widespread price pressures. Given the extreme volatility that has followed the emergence of global banking concerns, the BoE will undoubtedly watch the data print with great interest before choosing whether to hike by 25 basis points or adopt a more cautious stance.

The implied odds at this time indicate that there is a nearly equal chance of both no change in interest rates and a 25-basis point increase. In either case, sterling has resisted strengthening after previous hikes because doing so only makes the cost-of-living crisis worse. On the other hand, a choice not to hike could cause sterling to trade lower through the end of the week. The FOMC has led the charge in rate increases, which has contributed to a deflationary tendency in the general level of prices. Perhaps the Fed has more leeway than the ECB and BoE to contemplate leaving the Fed funds rate unchanged given the progress being made in containing inflation. The committee will be well conscious of the hot economy the US is experiencing, which presents upside risks to inflation. It’s a very difficult decision once again, but the additional liquidity measure revealed by the Fed for banks that need it might give the FOMC the assurance it needs to raise interest rates by 25 basis points.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Tomorrow’s RBA meeting minutes are planned, and given the recent drop in unemployment to 3.5% and the strong job market, an announcement of a rate cut for June 2023 is anticipated.

Large rate increases are not likely to occur this year, as the global bank failure suggested; if they do, the global financial infrastructure will experience contractions.

Last week, the Australian Dollar defied gravity by ending the week higher in a situation where the currency would usually face pressure. Risk confidence has declined, and the RBA might not raise interest rates again. Strong employment growth indicates a healthy domestic economy, but on the other hand, the global macro-outlook has rapidly deteriorated as a number of banks seek rescue aid. In this regard, the interest rate market has already discounted the RBA’s decision to reduce in June as its next move. The terminal rate, or the highest cash rate before a cut could be anticipated, was originally pegged by the market at 4.35% at the beginning of this month. However, it is now believed that the present cash rate of 3.60% is the terminal rate. According to statistics released by the Australian Bureau of Statistics (ABS) on last Thursday, the unemployment rate decreased to 3.5% in February as opposed to the 3.6% consensus estimate and 3.7% in January. Australian employment increased by 64.6k in the month, exceeding expectations of 50k and a prior increase of -10.9k. The tight domestic labor market was disregarded in light of the growing banking confidence problem in the US and Europe.

Market jitters appear to have been temporarily calmed by the various rescue deals for SVB Financial, Signature Bank, First Republic Bank, and Credit Suisse. The Federal Deposit Insurance Corporation asserted that it is aware of other banks that are in a similar position when it intervened to protect depositors at the banks that were in danger. The FT is reporting elsewhere that UBS is contemplating buying all or a portion of Credit Suisse. Therefore, even though things have temporarily calmed down, there may still be a few more hiccups before this financial saga is over. Other cracks in the global financial architecture may become apparent as a result of the aggressive tightening of monetary policy. Markets continue to be concerned about this, and if new problems develop, it may seem possible that risk assets like the AUDUSD will be scrutinized. Although the macro view seems likely to cause the AUDUSD to tremble, fundamentals like bond spreads could return to having an impact on currencies.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

Today’s meeting of the People’s Bank of China’s monetary policy committee is set; no rate change is anticipated; if it goes as planned, that will be good news for the New Zealand Dollar.

The biggest trading partner of China is New Zealand. The trade deficit for the month of February increased to 8.9%, and S&P Global Ratings suggested that the NZD currency should exercise more caution in maintaining its AA+ grade. If the trade deficit widens constantly, the NZD may lose its AA+ rating.

In the early Asian session, the NZDUSD pair is running into obstacles as it attempts to rise above the immediate support of 0.6280. As investors wait for the release of the People’s Bank of China’s interest rate decision before taking further action, the Kiwi asset is anticipated to stay on edge. The PBoC may continue to be dovish on interest rates in order to support the Chinese economy’s plan for economic recovery. A UOB Group economist hypothesizes that the PBoC might lower the Loan Prime Rate at its upcoming meeting on March 20. They continued, We see the potential for the 1Y LPR to fall to 3.55% and 5Y LPR to 4.20% in Mar, following the National People’s Congress, given the need for additional support measures for the real economy and for 5Y loan prime rate to decrease further to boost demand for homes. It is important to remember that New Zealand is one of China’s top trading allies, and the New Zealand Dollar would benefit from the PBoC’s dovish stance. The NZ current account imbalance is also affecting the country’s long-term viability.

According to data published last week, the country’s current account deficit widened to 8.9% of GDP in 2022 as it imported more goods and services than it exported. S&P predicted that the deficit would decline from 6.7% in June of last year to 5.8% by mid-2023. According to Bloomberg, if New Zealand’s current account imbalance continues to be too large, the country’s credit ratings with S&P Global Ratings may suffer. After finishing last week with substantial losses, S&P500 futures are showing respectable gains in the early Tokyo session, indicating a small amount of optimism in the general risk-aversion theme. Investor confidence in US stocks is returning as hopes for a steady monetary policy by the Federal Reserve rise. The US Dollar Index has also tried to recover from its recent low of 103.65, but the upside appears limited due to the collapse of the banking industry.

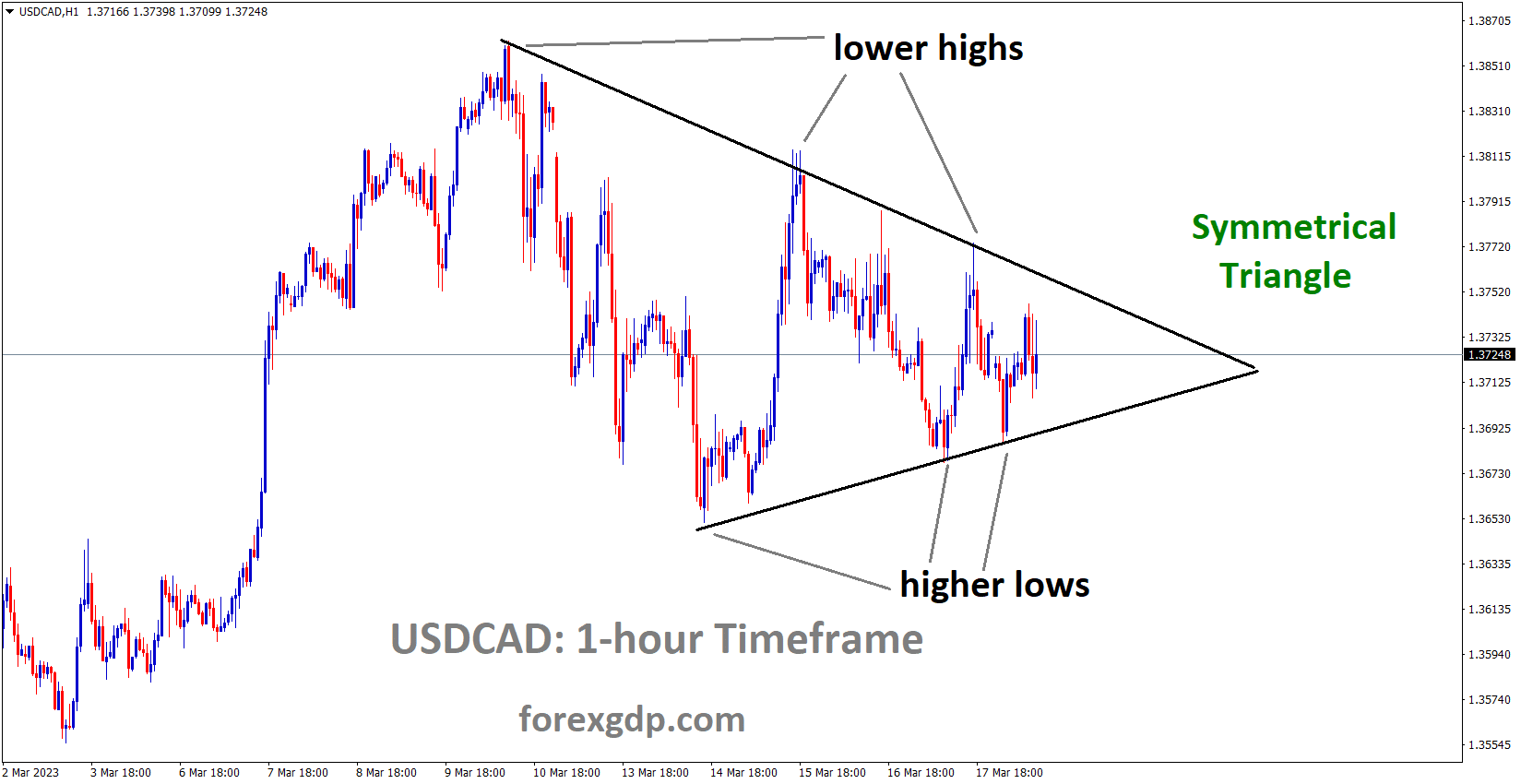

Crude oil Analysis

Crude oil price is moving in the Descending channel and the market has reached the lower low area of the channel.

The Canadian Consumer Price Index is anticipated to drop to 0.40% this week from the prior reading of 0.50%. Since the prior report put the annual core CPI at 5.0%, this data may bring it down to 4.6%.

The financial imbalance in US middle-sized banks and Swiss banks causes the oil markets to crash, which in turn causes a precipitous drop in the Canadian dollar. Since there is an abundance of Oil due to liquidity issues, the demand from customers has decreased. Another potential reason for the drop in oil prices is the Fed’s decision to raise interest rates.

After a slight retracement in the Asian session, the USDCAD pair has found support near 1.3700. As investors wait for the release of Canada’s Consumer Price Index statistics and the Federal Reserve’s decision on interest rates, which will occur on Tuesday and Wednesday, respectively, the loonie asset is exhibiting a contraction in volatility. The possibility of the Federal Reserve maintaining its current monetary policy decision is getting attention as the American banking shakedown has negatively affected investors’ confidence significantly. In the meantime, as the Fed is anticipated to ease up on interest rates, the US Dollar Index has reversed further to 103.65. Despite the S&P500 futures’ rebound move following Friday’s bearish settlement, investors’ risk appetite for US stocks is still very low. Investors are anticipating Tuesday’s Canadian inflation statistics on the Canadian Dollar front. The headline Consumer Price Index is anticipated to increase by 0.4%, which is less than the previous release’s 0.5% increase, according to opinion. The yearly headline CPI could increase as a result to 5.5%. Additionally, the yearly core CPI is predicted to decrease from its previous release of 5.0% to 4.6%.

Don’t trade all the time, trade forex only at the confirmed trade setups.

🎁 80% NEW YEAR OFFER for forex signals. LIMITED TIME ONLY Get now: forexgdp.com/offer/