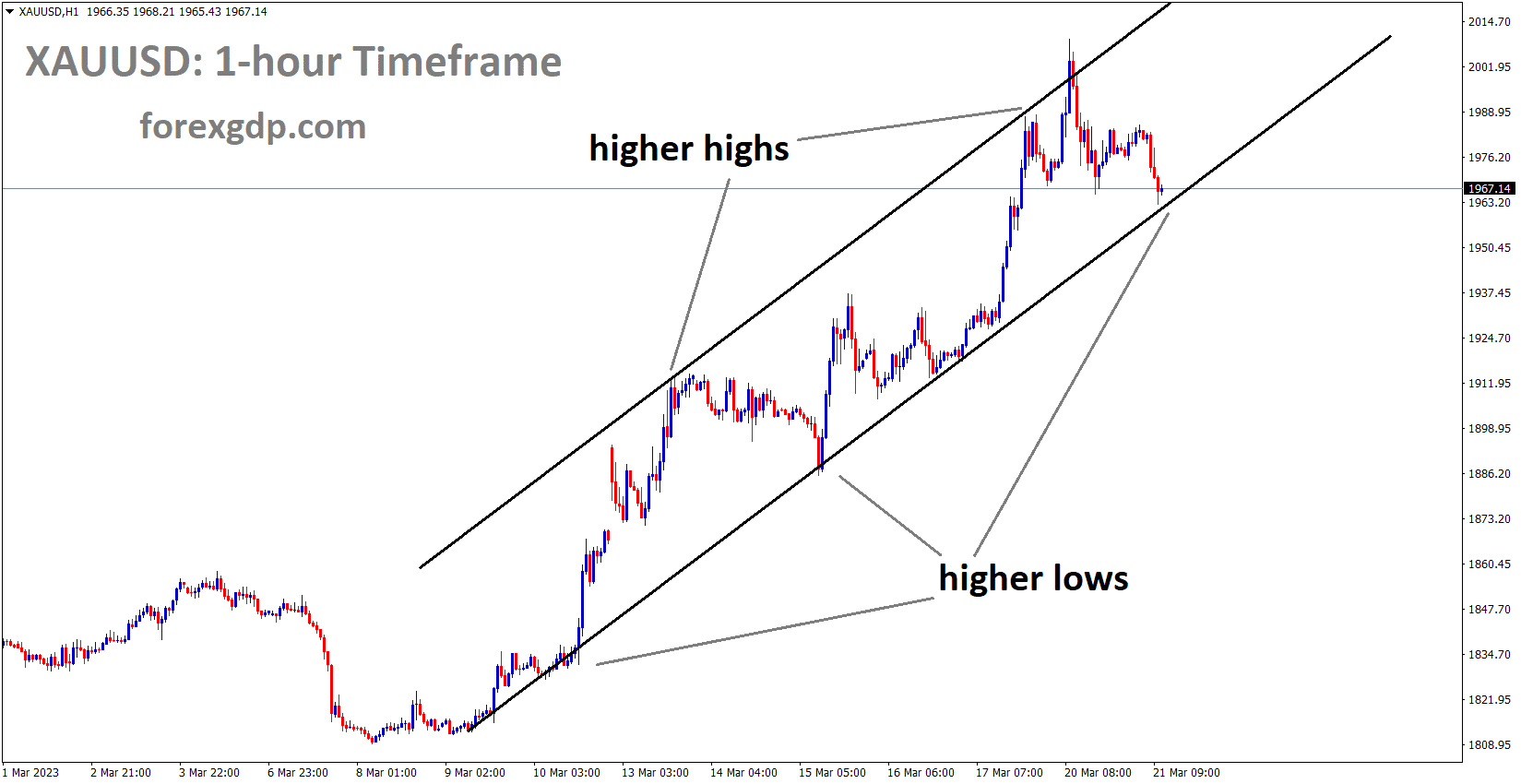

GOLD Analysis

XAUUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

After Credit Suisse bank defaulted and received assistance from the SNB for the default sum of CHF 50 billion, gold price reached the one-year area of $2010 the previous day. This news was unable to calm the yellow metal’s surging and market fears.

Banks are getting assistance from the Big Banks and Central Banks to maintain market stability, but the demand for yellow metal has not decreased.

As markets continue to process the effects of the Credit Suisse-UBS deal and wider concerns for banks with weak balance sheets, gold reached a one-year high overnight, just shy of US$ 2,010 per ounce. While First Republic Bank once again collapsed during the Wall Street cash session, large-cap banks saw significant gains. Given the uncertainty surrounding possible contagion, the price action may indicate that the market is looking for quality assets. Despite the terms of those notes being very different from those of the Credit Suisse bonds, other European bank AT1 bonds have also been hit severely and are currently trading near zero. Additional Tier 1 (AT1) Bonds are superior to equity but have no maturity date and are ranked below all other debt securities. With all this chaos, the precious metal’s supposed haven status seems to have increased its luster.

Yesterday’s four-week bottom for the US Dollar helped XAU/USD even more. Following the sell-off last week, Treasury yields have stabilized, and real yields have gained some of the territory they had lost in advance of the Federal Open Market Committee (FOMC) meeting on Wednesday. Although it is not yet completely priced in, the futures and swaps markets are leaning toward a 25 basis point increase. The Fed is in a pickle because it is unclear how many other banks and corporations could be susceptible to the tightening monetary conditions they have established to control the sky-high inflation. Gold has increased since SVB Financial collapsed, while the US Dollar and real rates have declined. The VIX and GVZ indices, which reflect equity and gold volatility, have both increased due to the unpredictability of the current situation. If these circumstances persist, the yellow metal may be supported and the record high of US$ 2,075 an ounce may be in sight.

USDCHF Analysis

USDCHF is moving in the box pattern and the market has fallen from the resistance area of the pattern.

Credit Suisse will receive $3.25 billion from UBS institutions, and additional funding will be secured from the SNB.FED already set a 50 basis point rate increase for this month, but as global banks tank, borrowing costs are continuing to fall. This can help finance the default banks at lower rates of interest. After Credit Suisse’s failure, the Swiss franc is weaker this week against the US dollar.

While UBS has consented to acquire troubled Credit Suisse for $3.25 billion with additional support provided to the purchaser by the Swiss National Bank. The integrity of the financial system was questioned following the failure of SVB, leading to a sell-off of banking stocks. Since then, unrest has spread to other significant players, such as First Republic Bank, which was given a $30BN rescue plan by a group of 11 big banks. Following the release of Japan’s inflation data on Thursday, the FOMC economic forecasts and Fed rate decision will be carefully watched on Wednesday.

Even though the Federal Reserve alluded at another rate increase of 50 basis points earlier this month, the likelihood of a forceful action has been greatly diminished due to worries about financial instability. The central bank is now in a challenging position to balance the demands of their dual mission while allaying concerns about a recession. The figures over the past eight months have shown encouraging signs of easing, even though inflation is still significantly higher than the Fed’s goal rate of 2% (it is presently at 6%). But up until now, the Fed has been able to execute strict monetary tightening without experiencing any significant consequences due to a healthy labor market. That is, until financial problems emerged at Silicon Valley Bank, Credit Suisse, and First Republic Bank, which were partly brought on by increasing borrowing costs. But since the ECB raised rates by 0.5% last week, the likelihood of a 25 bp (0.25%) increase is now 62%. The Dollar seems to lack credibility because these predictions are already factored in, which strengthens the safe-haven Yen.

USDCAD Analysis

USDCAD is moving in the Descending triangle pattern and the market has rebounded from the horizontal support area of the pattern.

Due to the market-wide decline in oil prices, the Canadian dollar continues to perform poorly. Oil buyers continue to put pressure on the markets because the financial industry is afraid. Today’s scheduled CAD CPI data is below expectations, which holds the currency further down and causes a reversal if it is higher.

In order to prolong the early Asian session recovery from a one-week low going into Tuesday’s European session, USDCAD picks up bids to refresh daily top around 1.3690. In doing so, the Loonie pair supports the recent US Dollar recovery advance of the country’s important inflation data for February while also applauding the declining price of WTI crude oil, Canada’s main export earner. WTI retreats to the 24-month low recorded the day before, holding lower ground near the intraday bottom around $67.20. The US Dollar’s recovery and looming concerns about the financial sector’s consequences both put pressure on the price of black gold.

Crude Oil Analysis

Crude Oil is moving in the Descending channel and the market has rebounded from the lower low area of the channel.

With that said, the US Dollar Index recovers from the lowest levels reached since early February, recorded the day before, breaking a three-day downtrend, and was mildly bid at around 103.40 at press time. In order to entice buyers, the US dollar index against the six most important currencies tracks the late-Monday recovery in US Treasury bond yields as well as the hawkish Fed bets. Although the UBS-Credit Suisse deal and policymakers’ attempts to contain the banking crisis weighed on the US Dollar and earlier favored USDCAD bears, the market’s uncertainty regarding the most recent steps taken to protect bank depositors appears to be undermining the risk-on stance.

As the US 10-year and two-year Treasury bond yields recovered from the lowest levels since September 2022 on Monday, it should be observed that they are still inactive but have maintained the previous day’s rebound from a multi-day low. Additionally, the likelihood of a 0.25% Fed rate increase on Wednesday is near 75% according to CME’s Fed Watch tool, up from 65% last week. In light of this, the S&P 500 Futures show modest gains to convey cautious optimism even as traders search for definitive guidance. Moving forward, despite talk of a policy shift, the Bank of Canada Consumer Price Index for February appears to be the crucial statistic that traders of the USDCAD pair should pay attention to.

USD Index Analysis

US Dollar Index is moving in the Descending channel and the market has fallen from the lower higher area of the channel.

Because the FED is expected to raise the interest rate by 25 basis points at its meeting tomorrow, the US Dollar index is increasing day by day.

The failure of SVB and Signature banks has increased US banks’ anxiety, but the FED is prepared to allay their concerns about prospering in the markets.

All significant institutions gave the First Republican Bank $30 billion, which has restored trust in US dollar buyers.

Focusing on the FOMC gathering is USD Index. In spite of some slight selling pressure in the risk complex and the flat performance of US yields across the curve, the index has so far reversed three straight daily pullbacks, including Monday’s drop to multi-week lows around 103.30. The likelihood that the Fed will raise rates by 25 basis points on Wednesday is currently around 80%, according to CME Group’s Fed Watch Tool, though investors are expected to closely monitor any indication from the Committee that the Fed might pause its tightening cycle in the relatively near future. The recent loss of momentum in some US factors and the ongoing deflation that has been observed since July 2022 seem to support the aforementioned in some way. The Existing Home Sales report for February will be the only noteworthy data publication in the US.

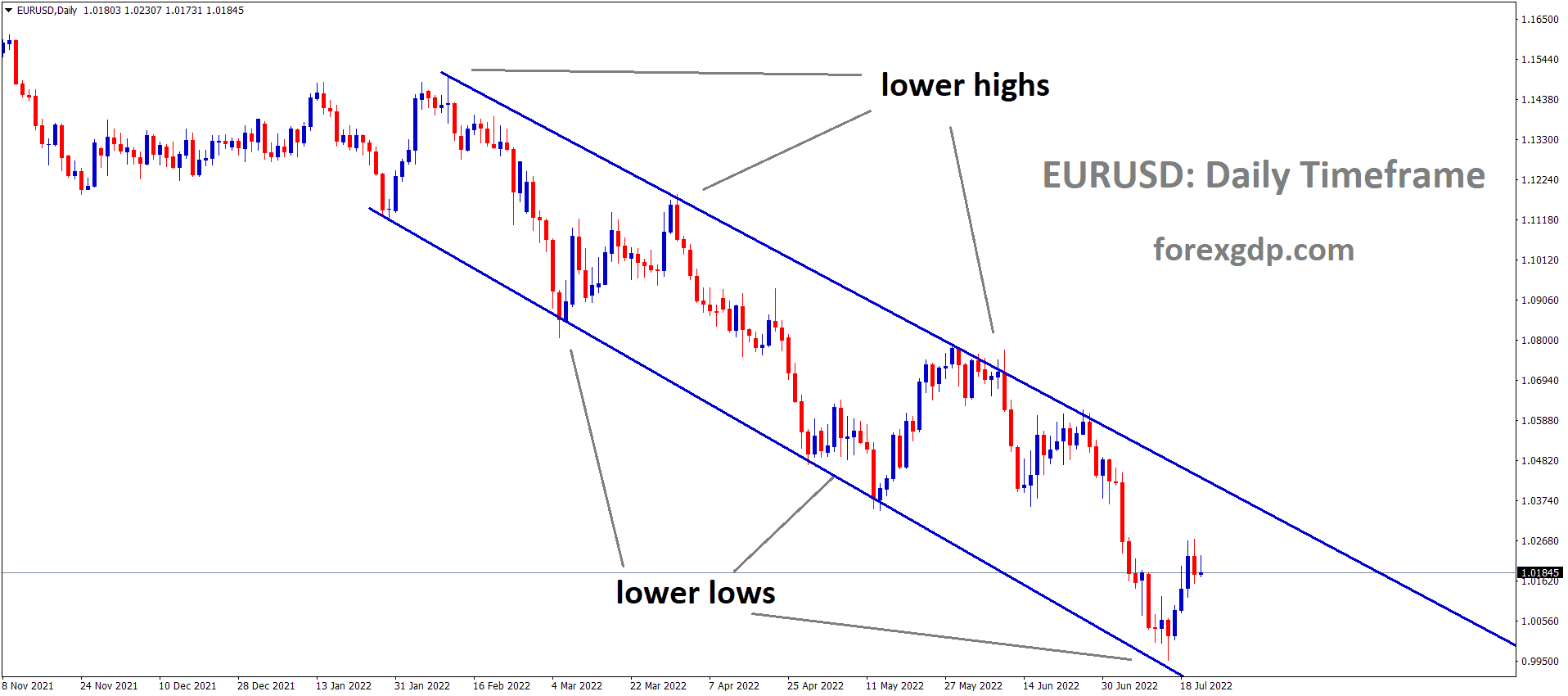

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

After major banks in the US and Switzerland experienced problems, the EURUSD is up. A 50bps increase this month by the ECB, which is at a strong point in financial circumstances, raises the possibility of lower inflation across Europe.

The problems facing the banking industry were very much on the thoughts of market participants as the Euro began a new trading week. According to reports, UBS AG, the largest lender in Switzerland, has agreed to pay $3.2 billion to acquire Credit Suisse, its troubled domestic competitor, while also taking on significant losses from the latter. Following the failure of Silicon Valley Bank and the saving of First Republic Bank by significant American lenders, the financial sector is suffering on the global equity market, and with it, a general appetite for risk.

According to the US Federal Reserve, it will work with other significant central banks to guarantee global banking liquidity. This is a positive step, to be sure, but it also evokes unsettling memories of previous financial crises, and it’s obvious that market players are wondering if any more banking dominoes will fall as a result. The European Central Bank’s (ECB) half-point interest rate raise from last week, which came with strong indications of additional increases to come, gave the euro a boost, has temporarily faded as European stock markets opened lower, following Asian bourses lower.

The decrease The worst week for European equities so far this year ended on Monday morning. The major scheduled economic event for the upcoming week will originate in the US, not Europe. On Wednesday, the Fed will reveal its monetary policy choice for March. Despite the turmoil in the banking industry, the Federal Open Market Committee is anticipated to raise borrowing costs for the ninth meeting in a run, with a quarter percentage point increase anticipated. The Fed is still dealing with the same issues that other central banks are dealing with as the economy weakens and inflation stays stubbornly elevated. Consumer prices in the Eurozone increased at an annual rate of 8.5% in February, scarcely changing from January. The “core” measure, which excludes the erratic impacts of food and fuel, increased by 5.6%, exceeding the 5.3% increase in January. The official inflation goal set by the ECB is only 2%.

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Due to DUP leader Donaldson’s declaration that the Brexit deal’s Northern Ireland Protocol is insufficient to uphold our commitments, the UK pound is now on edge over the Brexit Deal disappointment. As a result, only half of the MPs are voting for the deal.

However, UK PM Rishi Sunak worked arduously to complete the Brexit Deal despite NI procedure.

The banking catastrophe puts the Bank of England’s hawks to the test. Despite UK Prime Minister Rishi Sunak’s valiant efforts to reach an agreement regarding the Northern Ireland Protocol, the looming worries of another Brexit setback are also putting the Cable pair buyers to the test. The Bank of England will be forced to abandon an interest rate increase this week due to turmoil in the global financial markets, according to numerous analyst estimates reported in The Telegraph. The predictions became too significant before Super Thursday because some people on the floor anticipated a 50 bps rate increase from the BoE, or “Old Lady,” as she is affectionately known. However, according to Democratic Unionist Party Leader Sir Jeffrey Donaldson, as reported by BBC News, the agreement was insufficient to address the issues his party had made regarding post-Brexit trade regulations for Northern Ireland. When MPs are given a chance to vote on a portion of the agreement on Wednesday, the DUP has stated that it will reject the Windsor Framework.

In other places, the US Dollar appears to have been drowned and market mood favored by prospects of easing the banking crisis. The market’s concerns were allayed when UBS purchased the ailing Credit Suisse for 3 billion Swiss francs (£2.6 billion). A subsidiary of New York Community Bancorporation will assume the deposits of Signature Bridge Bank, according to comments made on the same line by the US Federal Deposit Insurance Corporation. The market’s risk-on attitude was further strengthened by the news that five major banks, including the BoE, joined the US Federal Reserve (Fed) to alleviate the US Dollar liquidity crunch through currency swaps.

However, it should be noted that a senior Swiss lawmaker cautioned on Monday that “the UBS-Credit Suisse merger is an enormous risk,” which prompted the market to question the pessimists amid its apprehension before this week’s major data/events. In light of this, the US Dollar Index fell to its lowest points in a month and US Treasury bond rates continued to be under pressure. Additionally, Wall Street ended on a positive note with the gold price regaining its year-to-date peak before declining as far as $1,980. Moving on, Cable traders should keep a watch on risk catalysts for a new impulse before the Bank of England’s top-tier results on Thursday and the Federal Open Market Committee’s monetary policy meeting on Wednesday.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

The RBA Meeting Minutes are still a little optimistic about interest rates in the months to come, which causes the AUD to fall against the USD today.

Future expectations may include the RBA pausing the rate increase or reducing it to 25 basis points due to the robust labor market, higher-than-expected inflation, and higher-than-expected wage growth.

The Australian currency remains weak below 0.6700 and is anticipated to continue falling as the publication of the Reserve Bank of Australia minutes has shown that policymakers are not as hawkish as had been speculated on the open market. Members noted that Australia’s inflation stayed too high, the labor market was extremely tight, and wage growth had picked up as they deliberated the policy choice. Surveys kept pointing to favorable business circumstances. Additionally, despite the Australian economy’s persistent inflation, RBA policymakers weighed the 25 bps option.

The RBA policymakers are concerned that the monthly Consumer Price Index may continue to fluctuate from month to month despite having slowed from its peak of 8.4%, which was reported in December, according to the minutes of the meeting on inflation guidance. S&P500 futures are continuing to trade with some minor losses that were added during the Asian session. On Monday, the 500-stock index of the US rebounded significantly as investors anticipated the Federal Reserve would maintain its current monetary policy. Fed Chair Jerome Powell may decide to refrain from commenting on interest rates in order to control the effects of escalating banking stress because doing so could fuel concerns about additional financial turmoil. The street thinks that, even in the most hawkish case scenario, the Fed won’t raise interest rates by more than 25 basis points because restoring investor confidence has also taken priority for them. As a result, the US Dollar Index is struggling to continue its recovery move above 103.44.

NZDUSD Analysis

NZDUSD is moving in an Ascending triangle pattern and the market has reached the higher low area of the channel.

The New Zealand Dollar continues to consolidate at a lower level before tomorrow’s FED Decision. In addition to a 25 bps rate increase this month, a rate reduction of the same amount is anticipated for the second half of 2023. China maintains its unchanged exchange rate policy for New Zealand shipments to China.

The NZDUSD pair continues to decline for the second straight day on Tuesday, extending the overnight modest retreat from the 0.6280 region, or over a one-month high. Early in the European session, the corrective decline continued unabatedly. Bears are now waiting for a sustained decline below the round-figure level of 0.6200 before making new bets. A downward pressure is being felt on the NZDUSD pair as the US Dollar regains some positive momentum and ends a three-day losing run to its lowest level since February 14. However, a new leg down in US Treasury bond yields combined with dwindling prospects for a more active tightening of monetary policy by the Federal Reserve (Fed) could weigh on the value of the dollar. Aside from this, a generally optimistic risk tone may help, at least temporarily, to contain losses for the risk-averse Kiwi.

The failure of two middle-sized US banks, Silicon Valley Bank and Signature Bank, stoked rumors that the US central bank would moderate its hawkish posture in order to avoid additional economic pressure from high interest rates. The markets actually give a higher probability of a smaller 25 bps lift-off in March and even a rate reduction by the Fed in the second half of the year. This further lowers US bond rates, which should prevent the greenback from appreciating significantly. In the meantime, investors’ confidence is increased by the news that UBS will save Credit Suisse in a $3.24 billion deal, which helps allay concerns about the danger of widespread contagion. This is clear from a continued rise in the value of global equity markets, which tends to undermine conventional safe-haven investments and may help to further cap the dollar. However, market participants are still concerned about a full-fledged banking catastrophe. This may prevent traders from setting up positions for the NZD/USD pair’s expected recovery from its recent bottom of 0.6085, which it reached earlier this month and represents the pair’s lowest level since November 17.

The publication of Existing Home Sales data is included in Tuesday’s US economic schedule and could give the early North American session some momentum. The outcome of the highly anticipated two-day FOMC monetary policy meeting, due to be announced on Wednesday, will, however, continue to be the center of attention. This will be crucial in determining the near-term USD market dynamics and the next leg of the NZD/USD pair’s directional shift.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Members of the Bank of Japan Policy Committee voted against ending the ultra-easy monetary policy given the current economic climate, which has made the JPY pair weaker than its counterparts.

The anticipated Japanese CPI is 4.1% lower than the previously reported figure of 4.3%. The sharp decline in oil prices is providing more support for JPY inflation this month.

After successfully holding the key support level of 161.00 during the early Tokyo session, the GBPJPY pair has gained momentum. The cross is attempting to increase its gains above 161.70 as hopes of the Bank of Japan ending its ultra-loose monetary policy have drastically diminished. According to the BoJ Summary of Opinions that were made public on Monday in connection with the March monetary policy meeting, board members supported the need to maintain an ultra-loose monetary policy for the time being, even as some cautioned about the need to carefully consider its side effects, such as declining market functions, according to Reuters.

Future Japan inflation statistics will be closely scrutinized. According to projections, the yearly headline Consumer Price Index will drop from its previous release of 4.3% to 4.1%. In addition, an increase to 3.4% is predicted for the core CPI, which excludes the cost of food and energy. The previous reading was 3.2%. Examining inflation figures reveals that while the impact of higher import prices is still present, it is less pronounced than the impact of higher energy and food prices. The Japanese government’s recent attempts to raise wages in order to maintain inflation at desired levels may have also contributed to the rise in the core CPI.

Investors in the UK are anticipating the publication of the country’s CPI data on Wednesday. A lack of workers and higher food costs have been the main causes of the UK’s extremely sticky inflation. The UK government has undoubtedly suggested some steps to encourage people to put off their retirement plans. But enough time will be needed for effective implementation. The Bank of England’s interest rate choice will be the main catalyst this week, causing the cross to experience extreme volatility. The Bank of England will likely choose to make one last 25 basis point hike on Thursday if it can, according to analysts at ING Global, despite encouraging signs that inflationary pressures are easing. However, this will surely depend on what occurs in the financial markets. As opposed to the Federal Reserve and the European Central Bank, the BoE has established a much lower standard for pausing hikes.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/