GOLD Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel.

The current gold price is close to $2070 per ounce. The peak in August of 2020 is in jeopardy. Weakness in the US Dollar is reflected on the market as domestic data from the US continues to underperform expectations. The Federal Reserve Funds Rate is currently between 475 and 500 points, but is likely to rise to 525 to 550 points if the 25 basis point rate hike in May, the rest in June, and rate decreases starting in July are seen this year, with a projected rate of 425 to 450 points by the end of 2023. Rate hikes that are less restrictive are good news for non-yielding investments like gold.

Gold’s continued ascent can be attributed to the declining value of the US dollar and the widespread belief that US interest rates have already reached or are very close to their maximum level. With a new record high so close at hand, the precious metal is sure to garner even more interest. As speculators continue to factor in the likelihood of an interest rate drop later this year, the value of the US dollar declines. Current expectations place a 25bps increase in the Fed Funds rate from its current range of 475-500 at the May FOMC meeting, with the rate remaining unchanged in June and rate reductions beginning in July. By the end of the year, Fed Funds are expected to be between $425 and $450, according to the most recent forecasts from CME Group. The dollar is weakening against other currencies that are still in a tightening trend because of this anticipated relaxation of Fed monetary policy. One such currency is the Euro, and recent ECB talk indicates that the central bank will keep raising interest rates to combat inflation. Because the European Central Bank is still in tightening mode, the Euro’s share of the US Dollar Index is expected to increase, leading to a lower US Dollar.

SILVER Analysis

XAGUSD Silver Price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

There are two major US economic announcements scheduled for later today: retail sales and Michigan consumer confidence. The Michigan consumer sentiment survey is a key indicator of consumer expectations, prospects, and economic outlook, while retail sales data is a key indication of activity on the high street. If either misses or exceeds projections, the market may react negatively or positively.

USD Index Analysis

USD index is moving in the Descending channel and the market has reached the lower high area of the channel.

Due of impending data from the US domestic market, counter pairings are penalising the US Dollar. The US PPI data and this week’s US CPI data both came in below expectations, sending the US Dollar down versus other major currencies. Yellow metal may halt in the second half of 2023 after reaching a high near 2020 due to expectations of a rate hike.

Over the past 24 hours, the US Dollar has been smashed, extending the most severe decline since early March. Australian and New Zealand dollars that are sentiment-linked fare better than their major equivalents. The DXY Dollar index is down more than 1% so far this week. This would be the worst five days since early January if losses persisted. Gold rocketed to record-setting heights. The most recent US inflation report is to blame for the drop in the greenback this week. In contrast to the 5.1% projection, the headline CPI gauge unexpectedly decreased to 5.0% y/y. However, the core indicator increased from 5.5% to 5.6%. Meanwhile, wholesale inflation data for the US during the past 24 hours largely fell short of predictions.

The Federal Reserve’s rate hike in May may be the final one it makes in this tightening cycle due to the ongoing dampening of inflation. Traders are likely clinging to a scenario where the economy can withstand the shock of the most aggressive tightening in decades because of the labour market’s resilience. Markets also keep betting that the central bank would lower rates this year. In light of this, there isn’t much possibility of a significant economic event for the US Dollar as the week comes to an end on Friday during the Asia Pacific trading session. For traders, this can make sentiment more important. Therefore, if regional indexes maintain their upward trend, it may continue to cool interest in the US Dollar as a safe haven.

USDJPY Analysis

USDJPY is moving in an Ascending triangle pattern and the market has reached the higher low area of the pattern.

Ueda, governor of Japan’s central bank, suggested at a G20 summit that Japan’s central bank ease monetary policy this month. There is no sign of a liquidity crisis in Japan’s banking sector or other financial institutions. Wage price hikes in Japan are expected to grow by 2% this year, bringing headline inflation to 3%. Since a slowdown is necessary for economic growth, the IMF has already warned of a severe global recession.

The news that Bank of Japan governor Kazuo Ueda told the G20 that Japan’s current core consumer inflation rate of roughly 3% is anticipated to fall back below 2% in the second half of this fiscal year has made its way across the wires. We warned our G20 partners to keep an eye out for threats to the financial system, such as those posed by the nonbank sector and their potential international repercussions.

We expect global GDP to pick up after a period of slowing, notwithstanding the IMF’s warning that a catastrophic global recession is a risk scenario. The IMF has identified a severe global recession as a danger scenario, but our outlook is for growth to rebound following a slowdown. We anticipate continued salary growth in Japan as a result of an improving global economy.

BoJ assured the G20 it would keep its existing monetary easing in place. I’d want to give it some thought before returning to Japan for the BoJ’s April policy meeting, but it’s only been a week since I took office as governor, and I’m now abroad on business. Inform G20 that Japan’s current core consumer inflation rate of roughly 3% is expected to drop back below 2% by the end of the current fiscal year.

USDCAD Analysis

USDCAD is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Tiff Macklem, governor of the Bank of Canada, stated that rate pauses are required in order to examine the growth and inflation rates. If necessary, rate reduction will also be considered in the second part of the inflation decline.

According to OPEC+, global oil consumption will increase by 2.32 million barrels per day by 2023, and output would decrease from 86,000 barrels per day to 28.80 million barrels per day.

After re-testing its two-month low early on Friday in Europe, the USDCAD has found stability around 1.332025. As a result, the Loonie pair follows the sluggish performance of the price of WTI crude oil, Canada’s primary export, and celebrates the decline of the US dollar. The cautious tone before the important US consumer-centric data tends to prod the pair traders as of late, nevertheless. WTI crude oil is holding on to little gains near $82.50 despite the markets being very quiet. It’s important to note that black gold buyers are having a hard time being reassured by predictions of rising Oil demand and supply reduction in the midst of economic slump worries. According to Reuters’ reporting, the Organisation of the Petroleum Exporting Countries kept its global oil demand growth prediction for 2023 at 2.32 million barrels per day in its monthly report released on Thursday. OPEC oil output fell by 86,000 bpd in March to 28.80 million bpd, the report noted.

However, greenback bears are making a push towards the 100.80 level, hovering around 100.85 at the very latest, sending the US Dollar Index tumbling below the February low for 2023. In this way, the dollar’s relative strength against the other six major currencies reflects the market’s less hawkish view of the Federal Reserve’s aggressive moves, which is mostly attributable to the negative effects of recent US inflation and employment data. However, at -0.5% MoM, the US Producer Price Index for March fell to a four-month low, missing expectations of a 0.0% MoM decline. And despite market expectations of 3.0%, the PPI YoY dropped to 2.7% from 4.9% in prior readings. The fact that the US Initial Jobless Claims report climbed to 239K from 232K projected and 228K previously further hurts hawkish Fed bets and the US Dollar. The dismal US figures released on Thursday mirrored the weaker US CPI readings seen in recent months. The Minutes from the most recent Federal Open Market Committee Monetary Policy Meeting were released on Wednesday, and they highlight the Fed officials’ reluctance to back more rate hikes. S&P 500 Futures struggle after posting the largest daily gain in two weeks amid these moves, while US 10-year and 2-year Treasury note rates fall to 3.44 percent and 3.96 percent, respectively.

Tiff Macklem, governor of Canada’s central bank, recently attempted to defend the status quo on monetary policy by stating, We need a time of poor growth. According to BoC Governor Macklem, the market generally anticipates a reduction in the Bank of Canada’s policy rate sometime this year. As of right now, we don’t see that as the most likely outcome. In the future, USDCAD traders should keep an eye on the March US retail sales report, the April Michigan consumer sentiment index, and the University of Michigan’s 5 year Consumer Inflation Expectations report. However, unless the expected data produces a huge positive surprise, the bears are likely to retain control.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel.

According to several reports from the IMF meeting in Washington, the West will see greater recession panic in 2023, which would put pressure on the US Dollar. Russia and China decided to keep using the Chinese Yuan for imports and exports rather than peg them to the US Dollar as a result of the BRICS meeting. This week, a -0.20% MoM decrease in Swiss producer and import prices for March is anticipated. Due to a US liquidity crisis, the Swiss Franc faced off against a basket of major currencies.

Early on Friday, USDCHF declines to 0.8885 after a corrective bounce from 0.8860 the day before. As a result, the Swiss Franc pair diminishes the recovery from its lowest point in 27 months despite widespread US Dollar weakening. The pair’s further decline appears to be constrained by the market’s cautious stance ahead of the crucial Swiss and US inflation reports. However, as the dollar bears target the 100.80 level—roughly 100.90 at the time of press—the US Dollar Index prods the lowest level of 2023 recorded in February.

The recent weak US inflation data, which disproves the necessity for higher Federal Reserve interest rates and, consequently, weighs on the US Dollar and the USDCHF price, may be responsible for the greenback’s most recent losses. Given that, The US Producer Price Index for March fell on Thursday to a four-month low of -0.5% MoM, down from the previous readouts of 0.0% and 0.0%, while the PPI YoY fell to 2.7% from 4.9%, below market expectations of 3.0%. The Consumer Price Index previously declined to its lowest point since May 2021, to 5.0% YoY in March from a prior 6.0% and below 5.2% market expectations. However, the annual Core CPI, or the CPI excluding food and energy, increased to 5.6% YoY during the aforementioned month, exceeding the previous 5.5% and meeting expectations.

In addition to hints about US inflation, discussions of Fed policymakers, as indicated by the most recent minutes of the Federal Open Market Committee Monetary Policy Meeting, give USDCHF bears hope. The cause may be related to the Minutes’ statement that the banking sector’s unrest has reduced expectations for rate increases. With the exception of May’s 0.25% rate hike, the Minutes did not provide any new information and cast doubt on the aggressive Fed actions. Furthermore, numerous comments made by representatives of the world’s central banks at the World Bank Spring Meeting and the International Monetary Fund imply that the West is more likely to experience a recession than other regions. The US dollar is under pressure due to weaker inflation figures. Additionally, the USDCHF price is under downward pressure because to expectations for an Asian economic recovery and efforts by Russia, China, and Brazil to undermine the US Dollar’s standing as a reserve currency.

In light of this, despite Wall Street’s firmer closing, S&P 500 Futures print modest losses by press time. Additionally, the US 10- and 2-year Treasury note yields undermine the DXY’s recovery from the previous day and put downward pressure on it. After that, the US Retail Sales for March, the Michigan Consumer Sentiment Index for April, and the University of Michigan 5-year Consumer Inflation Expectations will influence movements in the USD/CHF. Swiss Producer and Import Prices for March are predicted to remain constant at -0.2% MoM.

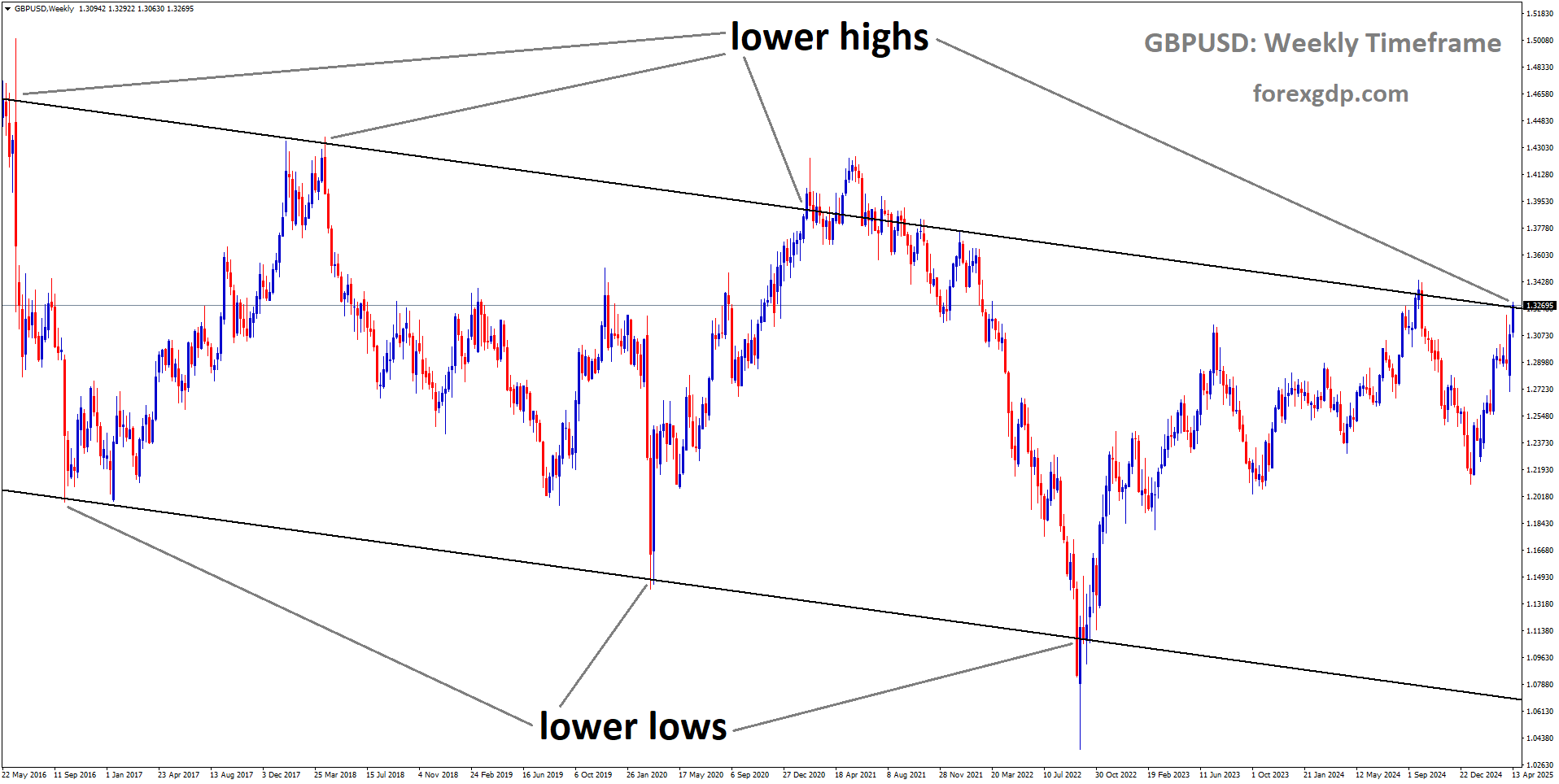

GBPUSD Analysis

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

According to Bank of England Chief Economist Huw Pill, energy price decreases in the second half of 2023 will reduce inflation in the United Kingdom. First-quarter GDP in the UK is anticipated to fall by 0.10% in 2023. Due to widespread fear of a recession in the United States, the value of the British pound has been steadily rising against the US dollar over the past few days.

At their best points in ten months, GBPUSD bulls pause while pushing their way to 1.2520-30 early on Friday. As a result, even as bulls look for further signs to continue the recent run-up, the Cable pair remained firmer for the fourth straight day after reaching its March 2022 peak the previous day. In contrast to mixed domestic statistics, the GBPUSD praised depressing US inflation data to illustrate the recent uptrend to the multi-day high. The Michigan Consumer Sentiment Index for April, the University of Michigan 5 Year Consumer Inflation Expectations for the current month, and a cautious attitude in advance of Friday’s US Retail Sales for March appear to be challenging the pair purchasers lately. The claims that the Bank of England hawks are losing steam could be on the same track.

The US Producer Price Index for March fell on Wednesday to a four-month low of -0.5% MoM, down from the 0.0% forecast and previous reading. In addition, the PPI YoY decreased to 2.7% from 4.9% in prior readouts, falling short of market expectations of 3.0%. The US Initial Jobless Claims report, which increased to 239K versus 232K anticipated and 228K before, is another factor impacting on the hawkish Fed wagers and the US Dollar. Despite this, the UK’s February 2023 GDP contracted to 0.0% from 0.1% predicted and 0.4% in January. Meanwhile, industrial production increased year over year but decreased month over month during the specified month. Additional information points to a rise in the trade deficit and no change in the February Index of Services figure of 0.1% compared to the anticipated -0.2%. The UK NIESR GDP Estimate for March increased to 0.1% from -0.1% anticipated and before.

The previous day, the GBP/USD values rose as UK Finance Minister Jeremy Hunt hinted that an election might be held as early as spring 2024 because he believes the economy has turned the corner. His later remarks, such as We do not believe a US trade agreement is imminent, however, seemed to test the bulls. Additionally, according to Reuters, Bank of England Chief Economist Huw Pill stated on Thursday that they continue to anticipate a decline in Consumer Price Index inflation in the second quarter as a result of last year’s sharp increases in energy costs being excluded from the annual comparison. According to bank officials, the precise path of inflation may be bumpier than anticipated, and they also estimate the GDP to contract by 0.1% in 2023 Q1 with the addition of BoE’s Pill.

Despite the firmer closing of Wall Street, S&P 500 Futures print minor losses by the press time. Additionally, the yields on US 10 year and 2 year Treasury bonds dampen the previous day’s recovery and put downward pressure on the DXY. In event of a happy surprise, the aforementioned US data may allow the US Dollar to lick its wounds. The scale of the GBP/USD drop, however, is constrained until Silvana Tenreyro of the BoE, who voted in favour of delaying the rate hike at the most recent monetary policy meeting, uses dovish language when speaking at the IMF Spring Meetings.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel.

Both the unemployment rate and inflation are declining in the Eurozone. According to Reuter reporting, a 25 to 50 bps rate hike is anticipated at the May monthly meeting, according to ECB Governing Council member Bostjan Vasle. The US feels greater pressure from first unemployment claims, which increased to 239K from 232K and 228K previously. In the short and medium term, the Euro is supported by the US Dollar weakness.

In the May meeting, ECB policymaker Pierre Wunsch said that a rate increase of 25 or 50 basis points was possible. This year, the ECB might discontinue reinvesting proceeds from the Asset Purchase Programme in order to promote liquidity savings more. This year, the ECB isn’t likely to decrease interest rates anytime soon.

The early European session is seeing a back-and-forth movement on the EURUSD pair near 1.1070. As the US Dollar Index struggles to hold onto its downward momentum, the main currency pair is anticipated to continue moving northward towards the round-level resistance of 1.1100. The higher-than-expected softening of the US Producer Price Index report increased the need to pause the cycle of policy tightening faster than previously anticipated, and the USD Index remained under the control of bears on Thursday.

In the Asian session, S&P500 futures have produced slight losses. US stocks were significantly acquired on Thursday after the announcement of an exceedingly sluggish PPI report, which made it necessary to reevaluate expectations of another rate hike at the Federal Reserve’s May monetary policy meeting. The general market sentiment is rather upbeat as expectations for the Federal Reserve’s adoption of a neutral stance have grown. In addition, March’s lower petrol prices have raised hopes that the S&P 500 businesses will post strong quarterly earnings. In spite of below-average petrol prices, businesses must maintain lower input costs, which would have increased operational profit margins.

In anticipation of a drop in US consumer inflation expectations, the demand for US government bonds has modestly increased. The yield on US 10-year Treasury notes has fallen below 3.44%. Examination of the US PPI report revealed that, due to lower petrol costs, the US headline PPI significantly decreased from 4.6% to 2.6%, falling short of both predictions of 3.0% and the previous release of 4.6%. As anticipated by market participants, the core US PPI stayed stable at 3.4%, which is significantly less than the previous report of 4.8%. Businesses offered goods and services at lower rates outside their factories as a way of passing on the benefit of decreased input costs brought on by lower petrol prices to end consumers.

This will reduce overall retail demand in terms of value and may prompt the Federal Reserve to consider pausing rates earlier. The US Department of Labour published a rise in weekly initial jobless claims data on Thursday, signalling that the US labour market conditions have further eased. The economic data increased from 228K in the previous release and projections of 232K to 239K. This has also lessened worries about persistent US inflation. In addition, according to Bloomberg, US commercial banks cut back on borrowing from two Federal Reserve backup lending facilities for a fourth consecutive week as liquidity restrictions ease in the wake of Silicon Valley Bank’s failure last month. Jerome Powell, the head of the Fed, would be forced to scale down rate decreases due to the synergistic effects of the tight credit conditions, softening US Consumer Price Index and PPI, and easing labour market.

Pierre Wunsch, a policymaker at the European Central Bank, stated on Friday that the magnitude of the policy decision in May will depend largely on core inflation for April. Reinvestments under the asset purchase programme may come to an end completely this year. Although the terminal rate’s market pricing is appropriate, no immediate rate reduction are likely to follow.

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has reached the higher low area of the channel.

The annual rate of inflation in the United States was 2.7%, which was lower than expected. Initial jobless claims in the United States were 239K, compared to the 232K expected. As a result of fewer forecasts of rate hikes in 2023, the US Dollar gains ground. China’s economy is strengthening as a result of the pandemic, which has aided New Zealand imports and exports to China. The RBNZ rate hike of 50 basis points this month has lifted the New Zealand Dollar against other currencies.

On Thursday, the NZD/USD formed a bullish engulfing candlestick pattern, which boosted an already substantial increase of 80+ points and sent the pair to a new five day high. Today weakness in the US Dollar can be largely attributed to the downward trend in inflation in the US and a softening labour market. After falling to a low of 0.6203, the NZDUSD is currently trading at about 0.6290. The mood in US stocks is optimistic. The argument for a Fed pivot is strengthening as producer price inflation has slowed and jobless claims for the week of April 8 have above projections. The core Producer Price Index fell 0.1% MoM in March, missing expectations of a 0.3% increase, while the overall PPI was -0.5% MoM, down from 0% in February. Annually, the PPI was 2.7%, which was lower than expected, but the core PPI was 3.4%, which was in line with predictions.

Meanwhile, the US Department of Labour said that first jobless claims for the previous week were 239K, which was more than the 232K that had been predicted. The number of people filing new claims decreased to 1.81 million in the week ending April 8. With the US Dollar weakening, the NZDUSD soared from roughly 0.6240 to its daily high of 0.6299. The US Dollar Index showed that the greenback hit a yearly low of 100.846 before recovering to 101.022, a loss of 0.50%. The yield on the 2 year US Treasury note has fallen by 2 basis points to 3.945% as investors anticipate one more rate hike from the US Federal Reserve before halting. The CME Fed WatchTool currently places the probability of a rate hike by the Fed at 66.5%, which is lower than the 70.4% odds it had on April 12th.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel.

Following the release of poor US PPI data, the Australian Dollar rose. The RBA predicted rate hike or lack thereof will depend on Australian inflation statistics due on April 26.

Overnight, after US PPI sent markets into a tailspin and the US Dollar faced renewed pressure to the downside, the Australian Dollar jumped higher again. Commodity prices and the Australian and New Zealand dollars gained the most. Final demand for US PPI fell short of expectations in March, coming in at 2.7% year over year instead of the 3.0% expected and 4.6% earlier. The month-over-month reading for March came in at -0.5%, much below the 0% and -0.1% expectations.

Treasury rates stayed put while equity indices, commodities, and high beta currencies like the Aussie and Kiwi rose. The day finished with the back of the curve higher by a few basis points. The probability that the Federal Reserve would raise interest rates by 25 basis points in early May has not budged in the interest rate market and is still hovering around 70%. With PPI falling further below CPI, businesses have the opportunity to either increase their profit margins or pass the savings on to customers. Whatever the case may be, it was well received by the financial markets.

Gold and silver both hit new highs on the commodity markets as the optimistic mood spread, as did most industrial metals. Since the stock market and commodity prices have been rising, the Australian and New Zealand dollars have followed suit. This may be a reflection of the difference in monetary policy between the RBA and the RBNZ, but the AUDNZD pair has struggled to stay above 1.0800. While the RBA is projected to keep rates steady at its May 1 meeting, the interest rate market anticipates a 25 bp increase from the Fed in late May.

Inflation reports from both countries’ central banks are due in the next weeks, and they may prove decisive for the AUDNZD pair’s future course. Despite the most recent quarterly CPI print in Australia being higher than New Zealand’s, the RBNZ has kept its benchmark rate at 5.25%, 165 basis points higher than the RBA. The RBA has been defending its dovish stance by pointing to the monthly inflation gauge, which is less reliable. They will maintain their stance if the quarterly CPI statistic released on April 26 is in line with expectations, but they may have to reevaluate their position if the number comes in significantly higher than expected.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/