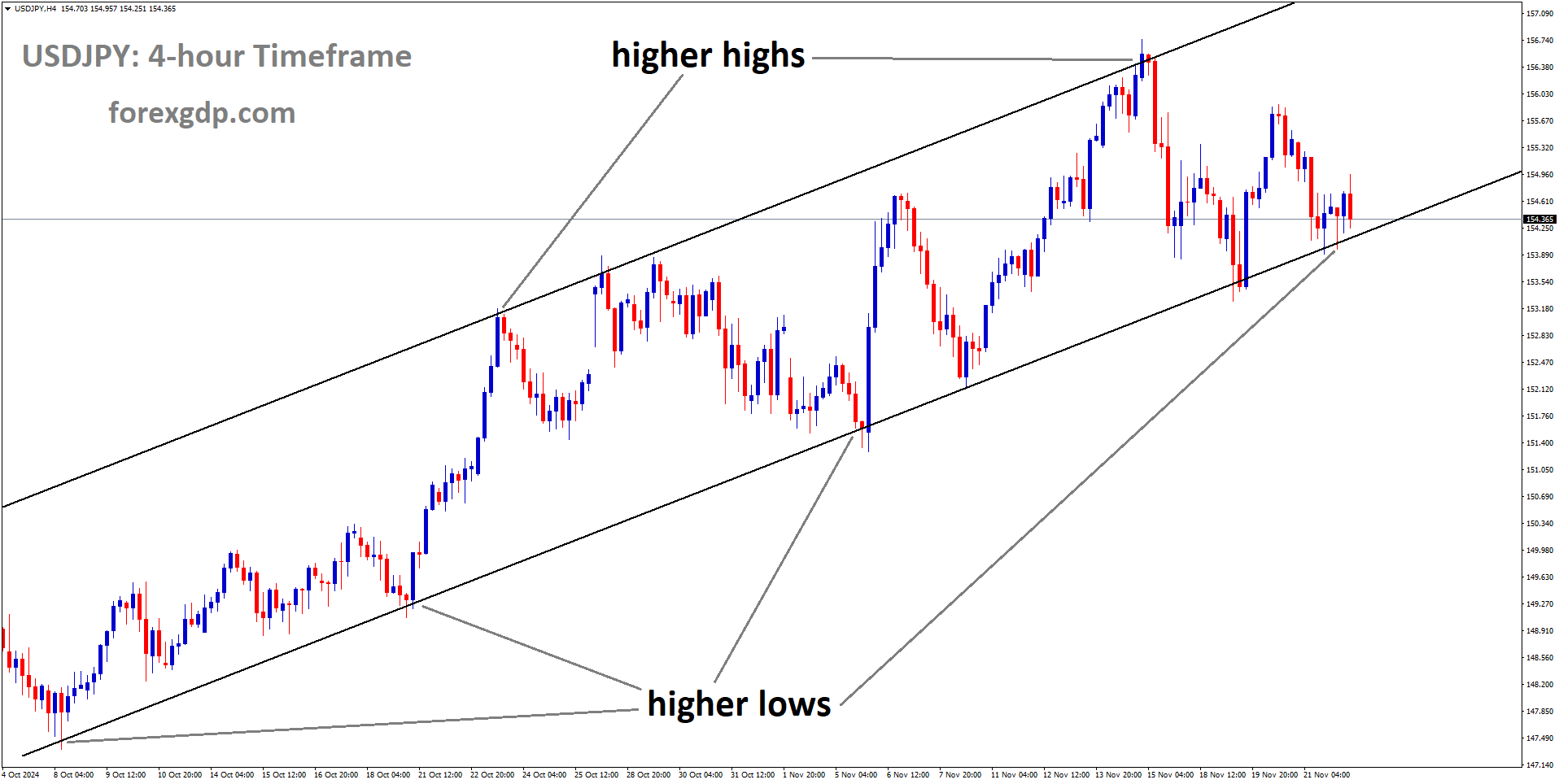

EURUSD Analysis

EURUSD has broken the Descending channel in upside.

Germany, the primary industrial centre of the Eurozone, has now entered a recession, and the ECB is anticipated to raise interest rates by 25 basis points this week. Even so, wage growth and employment are higher in European regions, and the 6.2% inflation rate in Europe is well above the desired range of 2-3%.

Although the direction of improvement may not be significant, particularly in the underlying metric, it is anticipated that US inflation will continue its downward trend. This might indicate that the Federal Reserve should take additional action to reestablish price stability. According to market projections, the annual headline CPI for May is expected to decline to 4.1% from 4.9%, while the core indicator—which excludes food and energy is expected to have decreased to 5.2% from 5.5%. The U.S. dollar performs better and risky assets perform worse as the numbers increase. In recent weeks, the Federal Reserve has taken a more circumspect stance and hinted that it may keep interest rates unchanged in June in order to better understand the economy’s laggard effects of cumulative tightening. Investors anticipate no change in monetary policy as a result next week. Trading participants should not completely discount the possibility of another 25 basis-point increase despite market pricing, as other central banks are beginning to act more aggressively again. For instance, the Bank of Canada started raising borrowing costs again last week after holding steady for two months, admitting that its stance is insufficiently restrictive to bring back price stability. Given the resiliency of the American economy, the Fed risked making a serious error by pausing too soon. For instance, policymakers might need to quickly exit the sidelines and resume larger and unconventional hikes if the break allowed inflation to pick up steam and become more entrenched. This would be an unnecessary and preventable risk at this time.

EURJPY Analysis

EURJPY is moving in an Ascending triangle pattern and the market has rebounded from the higher low area of the pattern.

To be the devil’s advocate, if the FOMC decides to hit the pause button to avoid shocking traders, the move would not necessarily be negative for the U.S. dollar as it might be accompanied by a more hawkish policy outlook. In this case, the dot-plot might include two additional 25 bp hikes for 2023 and no cuts through 2024. Overall, longer periods of higher rates should be favourable for the dollar.The European Central Bank is anticipated to raise interest rates by a quarter point at its June meeting, across the Atlantic. Since this choice has already been fully discounted, traders should concentrate on the underlying message and tone to determine where the terminal rate will ultimately go. The ECB may err on the side of caution and refrain from providing an aggressive assessment of the policy outlook given that regional inflation is declining and the German economy is in freefall. Markets may interpret this as a sign that the tightening campaign is coming to an end and that there will only be one more hike after that.

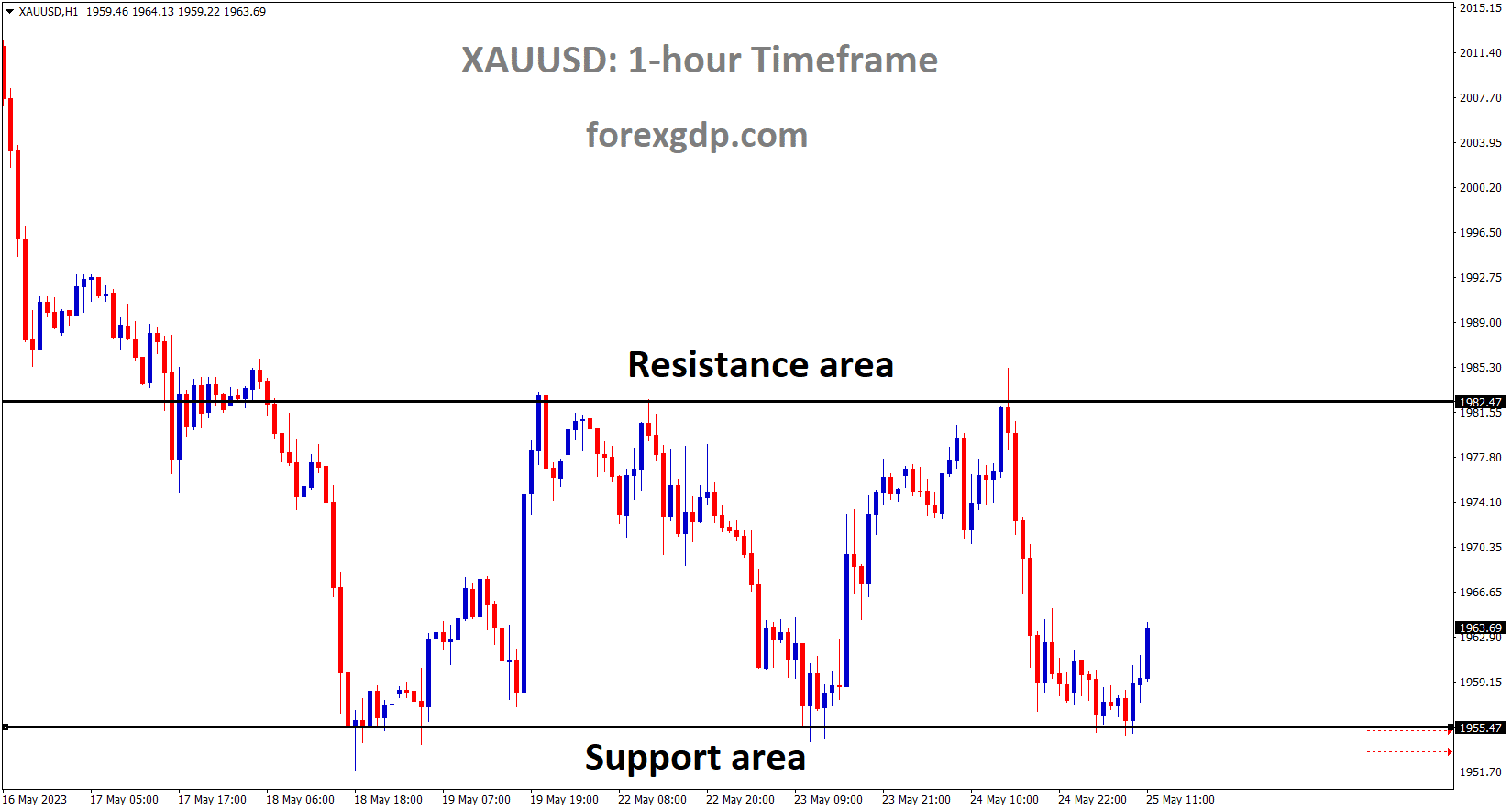

GOLD Analysis

XAUUSD Gold price is moving in the Box pattern and the market has rebounded from the Horizontal support area of the pattern.

Prior to this week’s FED Interest rate and US CPI data, gold prices are range-bound. Gold prices increased as China’s economy slowed down, selling more gold and providing more stimulus to the country’s economy.

The week is expected to end with higher gold prices, but the move is anything but convincing. For the majority of the week, the precious metal fluctuated between $1940 and $1970, as continued repricing of US Federal Reserve rate hike probabilities weighed on gold’s valiant attempt at recovery. The Reserve Bank of Australia and the Bank of Canada surprised the markets this week by raising interest rates by 25 basis points (bps) each in response to ongoing concerns about price pressure. Market participants are now assessing the likelihood of a hot CPI print from the US on Tuesday, the day before the Federal Reserve decides on interest rates, as a result of this. A strong CPI reading could make things more difficult for the Federal Reserve and raise the level of uncertainty before the meeting. Will the Federal Reserve take the ‘Hawkish’ pause or will it follow the RBA and BoC and hike rates now.

SILVER Analysis

XAGUSD Silver Price is moving in an Ascending channel and the market has fallen from the higher high area of the channel.

Market participants will undoubtedly welcome the busy economic schedule in the coming week from the perspective of volatility. The Federal Reserve is still divided over the best course of action, and there will likely be heated discussions about whether to take a break or continue raising interest rates by 25 basis points. There have been some recent indications that the economy may be starting to slow down, but wage growth remained stable at 0.3% despite an increase in unemployment in May. However, the NFP print exceeded expectations, providing the Fed doves with ammunition for their meeting on Wednesday. The likelihood of a hike could increase and Dollar bids could start before the FOMC meeting, which could thwart Gold’s attempt to move towards the $2000 level if the US CPI data significantly beat estimates.

USD Index Analysis

US Dollar index is moving in an Ascending channel and minor box pattern , market has reached the support area of the Box pattern.

The US dollar dropped last week as a result of the FED delaying this week’s rate hike because US initial unemployment claims came in higher than anticipated. In comparison to the previous reading of 4.9% y/y, US CPI data is predicted to decline by 4.1% y/y.

The US Dollar (DXY) suffered its worst 5-day performance since the middle of April last week, falling -0.47%. As the outlook for the stock market kept getting better, demand for the currency linked to havens declined. The S&P 500 index on Wall Street started a technical bull market after rising 20% from the most recent low. The Nasdaq 100 and Dow Jones both increased. The majority of DXY’s underperformance occurred on Thursday, when an unexpected rise in US unemployment claims dashed hopes of a Federal Reserve rate hike in July. Nevertheless, the data were insufficient to alarm financial markets about an impending recession, although this could change. The US Dollar faces two major economic event risks in the coming week. The US inflation report for May will be released on Tuesday. Due in part to the decline in commodity prices, headline CPI is predicted to move down from 4.9% to 4.1% y/y. Core inflation, which excludes volatile food and energy prices, is seen ticking down from 5.5% to 5.3% year over year.

Although the latter may annoy the Fed, overall, the data may still indicate that inflation is on the decline. The FOMC’s monetary policy statement for June will be announced the very next day, speaking of the central bank. It is widely believed that the Fed will maintain the current benchmark lending rates. However, it should be noted that the RBA and BoC have recently made hawkish announcements. The language used by the central bank regarding interest rates is where things will most likely get interesting. The reason for this is that the financial markets are currently pricing in a probability of about 2/3 that the Fed will continue tightening next month. As a result, you should not rule out the possibility that the US Dollar will turn higher in the coming week. Also keep in mind that haven demand may increase USD if economic conditions unexpectedly worsen.

USDCAD Analysis

USDCAD is moving in the Box pattern and the market has reached the horizontal support area of the pattern.

The Bank of Canada’s unexpected rate increase last week helped the CAD gain ground on its counterparts. Oil price outlook uncertainty makes the CAD supportive from its lows. This week, the Canadian Dollar may move in response to US CPI data and the FED FOMC meeting.

The USDCAD pair starts the new week slightly higher and appears to have temporarily ended a four-day losing streak that had brought it to a one-month low, near the 1.3315-1.3310 range reached on Friday. The lack of bullish conviction in spot prices, which have remained below mid-1.3300s throughout the Asian session, calls for some caution before positioning for any additional intraday appreciating move. For the third day in a row, crude oil prices have declined due to concerns that a slowdown in the global economy will reduce demand for fuel. As a result, the USD/CAD pair is expected to benefit from the weakening of the commodity-linked Loonie, though the upside is constrained by the US Dollar’s (USD) muted price action. In fact, the USD is unable to benefit from Friday’s modest recovery from the monthly low due to the uncertainty surrounding the Federal Reserve’s (Fed) rate-hike trajectory.

It is important to remember that in June, expectations for an impending break in the US central bank’s 12-month cycle of tightening policy were stoked by the recent dovish comments made by a number of Fed officials. The markets are still pricing in the possibility of a further 25 basis point lift-off in July, which benefits the dollar and supports the USDCAD pair. In contrast, traders appear hesitant and prefer to wait it out before this week’s key data/central bank event risks. The most recent US consumer inflation figures are scheduled for release on Tuesday, and the outcome of the two-day FOMC monetary policy meeting will be announced on Wednesday. However, in the absence of any significant market-moving economic releases on Monday from either the US or Canada, the Bank of Canada’s (BoC) surprise rate hike last week may continue to support the Canadian Dollar (CAD) and cap gains for the USDCAD pair.

GBPJPY Analysis

GBPJPY is moving in an Ascending channel and the market has reached the higher high area of the channel.

No changes to the policy framework were made at this week’s Bank of Japan meeting, according to Deputy Governor Wakatabe.

Due to the Bank of Japan meeting, where no changes are anticipated, JGB yields declined on Monday. JPY PPI index came in at 5.1% YoY versus a previous reading this week of 5.8%, which was lower than anticipated. Last week saw a decrease in Japan’s inflation rate, supporting the Bank of Japan’s decision to continue its ultra-easy monetary policy.

For the fourth day in a row, the GBPJPY is in the lead as bulls push prices to their highest levels since early 2016 in the early going of Monday’s European session. To support the market’s acceptance of the monetary policy divergence between the Bank of England (BoE) and the Bank of Japan (BoJ), the cross-currency pair prints modest gains in this manner. The firmer bond yields in anticipation of this week’s important data and events are strengthening the upward momentum. Hawkish concerns about the BoE are insufficient to explain the policymakers’ most recent statements, as Catherine Mann, a BoE official, stated earlier in the day that the UK government needs a long-term plan to protect future growth prospects. However, the UK’s Confederation of British Industry (CBI) trade group stated on Monday that although deep-seated issues like weak business investment will continue, Britain’s economy now looks likely to sidestep recession entirely this year. The BoE vs. BoJ divergence in favour of the GBPJPY bulls is maintained by the same factor—too high inflation in the UK compared to Japan.

In contrast, the Producer Price Index for Japan fell for the fifth consecutive month in May, from 5.8% in previous readings and 5.5% in market expectations, to 5.1% YoY. However, the monthly figures, which came in at -0.7% MoM instead of the expected -0.2% and 0.2%, also let down Yen traders. Masazumi Wakatabe, deputy governor of the BoJ, has ruled out any change in the BoJ’s monetary policy during this week’s meeting after seeing depressing inflation data for Japan, saying, “Do not expect a change from BOJ at this week’s meeting.” Bloomberg also points to significant selling pressure on Treasury bonds in order to support yields and GBPJPY prices. With bets that the Federal Reserve’s battle against inflation is far from over, hedge funds continued their record-breaking selling of short-dated Treasuries, according to the news. On the other hand, recent hawkish wagers in favour of the BoJ’s departure from the ultra-accommodative monetary policy appear to pose a threat to the GBP/JPY bulls. As investors increased their bets that the Bank of Japan will maintain its stimulus settings at its meeting this week, yields on Japanese government bonds decreased on Monday, according to Reuters. Moving on, Tuesday’s UK employment data will be crucial for those keeping an eye on the pair before the BoJ meeting on Friday.

CADCHF Analysis

CADCHF is moving in the Descending channel and the market has reached the lower high area of the channel.

UBS announced on Monday that it had successfully acquired Credit Suisse, with a balance sheet of $1.6 trillion. After this merger, people in the Swiss zone and elsewhere in the world started to have faith in Swiss banks and governments. After this Big Deal in Wealth Management, the Public had more hope because of the Guaranteed Funds and Swiss Government involvement.

On Monday, UBS announced that it had successfully completed its emergency takeover of struggling local rival Credit Suisse, forming a massive Swiss bank with a $1.6 trillion balance sheet and greater strength in wealth management. UBS Chief Executive Sergio Ermotti and Chairman Colm Kelleher stated that the largest banking transaction since the global financial crisis of 2008 would present “many challenges but also many opportunities” for clients, employees, shareholders, and Switzerland. According to an open letter that was published in Swiss newspapers, this marks the beginning of a new chapter for UBS, which bills itself as the largest wealth manager in the world, Switzerland as a financial hub, and the international financial sector. The letter also stated that they are confident in their ability to manage the takeover. The team will be in charge of $5 trillion in assets, giving UBS a dominant position in important markets where it would have otherwise taken years to expand its size and reach. The 167-year history of Credit Suisse, which has been tainted recently by scandals and losses, is also ended by the merger. On the last day of trading, shares of Credit Suisse increased by 0.9%, while those of UBS increased by about 0.8% in the early going. Together, the two banks employ 120,000 people around the world, though UBS has already announced it will be eliminating positions in order to cut costs and capitalise on synergies. In a rescue operation coordinated by Swiss authorities to stop a collapse in customer confidence from pushing Switzerland’s No. 2 bank over the edge, UBS agreed on March 19 to purchase the lender for a knockdown price of 3 billion Swiss francs ($3.32 billion) and up to five billion francs in assumed losses.

The conditions of a 9 billion Swiss franc ($10 billion) public backstop for losses from winding down portions of Credit Suisse’s business were agreed upon by UBS and the Swiss government on Friday. Given the deal’s size and complexity, it was a tight deadline that UBS met in order to give Credit Suisse customers and employees more security and prevent departures. The takeover will benefit shareholders and will not burden the tax payer, according to guarantees from both UBS and the Swiss government. They claim that protecting Switzerland’s reputation as a financial hub was another reason for the rescue, as the country would suffer if the failure of Credit Suisse led to a wider banking crisis.Two myths, namely that Switzerland was completely predictable and safe and that bank problems would not affect taxpayers, were debunked by the deal, which saw the state finance the rescue. According to Jean Dermine, professor of banking and finance at INSEAD, “it was supposed to be the end of too-big-to-fail and state-led bailout,” adding that the incident demonstrated that this crucial reform following the global financial crisis had failed.

According to Arturo Bris, professor of finance and director of the IMD World Competitiveness Centre, the rescue also demonstrated that even major international banks could experience brief episodes of bank panic that did not abate within a few days. After acquiring Credit Suisse for a small portion of its alleged fair value, UBS is expected to report a sizable profit in its second-quarter results on August 31. Ermotti has cautioned that the upcoming months will be “bumpy” as UBS continues to absorb Credit Suisse, a process that UBS has estimated will take three to five years. When presenting the first snapshot of the new group’s finances last month, UBS highlighted the significant risks by pointing out the uncertainty surrounding the tens of billions of dollars in potential costs and benefits. Many banks have scaled back their global ambitions since the global financial crisis in response to stricter regulations. The demise of Credit Suisse’s investment bank, which UBS has stated it will seek to drastically reduce, represents yet another European lender’s retreat from the securities trading industry, which is now largely controlled by American firms.A politically charged decision regarding the future of Credit Suisse’s crown jewel the bank’s domestic business may present Ermotti with his first challenge since being brought back to lead the merger.

Ermotti has suggested that the base scenario would be to fold it into UBS and combine the largely overlapping networks of the two banks, which could result in significant savings. However, UBS has stated that it is weighing all options because it must balance public pressure to maintain Credit Suisse’s domestic business with its own brand, identity, and, most importantly, workforce. According to analysts, public concerns about the new bank’s size with a balance sheet roughly twice the size of the Swiss economy—mean UBS may need to exercise caution to avoid being subject to even stricter regulation and capital requirements that its new scale would require. They also caution that UBS may find it difficult to keep customers and employees due to the uncertainty that comes with a takeover of this size and that it is still unclear whether the deal will ultimately benefit shareholders.

AUDCHF Analysis

AUDCHF has broken the Box pattern in upside.

Australian Dollar gained ground on US Dollar last week as a result of the RBA’s unexpected 25 bps rate increase. GDp for the first quarter came in at 0.20% as opposed to the predicted 0.30%. Iron ore commodity prices are rising from their lows; a rate hike in July may be delayed, and an increase in August is 80% likely.

The current Australian trade surplus is AUD 11.158 billion, less than the AUD 13.64 billion anticipated.

After the Reserve Bank of Australia unexpectedly raised its cash rate target by 25 basis points to 4.10% last week, the Australian dollar reached a one-month high. The move supported the Australian dollar on Tuesday, The RBA stated that additional monetary policy tightening may be needed to ensure that inflation returns to target in a reasonable amount of time, but that will depend on how the economy and inflation develop. The interest rate futures market anticipates a pause in July and a 25 bp increase at the monetary policy meeting in August with an 80% chance. Last week saw the release of the 1Q quarter-over-quarter GDP, which came in at 0.2% as opposed to the expected 0.3%. The previous print of 0.5% was revised up to 0.6%, which may have caused an offset in the most recent reading. At the end of December, the annual GDP was 2.3%, which was lower than the 2.4% forecast and 2.6% prior. The Australian economy is growing at a negative real rate of growth with inflation hovering around 7%. On the plus side, the trade surplus continued to boost the revenue in April, coming in at AUD 11.158 billion. Although it was less than the AUD 13.64 billion expected, it is still a good thing. Since the lows of last month, the price of iron and other industrial metals have been rising.

The Department of Agriculture, Fisheries and Forestry of the Australian Government has predicted that the harvests of wheat, barley, and canola will be 34%, 30%, and 41% lower, respectively, over the next 12 months. This follows several years of bumper crops brought on by excessive rainfall brought on by the La Nia weather pattern, which lasted for eight years. Beginning this winter in the southern hemisphere, the Bureau of Meteorology in Australia predicts a change to the drier El Nio pattern.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/