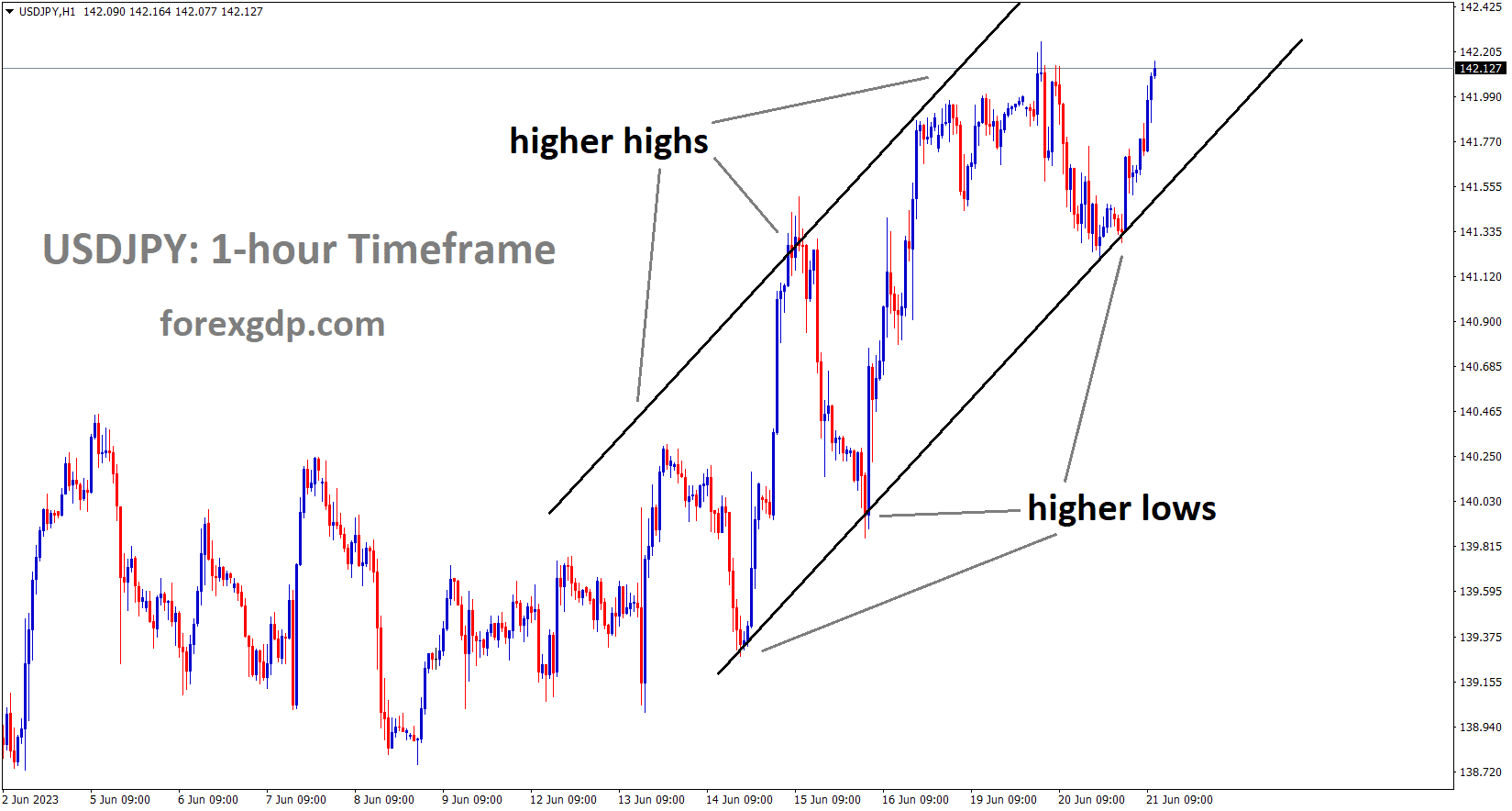

USDJPY Analysis

USDJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel.

Governor Ueda of the Bank of Japan stated that the monetary policy would remain loose until the 2% target was sustainably attained. The US banks’ losses to Japan are relatively small, and the Japanese economy is stable and slowly improving. In the middle of the current fiscal year, inflation will be moderate.

According to central bank governor Kazuo Ueda, the Bank of Japan will patiently maintain an easy monetary policy to stably and sustainably achieve the 2% price target accompanied by wage growth. Japan’s economy is strengthening. Economy of Japan is probably going to slowly improve. Overall stability of the financial system in Japan. Failures of US banks had little effect on the financial system in Japan. Consumer inflation in Japan is likely to start to decline in the middle of the current fiscal year.

GOLD Analysis

XAUUSD Gold Price is moving in the Descending triangle pattern and the market has reached the horizontal support area of the pattern.

Prior to Fed Powell’s testimony, which will be held today and tomorrow, gold prices have decreased. Fed Powell presents the semi-annual monetary policy report to the Senate committee on housing, banks, and urban affairs on Thursday and the US House of Financial Services today. Since rate increases are anticipated in July, the US dollar has risen against precious metals.

As the U.S. dollar strengthened ahead of Powell’s Congressional hearings and the release of remarkably strong May housing starts and building permits data, gold futures fell on Tuesday, falling about 1.3% to $1,945 in late morning trading. Wall Street might be persuaded by the U.S. economy’s resilient performance that the Fed will start raising borrowing costs in the second half of 2023, as predicted by its most recent guidance. Last week, policymakers left interest rates unchanged, but they also hinted at another 50 basis points of tightening through the end of the year. However, traders initially appeared to be dubious about these plans. Prior to the Fed Chair’s Congressional hearings later in the week, traders exercised caution. Powell will present the central bank’s semiannual monetary policy report, which can provide important insight into the outlook, before the U.S. House Financial Services Committee on Wednesday and the Senate Committee on Banking, Housing, and Urban Affairs on Thursday. Since not much has changed since the FOMC meeting in June, Powell is likely to reiterate that the fight against inflation is not over and that additional tightening may be necessary to reduce sticky price pressures. The U.S. dollar would increase as a result of a hawkish speech, which would hurt precious metals prices by raising yields and expectations for interest rates. In light of this, gold’s route may present less resistance.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel.

Due to the reading on inflation, the SNB would like to increase the rate by 25 basis points this week to bring it under the 0-2% level. The public has suffered more as a result of previous meetings’ massive rate increases. Last month’s decrease in inflation raised hopes that SNB would continue this month’s 25 bps rate increase.

When making their decision on Thursday, Swiss National Bank officials are unlikely to be discouraged by signs of weakening consumer price pressures and are likely to continue monetary tightening. Economists expect an increase in interest rates from the current level of 1.5% of at least a quarter point, despite the fact that inflation is now almost at their 2% ceiling and has never reached the levels seen elsewhere. Investors have factored in a larger half-point step in part. Due to its quarterly meeting schedule, the SNB’s tightening has lagged behind that of its major competitors in the US and the euro zone, where central bank decisions are made twice as frequently. Compared to the 400 basis points raised by the European Central Bank and the 500 basis points raised by the Federal Reserve, borrowing costs have increased by only 225 basis points in Switzerland under the leadership of Thomas Jordan since last June.

Despite the fact that inflation has slowed to 2.2%, officials maintain that Switzerland is still in danger. One incentive to act aggressively once more is the desire to catch up with peers. An underlying index that excludes volatile components like energy has fallen even lower, to 1.9%.Jordan has made it very clear that there is still inflationary pressure, according to economist Alessandro Bee of UBS Group AG, who forecasts a quarter-point increase. “If they do not leave the door open for another rate increase and more selling of foreign currency, I would be very surprised. A larger half-point move, one that exceeds recent ECB action, according to Bee, could perplex investors given Switzerland’s more moderate inflation environment.

EURCHF Analysis

EURCHF has broken the Box pattern.

He said that in order to make monetary policy sufficiently restrained and mitigate the risk of price pressure spreading, he could more easily envision increasing foreign exchange sales by 25 basis points from where they are now. Others do not share that opinion. A half-point increase is anticipated by a number of banks, including Credit Suisse and St. Galler Kantonalbank. An economist there named Patrick Haefeli predicts that Swiss policymakers will want to take more action right away before the cycle of global tightening reverses. According to him, the SNB will decide to take a slightly larger step right away to make up for it. “We think the window for increases will close in July or August because that is when both the ECB and the Fed will be reaching the end of their tightening cycles.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel.

The ECB decided to raise rates by three more times this year and increase standards by 25 basis points. Inflation in the Euro Zone is expected to decrease gradually, from 5.4% in 2023 to 3.0% in 2024 to 2.2% in 2023. Since there will be no meeting in August, a 25 bps rate increase by the ECB in July is anticipated.

The most recent ECB monetary policy meeting was reviewed by UOB Group economist Lee Sue Ann on June 15. While the ECB appears poised to hike rates once more in July, there is no meeting in August, and Lagarde stayed mum about what will happen in September. In September, new quarterly forecasts will present the ECB with another chance to review its stance on inflation and growth. As of right now, we are still anticipating a final 25bps hike in July. However, there is a higher than average risk of further rate increases after July. The ECB increased its forecasts for both headline and core inflation for this year and next year despite the recent slowdown in inflation. It now projects average headline inflation of 5.4% (up from 5.3% in 2023), 3.0% (up from 2.9% in 2024), and 2.2% (up from 2.1% in 2025). It is anticipated that core inflation will be 5.1% in 2023, 3.0% in 2024, and 2.3% in 2025.While the ECB appears poised to hike rates once more in July, there is no meeting in August, and Lagarde stayed mum about what will happen in September. In September, new quarterly forecasts will present the ECB with another chance to review its stance on inflation and growth. As of right now, we are still anticipating a final 25bps hike in July. However, there is a higher than average risk of additional rate hikes after July.

EURNZD Analysis

EURNZD has broken the Descending channel in upside.

Consumer confidence in New Zealand, measured by Westpac, increased to 83.1 in May from 77.7 in April. Due to higher interest rates and higher inflation rates in the economy, consumers have a low level of confidence. The RBNZ will meet again on July 12th, and last week’s GDP data showed a technical recession for the NZ economy.

Westpac consumer confidence in New Zealand increased to 83.1 in May, up from 77.7 in April and higher than the predicted 76.2 points. Although consumers continue to be pessimistic about the economy, this is still a low level. Even though household incomes were higher due to strong wage growth, the Westpac survey found that household finances were constrained for two reasons. First, the cost-of-living crisis has harmed households, as evidenced by the 6.7% increase in inflation over the previous year. Second, as mortgage rates skyrocketed, high interest rates had an impact on many households. A decline in consumer spending due to low consumer confidence would not be at all bad for the Reserve Bank of New Zealand, which needs the economy to slow in order to stop raising interest rates. The RBNZ will meet again on July 12; the benchmark rate is currently 5.50%. Due to two consecutive quarters of negative growth, as revealed by last week’s GDP report for the first quarter, New Zealand is technically in a recession.

This week’s data calendar in the US is incredibly light. The markets are anticipating Wednesday’s testimony by Jerome Powell before the House Financial Services Committee because there are no tier-1 releases on Tuesday. Given that the Fed paused last week after ten straight hikes but has indicated that it plans to resume raising rates at its meeting next month, Powell will likely face questions from lawmakers about the unconventional interest rate path of the Fed.

GBPCAD Analysis

GBPCAD is moving in the Descending channel and the market has reached the lower high area of the channel.

The Canadian dollar may gain support as oil prices recover. China also revealed a reduction in the purchase tax for the period 2024–2026. As a result, the US and China are once again at odds after US President Joe Biden accused Chinese President Xi Jinping of being a dictator. This is good news for oil buyers. As the US had broken its political promises to China, Chinese officials responded.

The top-tier Canadian and US catalysts ahead of Wednesday’s European session, and the recently firmer price of WTI crude oil, Canada’s main export good. However, the DXY struggles to continue the four-day downward trend due to conflicting worries about the Fed and the US-China trade war. China’s most recent efforts to combat the recession woes, including the People’s Bank of China rate cut and the Ministry of Finance’s announcement of lowering the purchase tax during 2024–2025 and 2026–2027, this favour the recovery of the oil price.The &P500 Futures halt the week-start retreat from the highest levels in 14 months, and WTI crude oil posts its first daily gains in three days around $71.60. Moving on, traders will be entertained by Canada’s monthly retail sales data for April before Fed Chair Jerome Powell’s biannual testimony.

GBPCHF Analysis

GBPCHF is moving in an Ascending channel and the market has reached the higher low area of the channel.

The May GBP CPI data (YoY) printout came in at the previous reading of 8.7% compared to the expected 8.4%. After today’s CPI data showed an increase, a rate increase by the Bank of England is now more likely.

The 8.7% YoY figure, the UK Consumer Price Index (CPI) for May increased past 8.4% market expectations. Nevertheless, the Core CPI, which does not include erratic food and energy prices, exceeded analysts’ expectations and earlier estimates of 6.8% YoY to show a 7.1% YoY increase in inflation for the aforementioned month. The positive UK inflation figures, along with the previously released positive British jobs report, suggest that the Bank of England will raise its benchmark interest rate again on Thursday. The UK inflation favours BoE hawks.nge to buyers of the GBPUSD pair.

Crude Oil Analysis

Crude Oil Price is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern.

Governor Ueda of the Bank of Japan stated that the monetary policy would remain loose until the 2% target was sustainably attained. The US banks’ losses to Japan are relatively small, and the Japanese economy is stable and slowly improving. In the middle of the current fiscal year, inflation will be moderate.

According to central bank governor Kazuo Ueda, the Bank of Japan (BoJ) will patiently maintain an easy monetary policy to stably and sustainably achieve the 2% price target accompanied by wage growth. Japan’s economy is strengthening. Economy of Japan is probably going to slowly improve. Overall stability of the financial system in Japan. Failures of US banks had little effect on the financial system in Japan. Consumer inflation in Japan is likely to start to decline in the middle of the current fiscal year.

AUDCHF Analysis

AUDCHF is moving in an Ascending channel and the market has reached the higher low area of the channel.

Australia’s Westpac Leading Index for May showed a reading of -0.27%, down from the previous reading of -0.03%. AUD is therefore losing ground to USD this week. Bullock of the RBA expresses confidence in a rate increase to curb inflation in his final speech.

The market’s preparations for this week’s major event, namely the twice-yearly testimony of Fed Chair Jerome Powell, may have contributed to the Aussie pair’s recovery during the early hours of Wednesday’s Asian trading session. It is important to note that the market sentiment is still risky and that the risk-barometer is available. The Reserve Bank of Australia’s Minutes, which are hawkish in contrast to the People’s Bank of China’s rate cut, and Assistant Governor Michele Bullock’s circumspect comments are also noteworthy. Recently, it was reported that US President Joe Biden had referred to Chinese President Xi Jinping as a despot on Tuesday. The remarks raise grave doubts about US-China relations after US Secretary of State Antony Blinken’s trip to Beijing produced few notable successes. The same should give Australian pair sellers reason for optimism.

The Australian Westpac Leading Index’s negative readings for May, which increased from -0.03% to -0.27%. A trick to increase confidence that inflation will return to normal sooner was how the RBA Minutes on the previous day defended the consecutive second hawkish surprise. RBA Deputy Governor Michele Bullock asserted that the RBA’s only tool for containing inflation is higher interest rates. The policymaker continued by saying that for a while, employment and the economy must grow below trend. It should be noted that sentiment deteriorated after the People’s Bank of China cut two important lending rates for the first time in almost a year, the Loan Prime Rate and the Medium-Term Landing Facility rate.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/