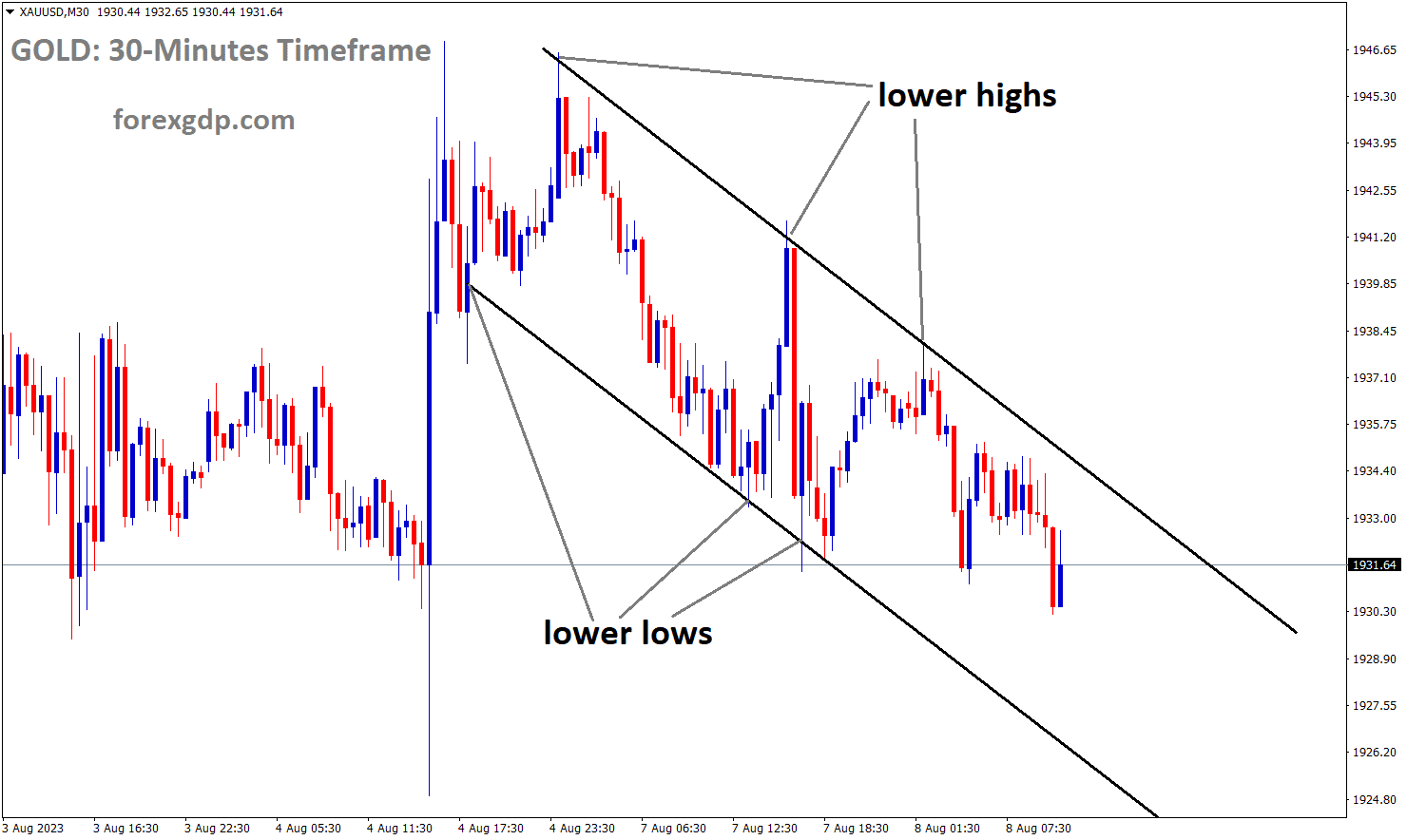

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel

The rise in the US dollar following the FED President’s speech caused the gold price to decline. Depending on the results of the decision-making process regarding the job data, a rate increase may occur in September or November.

Tuesday’s gold price continues to face some selling pressure for the second straight day and hits a new daily low in the $1,931 to $1,932 range during the Asian session. However, the XAUUSD maintains its position above a three-and-a-half-week low reached on last Friday. The likelihood of further Federal Reserve policy tightening helps the US Dollar USD gain some momentum, which is seen as a major factor weighing on the price of gold. In fact, market participants appear to be certain that the Fed will deliver one more rate hike of 25 basis points bps in either September or November, and their bets were confirmed by the US’s monthly employment report. Although the headline NFP was a little disappointing, strong wage growth and an unexpected decline in the unemployment rate indicated that the labour market remains tight. As a result, there is a greater chance that the US economy will experience a soft landing, which should allow the US central bank to maintain its hawkish outlook. Additionally, Fed Governor Michele Bowman stated on Monday that more rate increases will probably be required in order to bring inflation down to the central bank’s target rate of 2%. Bowman said in prepared remarks for a “Fed Listens” event in Atlanta that inflation is still too high and that job growth and other activity indicators show the economy has been expanding at a “moderate pace.” In turn, this maintains support for high US Treasury bond yields, which boost the US dollar and encourage capital outflows from the non-yielding Gold price. John Williams, president of the New York Fed, stated that the central bank will need to maintain its restrictive stance for a while.

XAGUSD Analysis

XAGUSD Silver price is moving in the Descending channel and the market has fallen from the lower high area of the channel

Williams, however, left open the prospect of a rate cut in early 2024, subject to the outcome of the economy. Additionally, he said that while he anticipated unemployment to rise slightly as the economy cooled, inflation was decreasing as hoped. This could prevent USD bulls from making risky bets and help the price of gold denominated in US Dollars suffer fewer losses. The most recent consumer inflation data from China and the US, which are scheduled for release on Wednesday and Thursday, respectively, may serve as a new catalyst for traders. Investors will be on the lookout for signs of deflation, which could temper expectations for further Fed rate increases and give the precious metal a modest boost. Surprisingly strong data should increase bets for one more Fed rate hike by the end of this year given that consensus estimates indicate a further easing of inflationary pressures. This could have a significant impact on the price of gold, which is seen as a hedge against inflation. Before setting up for a further decline in the price of gold, some caution is warranted given the conflicting fundamental backdrop. However, the emergence of new selling suggests that the decline seen over the past three weeks or so is still very much ongoing and that the XAUUSD’s path of least resistance is to the downside.

USDCAD Analysis

USDCAD is moving in the box pattern and the market has rebounded from the horizontal support area of the pattern

The NFP data from last week’s market-dominating performance of the US dollar indicates slower wage and job growth. As the US dollar strengthens and crude oil prices consolidate, the Canadian dollar declines.

After being rejected at the 100-day Simple Moving Average SMA of 1.3395 at the end of Monday’s session, the USDCAD pair ended the day flat at the 1.3370 area. On the one hand, the US Dollar gained strength due to rising US yields, while the CAD’s progress was constrained by falling oil prices. There was no pertinent data released at the beginning of the week, so markets continued to analyse Friday’s Nonfarm Payrolls NFPs from the US in July. The data revealed a slowdown in job growth and wage growth, but the lower-than-expected NFPs caused markets to sell off the USD. The US Treasury yields recovered during the session, helping the Greenback regain ground against its competitors. The 10-year rate increased by more than 1% to 4.09% after sharply falling on Friday, driving the pair higher.

All eyes are currently focused on the Consumer Price Index CPI figures for July, where markets anticipate an acceleration in the headline figure but a deceleration in the core measure. The Canadian calendar offered nothing pertinent in terms of the CAD. Throughout the session, the Loonie was under pressure due to the decline in West Texas Intermediate WTI and Brent barrel prices.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

According to State Economic Affairs (SECO), the unemployment rate for the month of July was 1.9%, the same as it was for the month of June. A weak employment report could force SNB to raise rates once more the following month.

In the opening hours of the Asian session on Monday, the USDCHF pair maintains modest gains. The pair is up 0.11% on the day and is currently trading at 0.8738. While investors wait for new momentum from US inflation data, the US Dollar Index DXY, which measures the USD’s value against six other major currencies, soars above 102.18. Michelle Bowman, the governor of the Atlanta branch of the Federal Reserve Fed, told Reuters that it is likely that more rate increases will be required to bring inflation back to the desired level. The New York Fed’s president, John C. Williams, predicted that interest rates would continue to decline in the upcoming 12 months. According to the data, total US consumer credit increased by $17.85 billion in June, exceeding market expectations of a $13 billion gain. It increased from $4,979.2 billion to $4,997.1 billion. US Nonfarm Payrolls increased 187,000 in July, which was worse than anticipated by 200,000. The unemployment rate decreased from 3.6% to 3.5%, and the average hourly wage exceeded the market expectation of 4.2% to come in at 4.4%. Market participants will follow market cues from the mixed employment and wage inflation data to the US inflation data due later this week. The Fed may decide to keep its hawkish stance and raise rates throughout the year if the data are stronger than expected.

The State Secretariat for Economic Affairs SECO in Switzerland announced on Monday that the country’s unemployment rate for July was 1.9%, in line with expectations. Its lowest level since October 2022, the figure remained unchanged from the June reading. Apart from that, the US-China relationship continues to be the main topic of discussion. In order to limit US investments in China in the high-tech industry, artificial intelligence, semiconductors, and quantum computing, US President Joe Biden is predicted to issue an executive order this week, according to Reuters. The Swiss Franc may gain from the heightened tensions between the world’s two largest economies while the USDCHF exchange rate may suffer. The US Consumer Price Index CPI for July is scheduled to be released on Thursday. The CPI MoM for July is predicted by the market to increase by 0.2% on a monthly basis. On Friday, the US Produce Price Index PPI will also be made public. Participants in the market will monitor the data and look for trading opportunities surrounding the USDCHF pair.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

Last day, FED Speakers Bowman and John Williams stated that rate increases were possible if domestic data performed well. Rate increases for FED are applicable based on incoming data. After the Speech, the euro loses ground to the dollar.

After Treasuries added a few basis points across the curve in the North American session overnight, the US Dollar rose against most other currencies as the Euro fell into Tuesday. Several Fed speakers made a few relatively hawkish remarks, which increased yields. President of the Federal Reserve Bank of New York John Williams stated that further rate increases were possible if necessary and that the policy would need to “be kept restrictive for some time.” Michelle Bowman, governor of the Federal Reserve, added, “I anticipate that additional increases will probably be required to bring inflation down to the FOMC’s target. Both of them reaffirmed what prior Fed speakers had said. This means that the incoming economic data will determine the rate path going forward. The notable mover today has been SD/JPY, which has re-established itself above 143.00. The growth-sensitive Australian and New Zealand dollars are also struggling. After Chinese trade data raised investor concerns about the Hong Kong economy, the Hang Seng Index (HSI) fell.

EURCHF Analysis

EURCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

While the trade balance for the month of July was higher than expected at USD 80.6 billion, both exports and imports fell sharply, raising worries for both domestic and international activity. APAC equity indices in general have been somewhat muted. With the WTI futures contract trading under US$ 82 bbl and the Brent contract trading under US$ 85.50 bbl, crude oil prices have slightly eased. Gold is stable near $1,930 USD. After the German CPI, the market will pay attention to US trade data. Harker and Barkin from the Fed will also be crossing the wires.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

Inflation in England will be achieved by the first half of 2025, according to Bank of England Chief Economist Huw Pill.By the second half of 2023, a 5% rate will be attained. In the second half of 2023, there was an increase in real wages.

Huw Pill, the chief economist at the Bank of England (BoE), stated on Monday that there are risks associated with UK inflation on both sides. He predicts that during the first half of 2025, inflation will most likely return to the target level. By the end of the current year, he anticipates the inflation rate to drop to 5%. According to Pill, real wages will increase in the second half of 2023. He noted that the most recent data indicated more persistent inflation, particularly as a result of food inflation that has persisted longer than previous bursts.

In the second quarter, consumer credit increased by 4%. The ratio of revolving to non-revolving credit rose to 3.0% from 7.1%. In June, the total amount of consumer credit increased to $17.85 billion from $4979.2 to $4997.1 billion. The actuals were higher than the $13 billion expected.

During the second quarter, consumer credit grew at a seasonally adjusted annual rate of 4%. Nonrevolving credit grew at an annual rate of 3%, whereas revolving credit increased at a rate of 7.1% annually. Consumer credit grew at an annual rate of 4.3 percent in June, according to data released on Monday by the Federal Reserve. When compared to market expectations of a $13 billion increase, total consumer credit increased by $17.85 billion in June, from $4,979.2 billion to $4,997.1 billion.

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has reached the higher high area of the channel

Due to the downgraded economic growth of the New Zealand economy this year, the RBNZ’s expected rate increase is more speculative.

In light of the worsening outlook for the New Zealand economy and the growing perception that the Reserve Bank of New Zealand (RBNZ) has stopped raising interest rates, the New Zealand dollar appears to have lost ground relative to some of its peers. In contrast to the RBNZ, which indicated in May that it would not be raising rates any further in the near future, the relative monetary policy appears to be shifting slightly in favour of the USD. This is because the US Federal Reserve is taking a data-dependent approach to future tightening. Additionally, although the outlook for US economic growth has improved recently, NZ growth projections for the current year remain downgraded.

Christian Hawkesby, the deputy governor of New Zealand’s currency, claimed that insurance companies handle claims from the general public in emergency situations such as prolonged illness, economic stress, and new pandemics well.

The Reserve Bank of New Zealand (RBNZ) announces the findings of its first stress test for the life insurance sector early on Tuesday in Asia, suggesting that the major players are well-positioned to weather the severe economic and insurance shocks while still honouring policy claims. RBNZ Deputy Governor Christian Hawkesby stated that the participating insurers were able to pay out sizeable claims from policyholders and maintain their financial stability during a hypothetical three-year scenario that included a protracted COVID, a new pandemic, and a period of extreme economic stress.

CHFJPY Analysis

CHFJPY is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The JGB Yields Curve remained at 0.50% above the free cap last week as a result of the Bank of Japan’s ultra-easy monetary policy, which caused JPY weakness against the USD. According to the BoJ’s official forecast, the market will experience inflation above 2%. Inflation is up due to demand generated by the economy.

Officials from the Bank of Japan (BoJ) sought to clarify that the slight yield curve adjustment announced on the 28th of July was a sustainable way to extend the current loose monetary policy. The Bank decided against making this level a cap and instead allowed the yield on 10-year Japanese Government Bonds to trade “flexibly” above 0.5%.

The slight modification was expected by international markets to be a first step towards a future policy normalisation as inflation and wages increase. BoJ officials are still not persuaded that the increase in inflation is being driven by demand and is likely to stay above 2% in a sustainable way. Therefore, it would seem that more work needs to be done before the Bank will be persuaded to change its course.

AUDCHF Analysis

AUDCHF is moving in the Descending channel and the market has reached the lower low area of the channel

China’s trade balance was $80.6 billion, higher than the $70.6 billion forecast and the $70.62 billion previous reading.

August’s Westpac consumer confidence for Australia was -0.40%, down from the previous reading of 2.7%. The NAB reading for the month of July increased from the previous reading of 9.0 to 10.0.

While tracing the stronger US Dollar to keep the bears on the table, the Aussie pair tries to explain the contradictory Australian and Chinese data.Despite this, China’s headline trade balance increased to $80.6 billion from $70.6 billion as expected and $70.62 billion previously. More information reveals that Imports fell -12.4% YoY, down from -6.8% previous readings and -5.0% market expectations, while Exports fell -9.2% YoY from -8.3% prior, down from -8.9% expected.Australia’s Westpac Consumer Confidence for August fell to -0.4% from 2.7% earlier in the day.

As opposed to this, the National Australia Bank’s (NAB) Business Conditions for July increased slightly to 10.0 from 9.0 the previous month and 8.0 market forecasts, while the NAB Business Confidence increased to 2.0% from -1.0% the previous month and 0.0% the prior.The recent market chatter about geopolitical concerns surrounding China, combined with the apprehensive atmosphere ahead of Thursday’s inflation hints from Australia and the US, weigh on the AUD/USD exchange rate. However, amid a light calendar and unimpressive yields, China’s warning against using the face recognition system joins the most recent Japan-China tension and the Sino-US disputes to dampen sentiment.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/