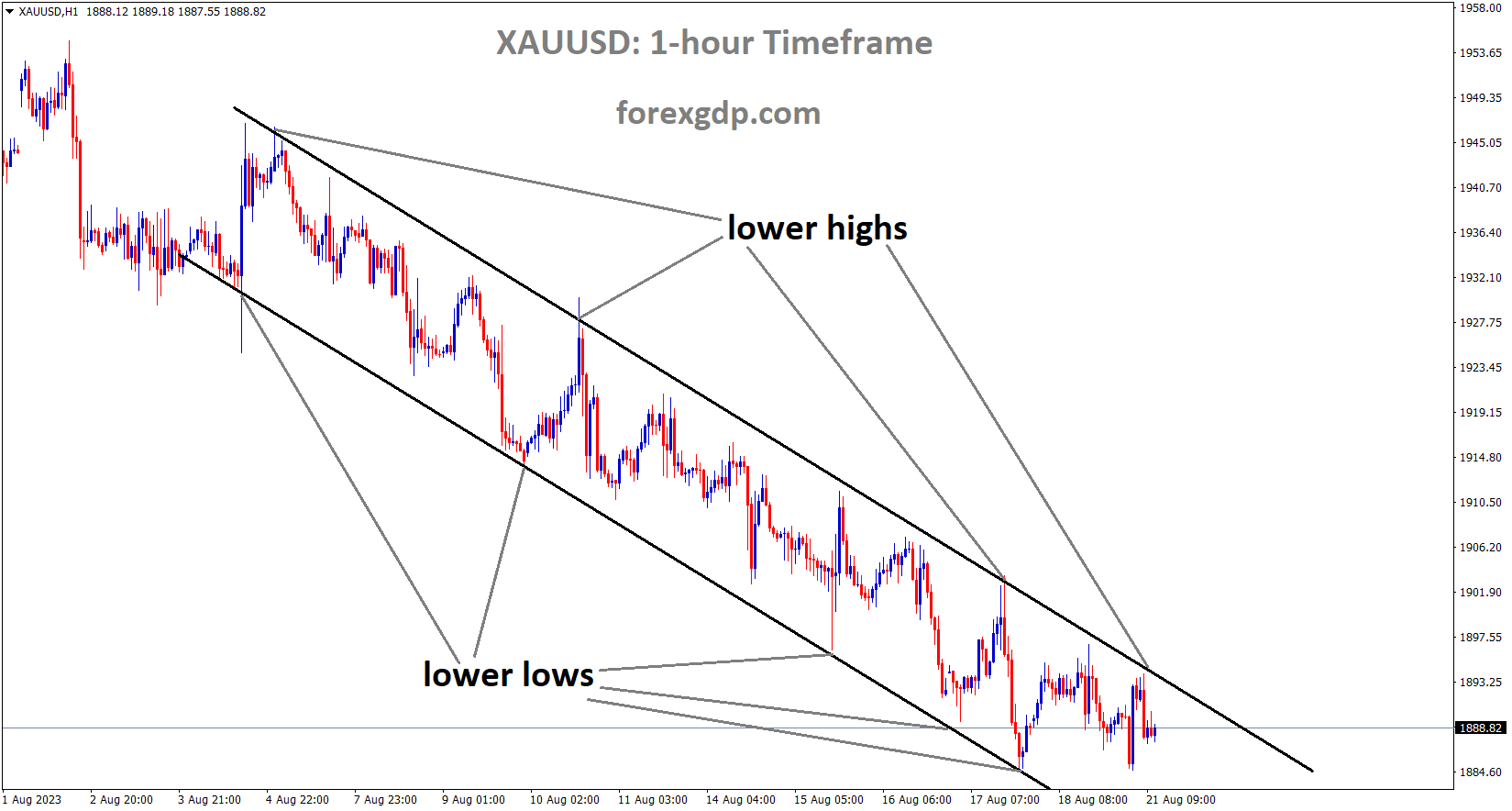

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel

Gold prices are declining in relation to the US dollar as a result of China’s severe real estate market issues. When businesses repeatedly fail to pay the public, the government has to sell gold to fund additional stimulus.

The price of gold struggles to rise and remains below $1,900 during Monday’s Asian session. Positive US economic data generally strengthen the US dollar, which puts some selling pressure on the XAU/USD pair. Consolidating its gains, the US Dollar Index (DXY), which compares the value of the USD against six other major currencies, hovers around 103.35. The People’s Bank of China (PBoC) made the decision earlier on Monday to keep the five-year LPR at 4.2% while reducing the one-year LPR by 10 basis points (bps) to 3.45% from 3.55%. The slowdown in consumer spending, declining credit growth, and a worsening property market have caused the Chinese recovery to lose steam and put pressure on policymakers to unveil additional fiscal stimulus plans. China is the world’s largest consumer of gold, so the encouraging developments surrounding the government’s plan could limit the downside of the metal.

Officials continue to have serious concerns about inflation, according to the Federal Open Market Committee (FOMC) minutes. Inflation is still too high. The Fed’s policymakers also stated that future rate decisions will be based on incoming data and that additional rate hikes might be required to meet the inflation target. The main event of the week will be Federal Reserve (Fed) Chairman Jerome Powell’s speech at the Jackson Hole Symposium on Friday. The officials might provide clues about the year’s overall monetary policy going forward. The Fed’s less aggressive approach may limit the USD’s upward potential and support the price of gold. In the near future, market players will keep an eye on the data from the S&P Global Purchasing Managers’ Indexes (PMI) and follow the central bankers’ remarks for inspiration. Additionally, Friday’s important speech by Fed Chair Jerome Powell is scheduled to cause volatility in the FX market.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Prior to the shift in Swiss employment on Friday, the Q2 2023 Swiss Franc appreciated versus its counterparts. As anticipated, SNB would like to raise the rate at the September meeting.

In the lead-up to Monday’s European session, the USDCHF pair renewed its six-week high at 0.8828, but there is now no discernible momentum around 0.8820. By doing this, the Swiss Franc pair illustrates the market’s hesitancy in front of the most important information or events. A lot of attention is paid to the Purchasing Managers Indexes (PMIs) for the month of August, China news, and the speeches given by leading central bankers at the annual Jackson Hole Symposium. Though traders are trying to ascertain the major central bankers’ opinions on the monetary policy measures by the top-tier central bankers, China’s efforts to restore market confidence and conflicting concerns about the US Federal Reserve (Fed) add strength to the USDCHF inaction. It should be mentioned that the policy change in question had an impact on the US dollar in July prior to the stronger US data and higher Treasury bond rates that helped buyers of greenbacks.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has fallen from the resistance area of the pattern

In other places, China used a variety of tools, including fiscal and central bank policies, to bolster market liquidity and prevent the second-biggest economy in the world from entering a recession. Nevertheless, the one-year Loan Prime Rate was dropped by the People’s Bank of China to 3.45% from 3.55% previously and 3.40% anticipated. A floor under the USDCHF price was also imposed, according to the Financial Times (FT), by geopolitical concerns regarding Taiwan, Russia, and the potential trade war between the Group of Seven and the BRICS countries, which are Brazil, Russia, India, China, and South Africa. In the meantime, the pair buyers are cautioned by the lack of significant data or events.

In the midst of these plays, the S&P500 Futures extend the day’s recovery from the lowest point since mid-June by printing modest gains around 4,390. In a similar vein, the yield on US 10-year Treasury bonds reversed Friday’s decline, closing at most at 4.29%. The US Durable Goods Orders and the Swiss employment change for the second quarter (Q2) 2023 on Friday are some additional filters towards the north to watch for clear directions, even though the central bankers are probably going to amuse the USDCHF pair traders.

USDCAD Analysis

USDCAD has broken the Descending channel in upside

The PPI data for Canada showed a 0.40% increase in July compared to a 0.60% decrease in June. Producer price data increases in response to rising oil prices.

The Canadian dollar is weaker than the US dollar due to lower numbers in employment and investment data.

Following its peak level since May during Monday’s early Asian session, the USDCAD pair is trading sideways above 1.3500. At the moment, the pair is trading close to 1.3542, down 0.08% for the day. Since Canada is the biggest oil exporter to the US, a drop in oil prices would be detrimental to the Canadian dollar. The Federal Reserve’s Fed case for another interest rate hike is strengthened by the improvement in US retail sales and the solid labour data. The FOMC Minutes from last week made clear that although inflation is still too high, more tightening of monetary policy might be needed to get it down to the desired level. Conversely, July saw a 0.4% increase in Canadian producer prices, in contrast to June’s -0.6% decline brought on by rising oil prices. As for raw material prices, they increased 3.5% in July after rising 11.1% so far this year. The USDCAD pair benefits from Canada’s poor employment and investment statistics, which are negative for the Loonie and supportive of US economic data.

Crude Oil Analysis

Crude Oil Price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

Reuters reports that the People’s Bank of China PBOC stated on Sunday that China would set up financial support to allay concerns about local government debt. The encouraging development may allay worries about how China’s debt crisis and real estate problems will affect other countries. This therefore serves as a barrier to the Loonie’s decline and a headwind for the USDCAD pair. Participants in the market await Wednesday’s release of the monthly Canadian Retail Sales data for June. The highlight of the week will be Jerome Powell, Chairman of the Federal Reserve Fed, speaking at the Jackson Hole Symposium on Friday. The occasion will be crucial in figuring out whether the USDCAD pair will move clearly.

EURJPY Analysis

EURJPY is moving in the Box pattern and the market has rebounded from the Support area of the pattern

According to German PPI data, the annual rate for July decreased by 6% from the previous month’s 0.1% increase and 5.1% forecast. The monthly PPI data was -1.1% as opposed to the previous reading of -0.30% and the expected -0.20%. Because PPI rates have been lowered, the ECB makes it difficult to raise rates.

The annual German Producer Price Index (PPI) for July dropped to -6% from 0.1% increase and worse than the market expectation of -5.1%, according to the most recent data released on Monday by the Statistisches Bundesamt Deutschland. Against the prior month’s market consensus of -0.2% and -0.3%, the monthly PPI figure dropped to -1.1%. Additionally, as per the data released by Eurostat on Friday, the inflationary pressure within the Eurozone is decreasing, thereby reducing the pressure on the European Central Bank to persist in increasing interest rates. This consequently causes the Euro to be weaker than its competitors. In the near future, this week will see the release of the German GDP Q2 and the S&P Purchasing Managers’ Index (PMI) and Eurozone Current Account.

Because of the increase in CPI data last week, Bank of Japan inventions in the FX Markets at higher levels are more expected.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In a survey of 110 economists, 99 predicted that the Federal Reserve would leave interest rates unchanged at its meeting in September. Most analysts predicted that the rate cut would occur once in the upcoming year, specifically in the second quarter of 2024. By September 2022, the US economy is predicted to enter a recession at a rate of 40%, down from 50%.

According to a Reuters poll, 99 economists out of 110 predicted that the Federal Reserve (Fed) would maintain current interest rates at its meeting in September. Eighty percent of those surveyed said they did not think the Fed would raise interest rates any further this year. By the end of the second quarter of next year, most economists anticipate that the Fed will have lowered interest rates at least once. Since September 2022, the likelihood of a recession in the US economy has dropped from above 50% to 40%.

July’s UK retail sales were 1.2% MoM lower than the projected -0.50% decline. The annual reading of -3.2% was higher than the predicted -2.1%.

The Bank of England will raise interest rates in its next meetings due to rising GDP figures and declining retail sales.

GBPAUD Analysis

GBPAUD is moving in an Ascending channel and the market has reached the higher high area of the channel

Although UK retail sales were lower than expected, the majority of data points to the Bank of England’s (BoE) case for raising interest rates at its next meeting. The GBP/USD pair reached a daily high of 1.2766 and is currently trading at 1.2740. Global equities following losses show a negative outlook that is hurting the GBP/USD pair, as flows looking for safety have strengthened the USD. The Office for National Statistics (ONS) reported that July’s retail sales fell -1.2% MoM, which was less than the predicted -0.5% decline, and that the annualised decline was -3.2%, which was higher than the projected -2.1% decline. Nonetheless, given that money market participants are pricing in a 6% peak for the Bank Rate, robust data on the UK GDP and continuously rising wages sustain expectations for additional tightening by the BoE. As a result, the GBP/USD exchange rate would rise in the near future due to the Sterling’s (GBP) favourable interest rate differential with the US Federal Funds Rates (FFR), which is currently at 5.25%–5.50%.

Regarding the US, the most recent economic data supports the US dollar and maintains the high yields on US Treasury bonds. Federal Reserve (Fed) officials stated in July’s monetary policy minutes that they expect monetary policy to stay at restrictive levels. The US Treasury bond yields are beginning to recover some of their losses, with the US 10-year Treasury note yielding 4.239%, down four basis points. Meanwhile, the US Dollar Index (DXY), which measures the value of the US dollar against a basket of six currencies, is trading near two-month highs at 103.680.

GBPNZD Analysis

GBPNZD is moving in an Ascending channel and the market has reached the higher high area of the channel

The NZD dollar declines after the RBNZ kept interest rates steady last week. The 5-year rate remained unchanged despite China’s 10-basis-point reduction in the 1-year benchmark rate. China promised to provide more funding to local governments under pressure from the real estate industry in response to the increasing debt issues that local governments were facing. Just as China’s growth impacted New Zealand’s exports.

Following China’s reduction of its benchmark lending rate for one year while maintaining its rate for five years, the New Zealand dollar relinquished its early gains against its peers. Contrary to expectations of 15 basis-point reductions to both, the five-year rate remained unchanged while the one-year benchmark lending rate was lowered by 10 basis points. China promised over the weekend to organise financial assistance to address local governments’ debt issues. A number of developers are experiencing credit difficulties as a result of the protracted weakness in the real estate market, which has gotten worse for local government finances. For the second time in three months, China unexpectedly lowered key policy rates last week in an attempt to spur the flagging post-Covid economic recovery, as deflation risks increased and credit conditions tightened.

In order to mitigate some of the negative economic risks, Beijing has recently announced a number of initiatives. These include lowering important lending benchmarks, implementing supply-side measures specifically targeted at the real estate industry, and announcing the end of an ongoing, years-long crackdown on the technology sector. Many are waiting for more steps to address the demand side and infrastructure in the beleaguered real estate industry. China is the main trading partner of New Zealand, so any improvement in China’s growth prospects is good news for the NZD. NZD has been underperforming relative to some of its due to the perception that NZ interest rates have peaked and the country’s economic growth outlook for the current year is deteriorating. As anticipated, the Reserve Bank of New Zealand (RBNZ) held its cash rate constant last week, but it moved forward its projected date for interest rate reductions until 2025.

AUDJPY Analysis

AUDJPY is moving in the Descending channel and the market has reached the lower high area of the channel

The rate is at its peak, according to the minutes of the RBA meeting last week. There will not be any changes at the next meeting, and we will continue tightening based on economic data. Faced with economic challenges, China’s currency weakens compared to the US dollar.

China’s future continue to undermine the Australian dollar until the end of August. Trader attention is once again focused on global macro as market dynamics seem to be moving towards correlations of minus one and one. This is usually interpreted as an indication of unpredictability in the financial markets as traders and investors ignore the subtle differences across asset classes in search of safer waters. Why is the US dollar rising so quickly is a question that many people in the market are asking. The headwinds that are hindering the Australian dollar may hold the key to the solution. China is in a difficult situation because of its weak growth prospects and the number of big real estate companies that are going out of business.

Relaxing monetary policy could spur growth within the country but also depress the Yuan’s relative value. Official agencies may have to sell Treasury bonds, of which China owns more than USD 800 billion, in order to reduce the volatility of the Yuan. With the exception of March, China has been a major seller of US Treasury securities through 2023, according to the most recent data on holdings. That was the month when there was a noticeable uptick in the Yuan. The People’s Bank of China (PBOC) reduced the rate on its one-year medium-term lending facility last week, from 2.65% to 2.50%. Two enormous Chinese real estate developers, Country Garden and Sino Ocean, have fallen behind on a number of their onshore and offshore bonds this month. After Zhongrong International Trust Co., a significant participant in China’s trust industry, failed to fulfil a number of its client obligations over the course of the previous week, the term “contagion” became widely used in the markets.

Another sizable Chinese real estate company, Evergrande, filed for Chapter 15 protection in the US last Thursday. Filing under Chapter 15 is comparable to filing under Chapter 11, but it is intended for businesses with both US and offshore interests. Although Beijing has been discussing ways to strengthen its economy, no real steps have been taken as of yet. The Yuan has been negatively impacted by all of this, and it may become necessary for authorities to sell Treasuries in order to have US dollars on hand to purchase the Yuan.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/