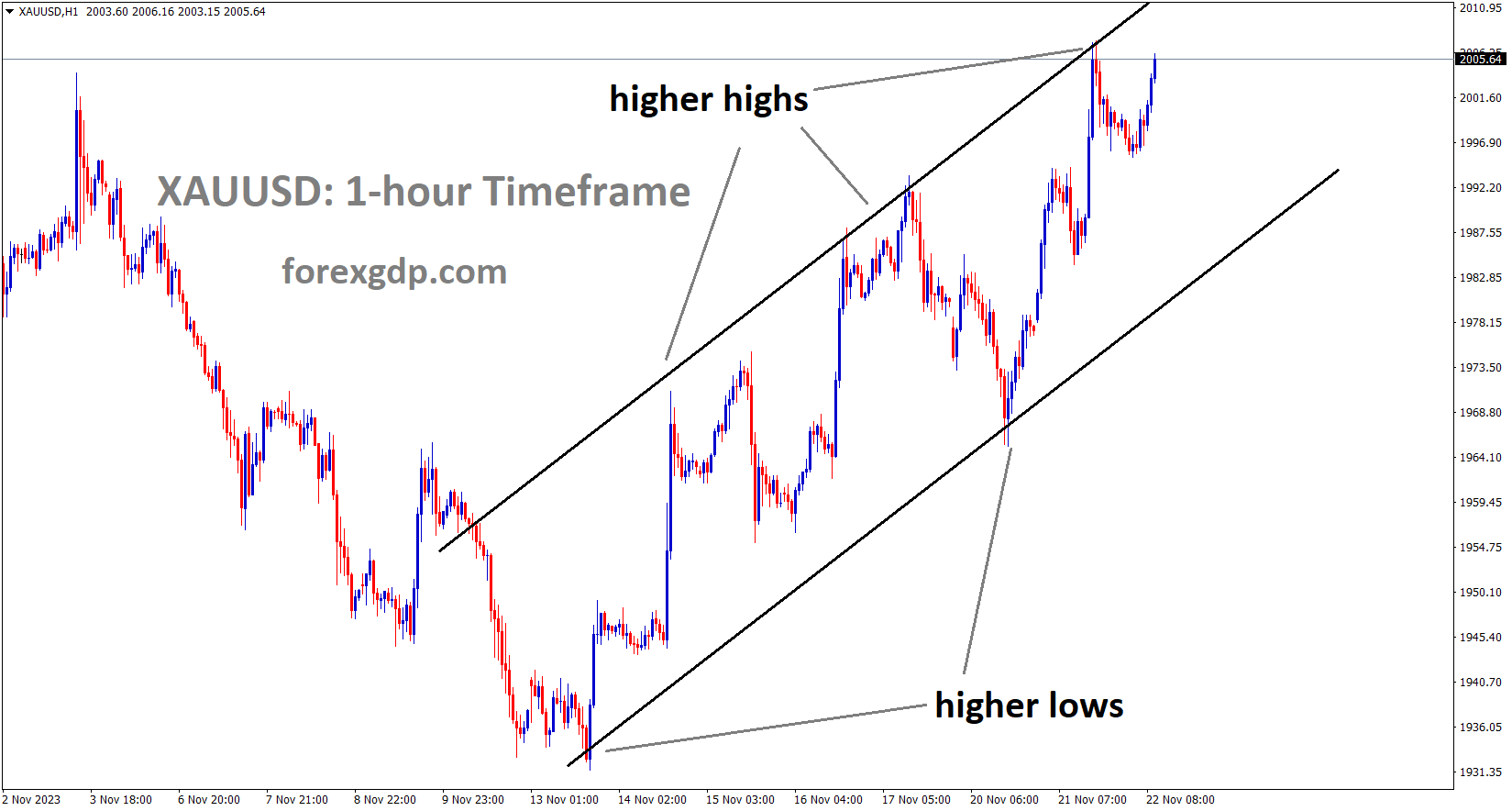

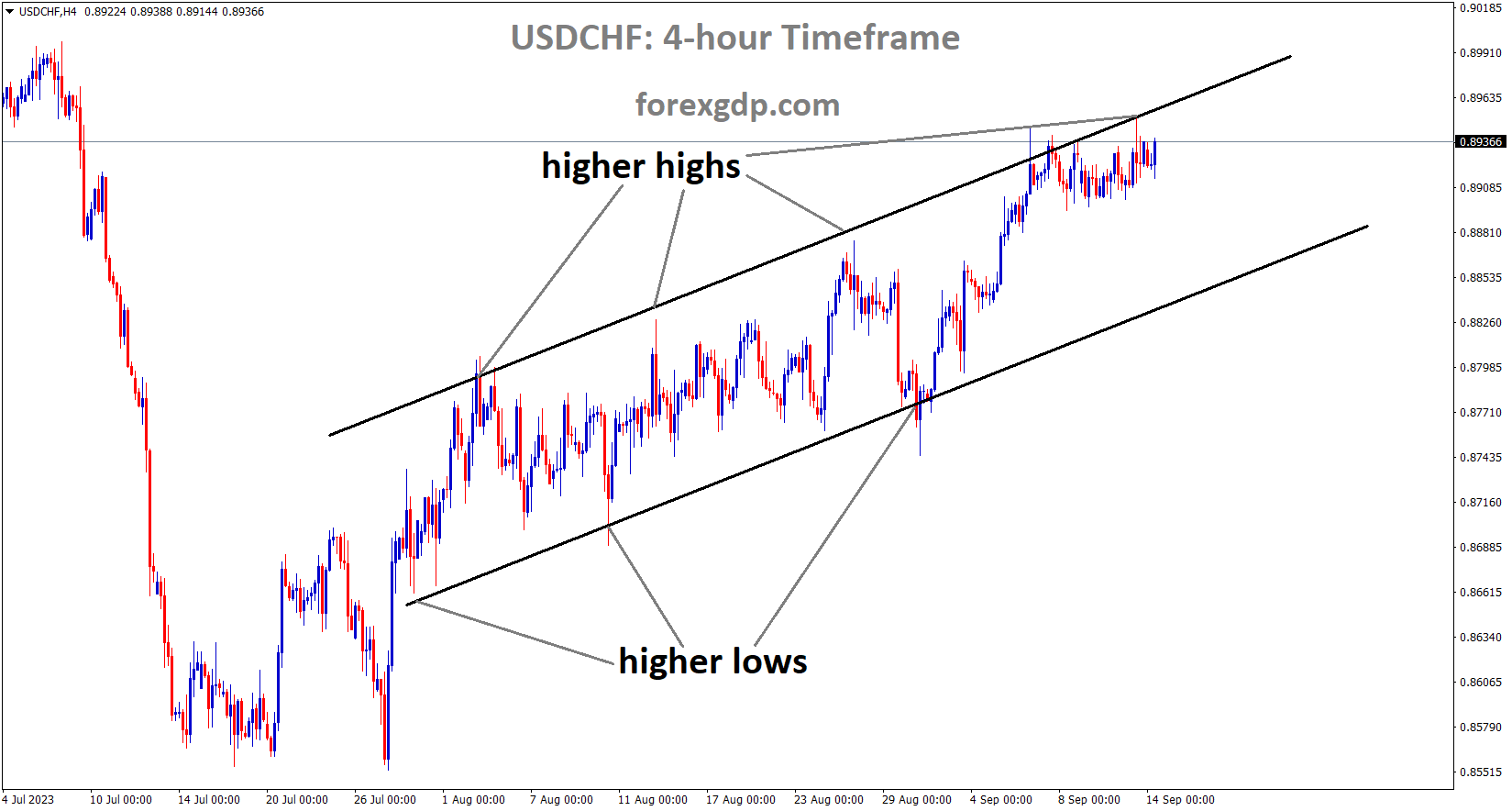

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

After two weeks in China, US Commerce Secretary Gina Raimondo has scheduled a meeting with CEOs of US corporations. Concerns about US companies’ relations with China are growing. Thus, the market fears a trade war resulting from the US-China relationship.

Thursday’s early Asian trading hours see the USD/CHF pair end a two-day winning run. As a result of the US inflation data, the US Dollar Index (DXY), which compares the value of the US dollar to six other major currencies, dropped from 104.96 to a current hovering point of 104.65. At the moment, the pair is trading close to 0.8930, down 0.10% for the day. The headline inflation rate in August reached its highest monthly gain in 14 months, according to data released by the US Bureau of Labour Statistics on Wednesday. The US Consumer Price Index (CPI) increased by 0.6% MoM from the previous reading of 0.2%. The annual percentage exceeded expectations, coming in at 3.7% from 3.2%. The core CPI increased 0.3% MoM from 0.2% in the prior month. The core CPI removes volatile food and energy prices. The annual core CPI was 4.3% as opposed to 4.7% previously. The data caused the Greenback (USD) to spike higher before the currency began to decline as investors assumed that the FOMC meeting next week would result in unchanged interest rates. The numbers do, however, suggest that the Fed should keep an eye out for any resurgence of inflation in the upcoming months. 97% of investors’ expectations are that the interest rate will remain unchanged in September at 5.25%–5.50%. But the CME Fedwatch Tool indicates that the likelihood of a rate hike at the November meeting rose to 49.2%.

The risk mood and the USD dynamic will be the key factors influencing the USD/CHF pair during the slow week of economic data releases from Switzerland. Two weeks after visiting China and expressing concerns about the state of the business environment, US Commerce Secretary Gina Raimondo is scheduled to meet with the CEOs of significant American corporations on Tuesday, according to Reuters. The US and China’s renewed trade war tension could lead to some selling pressure on the USD and act as a headwind for the USD/CHF pair. The Swiss Producer and Import Prices for August, which are due later on Thursday, will be of interest to market participants going forward. The focus will also be on the weekly US Initial Jobless Claims, the Producer Price Index (PPI), and the monthly Retail Sales releases. These numbers may provide a clear path for the USD/CHF exchange rate.

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending triangle pattern and the market has fallen from the lower high area of the pattern

In order to encourage the extraction of hard rock minerals from US lands, US President Joe Biden is talking about imposing royalties. This royalty charge varies between 4 and 8%. Once Republicans in the Senate and lower house are persuaded, this royalty fee will be put into effect.

As the US inflation picture continues to irritate gold bugs, the XAU/USD finished Wednesday trading at its lowest points in three weeks, recording a new low of $1,905 on the ticker tape. Following last week’s action, which saw the yellow metal retreat, gold is still rejecting the $1,940.00 level. The US Dollar (USD) and US Treasury yields are the two main issues plaguing the gold chart. At $2,060.00, the precious metal is much below its year-end highs. While the US Consumer Price Index (CPI) increased from 0.2% to 0.6% in August, worries about inflation are weighing on the XAU/USD exchange rate. Annualised CPI increased 3.7% compared to the 3.6% market estimate. Despite the Federal Reserve’s (Fed) projected decision to keep rates unchanged at their upcoming rate call next week, the increase in US inflation is forcing markets to reassess the likelihood of additional rate hikes from the Fed. Even though inflation rates are rising, there is not much of a downside for gold, so many investors are not overly alarmed. Notwithstanding their upward trend, CPI numbers are mostly concentrated in the volatile energy sector due to growing fuel expenses and volatile food prices. The basket of goods that does not include food and fuel, or core CPI, increased by 0.3% last month as opposed to the predicted 0.2%. Although it remains higher than anticipated by the market, the headline CPI all-prices total figure represents a notable decline. In a single month, the CPI’s petrol component increased by 10.6%, while overall energy prices increased by 5.6%. The inflation index saw gains due in part to rising housing costs, as rent increased for August by 0.3%, marking the 40th consecutive month of increases.

XAGUSD Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel

Broad-based support for the USD is being given by bolstered concerns about changes in the Fed rate hike cycle, which is preventing gold prices from rising too much in the short run as investors move to the Greenback in defensive positioning. Moving forward, gold bulls will be looking for a clearer picture from the Fed regarding potential rate cuts, and the XAU/USD pair is probably going to be limited to the downside until signs of a reversal of the Fed’s momentum on the rate hike cycle start to accumulate. In other gold-related news, the White House administration of US President Joe Biden is considering imposing the country’s first royalties—that is, royalties on the extraction of hardrock minerals—on precious metals that are extracted domestically.

The net royalty on any precious metals extracted from US federal lands would range from 4% to 8%. The royalty would necessitate the repeal of an 1872 statute, which expressly forbids the US from receiving mining royalties from the extraction of hardrock minerals. This legislation is unlikely to be approved by the Republican-controlled US Congress. If the royalty were to take effect, it would affect about 750 hardrock mines in the United States, most of which are in the West. Additionally, the measure would go against current White House proposals aimed at encouraging additional investment in US-based precious metals mining.

EURUSD Analysis

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The 3% inflation rate is still attainable, according to ECB President Christine Lagarde, but rate increases are necessary to keep it in check. Therefore, today’s meeting rate hike or not, solely based on historical domestic data.

Yesterday, the Euro recovered somewhat late, with the support of a declining Dollar Index (DXY) during the day. This was made worse by rumours that the European Central Bank (ECB) is set to raise its inflation forecast for 2024 to above 3%, which would signal a hawkish revision of the bank’s rate hike expectations. Ursula Von Der Leyen, President of the European Commission, echoed this rhetoric this morning when she said that it will take time to return to the ECB inflation target. The Euro Area economy is still struggling, so the news that the ECB intends to raise rates hike expectations is concerning. Germany, the most industrialised country in Europe, was the subject of special concern for economists analysing ZEW data yesterday. The deteriorating economic conditions in the Euro Area present a challenge for the ECB, which appears to want to raise rates tomorrow for the tenth time in a row. Whether we see a hike tomorrow seems to be split 50/50 right now, with the increase in oil prices probably playing a part as well. One worry might be that energy prices that are consistently high will eventually cause inflation, raising the possibility of inflationary pressures in a second cycle.

The US CPI data, which is anticipated later today, will be the final inflation report prior to the FED meeting the following week. It is an intriguing one because rising energy costs are probably going to cause headline inflation to pick up, which should theoretically maintain the dollar’s advantage. Investors seem to be certain that the Federal Reserve will keep interest rates unchanged for the upcoming week, with a potential hike in November. Will the FED’s decision at its meeting next week be influenced by the recovery in oil prices. The US CPI and the ECB Interest Rate Announcement tomorrow seem to be at opposite ends of the risk event spectrum as of right now. Even though there is currently a 50% chance that the ECB will raise interest rates tomorrow, US inflation is predicted to be sticky, which will keep the USD supported. It is possible that the Euro will continue to rise in the wake of the ECB’s hawkish pause tomorrow. It would not be a total surprise because markets continue to factor in an 80% possibility of one more rate increase from the ECB in 2023. With the third quarter coming to an end, the next two days might be critical for EURUSD.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

GBP GDP shrank by -0.20% on a three-month average, as opposed to a gain of 0.20% the previous month and an expected 0.30%. Since rate increases are greater in the UK, the GDP impact is less than it was in the previous reading.

GBPCHF Analysis

GBPCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The UK GDP missed estimates for both the 3-month average and the year-over-year period, which puts the pound on the defensive as we head into the European trading session. The economy shrank by 0.5% (the fastest rate in seven months!) in the MoM print, which is quite unexpected given that 0.2% was predicted. Despite certain encouraging manufacturing and trade balance data, the UK economy appears to be slowing down, in contrast to the previous print. It is evident that an environment with high interest rates is hindering economic growth. The weak labour data from the UK yesterday has added to the decline in the market today following the GDP. The market’s expectations for a 25 basis point rate increase later this month from the Bank of England (BoE) did not change significantly. The US CPI is now the focus of attention, and any positive surprise would probably destroy important support areas for the GBP/USD exchange rate.

GBPJPY Analysis

GBPJPY is moving in the Descending triangle pattern and the market has rebounded from the horizontal support area of the pattern

Yoshitaka Shindo, Japan’s recently appointed minister of economics, stated that structural wage growth and maintaining in an environment of higher rates will be two of the positive economic measures. Deflation is something we are trying to avoid this year, and growth driven by private demand is more likely in the Japanese economy.

Yoshitaka Shindo, Japan’s recently appointed minister of economics, declared on Thursday that he will mobilise all possible policy measures to support economy. In addition to working towards fiscal reform, Shindo stated that he is aiming to achieve a virtuous growth and wealth distribution. Will take audacious steps to lessen the impact of price increases. will exert every effort to secure structural pay increases. crucial to achieving growth driven by private demand. It is imperative to end deflation with decisiveness. One way to balance the primary budget is to put the economy on a growth path. The economy is starting to show signs of recovering from deflation.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern

As per Paul Grunewald, chief economist at S&P Global, the New Zealand economy anticipates a soft landing with low inflation. There is a strong job market and increased retail spending. Every month, employers support job applications, and RBNZ prefers to maintain the rates through the end of the current fiscal year.

According to a top macroeconomist in the world, the labour market’s continued strength is what holds out hope for a soft landing. Paul Gruenwald, global chief economist at Standard & Poor, noted that New Zealand’s economic problems were very similar to those that the US, the largest economy in the world, was facing. He stated that maintaining a robust labour market, finishing the Covid-19 recovery, and controlling inflation must be the top priorities for both. That is essential for a gentle touchdown. People will therefore have jobs if the labour market is strong. They believe that their employment will not change. Pay growth is positive. That will enable the authorities to gradually apply the brakes, allowing us to gradually approach the steady-state course, according to Gruenwald. We are concerned about a hard landing—that is, if businesses begin to reduce staff quickly, the demand will eventually decline, and we will experience an undershoot. But because highly skilled workers would be hard to replace, he claimed there was evidence of hoarding workers by businesses, which was good for the economy.

Gruenwald said that while the economy of New Zealand was doing well, growth would likely remain modest due to the uneven experiences of the largest economies in the world. It is most likely the US economy that is overheating. It is becoming a little too hot. According to him, the US needed to find a way back to a sustainable course that included balanced employment and reduced inflation. Europe is most likely a little off that trajectory. They are on the verge of stagnation. They certainly do not seem to be overheated, but they do have an inflation issue. More so than the US, he claimed, Europe was also reeling from the shock of Russia’s invasion of Ukraine. China has also been a little underwhelming. When the Party Congress declared in November of last year that the Covid restrictions would be lifted, we were all a little too hopeful. But the recovery was dulled by weakness in China’s property market, which was accompanied by a decline in consumer confidence and a high rate of youth unemployment. The Chinese bounce narrative has become less compelling. Therefore, we believe that the Chinese government may fail to meet its annual growth target of 5%. Gruenwald stated that New Zealand’s consumer-oriented exports, like meat and dairy, were at risk due to the weak Chinese economy. That is probably a little bit under pressure right now, but it is probably less volatile than, say, the demand for iron ore.

However, he pointed out that New Zealand had a history of capitalising on its advantages as a small, open export economy. The export economy is doing well. It is fiercely cutthroat. Its policy framework is strong. There is not much debt. You have a strong central bank, and I believe the government understands the need for a flexible economy.A small economy must be able to adapt to changes in the market, and New Zealand does so by manipulating its exchange rate. As a result, exporters are able to handle fluctuations in the value of the New Zealand dollar. He said that until the major economies of America, China, and Europe recover, which is anticipated to happen in 2024 or 2025, New Zealand should concentrate its efforts on strengthening its own economy. We are probably only going to be able to do that for the next six to twelve months. It will take time for the global recovery to accelerate before New Zealand can accelerate.

AUDJPY Analysis

AUDJPY is moving in the Descending channel and the market has reached the lower high area of the channel

Australian job data for August showed a 64.9K increase versus a 23K increase expected and job losses in the previous month. The RBA has now decided to postpone the rate hike until the next meeting.

Following the surprise creation of more jobs in Australia last month, the Australian dollar managed to hold its early gains against the US dollar. After job losses in July, the Australian economy added 64.9k jobs in August, against estimates of a gain of 23k. As anticipated, the unemployment rate stayed steady at 3.7%, barely rising from five-decade lows. The strong jobs report was almost entirely the result of gains in part-time employment (62.1k). Following losses of 24.2k in July, full-time employment increased by 2.8k.

As the Australian labour market begins to cool, there is less of a need to tighten further. Recent data from Australia, such as the GDP, composite, and PMI for services, have been positive and have surpassed previous readings. The Australian Economic Surprise Index, however, indicates that the data have generally been disappointing. The jobs report on Wednesday does not really change the general outlook for the RBA holding its rate of increase next month. The current market pricing indicates a slim chance of a rate increase in November.The Australian economy’s prospects have been getting worse. The demand picture in China, Australia’s top export market, would be crucial. In an attempt to reduce some of the negative risks, Beijing has recently announced a plethora of support and stimulus measures; however, the economy’s outlook has not yet improved as a result of these actions.

The Bank of Japan Governor Ueda’s announcement to stop negative interest rates strengthens the value of the JPY against counter-pairs. The monetary policy settings will tighten once inflation is achieved.

CADCHF Analysis

CADCHF is moving in the Box pattern and the market has reached the resistance area of the pattern

US dollars have benefited the Canadian dollar. The price of oil is rising, and the OPEC+ nations do not intend to raise their oil production.

The price of Western Texas Intermediate (WTI) crude oil is still rising, trading at roughly $88.30 per barrel. Amidst worries about tightening global supplies, the black gold has maintained a strong position near its highs since November.Recent announcements of further reductions by the world’s two largest oil producers, Saudi Arabia and Russia, have worsened the already tight supply conditions. These cuts, which are slated to take effect for the rest of 2023, will help to keep oil prices high and the Canadian dollar strong.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/