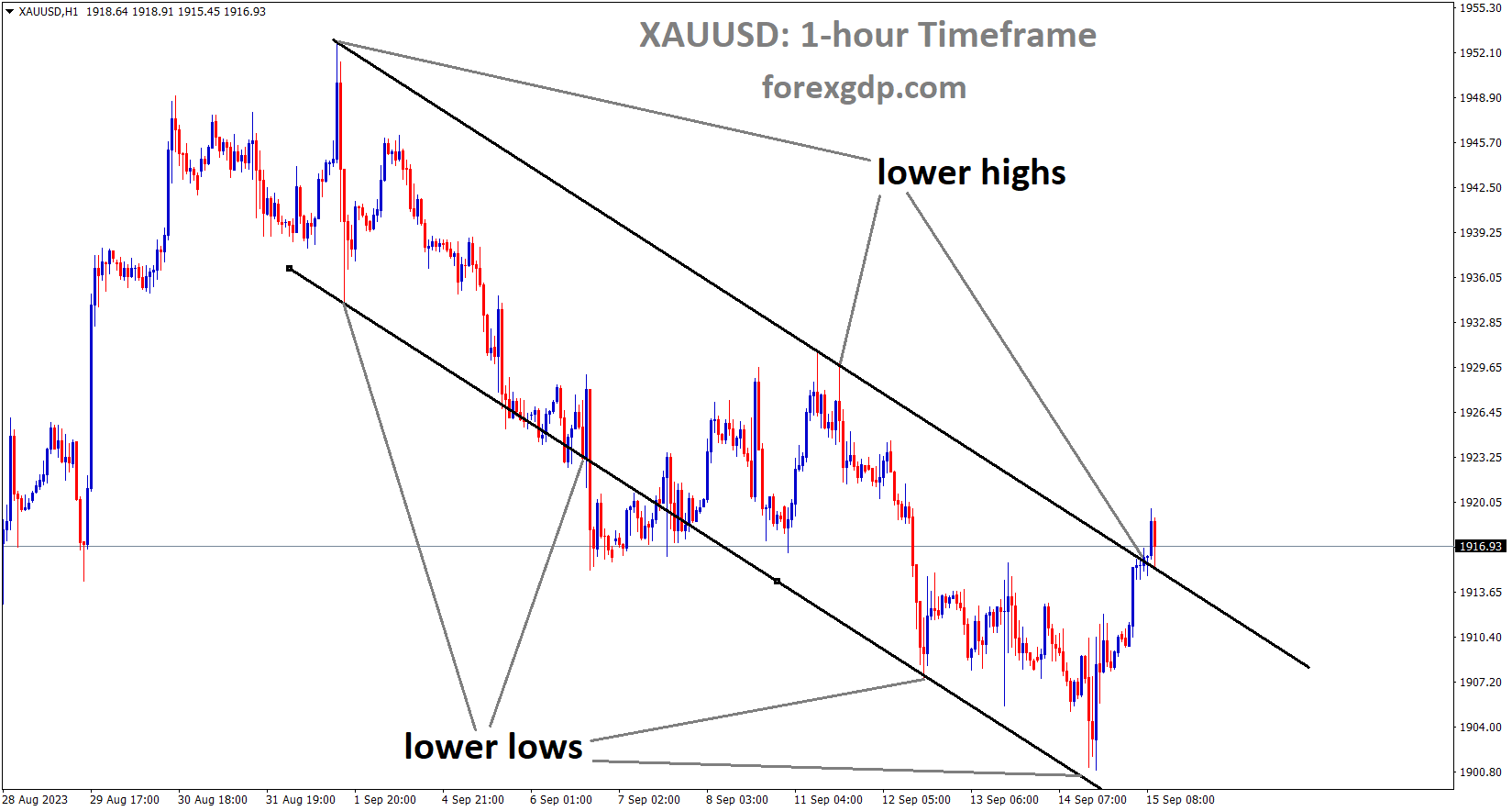

XAUUSD Analysis

XAUUSD Gold price is moving in the Descending channel and the market has reached the lower high area of the channel

After the US PPI data for August showed 0.70% instead of the predicted 0.40%, gold prices fell. Core PPI data showed a decrease to 0.20% from 0.40% in the preceding month.

During Thursday’s trading session, the XAU/USD briefly fell to new three-week lows before rising to end the day higher, just over $1,910.00. With better-than-expected US economic data and a dovish European Central Bank (ECB) that was unable to put enough powder in the pot for what may very well be the ECB’s final rate hike for the foreseeable future, gold tipped to the low side during the Thursday session, testing $1,901.00 before rising. US Producer Price Index (PPI) data for August came in on Thursday, beating forecasts and exceeding the previous month’s revised 0.4% increase (pre-revision: 0.3%). The index printed at 0.7% for the month, compared to the forecast of 0.4%. The headline gain was mostly driven by rising fuel and energy prices, even with the PPI printing creating more inflationary pressure. The core PPI, which does not include food and energy prices, came in at 0.2%, which was expected, down from 0.4% the previous month.

XAGUSD Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

US retail sales also showed a strong uptick, coming in at 0.6% for August, well above the 0.2% forecast and up from the previous 0.5%. Although inflation expectations are still low, the US economy looks to be on course to avoid a soft landing in the fourth quarter of 2023, either completely or mostly. This gave Gold the opportunity to regain some ground that had been lost recently. The ECB President Christine Lagarde noted that this may very well be the end of the ECB’s cycle of rate hikes, but the rate hike the bank announced early on Thursday did little to boost confidence in the larger markets. Following the dovish display by the ECB, investor risk appetite decreased. As a result, markets are now pricing in no more rate hikes from the ECB, with a rate cut now anticipated in March of 2019.

USDCHF Analysis

USDCHF is moving in an Ascending channel and the market has reached the higher high area of the channel

The FED is more likely to maintain rates between 5.25 and 5.50% at its meeting next week. Although the US government is more likely to expect a soft landing of economic inflation, the CPI data for the month of August in the US was higher than anticipated.

The US Federal Reserve is predicted by market pricing, which is based on the CME FedWatch tool, to maintain the federal funds rate at its meeting on September 19–20. A pause is warranted due to moderating core inflation (despite the headline CPI’s increase last month), cooling labour market conditions, and stabilising the housing market. In the meantime, Fed Chair Powell’s evaluation is probably going to be fair and emphasise the need for data in determining the short-term course of policy. He may be echoing remarks he made last month at Jackson Hole, where he hinted at the possibility of additional tightening to reduce above-trend growth and persistently high inflation. Is the Fed done raising rates? is the more important query. The likelihood of a revival in economic activity is increased by recent robust macro data, which also increases the risk of fresh price pressures. Therefore, it may be decided at the September rate meeting, but it may be close at the November meeting. Before the FOMC meeting on November 1, the payroll and CPI data from the following month will be crucial in this regard.

Next week, the September FOMC statement and the Summary of Economic Projections (SEP) will be the main points of interest. In particular, in accordance with the June assessment, the 2023 median policy rate may exhibit an additional 25 basis-point increase to 5.50%-5.75%. There would be more curiosity in whether the June projection of the median policy rate would increase to 4.6% in 2024. From a commercial standpoint, the SEP might be a major force. The current dovish 2024 market pricing is currently separated from reality by about 50 basis points, even with a 25 basis point increase. Anything above that would be seen as extremely hawkish, leading to a review of the dovish market pricing the following year and an increase in the value of the USD on a worldwide scale. However, the USD’s rally may pause if projections for the median policy rate in 2024 remain unchanged. Any retreat, though, might only last while the US economy continues to outperform the global economy.

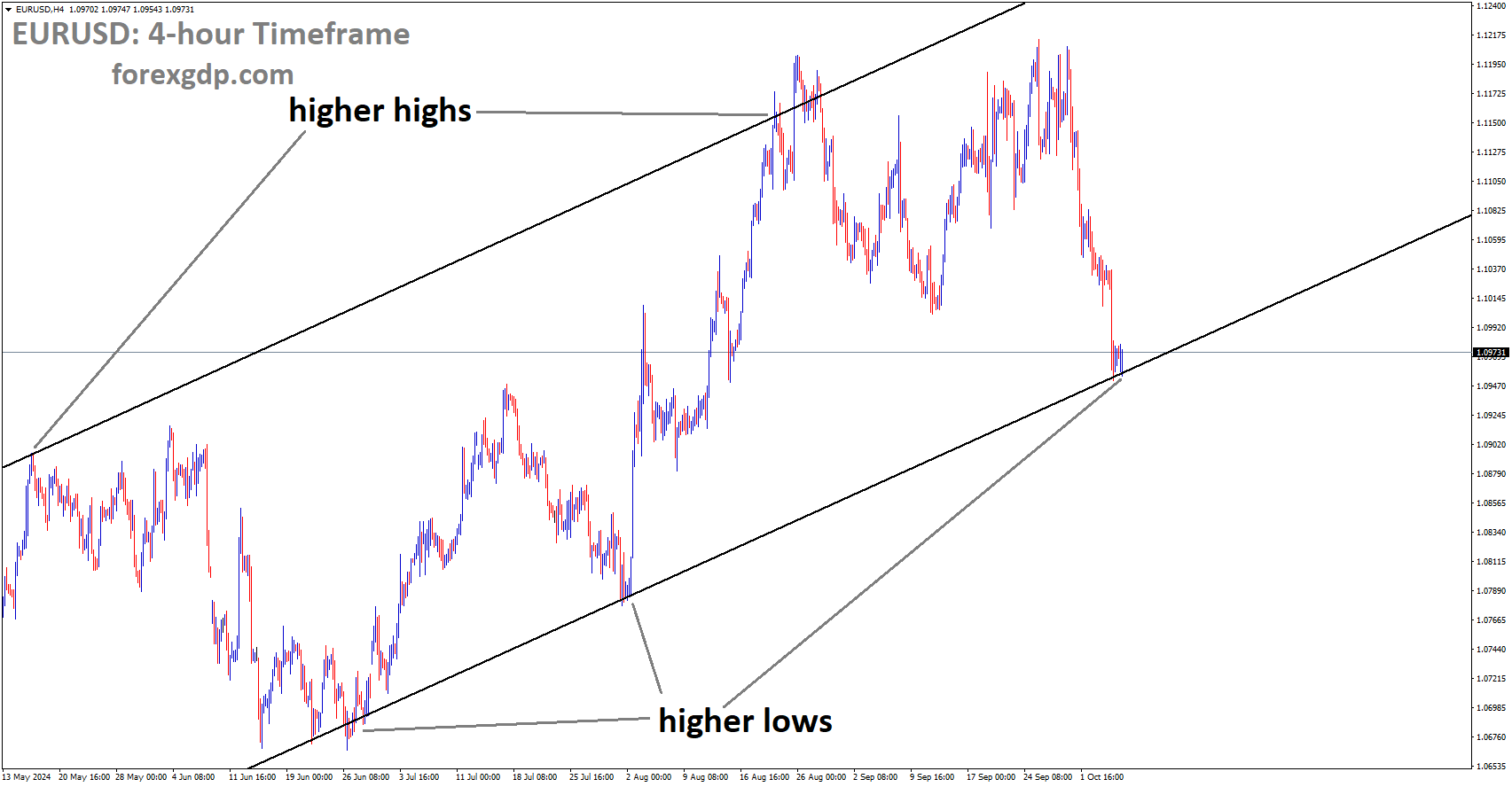

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has reached the lower low area of the channel

An analysis by Societe Generale suggests that the ECB may raise interest rates one more time this year if feasible. In order to fight inflation in the Euro area, the last-day rate hike is required. Following additional ECB tightening measures, the European economy has contracted.

The ECB raised rates by 25 basis points. Société Générale economists do not rule out additional rate increases. The press release’s wording strongly implies that the objective at this point is to maintain rates at these levels for an extended period of time, despite efforts to emphasise that additional hikes are still possible. Unfortunately, we believe that making this so explicit increases the likelihood that markets will now become more fixated on when the first cut will occur, particularly given that growth is still slow and inflation is probably going to decline. Contrary to expectations, the immediate effect on long-term yields and the Euro may indicate a more gradual return to price stability, necessitating additional rate hikes.

Even though we still see mostly upside risks to inflation, we do not anticipate any more rate hikes from the ECB this year. Instead, we are looking forward to the conversation about balance sheet normalisation by year’s end. There should be space to push the yield curve steeper with somewhat accelerated QT, which would also support price stability. We do, however, see a real risk that sticky core inflation brought on by high unit labour costs will occur, necessitating rate hikes by the ECB next year.

EURCHF Analysis

EURCHF is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern

It was widely anticipated that the SNB would hold interest rates at the September meeting due to the cooling off of import prices and producers in the Swiss zone. The Euro depreciated versus the Swiss Franc due to ECB President Christine Lagarde’s announcement that this is the final rate hike of the year.

The European Central Bank (ECB) raised interest rates on Thursday, but it hinted that this might be the final rate hike. As a result, the Euro (EUR) fell against the Swiss Franc (CHF). As a result, the EUR/CHF fell 0.52%, from its daily high of 0.9598 to 0.9538. Although it left the door open for further tightening, the European Central Bank (ECB) decided to raise rates by 25 basis points on Thursday, marking the tenth time since its tightening cycle began. The statement also stated that growth estimates had to be lowered and that rates needed to stay higher. Following the release of the statement, Christine Lagarde, President of the ECB, predicted a weak third quarter and stated that economic growth would remain muted. She also emphasised that there is a downside risk to growth and predicted that inflation would decline in the upcoming months. Mrs. Lagarde did not state that rates in the Eurozone (EU) had peaked, but she did note that some inflation indicators are still high.

In response to the ECB’s decision, the German 10-year bund fell three basis points to 2.599%, while the EUR/CHF fell from daily highs near 0.9600 towards 0.9550s. Prior to this, Switzerland’s producer and import prices decreased, which made it possible for the Swiss National Bank (SNB) to decide to keep interest rates unchanged at its September 21 monetary policy meeting. With the SNB expected to raise rates at the next monetary policy meeting and the underlying backdrop indicating that the ECB has finished raising rates, the EUR/CHF could continue to decline in the near future.

EURJPY Analysis

EURJPY is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern

The July month’s core machinery orders in Japan decreased 1.1% less than anticipated, weakening the JPY

One major factor supporting the JPY turns out to be the recent sell-off in Japanese government bonds (JGB), which was sparked by the prospect of an early end to the Bank of Japan’s (BoJ) negative interest rate policy. The yield on the benchmark 10-year JGB actually increased on Tuesday in response to hawkish remarks made by BoJ Governor Kazuo Ueda over the weekend, reaching its highest level since January 2014. Ueda hinted that raising interest rates is one of the options available if the BoJ gains confidence that prices and wages will continue to rise sustainably in an interview with the Yomiuri newspaper. The slowdown in China and the slowdown in global growth caused Japan’s core machinery orders to decline 1.1% in July, more than anticipated, according to the Cabinet Office. This is in line with a number of other indicators that have emerged in recent weeks, suggesting both domestic and foreign demand weakness and a challenging time ahead for the third-largest economy in the world.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower low area of the channel

UK GDP contracted to 0.50% at three-month average readings released this week; therefore, the Bank of England’s plan to raise interest rates this month is less likely than optimistic.

For the second day in a row, the GBPUSD pair exhibits some resilience below the 1.2400 barrier and draws some buyers on Friday during the Asian session. Though any significant recovery still seems elusive, spot prices have now partially reversed the decline from the previous day to over a three-month low and are currently trading around the 1.2420-1.2425 region, up 0.10% for the day. After the recent rally to the highest level since March 9, the bulls of the US dollar (USD) decide to take some profits off the table. This is seen as a major factor providing some support for the GBPUSD pair. Given the expectation of further stimulus from China, the largely positive macro data from China gives investors more confidence and causes some selling of the safe-haven US dollar. In addition, the dollar is further undermined by a slight decline in US Treasury bond yields; however, any significant decline should be limited by expectations that the Federal Reserve (Fed) will maintain its hawkish stance. At its meeting next week, the US central bank is almost certainly going to take a break from raising interest rates. Traders are still factoring in the potential for one additional 25 bps lift-off in November or December, though. Better-than-expected US economic data on Thursday confirmed the bets. Combined with persistently high inflation, this should enable the Fed to maintain higher interest rates for an extended period of time. Meanwhile, the outlook should support USD bulls and provide a tailwind for US bond yields. The GBPUSD pair may also be limited by the decreasing likelihood of a more aggressive policy tightening by the Bank of England (BoE).

Fears of a recession were stoked again when the Office for National Statistics revealed on Thursday that the British economy contracted by 0.5% in July, the fastest rate of contraction in seven months. This puts pressure on the BoE to halt its rate-hiking cycle, along with indications that the UK labour market is cooling. Moreover, the technical significance of the 200-day Simple Moving Average (SMA) break and close overnight indicates that the GBPUSD pair’s path of least resistance is downward. Therefore, any further increase carries the risk of quickly fizzling out and could still be viewed as a selling opportunity. For some motivation, traders are now anticipating the BoE survey on consumer inflation expectations. The US economic docket, which includes the Empire State Manufacturing Index and the Prelim Michigan Consumer Sentiment Index, may have an impact on USD price dynamics later in the early North American session and help create short-term trading opportunities around the GBPUSD pair. However, spot prices are still expected to close lower for a second consecutive week, and the previously mentioned fundamental environment appears to be strongly biassed in favour of bearish traders.

AUDUSD Analysis

AUDUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

In August, China’s retail sales improved from the previous reading of 2.5% to 4.6%, which was better than the expected 3.0% increase. In August, industrial production increased by 4.5%, compared to a 3.7% increase in July. Data income impresses the Australian dollar more.

During Friday’s Asian session, the AUD/USD pair continues to rise, closing the day at roughly 0.6470. The strengthening of the Australian dollar is being supported by China’s positive economic data. Positive economic trends can be seen in the data that the Chinese National Bureau of Statistics NBS has released. August saw a 4.6% year-over-year increase in retail sales, which was better than the 2.5% growth recorded in July and beat estimates of a 3.0% increase. In addition, Industrial Production grew at a rate of 4.5% in August as opposed to 3.7% in July, exceeding forecasts. These encouraging signs point to a growth in China’s economy, which may have both internal and global ramifications. China’s positive economic data suggests increased economic activity, which could have important ramifications for Australia given the two nations’ important trading relationship. Australia typically benefits from any improvement in China’s economic performance through higher exports and trade. Because it is likely to support Australia’s export-driven economy, the improved economic conditions in China could therefore be advantageous for the Australian Dollar AUD.

The People’s Bank of China PBoC recently reduced the Reserve Requirement Ratio RRR for a large segment of the banking system by 25 basis points bps in an effort to free up more liquidity and possibly boost growth in the second-biggest economy in the world. The US Dollar Index DXY holds steady at 105.30 after retreating from its six-month high. This shows how strong the US dollar USD is in relation to six other major currencies, giving us an idea of how the market is feeling and how strong people think the USD is. Given the US Federal Reserve’s Fed hawkish monetary policy stance, market participants seem to be taking precautions, which limits the possibility of a significant corrective decline in the US Dollar USD.Aggressive trading in the AUD/USD pair is likely to be discouraged by traders anticipating the Fed’s commitment to a more restrictive monetary policy, which may include additional interest rate hikes or tightening measures. In addition, the latest data on US initial claims for unemployment benefits for the week ending September 8 showed better results than anticipated, with 220,000 new claims—a slight increase from the previous week’s 217,000—than anticipated.

The Core Producer Price Index PPI increased by 2.2% in August, which was slightly less than the 2.4% increase that was anticipated. Retail sales showed signs of improvement, increasing to 0.6% from 0.5% the month before and above market estimates that had forecast a decline to 0.2%. These economic indicators show that consumer spending remained strong despite a minor moderation in the PPI, which reflects the intricate dynamics at work in the US economy. During the North American session, market players will be closely monitoring the release of the US preliminary Michigan Consumer Sentiment Index. The general consensus is that there will be a slight drop, from 69.1 to 69.5. Should the actual reading match or surpass these projections, it could give the US Dollar USD the propelling force it needs to continue rising. This data is important because it may provide information about consumer sentiment, which may have an impact on Greenback trading decisions.

In an effort to capitalise on the current economic recovery, the People’s Bank of China has lowered both the reserve requirements and the 14-day Reverse Repo rate.

As Asian markets followed Wall Street’s overnight rally, there is still a risk-on market profile going into the European session. The success of Arm’s initial public offering IPO raised investor sentiment and restored faith in the US capital markets. On the last trading day of the week, traders boosted market optimism by applauding China’s policy support measures and strong business activity data. Futures for the US S&P 500 are up about 0.20% today.

The Reserve Requirement Ratio RRR and the 14-day Reverse Repo rate were lowered by the People’s Bank of China PBOC in an attempt to boost the flagging economic recovery. In August, China’s industrial production and retail sales both grew more than anticipated. In relation to its principal competitors, the US Dollar USD declined from new six-month highs of 105.43 as risk appetite lessened the currency’s appeal as a safe haven. In the meantime, the yields on US Treasury bonds are consolidating upward while they wait for new US economic data. The mid-tier Industrial Production and the high-impact UoM preliminary Consumer Sentiment and Inflation Expectations will be included in the US docket.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has rebounded from the horizontal support area of the pattern

In August, the Business PMI data published by Business NZ was 46.1, down from 46.3 in July. The Chinese government has reaped greater benefits from the recovery of the Chinese economy in NZD dollars.

The New Zealand Business PMI dropped from July’s print of 46.3 to 46.1 in August, according to a Business NZ report released on Friday. The trend since March has seen the two major sub-index components of New Orders (46.6) and Production (43.9) all but entrenched in contraction, despite a minor improvement from July. For the sector to move in the direction of overall expansion, both of these important PMI components must show a consistent increase above 50.0. Once more, only Finished Stocks (52.1) continued to show growth in August, according to Catherine Beard, Director of Advocacy at BusinessNZ.

CADCHF Analysis

CADCHF has broken the Box pattern in upside

The oil prices increased in tandem with the anticipated resurgence of the Chinese economy, strengthening the CAD relative to all other counter pairs with the exception of the USD.

Prices for crude oil remain stable at or close to their highest point since November 2022, which supports the commodity-linked loner More stimulus measures from China, the world’s largest oil importer, provide a boost for the black liquid amid worries about reduced global supply. For the second time this year, the People’s Bank of China (PBoC) decreased the Reserve Requirement Ratio for the majority of the banking system by 25 basis points. This move is anticipated to increase liquidity and possibly support economic growth.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/