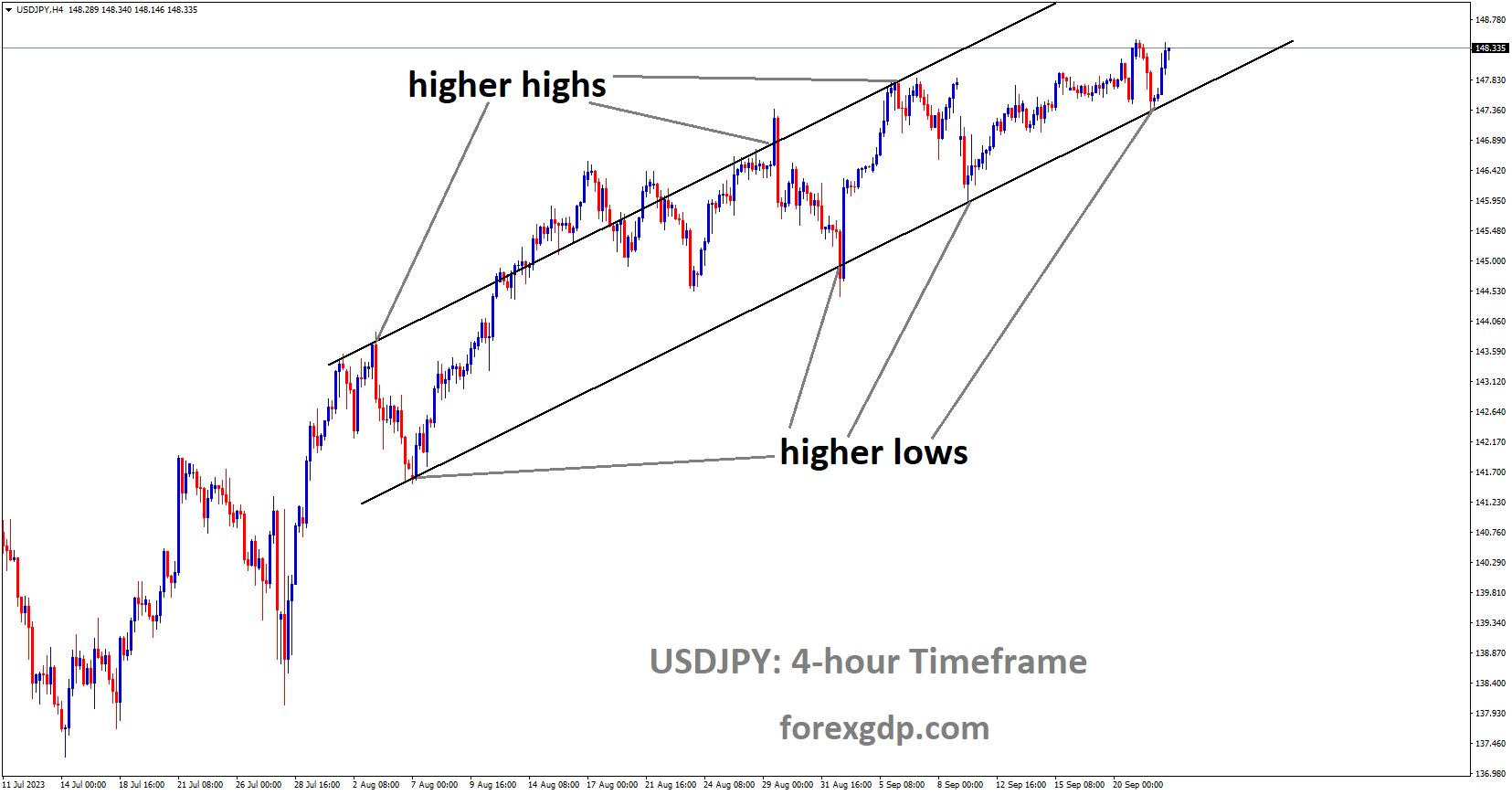

USDJPY Analysis

USDJPY is moving in Ascending channel and market has rebounded from the higher low area of the channel

Though the market had anticipated a change in policy, the Bank of Japan (BOJ) has maintained its commitment to monetary easing, maintaining ultralow rates unchanged. After two days of policy-setting meetings, this decision was made public on Friday. With short-term interest rates set at minus 0.1% and 10-year Japanese government bond (JGB) yields guided around zero percent, the BOJ’s yield curve control programme is still in place. This action follows the Policy Board’s July decision to permit a rise in 10-year yields towards 1%. During the recent meeting, the impact of this decision on the financial markets and the overall economy was thoroughly assessed. In spite of these adjustments, the BOJ reaffirmed its dedication to monetary easing and stated that it would be willing to carry out further easing measures as needed. The recent suggestion by Governor Kazuo Ueda to stop negative interest rates in the event that prices and wages increase complicated the conversation even more. By year’s end, Ueda predicted, there would be enough data and information available to enable a decision.

In terms of rate hikes, the BOJ’s decision keeps it well behind the European Central Bank and the US Federal Reserve. Despite growing inflation expectations, the BOJ is not convinced that stable inflation and sustainable wage growth are possible. But through August, headline inflation has continued to rise above its 2% target for 17 straight months, mostly as a result of rising import prices. A post-monetary easing future is priced in by financial markets, which has contributed to the upward trend in long-term JGB yields. Meanwhile, the BOJ’s dovish stance has caused the yen to weaken against the US dollar, putting Japanese authorities’ tolerance for rapid depreciation to the test. The Bank of Japan (BOJ) has stated that it will be closely observing the financial and foreign exchange markets, as well as their effects on the country’s prices and economic activity, in response to these developments.

This year, the BOJ has been buying JGBs at the fastest rate ever—an average of 10 trillion yen (US$67 billion) per month. The BOJ now owns 53% of all Japanese government bonds in circulation as a result. The aggressive bond-buying strategy has coincided with an increase in long-term yields, which have reached a 10-year high. The government is putting more and more pressure on the BOJ to address the sharp depreciation of the yen. It is anticipated that Governor Ueda will discuss this matter at his later-to-be-held news conference. For August, the ‘core’ rate of inflation in Japan—which does not include fresh food—was 3.1%, surpassing the 2% target set by the Bank of Japan for the seventeenth consecutive month. With volatile fuel prices excluded, the ‘core-core’ level came in at 4.3%.

USDCHF Analysis

USDCHF is moving in Ascending channel and market has reached higher high area of the channel

Despite money market futures indicating a 25 basis point rate hike, the SNB unexpectedly kept rates at 1.75%. The Swiss National Bank stated that additional tightening might be required to maintain price stability over the medium term, despite the fact that it was a dovish surprise. The Consumer Price Index CPI was 2.2% in 2023, according to the central bank’s updated inflation projections for 2023 and 2024. Inflation is expected to reach 1.9% in 2025, according to the SNB, even though it is still within the price stability range.

In addition, the Swiss Franc CHF was negatively impacted by the US Federal Reserve’s hawkish stance. The Federal Reserve’s Fed upward revision of the Federal Funds Rates FFR above 5% in 2024, compared to June’s 4.6% projection, caught market participants off guard. That is the main reason for the price action in the financial markets, which caused US bond yields to rise, US equities to plummet, and the US dollar to hold its value against the majority of G8 currencies. The yield on US Treasury bonds had continued to rise. The yield on the US 2-year bond, which is most vulnerable to changes in short-term interest rates, was at 5.146% after hitting a multi-year high of 5.202%. Nevertheless, the USD/CHF would be dependent on a difference in interest rates between the US and Switzerland, which would support the US dollar.

EURUSD Analysis

EURUSD is moving in Descending channel and market has fallen from the lower high area of the channel

The US dollar USD is still seeing a selling bias versus the euro EUR, which is what drove the EURUSD pair to record early Friday lows of nearly 1.0600. Based on the USD Index, the Greenback is able to move past its knee-jerk reaction from Thursday and continues its upward trend in the 105.60 region DXY. The Federal Reserve’s Fed hawkish stance on Wednesday has rekindled the Dollar’s unrelenting march north, which is also supported by the strong increase in US yields at the long end of the curve and the belly of the curve.

The European Central Bank ECB board members demonstrated some unity in their views despite the fact that inflation was still significantly above the bank’s target, suggesting a possible pause at the next meeting. While they are still well within contraction territory, Germany’s flash Manufacturing and Services PMIs surprised to the upside in September, coming in at 39.8 and 49.8, respectively, on the European docket. The advanced Manufacturing PMI for the entire eurozone was less than expected, at 43.4, while the Services PMI was higher than expected, at 48.4.

EURJPY Analysis

EURJPY is moving in Box pattern and market has fallen from the resistance area of the pattern

The Bank of Japan maintained its ultra-low interest rate and maintained its dovish outlook in forward guidance, which further pressured the value of the yen.

The BOJ’s target inflation rate is currently above, but policymakers have signalled that they are not in a rush to start tightening monetary policy just yet and will keep supporting the economy until it falls back to 2%. With recent talk about intervention also starting to wane, the pair maintains its full bullish stance, which was reinforced by the latest BOJ decision and remains on track for further gains.

EURCHF Analysis

EURCHF is moving in Descending channel and market has reached lower high area of the channel

The official data from the HCOB’s most recent purchasing managers index survey showed on Friday that while the services sector saw a slight improvement in September, the manufacturing sector contraction in the Eurozone deepened. The September reading of the Eurozone Manufacturing Purchasing Managers Index (PMI) was 43.4, slightly below the 44.0 forecast but higher than the 43.5 recorded in August.

There was a two-month low for the index. The Services PMI for the bloc increased to 48.4 in September from 47.9 in August, surpassing the consensus of 47.7 and reaching a two-month high. September’s HCOB Eurozone PMI Composite was 47.1, up from 46.5 in August and 46.7 in anticipation. Additionally, the index showed a two-month peak.

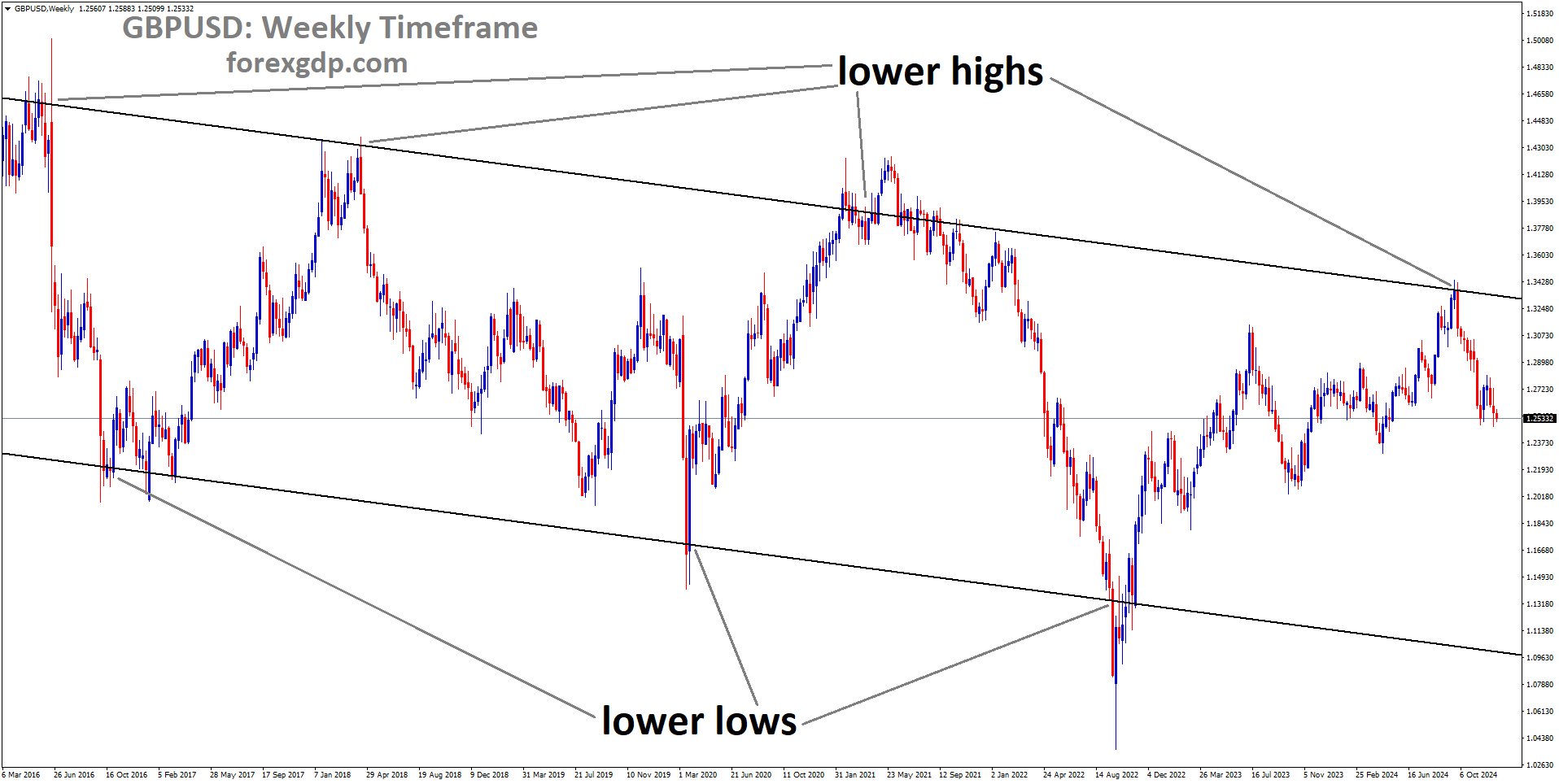

GBPUSD Analysis

GBPUSD is moving in Descending channel and market has reached lower low area of the channel

For the second day in a row, the GBPUSD pair ended the day lower on Thursday, and early on Friday, it continued to decline, reaching the 1.2250 region. The technical outlook for the pair in the near term indicates oversold conditions, but a strong rebound may be difficult to achieve. In a split vote, the Bank of England decided to hold the interest rate at 5.25%, defying the market’s expectation of a 25 basis point hike. According to the BoE’s policy statement, the majority of the Monetary Policy Committee cited the improving labour market, the soft August inflation data, and the decline in business sentiment as reasons to keep the rate unchanged. Markets are currently pricing in a 75% chance that the BoE will hold the rate steady in November, according to calculations done by Reuters. Following the BoE event, BNP Paribas and UBS released statements in which they reduced their terminal rate projections from 5.5% to 5.25%.

Early on Friday, UK data revealed that, after declining 1.1% in July, retail sales increased 0.4% monthly in August. In addition, the S&P Global/CIPS Composite PMI fell from 48.6 in July to 46.8 in August, indicating that the private sector’s activity is still contracting. Dr. John Glen, Chief Economist at CIPS, evaluated the report’s findings and said, Private sector businesses reported that output fell at the sharpest rate since March 2009, outside the lockdown years and inevitably job creation followed suit as headcounts reduced at the fastest level since October 2009. Manufacturers’ backlogs shrank at the quickest rate since February 2009, causing a sharp decline in their work pipelines. The BoE will probably be forced to hold off on tightening policy further due to the UK economy’s declining outlook. Therefore, the growing policy differences between the BoE and the Fed may keep the GBP/USD pair declining.

GBPJPY Analysis

GBPJPY is moving in Descending channel and market has rebounded from the lower low area of the channel

In September, the seasonally adjusted S&P Global/CIPS UK Manufacturing Purchasing Managers’ Index (PMI) unexpectedly increased to 44.2 from the final print in August of 43.0, which was the expected reading. In September, the preliminary UK services business activity index fell to 47.2, a 32-month low, from 49.5 in August’s final print and 49.2 in the forecast. The Chief Business Economist at S&P Global Market Intelligence, Chris Williamson, commented on the flash PMI data, saying, The disappointing PMI survey results for September mean a recession is looking increasingly likely in the UK. The sharp decline in output indicated by the flash PMI data is consistent with the GDP contracting at a quarterly rate of more than 0.4%, and there are few signs of an immediate improvement, Williamson continued.

GBPCHF Analysis

GBPCHF is moving in Box pattern and market has reached support area of the pattern

The policy rate of the Bank of England (BoE) remained at 5.25%. Wells Fargo economists report that the decision marks a loss of interest rate support for the Pound. As of right now, we predict that this cycle’s peak will occur at the policy rate of 5.25%. We do anticipate that rates will stay there for a while, and we only anticipate a first, small 25 bps rate reduction by the time of the May 2024 policy meeting.

This is due to a mild recession that started late in the year and the CPI inflation rate approaching the 2% target. We anticipate that the rate of rate cuts will pick up steam during the remainder of the following year, with the Bank of England policy rate ending at 3.25%. There is no longer any support from interest rates for the decision to pause and the likely end of policy tightening.

NZDUSD Analysis

NZDUSD is moving in Ascending channel and market has rebounded from the higher low area of the channel

NZDUSD is still steadily rising. ANZ Bank economists assess Kiwi’s future prospects. The movements have been ordinary and well within known ranges; looking ahead, it is challenging to identify a trigger for a significant range-break. While the Fed’s pursuit of soft landing is encouraging for the USD, the NZ economy is showing to be slightly stronger than initially anticipated, and this month’s domestic data clearly highlights the need for further tightening of monetary policy.

When you put everything together, it feels more like a way to limit downside than a way to overcome USD exceptionalism, especially given that markets are not ready to price in an increase in the OCR in November. At least for the Kiwi, it is not bad news.

AUDJPY Analysis

AUDJPY is moving in Ascending channel and market has rebounded from the higher low area of the channel

During the early Asian session on Friday, the AUDJPY cross trades in negative territory for the second straight day, under continued selling pressure. The cross is up 0.03% for the day at 94.71 as of the time of publication. According to the most recent data released on Friday, the preliminary S&P Global Australian Services PMI increased from 47.8 in August to 50.5 in September. However, the Manufacturing PMI fell from 49.6 in the prior reading to 48.2 in this one. Additionally, the Composite Index was raised from 48.0 to 50.2. In anticipation of the much-awaited Bank of Japan (BoJ) interest rate decision, investors are becoming more cautious, which is why the mixed Australian economic data fails to strengthen the Australian dollar.

In terms of the Japanese yen, it is generally anticipated that the BoJ will maintain its targets for the 10-year bond yield at roughly 0% and the short-term interest rate target of -0.1%. Changes in monetary policy will not be taken into consideration until local wage and inflation data align with the Japanese central bank’s projections, as it has previously stated. The markets are watching Governor Kazuo Ueda’s press conference following the meeting closely to see if he will provide any new clues about when to make policy changes and other adjustments to Yield Curve Control (YCC).

Regarding the statistics, the National Consumer Price Index (CPI) for Japan decreased from 3.3% in July to 3.2% YoY in August. Furthermore, the National CPI ex Food, Energy came in at 4.3% as opposed to 4.3% in prior readings, while the National CPI ex Fresh Food improved from 3.0% in July to 3.1% in August. Investors will be closely following the Bank of Japan’s (BoJ) interest rate announcement, which is scheduled for later this Friday. This could set off market volatility and provide the AUDJPY cross with a distinct direction.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/