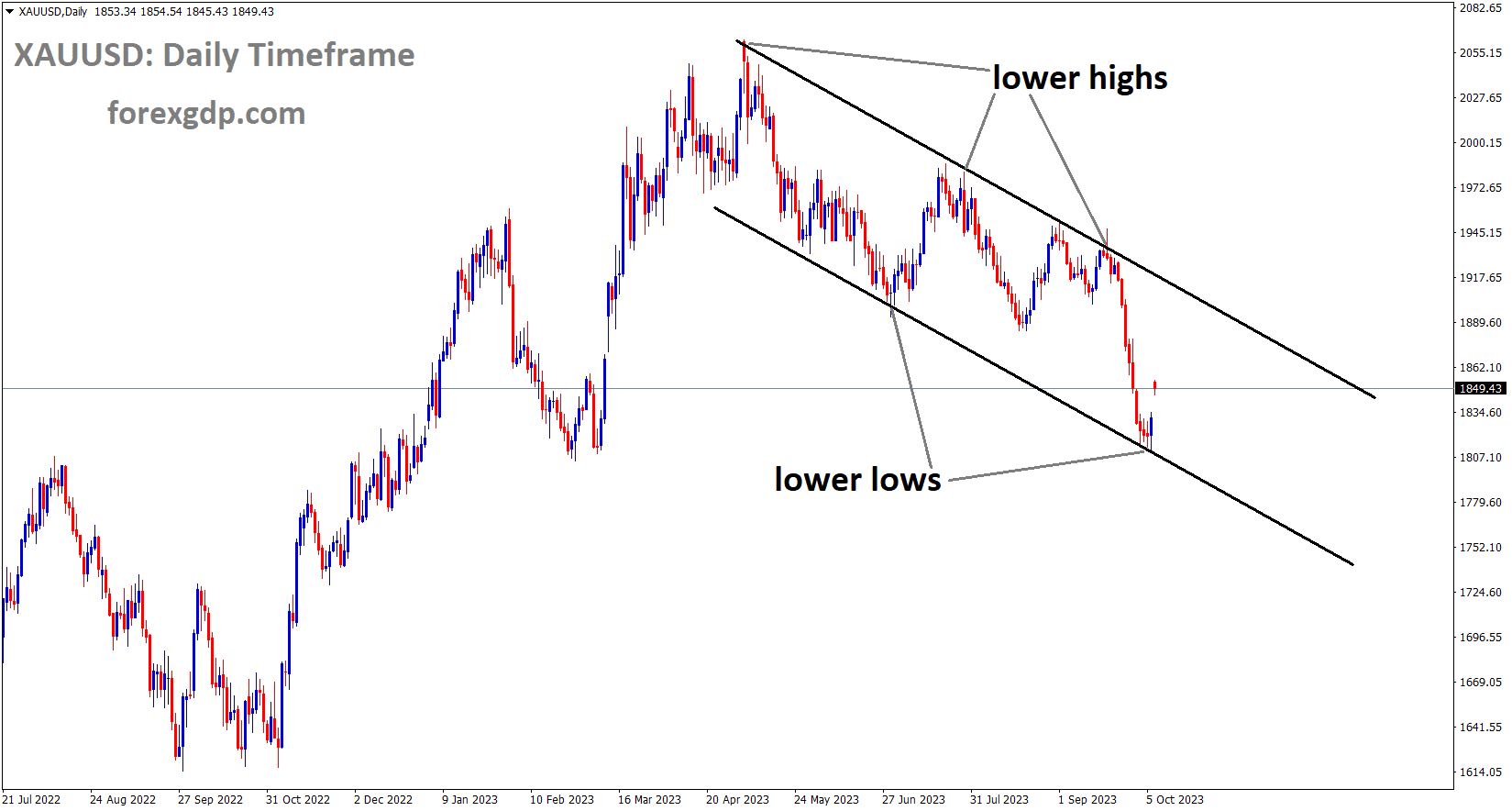

Gold Analysis

XAUUSD Gold price is moving in the Descending channel and the market has rebounded from the lower low area of the channel

Gold prices rose on Sunday after Hamas launched missiles into Israel’s Gaza Strip. Unexpected events in the Middle East paved the way for commodity prices to rise.

The gold price experienced a dramatic intraday turnaround on Friday, rallying more than 1.3% from $1,810, its lowest level since March 8 in the aftermath of the United States US monthly jobs data. Meanwhile, the US Nonfarm Payrolls NFP report reaffirmed expectations for at least one more rate hike by the Federal Reserve Fed in 2023, weighing on the precious metal. However, additional details of the report revealed that wage growth remained moderate during the reported month, easing inflationary concerns and potentially forcing the Fed to soften its hawkish stance. As a result, the US Dollar USD fell for the third consecutive day, prompting aggressive short-covering around the Gold price, allowing it to snap a nine-day losing streak. Furthermore, rising geopolitical tensions in the Middle East helped the XAU/USD open with a bullish gap and advance to a one-week high on the first day of a new week. However, the emergence of new USD buying keeps the gold price from further appreciating. Traders are now anticipating the release of the FOMC meeting minutes and US consumer inflation figures this week. Last Friday, the US NFP report showed that the economy added 336K jobs in September, which was much higher than expected, and the previous month’s reading was also revised higher to 227K from 187K.

Average hourly earnings increased by 0.2% during the reported month, matching a similar increase in August, and increased by 4.2% year on year through September, compared to 4.3% the previous year. Markets are still pricing in at least one more Fed rate hike before the end of the year, which supports elevated US bond yields and continues to support the US Dollar. Geopolitical tensions spark a new wave of global risk aversion, assisting the safe-haven Gold price to rise for the second day in a row and surpass a one-week high. The conflict between Israel and Palestine reached unprecedented heights on Saturday, when Hamas, a Palestinian militant group, launched an unprecedented attack on Israel and launched a barrage of rockets. In addition, Palestinian militants infiltrated Israeli territory in a number of locations. In response, Israel launched airstrikes on Gaza on Sunday and declared war on the Palestinian enclave. The development raises the risk of a wider Middle East conflict and increases demand for traditional safe-haven assets, which is seen as a key factor benefiting gold. The emergence of new USD buying limits the upside for XAU/USD as traders look for clues about the Fed’s future rate-hike path in the FOMC meeting minutes and US consumer inflation figures.

Silver Analysis

XAGUSD Silver price is moving in the Descending channel and the market has rebounded from the lower low area of the channel

In the United States, inflation is consistently higher. As a result, the FED may keep rates higher for a longer period of time until inflation falls. The US dollar fell against other currencies after Friday’s NFP data came in higher than expected.

The US Dollar Index DXY fell in Friday trading after briefly reclaiming the 107.00 level, settling at 105.95, a new low for the week. US Non-Farm Payrolls NFP figures released on Friday easily outperformed expectations, adding 336K jobs in September, far exceeding the forecast decline to 170K and exceeding the previous month’s reading of 227K revised upwards from 178K.

Nonfarm payrolls in the United States increased by 336,000 in September, exceeding the 170,000 forecast. Inflation remains a persistent thorn in the side of the Federal Reserve Fed, and market participants are concerned that the Fed will be forced to keep interest rates higher for longer.

USDCHF Analysis

USDCHF is moving in the Box pattern and the market has rebounded from the support area of the pattern

The recent war between Hamas and Israel causes haven assets such as the Swiss Franc to rise against currency pairs. The US job report on Friday was strong, but the USD failed to cheer against the Swiss Franc.

The military conflict between Palestine and Israel put downward pressure on the pair. Furthermore, the US Nonfarm Payrolls data released on Friday failed to support the USDCHF pair. The September jobs report revealed a significant increase of 336,000 jobs, exceeding the market expectation of 170,000. The revised August figure was 227,000. However, the US MoM remained stable at 0.2% in September, falling short of the expected 0.3%. The report showed an annual decline of 4.2%, which was lower than the expected consistent figure of 4.3%. The markets are keeping a close eye on the ongoing military conflict in the Middle East between Hamas and Israel. The fear is that the conflict will escalate and spread to other parts of the region, introducing geopolitical uncertainties that could have an impact on global markets.

The escalation of violence has the potential to drive investors to seek refuge in traditional safe-haven assets, such as the Swiss Franc CHF. During times of increased geopolitical uncertainty, there is an increased demand for safe-haven assets, and CHF is frequently viewed as a less risky asset in such circumstances. The US Dollar Index DXY has recovered after three consecutive days of losses, aided by higher US Treasury yields. At the time of writing, the spot price is around 106.30.

Treasury yields in the United States have recovered, owing to expectations that the Federal Reserve Fed will maintain higher interest rates for an extended period of time. By press time, the 10-year US Treasury bond yield had returned to near its 2007 peak of 4.80%. Investors will be watching the upcoming International Monetary Fund IMF meeting closely, as discussions will centre on strategies for stabilising international exchange rates and promoting development. Furthermore, the US Core Producer Price Index may be closely watched later in the week, as it plays an important role in assessing inflationary trends and economic conditions in the United States.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

German industrial production fell by -2.0% in August, following a -1.7% drop in July. The euro has not changed since the data was released. Germany’s industrial production is declining, paving the way for a recession.

Germany’s Industrial Production fell more than anticipated in August, indicating slow manufacturing sector activity, according to official data released on Monday. In July, industrial output in the economic powerhouse of the Eurozone fell by 0.6% MoM, while -0.1% was predicted and -0.6% was observed, according to data released by the federal statistics authority Destatis.

The figures were adjusted for calendar and seasonal effects. German Industrial Production decreased 2.0% in August on an annual basis, following a 1.7% decline in July.

EURJPY Analysis

EURJPY is moving in the Descending channel and the market has fallen from the lower high area of the channel

According to Japanese officials, one-sided FX movements are classified as volatile, as are strong hourly ups and downs brought on by increased accumulation or distribution. During the abrupt decline in the USDJPY last week, we refrained from intervening in the market.

Concerning the excessive volatility of the Japanese Yen (JPY) in the foreign exchange markets, the Japanese authorities have not abated. “If currencies move too much on a single day or, say, a week, that is judged as excess volatility,” Masato Kanda stated on Wednesday. Even if that is not the case, excess volatility still exists if we observe one-sided moves compound into very large moves within a given time frame, he said. and the coupon on the 10-year Japanese Government Bond (JGB) increased to 0.80%, allowing the Bank of Japan (BoJ) to step in and limit the recent increase in yields.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

The Bank of England is more likely to leave interest rates unchanged at its meeting in November, which makes the GBP pair slightly weaker than the counter pair.

In the aftermath of the global flight to safety, spurred by growing geopolitical tensions in the Middle East, the safe-haven narrative did receive a little boost. In a historic move on Saturday, the militant Hamas group in Gaza, Palestine, attacked Israeli towns. In retaliation, Israel declared war on the Palestinian enclave of Gaza on Sunday and began airstrikes there, killing hundreds of people on both sides. Nevertheless, the uncertainty surrounding the Federal Reserve’s (Fed) potential rate-hike trajectory restrains aggressive wagering by USD bulls and provides some support for the GBPUSD pair.

The economy added 336K jobs in September, according to the highly anticipated US monthly jobs data (NFP) released on Friday. This figure was higher than market estimates and the upwardly revised 227K reading from the previous month. The data confirms expectations for at least one more rate hike by the end of the year from the Fed, which supports elevated US Treasury bond yields and keeps the USD strong. However, more information in the report showed that wage growth was moderate during the month under review, allaying fears about inflation. Consequently, the Fed may be able to moderate its aggressive position.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has reached the support area of the pattern

Because of this, investors closely monitor this week’s FOMC meeting minutes, which are released on Wednesday, and the most recent US consumer inflation data, which are released on Thursday. This will assist investors in determining the Fed’s next course of action, which will ultimately determine the trajectory of the USD and give the GBPUSD pair new momentum. A significant increase in spot prices may be restrained in the interim due to expectations that the Bank of England (BoE) will maintain current interest rates at its November meeting, potentially undermining the value of the British pound.

CADCHF Analysis

CADCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Following Sunday’s conflict between Israel and Hamas, oil prices rose sharply. Rising oil prices provide the Canadian dollar strength versus other currencies.

The September employment report for Canada, which came in at 63800, supports the Canadian dollar. Although the Bank of Canada maintains its hold on the GDP for the entire year despite inflation beating forecasts, the GDP stagnated in Q2 and Q3, which was more than anticipated. Q4 is not a clear indicator either.

According to data released on Friday, employment increased by 63,800 in Canada in September, exceeding forecasts. CIBC analysts point out that the implications for the Bank of Canada should be limited by the weakness under the hood. Although the employment increase in the headlines was unexpected, the lack of specifics and the drop in hours worked indicate that the economy was still weak at the end of Q3.

We still see the Bank of Canada keeping its policy on hold despite the recent stronger-than-expected inflation readings because the GDP essentially stopped in Q2 and Q3, and there was no indication that it was picking up speed in the final quarter.

The dramatic increase in oil prices, which may be related to the military conflict between Israel and Palestine. It is possible that the fighting caused a fresh spike in oil prices. Given that Canada is the biggest oil exporter to the US, the increased geopolitical tensions may have an impact on the Canadian dollar CAD. The price of Western Texas Intermediate WTI oil continues to rise on the second day, closing at $85.00 per barrel. The markets are keeping a careful eye on the renewed military standoff between Israel and Palestine in the Middle East. There is worry that this conflict could intensify and spread to other areas of the region, bringing with it geopolitical unpredictability that might affect world markets.

AUDUSD Analysis

AUDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

Australia and Japan agreed to provide Japan with natural resources such as coal, LPG, and iron ore at the right price. The Australian economy will benefit from this agreement, which will increase exports to Japan.

The Australian Dollar AUD finds it difficult to maintain its recent upward trend that started on Wednesday. With the ongoing violence in the Middle East, strong underlying commodity prices supported the Australian dollar’s upward movement. During their fifth Ministerial Economic Dialogue, Australia pledged to guarantee Japan a steady supply of energy resources. This accord signifies a strategic alliance between the two nations, stressing the significance of a steady and dependable supply of energy resources, most likely including coal and LNG. Furthermore, the goal of this commitment is to establish a stable investment climate in Australia’s energy and resources sector. China’s commerce ministry said on Monday that it had chosen to extend its investigation into trade barriers imposed by Taiwan for a further three months. When it comes to exporting goods like coal, natural gas, and iron ore, Australia leads the world. Commodity prices may be impacted by any worsening of trade tensions between China and Taiwan and the dynamics of global trade. The Australian economy and the Australian Dollar AUD may be impacted as a result.

After losing three days in a row, the US Dollar Index DXY has recovered and is currently trading at 106.20 as of this writing. The impressive US Nonfarm Payrolls data released on Friday is what is responsible for the USD’s strength. The performance of the AUDUSD pair is positively impacted by the elevated demand for commodities like gold and energy as a result of the heightened geopolitical tensions in the Middle East. For the fifth Japan-Australia Ministerial Economic Dialogue, Ministers of Resources Madeleine King, Climate Change and Energy Chris Bowen, and Economy, Trade, and Industry Yasutoshi Nishimura of Japan met in Melbourne with Don Farrell of Australia. Speaking to reporters following the meeting, Nishimura emphasised that they had come to an agreement to ensure a steady flow of resources, including LNG, and to create a stable investment climate in Australia’s energy and resource sectors. The Reserve Bank of Australia may decide to raise interest rates, with a peak of 4.35% anticipated by year’s end. This estimate is consistent with inflation continuing to rise above the objective. The September Nonfarm Payrolls report for the United States showed a noteworthy increase of 336,000 jobs, above the 170,000 market expectation. The updated August figure was 227,000.

US Average Hourly Earnings MoM for September were unchanged at 0.2%, below the forecasted 0.3%. The report showed an annual increase of 4.2%, which was less than the 4.3% consistent figure that was expected. Expectations that the Federal Reserve Fed will keep interest rates higher for an extended period of time have contributed to the increase in US Treasury yields as well. The yield on US Treasury bonds maturing in ten years has once again risen to 4.88%, the highest level since 2007. The International Monetary Fund IMF meeting, which is scheduled to discuss tactics for stabilising foreign exchange rates and promoting development, is expected to be watched by investors. Later in the week, attention will also be on the US Core Producer Price Index, which is a critical indicator of inflationary trends and US economic conditions.

NZDUSD Analysis

NZDUSD is moving in the Box pattern and the market has reached the resistance area of the pattern

The NZD dollar is facing significant resistance versus the USD because of this week’s impending political changes. According to analysts, new political parties may implement some economic reforms that increase the likelihood of NZD strengthening against counter pairs in the coming days.

According to the USD Dixy Currency Index, the US dollar has strengthened against all other currencies by 2.60% during the past month. It started the month at 104.17 in early September and reached a high of 106.86 on October 4, 2023. Sharply rising US bond yields, hawkish remarks from Fed members regarding monetary policy, and slightly better-than-expected US ISM manufacturing survey data for September have all contributed to the demand for the US dollar.The remarkable sell-off in US Treasury bonds over the past month has been caused by more than just the US government’s increased issuance of bonds during this time period exceeding investor demand. It has been known for a few months that the significant increase in supply during the September and December quarters is what caused the 10-year bond yield to rise from 3.80% in June to 4.20% in August. However, other factors and market forces have led to the continuation of the massive bond selling that has occurred over the past few weeks, reaching 4.80%. The market’s reaction to each member of the Fed’s monetary policy committee raising their respective “dot-plot” interest rate projections for 2024 is the main cause of the extra bond sales. Compared to earlier projections, a greater number of Fed members now expect the Fed Funds interest rate to remain above 5.00% through 2024. Hedge funds and other leveraged and speculative bond traders have placed fresh bets in the market in recent weeks, betting that these interest rate projections will hold true as the year progresses. US inflation would have to pick back up to an alarming rate in order for the bond market punters to be correct and the interest rate forecasts to be validated.

In this humble writer’s opinion, there is little chance that US inflation will rise from an annual rate in the 2.00% to 3.00% range in late 2023 to above 4.00% in 2024. It is challenging to predict which specific components of the prices of goods and services in the US will surge higher in 2024 after reversing their present downward trends. Rents and housing costs are now declining quickly after a 12-month lag, wage growth is trending downward, and global shipping and freight prices have returned to pre-Covid levels. The selling of bonds that has caused the 10-year yield to soar to 4.80% has nothing to do with the anticipated levels of inflation in the future. It must therefore be extremely speculative in nature, particularly in light of the many US investment bank CEOs who have made audacious predictions that bond yields must rise to levels above 5.00% and 6.00%. Cynics and veterans of the investment market will notice that these guys from investment banking always “talk their book” and that their main motivation is the extreme market volatility that their bank’s bond traders need in order to profit from short selling the bonds. The global bond market devastation, which has driven US 10-year yields to 4.80%, is highly detrimental to borrowers, investors, economies, and equity markets worldwide. Because of how speculative and leveraged the bond selling is, anything could cause a sharp reversal to lower yields as the “short-sold” positioning unravels. A substantial possibility for the reversal trigger would be substantially lower-than-expected actual US inflation data. Less than the +0.30% predicted core and headline inflation increases for the month of September on Friday, October 13 may serve as that catalyst.

It will turn out that the bond sell-off was only temporary because it was speculative in nature rather than grounded in sound economic principles. Similar to the recent sharp rise in crude oil prices from US$70b WTI to over US$93b as a result of supply reductions by OPEC members. Over the past week, the price of oil has suddenly dropped to below US$83b as supply has increased due to higher prices and demand has decreased due to slower economic growth. The expectation in the forex markets that there will be a change of government in New Zealand this Saturday a change that is most definitely not going to be detrimental to the Kiwi dollar—partially explains the NZ dollar’s recent stability in the face of a stronger US dollar and weaker global equity markets. Thus, a decisive, centre right win for National ACT is essentially already factored into the 0.6000 NZD exchange rate.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get Live Free Signals now: forexgdp.com/forex-signals/