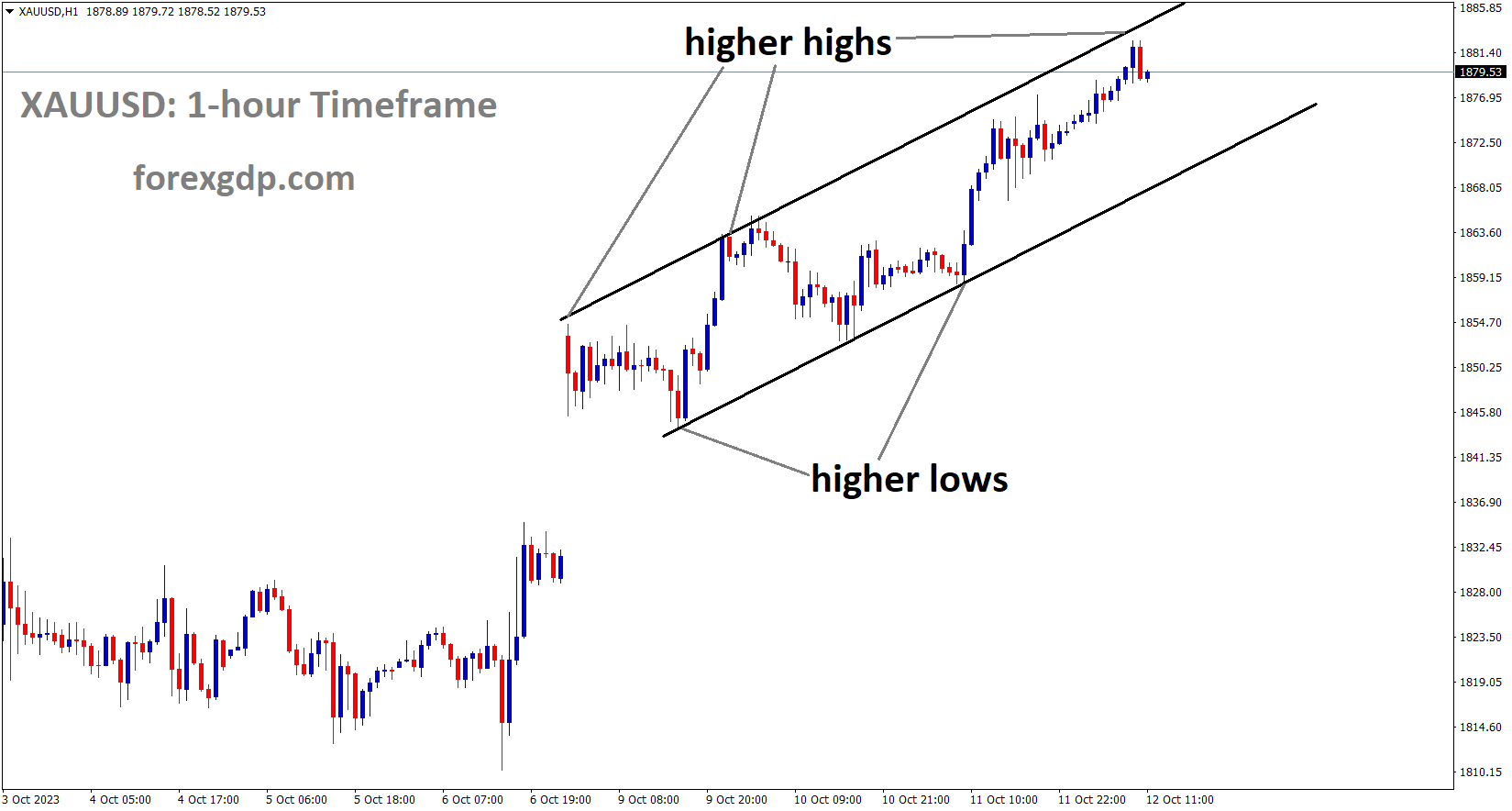

Gold Analysis

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

The outcome of the FOMC meeting minutes did not meet the expectations of US Dollar buyers. Interest rates will remain unchanged, and it is anticipated that inflation will reach its target in the coming year. As a result, Gold prices have surged against the US Dollar.

Amid escalating geopolitical tensions in the Middle East, the precious metal has once again established itself as the preferred safe haven, benefiting from the recent decline in the US Dollar (USD). Additionally, the drop in global bond yields has further boosted the appeal of this non-yielding asset, fueling its ongoing rally.

With its most recent surge, the price of Gold has now recovered more than 30% of the losses it incurred back in September. Notably, this positive momentum remains largely unaffected by the generally upbeat sentiment in the equity markets. Coupled with speculations that the Federal Reserve is approaching the end of its current rate-hiking cycle, the path of least resistance for XAUUSD appears to be upward.

However, traders may exercise caution and await the release of the latest US consumer inflation figures later in the North American session. Any indications of a further moderation in US inflationary pressures would strengthen market expectations of the Fed maintaining its current policy stance in November and could spark speculation about a potential rate cut in Q2 2024. This scenario would set the stage for a further weakening of the US Dollar and increased demand for Gold priced in USD. Conversely, a robust inflation report could leave the door open for at least one more Fed rate hike before year-end and may prompt profit-taking among XAU/USD bulls, although any corrective decline is likely to be short-lived.

The ongoing conflict between Israel and the Palestinian Islamist group, Hamas, continues to drive safe-haven flows towards Gold. Federal Reserve officials have hinted that the recent surge in Treasury yields might reduce the necessity for further rate hikes. Fed Governor Christopher Waller, for instance, suggested that higher market rates could warrant a “watch and see” approach.

In September, the US Producer Price Index (PPI) exceeded expectations, though underlying inflationary pressures appeared to be subsiding. Investors increasingly believe that the Fed is approaching the end of its tightening cycle, with interest rates likely having peaked. The yield on the 10-year US Treasury note has retreated from its recent 2007 highs. This retreat, coupled with the diminishing strength of the US Dollar, has further supported XAU/USD. The minutes from the September FOMC meeting indicated that most Fed members supported the case for one more rate hike. Market participants are now closely watching the latest US consumer inflation figures for insights into the Fed’s future rate-hike trajectory. The headline Consumer Price Index (CPI) is expected to have slowed to 0.3% in September, with the yearly rate ticking down to 3.6%. The more closely monitored Core CPI is forecasted to remain steady at a 0.3% monthly pace and come in at 4.1% year-on-year. The crucial CPI report will significantly impact the Fed’s next policy decision and provide fresh direction for the commodity.

Silver Analysis

XAGUSD Silver price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The September US Producer Price Index (PPI) data surprised with a rise to 2.2% from the previous 2.0%, surpassing the anticipated rate of 1.6%. Following the release of this data, the US Dollar exhibited a modest weakening. Investors are now eagerly awaiting the release of the US Consumer Price Index (CPI) data for September later today.

The US Dollar has encountered mixed performance this week, struggling against the Euro, Sterling, and Swiss Franc, while performing relatively better against the Yen and currencies linked to commodities. This shift in the US Dollar’s fortunes is primarily driven by a notable change in the Federal Reserve’s stance, which has cast a shadow on the outlook for the “big dollar.”

Until this week, the debate had predominantly revolved around the possibility of a rate hike or no hike at the upcoming Federal Open Market Committee (FOMC) meeting. However, in recent days, the market sentiment has shifted towards a more balanced view of the risks associated with future monetary policy. This has opened up the possibility of a potential rate cut further down the road.

The less hawkish tone began on Monday with comments from several Fed speakers and has persisted throughout the week. This culminated with the release of the FOMC meeting minutes from the September meeting, which further underscored the Fed’s hesitancy to raise rates, especially with the rise in yields at the longer end of the Treasury yield curve effectively achieving some of the desired tightening without the need for an adjustment in the short-end target rate.

meeting")

The benchmark 10-year bond yield had reached 4.88% last Friday, marking its highest level since 2007. However, it has since dipped below 4.55%, potentially undoing some of the Fed’s intended tightening. The FOMC minutes explicitly mentioned that participants believed that, with monetary policy already in restrictive territory, the risks to the Committee’s goals had become more balanced.

With the Fed signaling reluctance to raise rates and Treasury yields declining, it’s not surprising that the US Dollar has struggled against most major currencies. The Swiss Franc has particularly benefited from these developments, reversing the gains seen last week when USD/CHF reached a seven-month high. The Swiss National Bank (SNB) has been able to maintain a more accommodative monetary policy due to benign inflation in Switzerland. Its target rate of 1.75% is considerably lower than that of other major central banks, except for the Bank of Japan (BoJ), which has a negative interest rate policy.

Recent US Producer Price Index (PPI) data has come in hotter than expected, with a year-on-year increase of 2.2% up to the end of September, compared to the anticipated 1.6%. The market’s attention now turns to the US Consumer Price Index (CPI) data due later today, but it appears that a substantial deviation from expectations would be required to significantly alter the market’s outlook for the Fed’s interest rate trajectory. Economists surveyed by Bloomberg estimate that the year-on-year headline CPI will be 3.7% up to the end of September.

USDCHF Analysis

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel

Inflation in the Swiss region remains below the target level, necessitating the Swiss National Bank (SNB) to maintain its current hold on monetary policy during its meetings. The performance of the Swiss Franc this week is expected to be influenced by upcoming data on Swiss exports and imports, which are scheduled for release.

USDCHF is currently hovering near its three-week lows. Despite robust economic data coming out of the United States (US), the US Dollar (USD) is encountering challenges stemming from the potential conclusion of the Federal Reserve’s (Fed) rate-hiking cycle. This divergence in perspectives is evident in the recently released Federal Open Market Committee (FOMC) minutes, which underscored the importance of data dependence. There was a suggestion that consensus-building for monetary policy decisions would hinge on achieving a substantial increase in inflation.

In September, the US Producer Price Index (PPI) showed a notable uptick, rising from 2.0% to 2.2%, surpassing the expected rate of 1.6%. The market’s attention is now focused on Thursday’s release of the Consumer Price Index (CPI), with forecasts indicating a potential decrease in the annual rate from 3.7% to 3.6%. Additionally, investors are eagerly awaiting the upcoming weekly Jobless Claims report.

Amidst dovish comments and neutral stances from Federal Reserve officials, there appears to be speculation that the Fed may abandon the idea of a rate hike. Fed Governor Christopher Waller advocates a cautious approach to rate developments, suggesting that tightening in financial markets “would do some of the work for us.” On the other hand, Fed Governor Michelle Bowman leans toward another rate hike, citing persistent inflation above the Fed’s 2% target. These varying viewpoints within the Federal Reserve introduce complexity to the current economic landscape.

The US Dollar Index (DXY) is grappling with these challenges and is currently trading lower, around 105.70 at the time of writing. This struggle is partly attributed to the subdued performance of US Treasury yields, with the 10-year Treasury bond yield standing at 4.57% as of the latest update. Conversely, the Swiss Franc is finding support as a safe-haven currency amidst the ongoing military conflict in the Middle East. Switzerland’s Producer and Import Prices, scheduled for release on Friday, may provide fresh insights into the nation’s inflation outlook.

EURUSD Analysis

EURUSD is moving in the Descending channel and the market has reached the lower high area of the channel

According to ECB policymaker Yannis Stournaras, the decision to not halt bond buying prematurely was the right one, and the Israel-Hamas conflict had a limited impact on the Eurozone. Consequently, the bond buying program will persist until inflation reaches the ECB’s target.

ECB policymaker Yannis Stournaras emphasizes a cautious and flexible approach to the European Central Bank’s emergency bond-buying program (PEPP). His perspective suggests that ending the bond purchases prematurely may not be advisable. This stance is driven by the recognition of ongoing uncertainty, particularly in light of recent events in Israel and Palestine. Stournaras underscores the importance of maintaining flexibility and being ready to take action if circumstances warrant it. This viewpoint reflects the ECB’s commitment to responding to evolving economic and geopolitical developments with a measured and adaptable monetary policy approach.

GBPUSD Analysis

GBPUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In August, the monthly GDP figures exceeded expectations, with a 3-month average reading of 0.30% compared to the anticipated 0.20%. Similarly, the year-on-year (YoY) reading came in stronger at 0.50% against an expected 0.30%. Notably, the services sector showed robust growth, expanding by 0.40% in August. However, there are indications that the production and construction sectors may experience a slowdown.

The UK GDP has shown a positive rebound from the previous month’s unexpected contraction in July, which has been revised lower from an initial estimate of -0.5% to -0.6%. In August, GDP increased by 0.2%, aligning with expectations. The three-month average, which provides a more smoothed measure of GDP, also rose by 0.3%, in line with forecasts.

GBPCHF Analysis

GBPCHF is moving in the Box pattern and the market has reached the support area of the pattern

Notably, the services sector experienced a growth of 0.4% in August, but there were contractions in both the production and construction sectors. The trajectory of UK GDP in 2023 has been marked by fluctuations, reflecting the uncertainty in both the domestic and international economic landscape, especially as the global growth slowdown takes hold.

While progress has been made in addressing inflation, it still remains relatively high compared to other developed economies. The Bank of England will now be closely monitoring next week’s unemployment data and average earnings figures. Positive developments have been observed in the job market with a moderate easing, but concerning wage data recently breached the 8% mark, which is a point of concern for the central bank.

GBPJPY Analysis

GBPJPY has broken the Descending channel in upside

Bank of Japan Board member Asahi Noguchi has stated that wage prices are expected to rise by 3.0%, and inflation is anticipated to reach the 2% target. Only when these conditions are met will we consider refraining from implementing loose monetary policy measures in Japan. Until then, we will continue to maintain such measures.

The Japanese Yen (JPY) has been under pressure due to the Bank of Japan’s prolonged ultra-easy monetary policy stance. Additionally, Bank of Japan board member Asahi Noguchi has come into focus with his remarks, stating that the central bank cannot be overly optimistic about a rapid increase in wage growth. Noguchi attributes inflation to price hikes in imports, which include currency-related factors, and he acknowledges that there is still a significant gap in achieving the 2% inflation target. He underscores that there is currently no immediate requirement to adjust the Yield Curve Control (YCC) policy. Noguchi emphasizes the importance of turning real wages positive and aims to bring wage growth closer to 3%, although he cannot specify a timeline for this to happen.

Earlier in the day, Noguchi shared his perspective, suggesting that if central banks refrain from raising interest rates and inflation moderates, it would help mitigate the risk of a severe economic downturn. He observes that Japan’s economy is gradually on the path to recovery. In a context where inflation expectations are on the rise, Noguchi advocates for some flexibility in maintaining an accommodative policy under the framework of Yield Curve Control (YCC). This approach seeks to strike a balance between promoting economic recovery and effectively managing inflation expectations.

AUDCAD Analysis

AUDCAD is moving in the Descending channel and the market has reached the lower high area of the channel

In August, Canadian building permits surpassed expectations, recording a 3.4% increase compared to the forecasted 0.50%. However, despite this positive economic data, the Canadian Dollar is facing downward pressure against other currencies. This depreciation can be attributed to the cooling down of oil prices, which is affecting the Canadian Dollar’s performance.

Saudi Arabia’s Energy Minister, Prince Abdulaziz bin Salman, has announced that voluntary cuts in oil production will be extended through the remainder of this year. The aim is to bring stability to the oil market and reduce volatility in oil prices, signaling a commitment to maintaining a steady course in the industry.

This week, the primary focus in the market continues to be on inflation expectations. With very few Canadian economic data releases scheduled, the direction of charts will largely depend on how the market reacts to US inflation data for the remainder of the week. In terms of Canadian economic data, there are only a few low-impact releases. Notably, Canadian Building Permits for August exceeded expectations, registering a 3.4% increase compared to the anticipated 0.5%. However, it’s worth mentioning that the previous reading for Building Permits was significantly revised downward, from -1.5% to -3.8%.

Meanwhile, Crude Oil prices are experiencing further softening, retracting from the initial price surge earlier in the week following the escalation of tensions in the Gaza Strip between Israel and Palestinian Hamas over the weekend.

Prince Abdulaziz bin Salman, Saudi Arabia’s Energy Minister, stated on Thursday that they intend to prolong voluntary production cuts until the end of the year. He emphasized that the less volatility there is in the global oil market, the fewer interventions will be necessary. Acknowledging the prevailing uncertainty, he underscored the need for caution and proactive measures in addressing the numerous challenges facing the oil market. The overarching goal is to achieve and maintain stability in the oil market.

AUDUSD Analysis

AUDUSD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The Melbourne Institute’s consumer inflation expectations have risen to 4.85%, up from the previous estimate of 4.6%. This increase is likely influenced by the global surge in oil prices, which could potentially impact Australian consumer spending on oil-related products.

The Australian Dollar has relinquished its earlier gains and is now experiencing losses, despite the uptick in Australian Consumer Inflation Expectations. The Melbourne Institute’s Consumer Inflation Expectations for October have been reported at 4.8%, showing a slight increase from the September figure of 4.6%. This modest rise in consumer expectations regarding inflation in Australia is likely tied to the recent surge in global oil prices, which has a significant impact on consumer sentiment.

The AUDUSD pair could potentially strengthen further, as the possibility of another interest rate hike by the Reserve Bank of Australia (RBA) gains traction. Meanwhile, the US Dollar Index (DXY) is struggling to maintain its position around 105.70 at the moment due to the subdued performance of US Treasury yields. Despite robust economic data in the United States (US), particularly in wholesale inflation, and the release of the Federal Open Market Committee (FOMC) meeting minutes, the US Dollar (USD) is facing challenges.

Speculation is mounting regarding the US Federal Reserve (Fed) possibly abandoning the idea of a rate hike. This speculation is fueled by dovish comments and neutral stances from key officials, introducing an element of uncertainty to the currency’s outlook. In contrast, Australia saw an uptick in inflation in August, largely attributed to elevated oil prices, increasing the likelihood of another interest rate hike by the RBA.

The ongoing Middle East conflict adds complexity to the situation, potentially prompting the RBA to implement a 25 basis points (bps) interest rate hike, bringing it to 4.35% by year-end. The heightened geopolitical tension is driving increased demand for commodities, particularly energy and gold, which is positively affecting the performance of the AUD/USD pair.

Furthermore, Australia’s Westpac Consumer Confidence data for October indicates an improvement in current buying conditions, with the index rising 2.9% following a 1.5% decline in September.

In the US, the Producer Price Index (PPI) surged in September on a yearly basis, jumping from 2.0% to 2.2%, surpassing the expected 1.6%. Core PPI also experienced an increase, rising to 2.7% from the anticipated easing to 2.3%. US Treasury bond yields faced losses on Wednesday, with the 10-year US Treasury bond yield reaching its lowest level at 4.54%. The recently released Federal Open Market Committee (FOMC) minutes revealed a divergence of opinions within the Fed, underscoring the importance of data reliance. The consensus for additional interest rate hikes appears to hinge on a significant uptick in inflation. Some participants argue that as the policy rate approaches its peak, the focus should shift from the extent of rate increases to determining how long to maintain the policy rate at restrictive levels.

In anticipation of Thursday’s Consumer Price Index (CPI) release, there is heightened interest. Projections suggest a dip in the annual rate for September, sliding from 3.7% to 3.6%. Following this release, the weekly Jobless Claims report is expected to provide further insights into the economic landscape.

NZDUSD Analysis

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

ANZ bank analysts anticipate that the third-quarter inflation data, set to be released next week, will show a year-on-year inflation rate of 6.1%. This expectation slightly surpasses the Reserve Bank of New Zealand’s August Monetary Policy Statement forecast, which projected a inflation rate of 6.0%.

Analysts at the Australia and New Zealand Banking Group have provided insights into their expectations for New Zealand’s Consumer Price Index inflation data, which is scheduled for release next Tuesday. They anticipate that annual CPI inflation will have accelerated to 6.1% year-on-year in the third quarter . This projection is slightly higher than the Reserve Bank of New Zealand’s August Monetary Policy Statement forecast of 6.0%.

Several specific drivers are contributing to this anticipated inflation increase, including the cessation of the fuel excise, road-user charges, and public transport subsidies, collectively adding roughly 0.6 percentage points to the headline inflation rate. Additionally, higher oil prices have led to increased fuel costs, and there has been a significant rise in local authority rates bills.

Overall, ANZ’s assessment suggests that the upcoming CPI report will raise questions about whether the Official Cash Rate of 5.50% will be sufficient to bring down persistent domestic inflation in a timely manner. However, it remains uncertain whether the RBNZ will feel an immediate need to raise rates in November or whether they will choose to wait for more evidence before making a decision, with the next opportunity being in February.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/