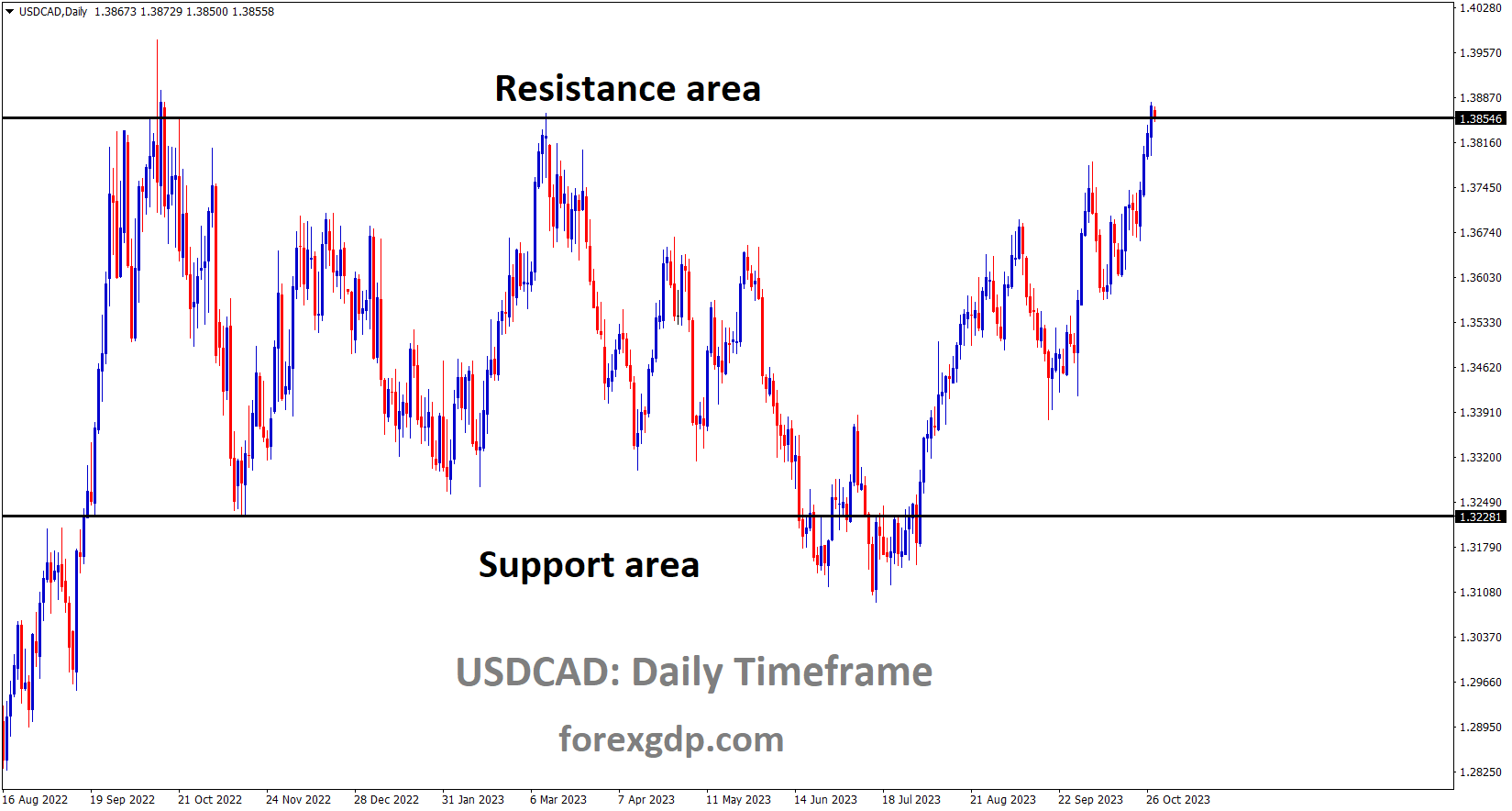

USDCAD Analysis:

USDCAD is moving in the Box pattern and the market has reached the resistance area of the pattern

Bank of Canada Governor Tiff Mackhelm stated that there are no plans for either a decrease or an increase in interest rates. He noted that inflation is currently experiencing a slowdown and projected that by 2025, the inflation rate may align with the 2% target.

The Canadian dollar is currently testing the lower end of its one-year range against the US dollar, following remarks by Bank of Canada Governor Tiff Macklem last week. Macklem suggested that interest rates may have reached their peak. He mentioned that if inflation continues to moderate, there might not be a need for further rate hikes. Nevertheless, the central bank governor emphasized that the Bank of Canada would require “clear evidence” of inflation moving toward the 2% target before considering any interest rate cuts.

In its most recent decision, the Bank of Canada opted to maintain benchmark rates at a 22-year high, but it left the possibility of additional rate hikes open, citing the potential for inflation to exceed its target for another two years. Meanwhile, financial markets are currently pricing in a very slim probability of another rate increase at the next meeting scheduled for December.

Gold Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The increase in gold prices can be attributed to both geopolitical tensions in Israel and the consideration of gold as a non-bearing asset.

Last Friday, the spot gold price surpassed the significant milestone of US$ 2,000, as market participants brace themselves for this week’s Federal Open Market Committee (FOMC) meeting, scheduled to conclude on Wednesday.

While Treasury yields have eased slightly from recent highs, they remain elevated, particularly the benchmark 10-year bond, which was trading at 5.02% last week, marking its highest yield since 2007. Subsequently, it experienced a rapid decline towards 4.80%, leading to volatile price movements.

The rise in returns on US Government debt has provided support for the US Dollar. Additionally, perceived safe-haven assets like the USD and gold have appreciated, partly due to the geopolitical instability in the Middle East, which has contributed to concerns about economic growth and riskier assets.

In simplified terms, when both the US Dollar and Treasury yields increase, gold can sometimes face selling pressure. Similarly, gold occasionally declines when US real yields rise, as it is considered a non-interest-bearing asset.

Throughout 2023, US real yields have steadily climbed and recently reached a 15-year peak, particularly at the 10-year point on the yield curve, exceeding 2.60%. Real yield is calculated as the nominal yield minus the market-derived inflation rate from Treasury inflation-protected securities (TIPS) of the same maturity.

This surge in real yields is the result of a combination of higher nominal yields and a decrease in inflation expectations.

As depicted in the chart below, the elevated 10-year Treasury yields, real yields, and the DXY (USD) index have yet to significantly impact the gold price. However, it’s worth monitoring these markets in case of sudden movements.

The interest rate market is currently pricing in no change for the Fed funds target rate at the upcoming FOMC meeting on Wednesday. However, the post-decision remarks from Fed Chair Jerome Powell could potentially influence the gold price. For more insights into how central banks affect the financial markets, please click on the banner.

Silver Analysis:

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel

It is expected that the Federal Reserve (Fed) will likely pause in the upcoming meeting, primarily because major economic data has been surpassing expectations.

The rally of the US dollar has paused in anticipation of the October 31 to November 1 Federal Open Market Committee (FOMC) meeting. This pause is partly attributed to the dovish statements made by Fed officials earlier in the month, highlighting that the increase in yields has eased financial conditions and reduced the immediate necessity for tightening monetary policy. Consequently, it is widely anticipated that the Fed will keep interest rates unchanged in the upcoming meeting.

will likely pause in the upcoming meeting")

Fed Chair Powell, while acknowledging the recent tightening in financial conditions, has not ruled out the possibility of future rate hikes. Additionally, robust economic data in the United States and the perception of higher interest rates for a longer period have led to a shift away from expectations of rate cuts in 2025.

However, for the current consolidation to transform into a reversal, several factors would need to change. This includes a potential shift in US exceptionalism, which refers to the US economy’s relative outperformance compared to the rest of the world, and a more broadly hawkish stance from the Fed. Until these conditions change, it may be premature to conclude that the US dollar has reached its peak.

USDCHF Analysis:

USDCHF has broken the Descending channel in upside

The Swiss ZEW Survey for October showed a decrease to -37.8, following a decline of 27.6 in September. Consequently, the Swiss Franc weakened against other currencies.

The Greenback is currently encountering a hurdle, as market expectations point towards the likelihood of the US Federal Reserve (Fed) maintaining the interest rates at 5.5% in the forthcoming Wednesday meeting. Moreover, the US Core Personal Consumption Expenditures Price Index (YoY) saw a slight easing to 3.7% in September, down from the 3.8% reading in August. This easing may constrain the potential advances of the USD/CHF currency pair. However, when examining the monthly data, it revealed an as-expected increase, with a 0.3% reading compared to the previous 0.1%, though it failed to invigorate the USD.

The ongoing escalation of the conflict in the Middle East could lend support to the safe-haven Swiss Franc (CHF) against the US Dollar (USD). Israel has expanded its ground operations in Gaza and carried out multiple attacks.

The US Dollar Index (DXY) seems to be maintaining a subdued presence, attributed to the decline in US Treasury yields observed on Friday. However, there are indications of a potential rebound in the 10-year US Bond yield, currently standing at 4.87% as of the time of this report.

Additionally, a recent report showed a decline in Switzerland’s business conditions and labor market, with the ZEW Survey Expectations falling to 37.8 in October, following a previous decline of 27.6.

Looking ahead, investors will be closely monitoring key economic events, including the US ADP Employment Change and ISM Manufacturing PMI for October during the week. On the Swiss economic calendar, Real Retail Sales (YoY) data will be of interest on Tuesday.

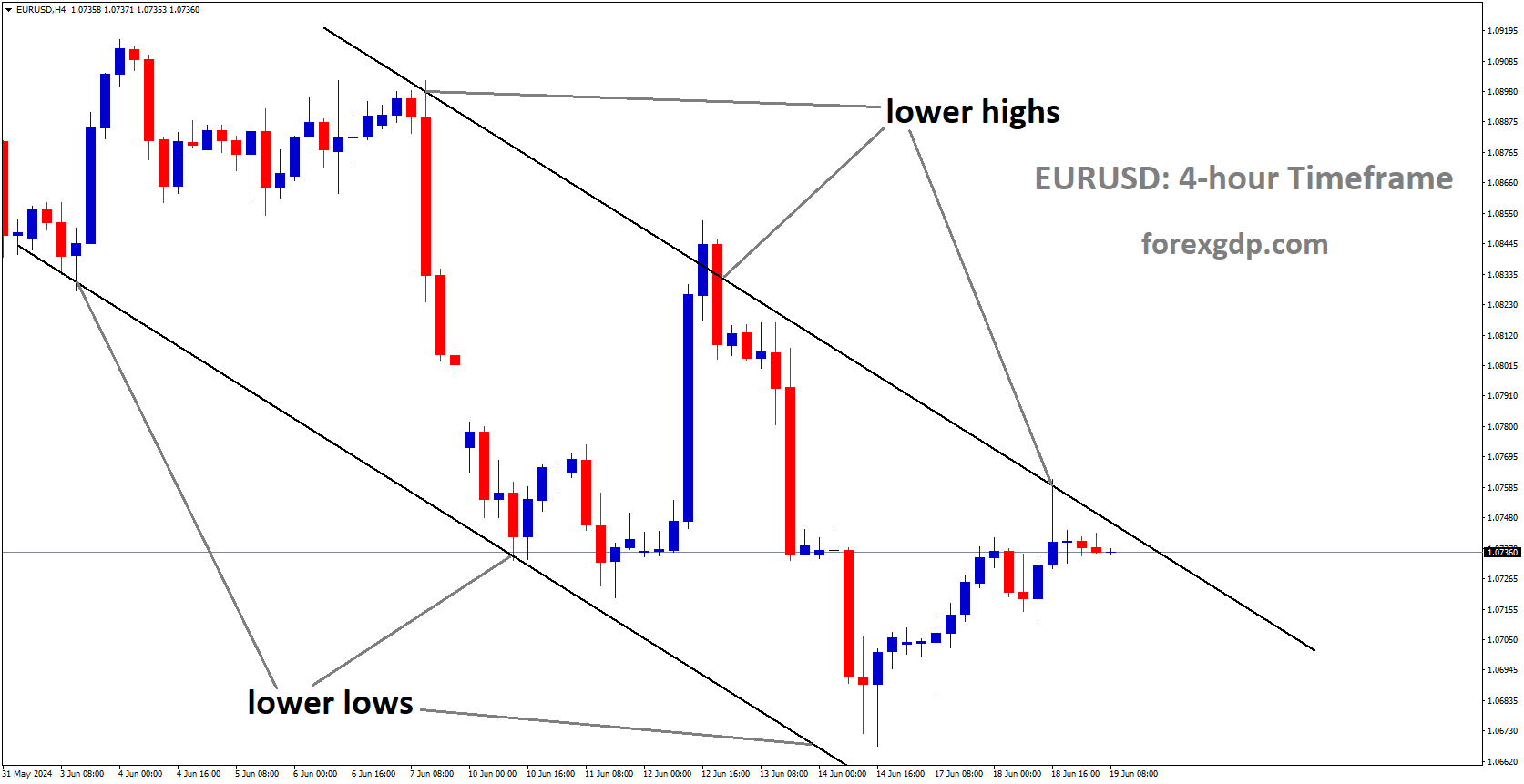

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

Boris Vujcic, a member of the ECB Governing Council, has stated that there won’t be any further rate hikes at this point. Instead, the focus will be on bringing inflation in line with our 2% target by 2025.

Boris Vujčić, a member of the ECB Governing Council and the Governor of the Croatian National Bank, shared in a television interview with Croatian state broadcaster HRT1 that the recent news regarding the end of rate hikes is not surprising and has been anticipated for several weeks. Vujčić expressed confidence that inflation would align with the ECB’s target by 2025.

He noted that the process of increasing interest rates has concluded for the time being. Currently, there is a trend of falling inflation, characterized by a disinflation process. Vujčić also highlighted that after implementing various measures to curb lending, inflation has decreased.

EURJPY Analysis:

EURJPY is moving in the Box pattern and the market has fallen from the resistance area of the pattern

It is expected that in tomorrow’s meeting, the Bank of Japan will consider raising the Yield Curve Control (YCC) target from 1% to 1.5%. If this adjustment occurs, it could lead to a strengthening of the Japanese yen against other currencies.

Next week, the Federal Reserve, the Bank of England, and the Bank of Japan will all announce their latest monetary policy decisions. Among these central banks, it is the Bank of Japan that is expected to potentially trigger a fresh wave of market volatility. While the Fed and the BoE are anticipated to maintain their current policy settings, the BoJ might make adjustments to its yield curve control policy, potentially allowing Japanese Government Bond (JGB) yields to rise. Presently, the Japanese central bank sets a cap on the 10-year bond yield at 1% and intervenes if this level comes under pressure. However, there is speculation in the market that the BoJ may consider allowing market yields to increase to 1.5%, a move with a hawkish undertone that could lead to yen strengthening.

Today, the latest Tokyo Consumer Price Index (CPI) reading exceeded market expectations, indicating rising price pressures. This CPI reading is often viewed as a proxy for nationwide inflation trends and might push the Bank of Japan towards recognizing that inflation in Japan is gradually becoming more entrenched. If the BoJ revises its inflation outlook upward, it could lead to a strengthening of the Japanese yen against other currencies.

GBPUSD Analysis:

GBPUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

The GBP is facing weakness against the USD due to escalating tensions in the Middle East. Moreover, domestic data from the UK is showing vulnerability, and the Bank of England is expected to keep interest rates unchanged in the upcoming meeting.

The recent escalation of the conflict in the Middle East has had a significant impact on the financial markets, with increased volatility being the prevailing theme. Notably, gold prices have surged past the $2,000 mark for the first time since May 16, 2023. This surge in gold prices comes in response to news that Israel has intensified its ground offensive in Gaza, leading to the destruction of communication and internet services in Palestine, as reported by Pallet, the Palestinian telecommunications company. Simultaneously, Israeli military authorities have confirmed that they are conducting extensive attacks on Gaza, with a particular focus on underground targets and areas associated with terrorist activities. This development has prompted reactions from around the world, with the United States urging Israel to refrain from a “full-scale” invasion and instead employ a more surgical approach utilizing aircraft and special operation forces.

Furthermore, recent economic data from the United States indicates that inflation continues to moderate but is struggling to drop below the 3% threshold. The Federal Reserve’s preferred inflation gauge, the Core Personal Consumption Expenditures (PCE) Index, declined slightly from 3.8% to 3.7% year-on-year in September, while the overall PCE remained unchanged compared to August at 3.4%.

In addition, the University of Michigan’s Consumer Sentiment Index showed a slight improvement in overall consumer sentiment, but it also revealed deteriorating expectations regarding inflation. Americans now anticipate a 4.2% increase in prices over a one-year period and expect prices to remain at a 3% level over a five-year period.

Looking ahead to next week, the economic calendar in the UK will feature the FS&P Global/CIPS PMIs along with the Bank of England’s monetary policy decision. On the US front, upcoming data releases include the Conference Board Consumer Confidence Index, S&P Global and ISM Manufacturing PMIs, US Nonfarm Payrolls report, and the monetary policy decision from the US Federal Reserve.

AUDUSD Analysis:

AUDUSD is moving in the Descending triangle pattern and the market has reached the lower high area of the pattern

Stronger-than-anticipated retail sales data for the month of September has bolstered the Australian Dollar, causing it to appreciate against other currencies. There is also an expectation among economists that the Reserve Bank of Australia (RBA) will likely implement a 25 basis points (bps) interest rate hike in the upcoming meeting next week.

The AUDUSD pair continues to strengthen, mainly due to a weakening US Dollar (USD) influenced by recent economic data releases from the United States (US). Moreover, there is growing anticipation that the Reserve Bank of Australia (RBA) will implement a policy rate increase in the upcoming meeting scheduled for November 7.

Australia’s Retail Sales s.a. (MoM) for September pleasantly surprised the market with a substantial increase, surpassing both market consensus and the previous figure. Additionally, during the previous week, Australia’s Consumer Price Index (CPI) exhibited growth in the third quarter of 2023, surpassing the uptick observed in the second quarter. This heightened inflation scenario increases the likelihood of a 25 basis points rate hike by the RBA during its upcoming policy meeting on November 7. Reports suggest that the US and China have tentatively agreed to hold a meeting between Presidents Joe Biden and Xi Jinping in November, potentially opening the door for constructive dialogue between the two nations. The positive market sentiment stemming from this development could potentially boost the commodity-linked Australian Dollar. Furthermore, investors will closely monitor Chinese PMI data set to be released during the week.

In contrast, the US Dollar Index (DXY) is striving to regain lost ground following recent setbacks. The Greenback encountered resistance as the Core Personal Consumption Expenditures Price Index (YoY) showed a decline in September. However, the monthly data revealed an expected increase. The University of Michigan Consumer Index exceeded expectations in October but failed to give a favorable boost to the US Dollar. This suggests that the market is anticipating no changes to interest rates in the upcoming Federal Open Market Committee (FOMC) meeting.

Australia’s Retail Sales s.a. (MoM) for September posted a substantial increase of 0.9%, exceeding the market consensus of 0.3% and the previous figure of 0.2%. Australia’s Producer Price Index (PPI) exhibited a slight decline, with a yearly rate of 3.8% in the third quarter (Q3), down from the 3.9% recorded in the previous quarter. On a quarterly basis, the nation’s PPI surged to 1.8%, a notable rise from the previous reading of 0.5%. Australia’s Consumer Price Index (CPI) for the third quarter of 2023 reached 1.2%, surpassing the 0.8% uptick in the previous quarter and the market consensus of 1.1% for the same period.

Australia’s S&P Global Composite PMI for October declined to 47.3 from the prior reading of 51.5. The Manufacturing PMI experienced a slight dip to 48.0 compared to the previous figure of 48.7, and the Services PMI fell into contraction territory, dropping to 47.6 from the previous month’s reading of 51.8. The RBA expressed heightened concerns regarding the inflationary impact resulting from supply shocks. RBA Governor Michele Bullock stated that if inflation persists above projections, the RBA will take appropriate policy measures. There is also an observable deceleration in demand, with per capita consumption on the decline.

The US Core Personal Consumption Expenditures Price Index (YoY) decreased to 3.7% in September from the previous reading of 3.8%. However, the monthly index increased to 0.3%, as anticipated, up from 0.1% previously.

The University of Michigan Consumer Index exceeded expectations in October, reporting a figure of 63.8, higher than the anticipated 63.0. Market sentiment currently leans towards the expectation of no changes to interest rates by the US Federal Reserve (Fed) in the upcoming meeting scheduled for Wednesday. The preliminary US Gross Domestic Product (GDP) Annualized data showed growth in the third quarter, expanding by 4.9%, a significant improvement from the previous reading of a 2.1% expansion and surpassing the market expectation of 4.2%. However, there was a decrease in US Core Personal Consumption Expenditures, declining to 2.4% in the third quarter from the 3.7% recorded previously. Investors will be closely monitoring the US ADP Employment Change, ISM Manufacturing PMI for October, along with the Fed Interest Rate Decision on Wednesday.

AUDCHF Analysis:

AUDCHF has broken the Descending channel in upside

The trade deal between Australia and the European Union remains open, with negotiations currently on hold, as stated by Australian Trade Minister Don Farell. There is optimism that a deal may be reached with the European Union in the future.

Australian Trade Minister Don Farrell has made comments indicating that discussions regarding a Free Trade Agreement with the European Union have come to a standstill. Differences on several key issues have prevented both sides from reaching a mutually agreeable solution. Regrettably, we have encountered challenges in making headway. Nevertheless, negotiations will persist, and I remain optimistic that, in due course, we will achieve an agreement that is advantageous for both Australia and our European counterparts.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

In the upcoming week, it is expected that the Q3 Employment Change for the New Zealand Dollar (NZD) will experience a slowdown, decreasing to 0.40% from the 1.0% reported in the previous quarter. Additionally, there is an anticipation that the unemployment rate will increase slightly to 3.9%, up from the expected 3.6%.

The New Zealand Dollar (Kiwi) reached a new low for the past eleven months this week, touching 0.5772 on Thursday. Currently, the NZDUSD pair is encountering resistance that is preventing a successful rebound. The US Personal Consumption Expenditure (PCE) Index figures met expectations, and attention is now turning to the Federal Reserve (Fed) meeting scheduled for next week.

It is widely anticipated that the US central bank will refrain from raising interest rates. Investors will be closely monitoring Fed Chairman Jerome Powell’s speech, scheduled half an hour after the Fed’s rate announcement, and will be attentive to any shifts in the Fed’s communication. Despite the expected rate hold, markets are increasingly pricing in the possibility of one final rate hike from the Fed in December, as inflationary pressures persistently remain higher than initially anticipated by the markets.

Additionally, next week includes the release of New Zealand labor market data on late Tuesday. The expected scenario is that the NZ Unemployment Rate will edge up from 3.6% to 3.9% for the third quarter, and there is an anticipation of a slowdown in hiring as reflected in the NZ Employment Change, with Q3 new job additions expected to increase by only 0.4%, a decline from the 1.0% growth seen in the previous quarter.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/