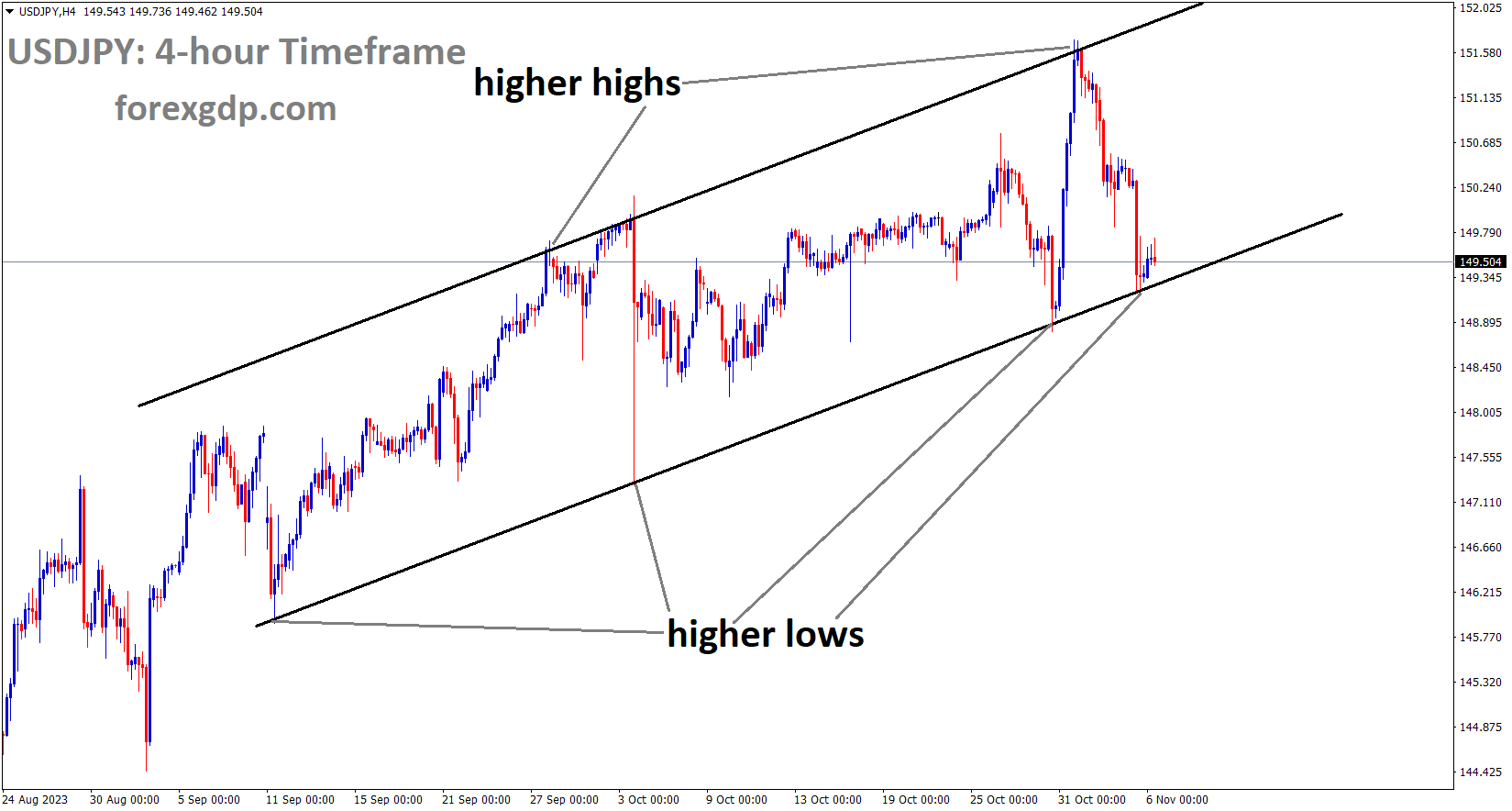

USDJPY Analysis:

USDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

The Japanese Yen remains weak in the market, primarily due to the Bank of Japan’s ongoing bond purchases and its accommodative monetary policy. In the recent meeting held last week, there were no alterations made to the existing policy settings.

Last week’s Bank of Japan meeting marked a small step toward policy normalization as the Central Bank adjusted its Yield Curve Control policy. While the BoJ maintained its target for the JGB 10Y yield at around 0%, it redefined 1% as the upper band instead of a strict cap as it had been previously. This move by the BoJ was perceived by the markets as a dovish signal, suggesting that the BoJ might not immediately intervene as the yield approaches 1%. Looking at the probability of a rate hike from the BoJ, market participants are currently pricing in a 70% chance of a hike in April 2024. Interestingly, as the week progressed, the US Dollar lost some of its early-week strength, and the reduction in the yield differential also favored the Japanese Yen. The FOMC meeting in the US added to this sentiment, as market participants began to increase their bets that the Fed’s rate hike cycle might be coming to an end. Looking ahead, there are no high-impact data releases expected from Japan, but the BoJ meeting minutes could provide additional insights into the policymakers’ thought process and their outlook.

In the US, data releases will slow down, with speeches from Fed Chair Powell scheduled for both November 8th and 9th before the focus turns to the Michigan Consumer Sentiment data. It will be interesting to hear Chair Powell’s comments and whether he will push back on the emerging dovish narrative surrounding future rate hikes. However, following Friday’s jobs data, Chair Powell may unintentionally reinforce the dovish narrative. If this trend continues, the BoJ could be the primary beneficiary, and USDJPY might enter another phase of consolidation driven by ongoing US Dollar weakness. Of course, there are other potential factors that could come into play, such as events in the Middle East, which might provide support for the US Dollar if signs of contagion emerge next week. These developments should be closely monitored.

Gold Analysis:

XAUUSD Gold price has broken the Descending channel in upside

Gold prices saw an increase as the US Dollar weakened in the market. The US Non-Farm Payrolls (NFP) data for last week came in lower than anticipated, and there were dovish hints from the Federal Reserve (Fed) regarding monetary policy settings. These unfavorable developments resulted in the US Dollar declining in value compared to Gold prices.

The price of gold has broken out of its consolidation phase following a report from the United States Bureau of Labor Statistics indicating a slowdown in job growth for October. Nonfarm Payrolls came in at 150,000, falling short of expectations for 180,000 and the revised figure of 297,000 from September. This drop in job growth was expected, as approximately 30,000 United Auto Workers union members had gone on strike against the “Big Three” car manufacturers in Detroit.

Furthermore, the Unemployment Rate increased to 3.9%, exceeding both expectations and the previous rate of 3.8%. In addition to the headline job growth figure, the Average Hourly Earnings data, which offers insights into consumer spending and inflation, showed a slower monthly increase of 0.2% for October, compared to the consensus and the previous month’s reading of 0.3%. However, the annual Average Hourly Earnings data saw a slightly higher growth rate of 4.1%, surpassing the expected 4.0% but remaining below the previous reading of 4.2%.

The subdued labor market and slow wage growth have tempered expectations for another interest rate hike by the Federal Reserve (Fed). Gold demand in the near term has been bolstered by ongoing geopolitical tensions in the Middle East and the anticipation that the Fed will maintain elevated interest rates for an extended period due to the weak job growth in October.

Following the release of the lackluster US NFP report, the price of gold surged above the psychological resistance level of $2,000. The precious metal is poised for further gains amid various favorable factors, including soft labor demand and escalating tensions in the Israel-Palestine conflict. Investors are optimistic that the Federal Reserve may have concluded its interest rate hikes after leaving rates unchanged in the 5.25%-5.50% range for the second consecutive time. However, Fed Chair Jerome Powell has left the door open for additional rate hikes, citing robust retail demand and favorable labor market conditions, which could sustain inflationary pressures.

The US Dollar Index found intermediate support around 106.00 as investors adopted a cautious stance ahead of the labor market data. Although 10-year US Treasury yields rebounded to approximately 4.67%, they remain subdued amid expectations that the Fed’s rate-tightening cycle may be coming to an end. According to the CME Fedwatch tool, over 80% of traders anticipate that monetary policy will remain unchanged for the remainder of the year.

In addition to these factors, the deepening tensions in the Middle East have contributed to the positive sentiment surrounding gold. The Israeli military has surrounded Gaza and is prepared for a ground assault. US Secretary of State Antony Blinken has arrived in Israel with the aim of negotiating a temporary pause in the ground invasion plan by Israeli troops to facilitate the secure delivery of humanitarian aid and aid in hostage negotiations.

Meanwhile, the US Institute for Supply Management Services PMI for October disappointed expectations, with the Services PMI, a key indicator of activity in the US service sector representing a significant portion of the US economy, declining to 51.8, below the expected 53.0 and the September reading of 53.6. On a positive note, New Orders for the service industry showed significant growth, rising to 55.5 from the previous figure of 51.8.

Silver Analysis:

XAGUSD Silver price is moving in the box pattern and the market has rebounded from the support area of the pattern

Thomas Barkin, the President of the Richmond Federal Reserve, expressed his belief that a 25 basis points rate hike alone may not be sufficient to bring inflation back to the 2% target. He also clarified that rate cuts are not under consideration at the moment. He mentioned that middle-class individuals tend to reduce spending when faced with economic challenges, while high-income individuals are less likely to curtail their expenditures. Furthermore, he stated that tensions in the Middle East are unlikely to have a significant impact on the US economy and labor market data.

During an interview with CNBC on Friday, Thomas Barkin, President of the Federal Reserve Bank of Richmond, expressed his satisfaction with the diminishing pressure observed in jobs data and highlighted that the labor market was achieving a better balance, according to Reuters. He emphasized that the Federal Reserve requires more data before making its next rate decision and remains focused on observing a decrease in inflation. Barkin mentioned that he believes market reactions are influenced by data and cautioned against viewing a 25 basis point rate adjustment as a solution to all global issues. He noted that there is some evidence that price setters are losing their pricing power, although many still retain it.

Additionally, he pointed out that lower-end consumers are changing their spending habits, whereas high-end consumers are not significantly reducing their expenditures. Barkin expressed his satisfaction with recent productivity data and indicated that rate cuts are still not imminent in his view. He expressed hope and expectations of further progress in reducing inflation but acknowledged uncertainty about whether the Fed has reached the peak of its rate hike cycle. He emphasized the significant risks associated with both overly aggressive and overly lenient monetary policy, and he noted that the ongoing turmoil in the Middle East has not yet had a substantial impact on the data.

USDCHF Analysis:

USDCHF has broken the Ascending channel in downside

The Swiss National Bank (SNB) reported a quarterly loss last week, which was disappointing for investors. SNB had increased its investments in foreign bonds, particularly US Treasuries; however, the appreciation of the Swiss Franc within its domestic borders affected the profits generated from its foreign assets. Up to this point, the Federal Reserve (Fed) has not received any profits from SNB.

In the third quarter, the Swiss National Bank (SNB) incurred a billion-dollar loss. The value of the foreign bonds that the SNB had acquired in recent years has significantly decreased. Bond prices tend to decline when interest rates rise, which has led to the challenges stemming from past monetary policies affecting the present.

Another consequence of these policies is the strengthening of the Swiss Franc, which has helped maintain low import prices and, consequently, a low inflation rate. However, this has placed a burden on export-oriented companies. Additionally, the SNB’s foreign currency investments have suffered as the Franc has gained strength against most other currencies.

incurred a billion-dollar loss")

Economist Adriel Jost warns that the SNB’s credibility may even be at risk due to these developments. The underlying issue is that the SNB has invested a significant portion of its foreign currency assets, acquired for the purpose of exchange rate control, in government debt from major currency areas, particularly in US bonds. This has exposed the SNB to the uncertainties of the US debt situation, characterized by what Jost describes as an irresponsible fiscal policy in which the US takes on debt and relies on central banks for financing.

While the actual whirlpool of challenges may lie ahead, the substantial losses on these investments are already a reality. It appears increasingly unlikely that the federal government and cantons will receive any profits from the SNB this year. Their earnings are expected to fall short, supporting the views of those who have cautioned cantons against expecting fixed profit distributions from the central bank.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

In September, German factory orders defied expectations by rising to 0.20%, contrary to the anticipated 1.6% decline following a robust 3.9% increase in August. The Euro currency saw an upward movement following the release of this news. When considering the annual figures, German orders for the year registered at 4.3%, showing a significant improvement compared to the 6.3% slump observed in the previous month.

Germany’s Factory Orders defied expectations by increasing in September, as reported by the Federal Statistics Office. This data indicates that the German manufacturing sector continues to maintain its recovery momentum. On a monthly basis, contracts for goods labeled as ‘Made in Germany’ grew by 0.2%. This growth, while less substantial than the 3.9% increase observed in August, surpassed market predictions of a 1.0% decline. Furthermore, on an annual basis, Germany’s Industrial Orders declined by 4.3% in the reported month, a less severe drop compared to the previous decline of 6.3%.

EURNZD Analysis:

EURNZD has broken the Box pattern in downside

In October, the Non-Farm Payrolls data for Friday reported the addition of 150,000 jobs, falling short of the expected 180,000 and significantly lower than the 297,000 jobs reported the previous month. The US unemployment rate for the same period came in at 3.9%, slightly exceeding the expected rate of 3.8%. Following the release of this data on Friday, the New Zealand Dollar (NZD) experienced a rally in its value.

The US Dollar is under significant selling pressure following the release of weak labor market data, leading to a decline in US Treasury yields and increased hawkish expectations for the Federal Reserve’s December meeting. In contrast, there were no significant data releases for the New Zealand Dollar.

The latest report from the US Bureau of Labor Statistics dealt a blow to market expectations, as Nonfarm Payrolls for October fell short of projections. The report revealed that the US economy added only 150,000 jobs, falling below the anticipated 180,000 and showing a slowdown from the revised prior figure of 297,000. Furthermore, the Unemployment Rate for the same period increased to 3.9%, surpassing the projected 3.8%. Despite these labor market challenges, Average Hourly Earnings for October exhibited sluggish monthly growth of 0.2%. However, they managed to climb to 4.1% year-over-year , exceeding the expected 4% and surpassing the previous figure of 4.3%.

Concurrently, US Treasury yields are continuing to decline, with the 2-year rate reaching its lowest level since early September at 4.83%. Likewise, longer-term rates, such as the 5 and 10-year rates, retreated to approximately 4.50% and 4.54%, respectively. In anticipation of the December Fed meeting, the CME FedWatch Tool indicates that the probability of a 25 basis point rate hike has declined to a mere 9%, intensifying the selling pressure on the US Dollar. On November 14th, the US will release inflation rate figures for October, which will be closely monitored by investors as they continue to shape their expectations.

GBPUSD Analysis:

GBPUSD has broken the Descending channel in upside

Last week, the Bank of England decided to keep its monetary policy settings unchanged. This development has had a positive impact on the value of the GBP relative to the USD. Additionally, this week, we are expecting to see the release of Q3 GDP data. The prevailing weakness of the USD in the market is contributing to the strength of the GBP.

During last week’s Bank of England meeting, the Monetary Policy Committee kept interest rates unchanged, as widely anticipated. However, Governor Andrew Bailey’s slightly hawkish remarks in the post-decision commentary pushed back expectations of a potential rate cut in the UK further into the next year, providing support for the British Pound.

Earlier today, the latest US Jobs Report revealed that 150,000 jobs were added in October, falling short of market expectations of 180,000. Additionally, the previous month’s job figure was revised downward from the previously reported 336,000 to 297,000, while the August figure was revised down from 227,000 to 165,000. Furthermore, the unemployment rate experienced a marginal increase from the prior reading of 3.8% to 3.9%.

This week, US Treasury yields have been on a downward trend, and the decline accelerated after the release of the Non-Farm Payrolls (NFP) report. There is a growing sentiment that interest rates in the US may have reached their peak, and given the potential for a recession in the coming months, there is an increasing belief that rate cuts may be necessary sooner rather than later next year. The benchmark US 10-year yield reached a new 16-year high of 5.02% in late October but has since eased to 4.53%.

GBPCHF Analysis:

GBPCHF is moving in the Descending channel and the market has reached the lower high area of the channel

According to Bank of England Executive Director Andrew Hauser, banks should ensure they have adequate liquidity reserves in case of economic concerns or inflationary pressures. It is imperative that banks maintain a sufficient liquidity cushion to address such situations.

On Friday, Andrew Hauser, Executive Director – Markets at the Bank of England, emphasized the importance of ensuring that banks’ liquidity insurance remains suitable in light of increasing technological changes that pose a higher risk of rapid and substantial deposit runs. He noted that following the unwind of Quantitative Tightening, the Bank of England will need to provide a significantly larger amount of reserves compared to the period before the 2008 financial crisis.

Furthermore, Hauser mentioned the bank’s commitment to enhancing alternative liquidity sources for banks and the intention to adjust the Bank of England’s liquidity toolkit to reintroduce market discipline into banks’ liquidity management. However, he acknowledged that there are real limitations in the extent to which the Bank of England can use price-based incentives to manage banks’ reserve demand. Additionally, he highlighted the complexities associated with non-price levers and the need to be cautious to avoid risks to monetary control and financial stability.

CADCHF Analysis:

CADCHF is moving in an Ascending channel and the market has fallen from the higher high area of the channel

In October, Canada experienced an employment change of 17.5K jobs added, falling short of the expected 22.5K and significantly lower than the previous month’s figure of 63.8K. The unemployment rate also increased, reaching 5.7%, which is the highest reading compared to the forecasted 5.6% and the 5.5% rate recorded in September.

The Canadian Dollar is strengthening against the US Dollar following a US Nonfarm Payrolls report that fell short of expectations, marking its lowest reading since February 2021. This data miss is seen positively by investors who have been hoping for softer economic data in the US, aiming to persuade the Federal Reserve (Fed) that further rate hikes are unnecessary and to nudge the central bank closer to potential rate cuts. The CAD gains ground as the US NFP report records only 150,000 job additions, the lowest level in nearly three years. Additionally, US wages also failed to meet expectations, with Month-over-Month Average Hourly Earnings increasing by only 0.2%, below the forecasted 0.3%. The previous month’s figure was revised upward from 0.2% to 0.3%.

Meanwhile, Canada’s Net Change in Employment came in below expectations at 17.5K, falling short of the anticipated 22.5K, with a previous figure of 63.8K. The data highlights a low-quality employment situation, characterized by a surge in part-time job additions while full-time positions declined. The majority of job additions occurred in the services sector, with the goods sector adding only 7.5K jobs. Canada’s Unemployment Rate for October increased to 5.7%, the highest level since February 2022, exceeding the forecasted 5.6% and continuing the trend from September’s 5.5% reading. Similarly, the US Unemployment Rate also rose to 3.9%, contrary to expectations of it remaining at 3.8%. The US ISM Services Purchasing Manager Index also missed expectations, declining to 51.8 for October. In summary, the US Nonfarm Payrolls report showed an increase of 150,000 jobs in October, falling short of the anticipated 180,000.

AUDCAD Analysis:

AUDCAD is moving in an Ascending channel and the market has reached the higher high area of the channel

In anticipation of tomorrow’s interest rate decision by the Reserve Bank of Australia (RBA), the Australian Dollar is maintaining a positive stance, primarily driven by expectations of a 25 basis points rate hike in the upcoming meeting. The third-quarter Consumer Price Index (CPI) data has surpassed that of the second quarter, instilling confidence among analysts that the RBA may indeed opt for a rate increase.

On the domestic front, the Reserve Bank of Australia (RBA) is scheduled to meet to discuss monetary policy on Tuesday, coinciding with the Melbourne Cup, a globally-watched horse race. Recent comments from RBA officials have strongly hinted at a rate hike, consistent with what was previously suggested more than two weeks ago. RBA Governor Michele Bullock, who assumed her role in September following a government review of the bank, has emphasized the importance of more effective communication during her tenure. The language used in the October meeting minutes and comments from Assistant Governor Chris Kent and Governor Bullock has been notably hawkish, indicating a willingness to consider further tightening to bring down persistently elevated inflation levels.

is scheduled to meet to discuss monetary policy on Tuesday")

The RBA Board has expressed a low tolerance for a slower return of inflation to its target than currently expected. The decision on whether to raise interest rates further hinges on incoming data and its impact on the economic outlook and risk assessment. The challenge lies in the series of supply shocks that have kept inflation high, leading to adjustments in people’s inflation expectations, which could further entrench inflationary pressures.

Following the release of CPI data, Ms. Bullock refrained from confirming a rate hike as definite, leading some in the market and media to interpret her stance as dovish. Treasurer Jim Chalmers also chimed in, stating that he didn’t believe the latest CPI data warranted a rate hike, a surprising comment given his previous support for the RBA’s independence. However, with a tight labor market, rising inflation, and soaring housing prices, the RBA’s current stance appears less restrictive compared to many other jurisdictions grappling with price pressures. If the RBA does not proceed with a rate hike in either November or December, its credibility in fighting inflation may be questioned. While an RBA rate hike could initially boost the Aussie Dollar, global factors are expected to continue influencing its exchange rate over the medium and long term.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/