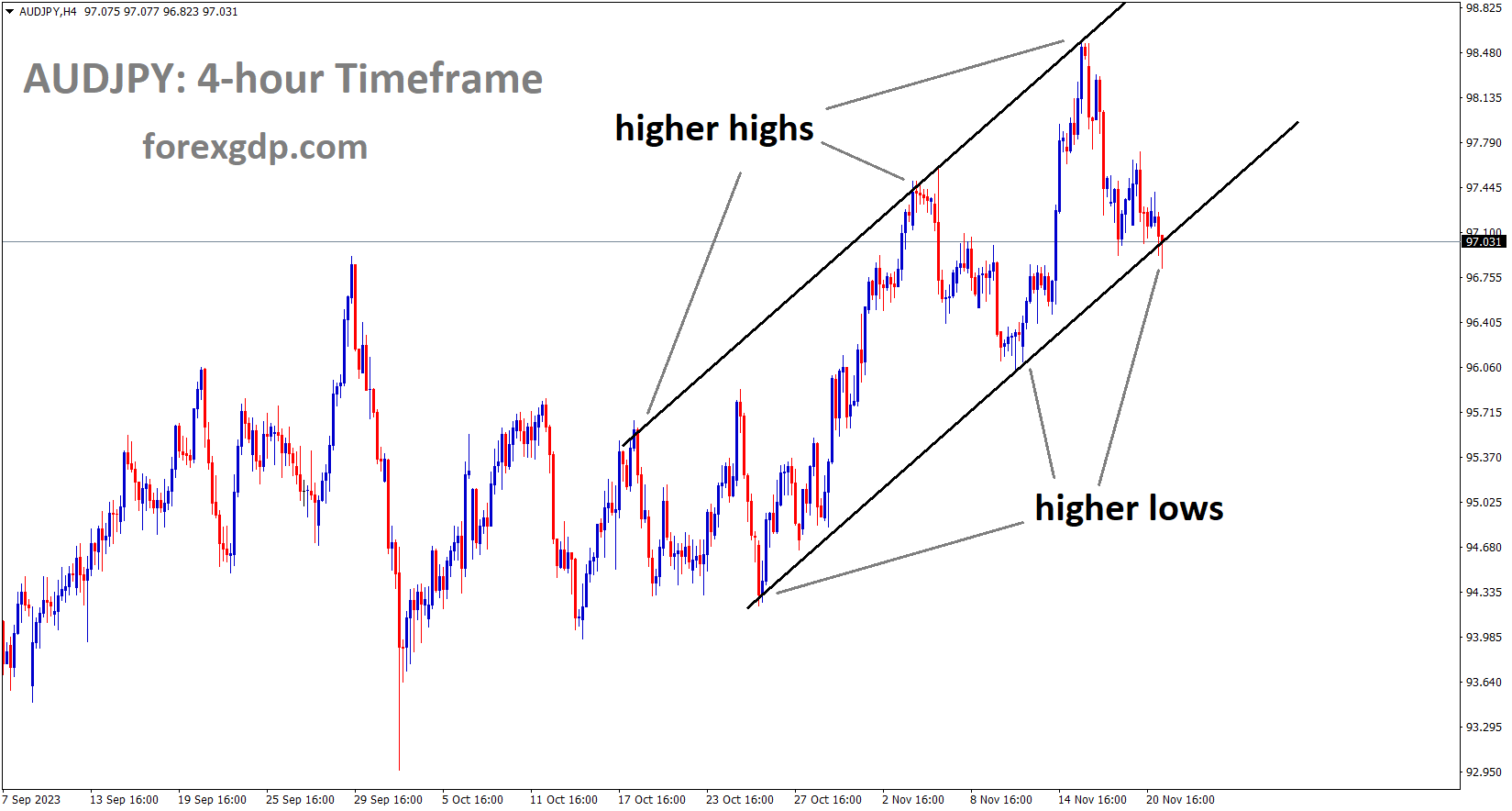

AUDJPY Analysis:

AUDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

The Japanese Yen has gained strength against the USD and other currencies in the past day. There is a possibility that the Bank of Japan might intervene at a higher level, and there are indications that the Bank of Japan is considering raising rates in early 2024.

The Japanese Yen benefits from the diminishing US-Japan rate differential and speculations that the Bank of Japan is likely to end its negative interest rate policy by early next year. While this adds to the negative sentiment around the USDJPY pair, the risk-on mood in the market could mitigate the safe-haven appeal of the JPY, providing some support. Traders may adopt a cautious approach, awaiting the release of the FOMC minutes later in the US session.

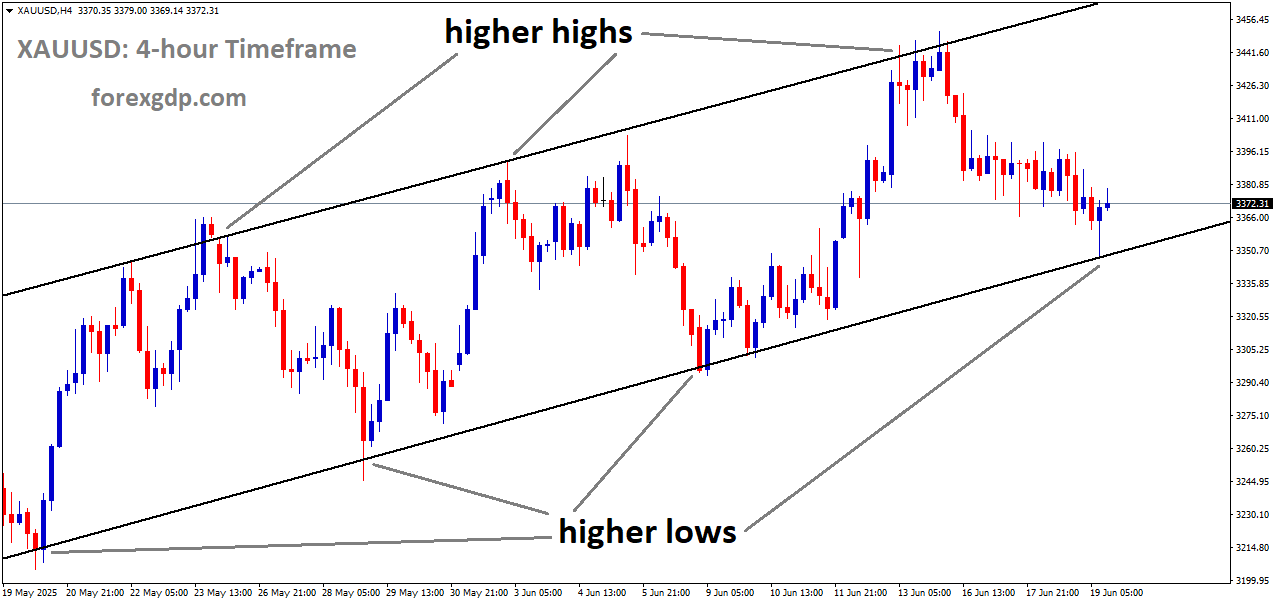

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

In anticipation of this week’s FOMC meeting minutes, the expectation is for the Federal Reserve to maintain unchanged interest rates from the December meeting. As a result, gold prices are on the rise against the US dollar. The price of gold surged, reaching a two-week high above $1,994 during the European session. The US Dollar continued its significant decline, hitting a nearly three-month low, prompted by speculation that the Federal Reserve might initiate rate cuts as early as March 2024. This dovish outlook, reinforced by declining US Treasury bond yields, became a crucial factor driving investors towards the non-yielding gold. Despite the positive sentiment in equity markets due to China’s commitment to additional stimulus measures, the traditional safe-haven status of gold was not compromised, indicating a strong intraday bullish movement. The prevailing trend suggests that the XAUUSD is inclined towards further gains. However, traders may exercise caution, refraining from aggressive bets ahead of the Federal Open Market Committee meeting minutes, given the uncertainty surrounding the timing of the Fed’s monetary policy easing.

The ongoing sell-off of the US Dollar, fueled by expectations of a dovish Federal Reserve, supported a robust upward movement in gold prices on Tuesday. Investors now appear convinced that the Fed has concluded its interest rate-hiking cycle and are eager for signals regarding when the central bank might initiate monetary policy easing.

The 2-year US government bond yield, a gauge of interest rate expectations, remains below the current 5.25-to-5.50% Fed funds target, signaling a growing momentum favoring rate cuts. The CME’s Fedwatch tool indicates approximately a 30% probability that the Fed will begin cutting rates as early as March 2024, with expectations of nearly 100 basis points of cumulative easing by year-end. The benchmark US 10-year Treasury yield reaches a fresh two-month low, putting pressure on the USD, countering the positive market sentiment, and benefiting gold as a non-yielding asset.

Investor optimism increased after Chinese officials pledged more policy support for the troubled real estate sector, aiming to stimulate stronger economic growth. China’s new finance minister, Lan Fo’an, announced plans to boost budget spending to support the post-pandemic recovery in the world’s second-largest economy. While Fed officials have not ruled out the possibility of further interest rate hikes, Richmond Fed President Thomas Barkin indicated on Monday that inflation might persist, necessitating the central bank to maintain higher rates for a longer duration than current investor expectations. This potential headwind for gold underscores the importance of the upcoming FOMC minutes for fresh insights into the Fed’s future policy actions and meaningful market direction.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel

In accordance with HSBC’s perspective, the anticipated decline of the USD Dollar in 2024, as predicted by FED rate cuts, may not materialize. The belief is that rate cuts will contribute to the US economy’s recovery, offering support to the USD rather than causing a significant and sharp decline in 2024.

HSBC economists anticipate that the USD will not undergo significant changes due to anticipated Fed rate cuts in 2024. Their outlook for modest USD strength in 2024 is not contingent on an expected crisis, either within the US economy or globally. Therefore, the potential impact of Fed easing on the USD is viewed as uncertain, rather than generating a ‘safe-haven’ USD bullish sentiment. If rate cuts align with a deceleration in US inflation, it is likely that US real interest rates will persist in positive territory, providing support for the USD. Shallow cuts could eventually result in the US economy regaining momentum, contributing to the ongoing support for the USD.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel

SNB Chairman Thomas Jordan indicated that the possibility of rate hikes in the upcoming meeting cannot be dismissed, citing dissatisfaction with the inflation reading, which is not within the desired range. Q3 industrial production recorded a growth of 2.0%, a notable improvement from the -0.70% in the previous quarter. The Swiss Franc is currently in a consolidation phase against its counterpart currencies.

The USDCHF pair encounters challenges, likely influenced by an enhanced risk appetite and signs of a cooling labor market, as investors anticipate a dovish stance from the Federal Reserve. The softer Consumer Price Index in the United States for October has prompted a reevaluation of the likelihood of a rate hike by the Fed at the December meeting, leading investors to consider the prospect of potential rate cuts in 2024. According to the latest report from the US Bureau of Labor Statistics, the US CPI decelerated to 3.2% (YoY), falling below the consensus of 3.3% and down from the previous reading of 3.7%. The Core CPI eased to 4.0% (YoY), slightly below the expected unchanged figure and the previous reading of 4.1%.

EURCHF Analysis:

EURCHF has broken the Descending channel in upside

The hawkish comments from Swiss National Bank Chairman Thomas Jordan, where he does not dismiss the possibility of more interest rate hikes in the future, continue to provide support and bolster the strength of the Swiss Franc. Additionally, Swiss Industrial Production (YoY) for the third quarter surpassed expectations, registering at 2.0%, a notable improvement from the revised -0.7% (initially -0.8%) reported in the previous quarter by Swiss Statistics.

This positive trend, seen as inflationary, may have contributed to weakening the USDCHF pair. On Tuesday, the release of Swiss Import and Export data will add to market developments. Traders will then shift their attention to crucial US economic indicators, including Existing Home Sales and the Chicago Fed National Activity Index. Furthermore, insights into the Federal Reserve committee’s decision-making process regarding interest rates may be gleaned from the upcoming release of the FOMC meeting minutes.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

Francois Villeroy De Galhau, a member of the ECB Governing Council, stated that interest rates have reached their peak and suggested that even in the event of a war conflict affecting EU imports of energy, inflation may not escalate further.

Francois Villeroy de Galhau, a member of the European Central Bank Governing Council and the President of the Bank of France, asserted on Tuesday that interest rates have reached a plateau and are expected to remain at this level for the next few quarters. He dismissed any discussion of a rate cut as premature, emphasizing that our reliance on forward guidance has been excessive and that a more modest approach should be taken with future guidance. Villeroy de Galhau anticipates increased bond volatility, stating that renewed increases in volatility would be an additional reason not to raise rates. He also emphasized the need to discontinue Pandemic Emergency Purchase Program reinvestments in due time, possibly earlier than the originally planned end date of 2024.

Regarding the inflation target, Villeroy de Galhau expressed a lack of fixation on achieving a 2% target to the nearest decimal place. He downplayed the impact of recent developments in Israel and the oil market, suggesting that these factors should not significantly alter the downward trend in inflation. Villeroy de Galhau expressed confidence in the ability to avoid a recession, stating that a soft landing path is more likely. He noted a shift in the central question from “When will we stop hiking?” to “When will we start cutting?” He anticipates that rates will plateau for at least the next several meetings and the next few quarters.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

Governor Bailey of the Bank of England remarked that inflation has moderated, decreasing from 11.1% in October 2022 to 4.6% in October 2023. There is a potential for further cooling to 2% in the coming year. Although food inflation continues to exceed 10%, there is an expectation that it will soon decrease to 3% in the near-term cycle.

During the Henry Plumb Memorial Lecture, Bank of England Governor Andrew Bailey acknowledged that while inflation has significantly exceeded the central bank’s primary targets, there are indications that the surge in prices, particularly in the food sector, is starting to subside. Governor Bailey highlighted that overall inflation surpassed the Bank of England’s 2% target, peaking at 11.1% in October 2022.

Although recent data shows a reduction to 4.6%, there remains a considerable gap to bridge before returning to the 2% target, and Governor Bailey cautions against prematurely declaring victory over inflation.

The inflation rate for food and beverages reached 19.1% in March 2023, contributing a substantial 2 percentage points to the overall inflation figure. Governor Bailey emphasized that as of October, food inflation still exceeds 10%, and the Bank of England anticipates a slowdown in food price growth to 3% by the conclusion of the short-term forecast cycle in March 2024.

GBPCAD Analysis:

GBPCAD is moving in an Ascending channel and the market has reached the higher high area of the channel

Crude oil prices are undergoing a correction, rebounding from yesterday’s lows, driven by anticipated oil output cuts in the upcoming November 26th OPEC+ meeting. The expected Canadian CPI data adjustment from 3.8% to 3.2% contributes to the weakening of the Canadian Dollar against its counterpart currencies.

The Canadian Dollar is finding upward support against the US Dollar, courtesy of higher Crude Oil prices. Western Texas Intermediate is trading near $77.50 per barrel as of the current press time. Market speculation suggests that the Organization of the Petroleum Exporting Countries (OPEC) may opt for further production cuts during its upcoming meeting on November 26. Adding to the market dynamics, Canada’s Consumer Price Index data is scheduled for release on Tuesday. The year-on-year inflation rate in October is expected to decrease to 3.2% from the previous reading of 3.8%. A decline in inflation might provide the Bank of Canada with flexibility to maintain its target for the overnight rate at 5.0% during the December meeting, particularly as the central bank has indicated that economic indicators will influence rate decisions.

The US Dollar is facing challenges amid an enhanced risk appetite, fueled by expectations of a dovish stance from the Federal Reserve. The release of softer inflation figures last week, with the Consumer Price Index slowing to 3.2% (YoY) and the core CPI dropping to 4.0% (YoY), has prompted investors to reconsider the probability of a rate hike at the December meeting and consider potential rate cuts in 2024. Traders are closely monitoring key US economic indicators, including Existing Home Sales and the Chicago Fed National Activity Index on Tuesday. Additionally, market participants eagerly await insights from the Federal Reserve’s minutes from its recent meeting.

AUDCHF Analysis:

AUDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

The Australian Dollar experienced an upward shift following the release of the RBA Meeting minutes speech by Michelle Bullock, reflecting a hawkish stance on potential rate hikes. Anticipated higher inflation in the coming days suggests that interest rates will be maintained at elevated levels for an extended period into 2024.

The Australian Dollar has continued its upward trend for the third consecutive session on Tuesday, propelled by the hawkish remarks from Reserve Bank of Australia Governor Michele Bullock. This surge is further supported by the hawkish undertone in the RBA’s November meeting minutes, escalating commodity prices, and a positive outlook from investors regarding potential additional stimulus measures in China. Governor Bullock highlights the robustness of Australia’s labor market, expressing confidence in the sustainability of employment progress. Additionally, she emphasizes that the inflation challenge is influenced not only by supply issues but also by underlying demand, posing a significant concern for the next one or two years.

The RBA’s November meeting minutes reveal the board’s acknowledgment of a credible case against an immediate rate hike but a stronger consideration for tightening due to heightened inflation risks. The decision on further tightening is contingent on data and risk assessment, with an emphasis on preventing even a modest rise in inflation expectations. Staff forecasts assume one or two more rate increases, and the rise in house prices suggests that policy might not be overly restrictive.

According to Bloomberg sources, Chinese authorities are anticipated to support the real estate sector by compiling a list of 50 eligible developers, both private and state-owned. This list is expected to guide financial institutions in providing support through avenues such as bank loans, debt, and equity financing. The US Dollar Index continues its decline, approaching three-month lows, driven by improved risk appetite and lower US Treasury yields. Despite the growth in the US economy, the Greenback faces short-term vulnerability. Focus is on US data, including Existing Home Sales, the Chicago Fed National Activity Index, and the release of the Federal Reserve’s meeting minutes.

Australia’s October seasonally adjusted Employment Change exceeded market expectations at 55K, compared to the anticipated 20K and the previous month’s 6.7K. The Aussie Unemployment Rate for October met expectations at 3.7%, in line with the previous figure of 3.6%. Australia’s Wage Price Index grew as expected at 1.3%, surpassing the previous reading of 0.8%. The year-over-year data showed a 4.0% increase, exceeding the anticipated 3.9%.

RBA Assistant Governor Marion Kohler anticipates a decrease in inflation but does not expect it to reach the RBA’s 2-3% target until the end of 2025. The People’s Bank of China (PBoC) maintains its loan prime rate at 3.45%, as predicted. Boston Federal Reserve President Susan Collins expresses optimism about the Fed’s ability to lower inflation without significant damage to the labor market by adopting a “patient” approach to further interest rate moves. October’s US Consumer Price Index indicates lower readings than expected, with the annual rate slowing from 3.7% to 3.2%, falling below the consensus forecast of 3.3%. The monthly CPI reduces to 0.0% from 0.4%, and the US Core CPI rises by 0.2%, below the expected 0.3%, with the annual rate decreasing to 4.0% from the prior 4.1%.

NZDUSD Analysis:

NZDUSD has broken the Box pattern in upside

China infused 80 billion Yuan into its economy, earmarked for supporting infrastructure and real estate development. Consequently, the New Zealand Dollar is experiencing an upward movement against its counterpart currencies today.

The New Zealand Dollar’s trade balance for October was -$14.81 billion, an improvement from the previous month’s -$15.41 billion. Exports saw a positive shift, reaching $5.40 billion compared to the previous month’s $4.77 billion, while imports declined to $7.11 billion from $7.20 billion in the preceding month.

The selling pressure on the US Dollar persists as the consensus grows that the Federal Reserve has concluded its policy-tightening efforts. Additionally, the markets are now factoring in the likelihood that the Fed might initiate rate cuts soon, potentially as early as March 2024. This results in a further drop in US Treasury bond yields, dragging the USD to a nearly three-month low. This decline is a pivotal factor in propelling the NZDUSD pair higher. In addition to these factors, optimism surrounding additional stimulus measures from China weakens the safe-haven appeal of the US dollar, benefiting antipodean currencies, including the New Zealand Dollar (NZD). Chinese officials have committed to providing more policy support to the beleaguered real estate sector, and the People’s Bank of China has maintained its benchmark Loan Prime Rate (LPR) near record lows while injecting approximately 80 billion Yuan of liquidity into the economy on Monday.

Despite these supportive factors, the NZDUSD pair faces challenges in capitalizing on the positive momentum. Traders appear hesitant to take aggressive positions and prefer to wait on the sidelines, especially in anticipation of the upcoming release of the FOMC meeting minutes during the US session. The uncertainty revolves around the timing of the Fed’s potential rate cuts. Investors are keen to gain fresh insights into policymakers’ views on whether the US central bank should consider raising interest rates again. The outlook will play a crucial role in shaping near-term USD price dynamics and offer significant momentum to the NZDUSD pair. As the market awaits this event risk, attention will also be on the US economic docket, featuring the release of Existing Home Sales data, providing short-term trading opportunities.

According to the latest data from Statistics New Zealand released on Tuesday, New Zealand’s Trade Balance for October was reported at -$14.81 billion year-on-year, an improvement from the previous figure of -$15.41 billion. Detailed breakdown reveals that exports increased to $5.40 billion during the same month, up from $4.77 billion in the previous period, while imports declined to $7.11 billion, compared to the earlier reading of $7.20 billion.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/