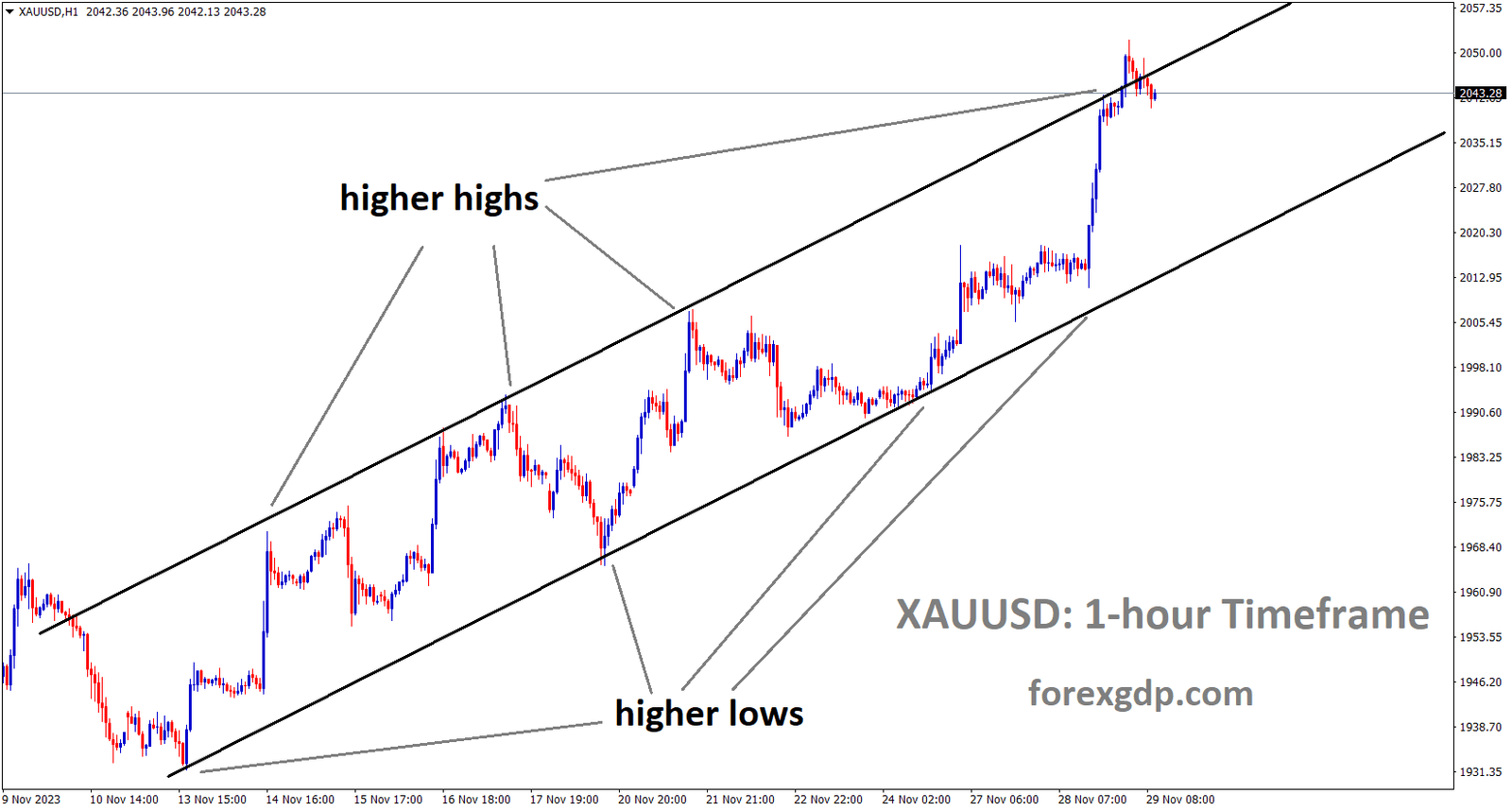

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher high area of the channel

Yesterday, Federal Reserve President Christopher Waller remarked that current interest rates are deemed excessively high, indicating the potential for a rate cut in March 2024. This announcement prompted a surge in the price of Gold against the USD.

The price of gold reached nearly a seven-month high around the $2,052 area on Wednesday but retraced some of its intraday gains as the European session approached. A modest rebound in the US Dollar from its lowest level since August 11, coupled with an overall positive risk sentiment, limited the gains for the precious metal. Despite this, gold maintained positive momentum for the fifth consecutive day, also marking the sixth day in the last seven, and appears poised for further appreciation amid expectations that the Federal Reserve will refrain from raising interest rates.

Furthermore, comments by Fed Governor Christopher Waller on Tuesday, signaling a less hawkish stance, reinforced market expectations that the US central bank might start easing its monetary policy as early as March 2024. In addition, a lackluster US bond auction on Tuesday pushed the yield on the benchmark 10-year US government bond further below. This is expected to restrain a significant USD recovery and continue to act as a tailwind for gold, which does not yield interest. Traders may exercise caution in making aggressive bets ahead of key macro data from the US.

The preliminary or second estimate of the US GDP report is scheduled for release in the early North American session, with expectations of the world’s largest economy expanding at a 5% annualized pace in the third quarter, up from the previously reported 4.9% growth. Additionally, Fedspeak is anticipated to influence USD demand, presenting short-term trading opportunities around the gold price. However, the primary focus remains on crucial US inflation data expected on Thursday, which could impact the Fed’s near-term policy outlook and provide new momentum for the precious metal.

Despite the US Dollar rebounding from a three-and-a-half-month low, the expectation of Fed rate cuts in 2024 continues to support gold. Governor Waller’s remarks about potential rate cuts contrast with the views of Governor Michelle Bowman, who reiterated the likelihood of further rate hikes due to persistent inflation. While the market anticipates the Fed to maintain its key lending rate in December, officials emphasize vigilance on inflation.

The extension of the Israel-Hamas ceasefire deal by two days, beyond its initial expiration on Tuesday morning, could diminish gold’s safe-haven appeal. As part of the original agreement, Hamas released about 50 hostages, with another 20 expected to be freed over the next two days in exchange for the release of Palestinian prisoners by Israel. Traders are now turning their attention to the preliminary US GDP report and, subsequently, the US Core PCE Price Index on Thursday, the Fed’s preferred measure of longer-term inflation trends.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower high area of the channel

In November, the US Consumer Confidence Index from the Conference Board rose to 102.0, up from October’s 99.1. Following the release of this data, the US Dollar experienced a decline. Additionally, US inflation expectations have decreased to 5.7%, down from the previous figure of 5.9%.

US consumer sentiment rebounded in November, as indicated by the Conference Board’s Consumer Confidence Index, which climbed to 102.0 from the revised October figure of 99.1 initially reported as 102.6. Additional insights from the report showed a slight dip in the Present Situation Index to 138.2 from 138.6, while the Consumer Expectations Index saw an increase to 77.8 from 72.7. Notably, the one-year consumer inflation rate expectation eased to 5.7% from the previous 5.9%.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower low area of the channel

Over the past week, the Swiss franc has gained value against the USD, propelled by the Federal Reserve’s dovish stance on interest rates and the Swiss National Bank’s hawkish stance. This week, Swiss data, specifically the scheduled release of Q3 GDP figures, is noteworthy.

The USDCHF pair is grappling with ongoing losses attributed to the weakening US Dollar, fueled by the growing likelihood of the US Federal Reserve concluding its monetary rate hike cycle. Furthermore, investors are factoring in the anticipation of nearly 85 basis points in interest rate cuts by the Fed in the coming year.

The US Dollar Index is hovering around 103, exhibiting a negative bias as a risk-on sentiment prevails. This sentiment is reinforced by the latest report from the US Census Bureau, revealing a significant 5.6% decline in New Home Sales for October, totaling 679,000, falling short of the market expectation of 725,000. The current trend continues to tilt towards the downside, influenced by a decrease in US Treasury yields. In the upcoming sessions, the United States is set to release the Housing Price Index and CB Consumer Confidence, alongside insights from Federal Reserve officials, providing a comprehensive overview of the economic landscape.

The Swiss ZEW Survey Expectations scheduled for Wednesday holds particular significance as it initiates a week of notable data releases. The last reported reading in October stood at -37.8, indicating prevailing pessimism among businesses concerning the Swiss economy. Additionally, the release of Swiss Real Retail Sales for October on Thursday is anticipated to show an improvement of 0.2% from the previous 0.6% decline. Finally, on Friday, attention will be on the Gross Domestic Product for the third quarter.

EURCHF Analysis:

EURCHF is moving in the Box pattern and the market has reached the support area of the pattern

ECB President Lagarde stated that discussions and deliberations among Governing Council members are ongoing regarding the PEPP program. Analysts predict that the ECB is unlikely to swiftly conclude the PEPP program in the near future.

ECB President Lagarde addressed the European Financial Reporting Advisory Group Conference in Brussels via a pre-recorded video, touching on the topic of quantitative tightening . Lagarde mentioned that it would be a subject for discussion and consideration within the governing council in the near future. Despite Lagarde’s remarks, financial markets paid more attention to comments from Federal Reserve officials leaning towards the dovish end of the spectrum. Market participants appear skeptical that concluding the pandemic emergency purchase program will be a straightforward or rapid undertaking.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

The EURUSD pair is reaping the benefits of a softer US Dollar, influenced by a less hawkish stance from the US Federal Reserve. Investors are poised to closely monitor economic data related to the European Central Bank on Wednesday. Both Spain and Germany are expected to unveil preliminary Consumer Price Index data for November, with projections pointing toward a deceleration in the annual inflation rate in both countries. Additionally, the European Commission is scheduled to release its Economic Sentiment Indicator, offering insights into the overall trend of the Euro Zone economy. Despite better-than-expected economic data from the United States, the US Dollar Index continues to falter around 102.60.

The US Housing Price Index for September, holding steady at 0.6% and surpassing the expected figure of 0.4%, indicates a resilient and positive trajectory in housing prices, signaling growth in the housing market. In November, the US CB Consumer Confidence Index increased to 102.0, up from the revised October reading of 99.1.

Moreover, the Greenback’s weakening is attributed to the decline in US Treasury yields, serving as an additional negative factor. Additionally, the accommodating statements from Fed Governor Christopher Waller may have contributed to the Dollar’s depreciation. Waller suggested that the Federal Reserve might not insist on maintaining high-interest rates in the face of consistently declining inflation. Investor attention will shift to the preliminary Gross Domestic Product Annualized for the third quarter in the US. Later in the day, the Federal Reserve is set to release the Beige Book, providing a comprehensive overview of overall economic growth in the United States.

EURJPY Analysis:

EURJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

According to Seiji Adachi, a member of the Bank of Japan Board, the cessation of negative rates depends on the progression of the wage inflation cycle, which needs to gradually increase. However, as this condition is not currently evident in the economy, the possibility of ending negative rates is not being considered for inclusion in the rate hike agenda.

Bank of Japan board member Seiji Adachi returned to the headlines during early European trading on Wednesday, emphasizing the challenge of discontinuing negative interest rates until a positive wage-inflation cycle initiates. He highlighted that such a cycle has not materialized thus far. However, he suggested that if the likelihood of its occurrence rises, discussions about an exit strategy can commence. Adachi emphasized that waiting for the cycle to turn positive is not a prerequisite for deliberating the exit from negative rates.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

The Bank of England’s announcement of tightening measures has bolstered the strength of GBP against its counterparts in the market. Additionally, positive domestic data in the UK further contributes to the support for GBP.

The winning streak for GBPUSD, with the Pound Sterling displaying strength against the US Dollar for the fourth consecutive day. This resilience underscores the robust performance of the UK economy, even in the face of the tightening measures implemented by the Bank of England.

CADCHF Analysis:

CADCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Following market rumors, oil prices have risen due to indications that OPEC+ reached an agreement on supply cuts during a pre-scheduled meeting before November 30. While African countries did not provide support for the OPEC+ supply cuts, there is optimism that a consensus may be reached in tomorrow’s meeting.

Oil prices have rebounded, surpassing $75 and moving away from the monthly lows near $72. This increase is occurring as OPEC prepares for a preliminary meeting to reach an agreement on overall production cuts before the official OPEC+ meeting. This upward trend contrasts with the bearish sentiment confirmed by recent data from the Commodity Futures Trading Commission, revealing that Money Managers reduced their net-long positions in WTI last week. While markets are becoming less optimistic about oil, uncertainty lingers over the potential depth and duration of OPEC+ production cuts.

The US Dollar is recovering from its monthly lows as US traders return to their regular schedules, attempting to offset Monday’s losses. The Greenback is modestly higher in a mixed Tuesday market. With five Federal Reserve speakers scheduled, traders are eagerly awaiting guidance on the Fed’s next steps in December.

OPEC is scheduled to hold a virtual meeting on Thursday before the OPEC+ meeting later that day to discuss specific production cuts. However, African countries within OPEC+ are still in disagreement over oil output quotas ahead of Thursday. The latest data from the Commodity Futures Trading Commission indicates that Money Managers have reduced parts of their net-long positions in WTI, with Brent futures displaying their most significant discount since August. Russia’s seaborne crude exports are rebounding, reaching 3.24 million barrels per day, up 370,000 from November 19th.

Tensions are building among traders due to the lack of individual comments from OPEC+ members ahead of Thursday, making prepositioning uncertain. In a statement, OPEC defended the Oil-and-Gas industry ahead of the COP28 climate convention, pushing back against the International Energy Agency and highlighting the ongoing debate on the best approach to tackle global warming. Saudi Arabia continues to urge all OPEC members to reduce their production quotas as part of a collective effort to stabilize the supply side.

As is customary, the American Petroleum Institute is set to release its latest stockpile figures on Tuesday evening around 21:30 GMT. Previous data showed a build of 9.047 million barrels, and projections now suggest a 2 million barrel drawdown, potentially marking the end of the supply buildup throughout November.

AUDUSD Analysis:

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The October Australian Consumer Price Index data recorded a rate of 4.9%, down from the previous reading of 5.6%, with an anticipated figure of 5.2%. This result led to a relatively subdued movement in the Australian Dollar within the market.

The Australian Dollar halted a four-day winning streak after paring intraday gains in the early European session on Wednesday. Nonetheless, the AUDUSD pair had initially surged due to increased risk appetite in the market and a rise in commodity prices. The softer US Dollar (USD), influenced by a less hawkish stance from the US Federal Reserve, provided additional support to the AUDUSD pair. Australia’s Monthly Consumer Price Index for October came in at 4.9%, a slight decrease from the previous reading of 5.6% in September and slightly below the expected 5.2%. Although this less optimistic data initially applied some downward pressure, the Australian Dollar appeared to recover from this setback.

The US Dollar Index dipped to its lowest level since August 11, despite better-than-expected Housing Price Index and Consumer Confidence data from the United States. The decline in US Treasury yields served as an additional negative factor for the Greenback. Fed Governor Christopher Waller’s comments, suggesting that there is no need to insist on maintaining high interest rates if inflation consistently declines, added to the downward pressure on the Greenback. Investors are anticipated to shift their attention to the preliminary Gross Domestic Product Annualized data for the third quarter in the US, providing insights into the pace and trajectory of economic growth during that period. Later in the day, the Federal Reserve will release the Beige Book, offering a comprehensive picture of overall economic growth in the United States.

Australia’s seasonally adjusted Retail Sales data for October showed a monthly decline of 0.2%, contrasting with market expectations of a 0.1% rise and the previous month’s 0.9% increase. Reserve Bank of Australia Governor Michele Bullock noted that the current monetary policy is on the restrictive side, with rate hikes dampening demand, especially in the context of persistent services inflation. Governor Bullock emphasized the need for caution in deploying high interest rates to combat inflation without inadvertently increasing the unemployment rate. The People’s Bank of China issued a notice to enhance financial support for private firms, covering areas such as listing and financing, mergers and acquisitions, and restructuring. The Federal Open Market Committee meeting minutes revealed a unanimous decision to keep policy restrictive until there is clear and sustainable evidence of inflation moving down toward the Committee’s target. The US Housing Price Index remained consistent at 0.6% in September, in line with the expected figure of 0.4%. The CB Consumer Confidence Index saw an increase in November, reaching 102.0, following a downward revision of October figures from 102.6 to 99.1.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

The Reserve Bank of New Zealand announced its interest rate decision today, maintaining rates at 5.50%. RBNZ Governor Adrian Orr mentioned that if inflation exceeds the tightening measures implemented, the current domestic data reflects notable improvement following the measures taken in the previous meeting.

During its November monetary policy meeting, the Reserve Bank of New Zealand board members opted to maintain the interest rate at 5.50%, aligning with market expectations. Following the release of the RBNZ interest rate statement, the NZDUSD pair saw an almost 1.0% increase. The statement acknowledged the potential for an increase in the Official Cash Rate if inflationary pressures exceed expectations. Emphasizing that current interest rates are curbing spending in the economy, the RBNZ highlighted the decline in consumer price inflation, in line with its objectives. To achieve its goals, the RBNZ stressed the importance of keeping the OCR restrictive to temper demand growth and bring inflation within the 1 to 3 percent target range.

The minutes from the RBNZ interest rate meeting revealed key points, including the committee’s consensus on the need for prolonged restrictive interest rates. Despite the existing restrictiveness, the committee opted to await additional data before considering adjustments. Acknowledging a easing in labor market pressure while keeping employment above its sustainable level, the committee noted a milder-than-expected decline in aggregate demand growth in certain economic sectors.

The RBNZ committee also pointed out a 25-basis-point increase in the estimate of the long-run nominal neutral OCR to 2.50%. Governor Adrian Orr, in the post-meeting press conference, highlighted a constructive meeting with the new Prime Minister and reiterated the RBNZ’s commitment to maintaining steady rates in the coming year. Although projections indicate a potential upward bias in rates, Orr emphasized the uncertainty of this outlook.

Conversely, US Federal Reserve Governor Christopher Waller’s comments contributed to the negative momentum for the US Dollar. Waller’s suggestion that there’s no need to uphold high interest rates if inflation consistently decreases signalled a more accommodative stance from the Federal Reserve. Despite positive economic indicators such as the better-than-expected Housing Price Index and Consumer Confidence data, the US Dollar Index reached its lowest level since August 11. The decline in US Treasury yields added to the challenges facing the Greenback. The September US Housing Price Index remained stable at 0.6%, surpassing the expected figure of 0.4%. The CB Consumer Confidence Index increased to 102.0 in November, though this followed a downward revision of October figures from 102.6 to 99.1. The upcoming estimate of US GDP growth for the third quarter and the release of the Beige Book by the Federal Reserve will be closely monitored for insights into economic expansion.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/