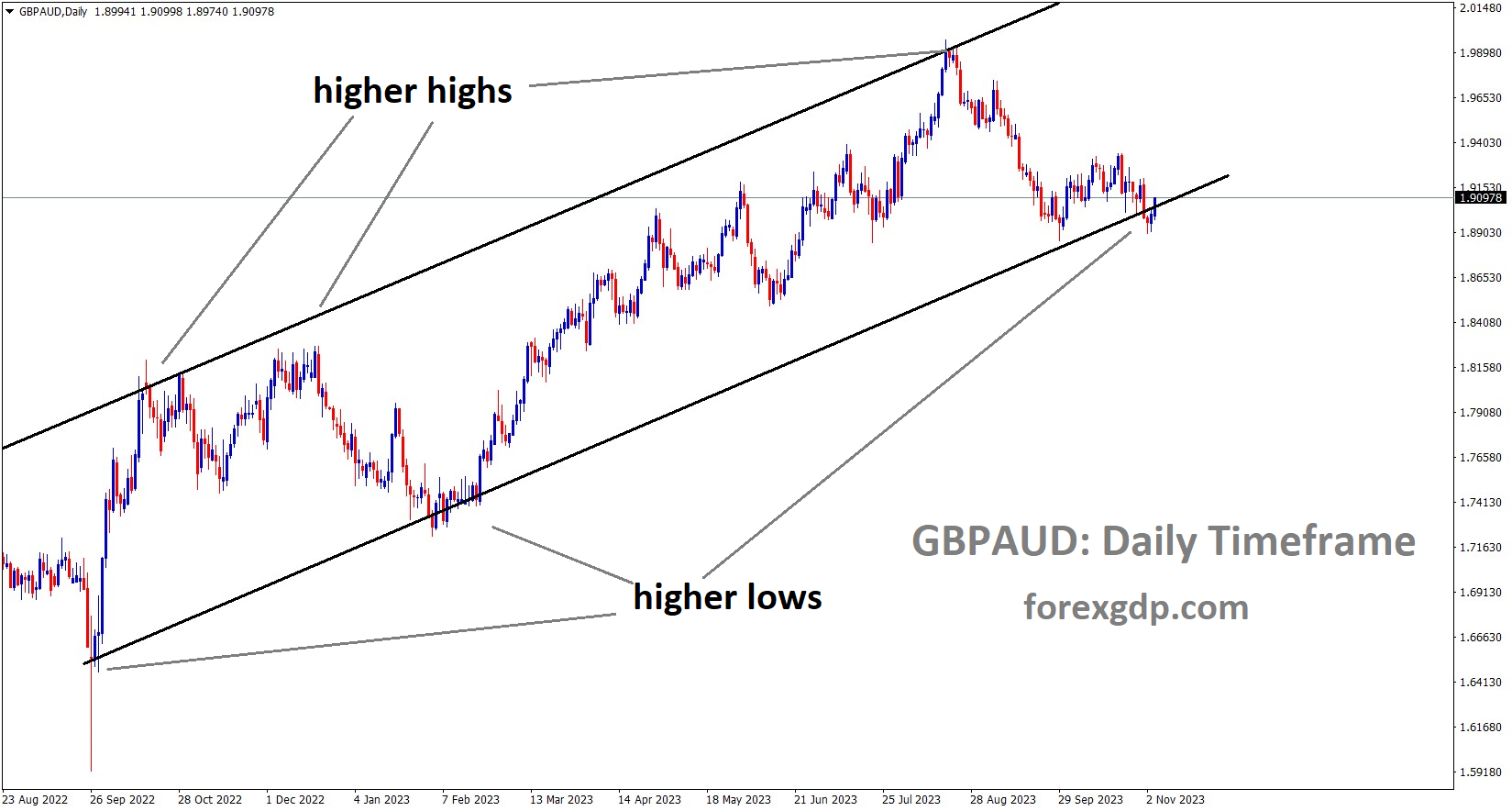

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

In November, inflation in the Euro area was reported at 2.4%, a decline from the previous reading of 2.9%. Similarly, core inflation decreased to 3.6% from the previous month’s 4.2%. Following the release of this data, the euro currency exhibited weakness in the market. In the Euro Area, inflation continues its descent, as the most recent data reveals a downturn from October’s figures.

Core inflation declined by 0.6%, settling at 3.6%, while headline inflation dropped by 0.5%, reaching 2.4%. Headline inflation has now reached its lowest point since July 2021, and the core rate is at its lowest since April 2022. Both figures fell below market expectations. This inflation update reinforces the growing sentiment that the European Central Bank is likely to implement rate cuts sooner than initially anticipated. The latest projections for ECB rates indicate the possibility of a 25 basis point rate cut at the April meeting, with a total of 115 basis points of cuts priced in for the year 2024.

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

Today marks the scheduled speech by FED Chair Powell. The recent Core PCE Index data, released yesterday, came in lower than anticipated. This index is crucial for determining the likelihood of a future rate hike by the Federal Reserve. The market mostly favored gold prices due to the dovish stance implied by the data. U.S. Treasury yields rebounded following remarks by San Francisco Federal Reserve President Mary Daly, who emphasized that declaring victory against inflation and contemplating a reduction in borrowing costs is premature for policymakers. The resulting surge in rates had a broad impact, strengthening the U.S. dollar and exerting downward pressure on technology stocks and non-yielding assets. The Nasdaq 100 experienced its second consecutive day of decline, while gold prices stalled at technical resistance. Anticipating potential volatility in the days ahead, particularly with Fed Chair Powell’s scheduled fireside chat at Spelman College in Atlanta, Georgia, on Friday, traders are advised to closely monitor his statements. Given the recent mixed signals and inconsistent messaging from the central bank, Powell’s comments could significantly influence market dynamics.

Should Powell adopt a hawkish stance, expressing support for higher interest rates over an extended period, U.S. yields may face upward pressure, contributing to the ongoing recovery of the U.S. dollar. This, in turn, could adversely affect both gold prices and the Nasdaq 100. On the other hand, a dovish outcome, marked by a lack of strong resistance against the dovish monetary policy outlook, might lead traders to believe that the Fed is on the verge of a policy shift. Such a perception could weigh on yields and the U.S. dollar, creating a favorable environment for bullion and tech stocks. To prevent a further easing of financial conditions, which could complicate efforts to sustainably restore price stability, Powell may take a firm stance, pledging to maintain the current course and uphold a restrictive monetary policy for an extended duration. Such a position could disrupt the positive momentum observed in the equity market and precious metals complex in recent weeks.

SILVER Analysis:

XAGUSD Silver price is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The October US Core PCE index showed a decrease from 3.7% to 3.5%, signaling a positive improvement in inflation levels. As a result, there is an anticipation of further rate cuts from the FED in March 2024.In October, the month-over-month growth of Core Personal Consumption Expenditures (PCE) prices decelerated, marking a departure from two consecutive months of 0.4% increases. The October figure, aligning with expectations at 0.2%, represented the weakest reading since July 2022. The PCE price index saw an increase of less than 0.1%, while the index, excluding food and energy, rose by 0.2%. The annual growth rate eased to 3% from 3.4%, reaching a level not observed since March 2021, in line with forecasts. Simultaneously, annual core PCE inflation, which excludes food and energy, slowed to 3.5% from 3.7%, marking a new low since mid-2021.

The rise in current-dollar personal income for October primarily stemmed from increases in personal income receipts related to assets and compensation, partially offset by a decrease in personal current transfer receipts.The recent data releases consistently suggest a deceleration in the United States, despite a robust labor market and services inflation. Market participants, encouraged by the latest data, are increasingly speculating on potential rate cuts in 2024. The upcoming Non-Farm Payrolls (NFP) report next week holds significance as it could further reinforce the case for the Federal Reserve’s stance heading into the December meeting. The lingering question is whether a softer NFP print, indicating a cooling labor market, would prompt the Fed to signal that they are concluding their series of rate hikes.

USDCAD Analysis:

USDCAD has broken the Ascending channel in downside

Most countries within OPEC+ were reluctant to endorse supply cuts, resulting in an agreement for approximately 2.20 million barrels per day by the end of yesterday’s meeting. The Canadian Dollar gained favorably from this accord, while the US witnessed a reduction in its daily supply to 20 million barrels.

The Canadian GDP data for Q3 revealed a contraction of -1.1%, contrasting with the expected growth of 0.20%. The monthly reading also showed an increase of 0.10%, surpassing the anticipated 0.0%.

This morning saw a surge in oil prices, nearly reaching the significant $80 per barrel threshold. However, the anticipated OPEC+ meeting, aimed at boosting prices above $80, had an unexpected outcome, leading to a sell-off afterward. Reports suggest that the meeting encountered numerous challenges and conflicting perspectives, keeping the market on edge for a potential announcement on production cuts. Ultimately, it was disclosed that OPEC+ members had agreed to implement voluntary cuts of approximately 2 million barrels per day for the first quarter of the following year. Saudi Arabia chose to extend its voluntary output cuts as the virtual meeting failed to yield a comprehensive solution. Nevertheless, members, including Saudi Arabia, Kuwait, Russia, Algeria, and Kazakhstan, agreed to gradually unwind the cuts after the first quarter of 2024. The announced cuts comprised reductions from Oman (42,000 barrels/day), Iraq (220,000 barrels/day), UAE (163,000 barrels/day), in addition to extended cuts by Saudi Arabia and Russia, resulting in a total reduction of around 2.19 million barrels per day. A surprising development occurred as Brazil received an invitation to join the OPEC+ group, with the Brazilian Energy Minister expressing hope to join by January.

Adding to concerns, Energy Information Administration (EIA) data for September indicated a decline in Crude and Petroleum products supply to 20.09 million barrels per day, the lowest since April. This data raises worries about a potential global economic slowdown in 2024. Attention now turns to upcoming US data, which could impact oil prices. The decline observed today may be attributed, in part, to a strengthening US Dollar and rising US yields, influencing risk appetite. Tomorrow’s agenda includes manufacturing PMI data and speeches by Federal Reserve policymakers. The comments made today have adopted a more hawkish tone than in recent days, possibly contributing to the rise in the US Dollar.

The Canadian Dollar has received a boost from the anticipated rise in Crude Oil prices, driven by additional OPEC production cuts extending into the first quarter of 2024. Currently, the Canadian Dollar stands out as the best-performing major currency, showing gains against all its major counterparts. Canadian Gross Domestic Product data is a mix of positive and near-term indicators, while the support from Crude Oil adds strength to the fossil-fueled Loonie. The Organization of the Petroleum Exporting Countries unanimously agreed to implement further production cuts, with an unclear end date expected sometime next year. The Canadian GDP figures for September exhibited a mixed performance, surpassing expectations with a 0.1% month-on-month increase against the projected flat 0.0%. However, the year-on-year figure experienced a significant contraction. The annualized third-quarter Canadian GDP reported -1.1%, falling well below the market’s median forecast of 0.2% year-on-year growth. Despite this, the previous period’s figure underwent a notable upward revision, adjusted from -0.2% to 1.4%.

In the Crude Oil markets, there is an anticipation of an upward turn following OPEC’s unanimous decision to cut oil output by an additional million barrels per day. However, the potential gains in Crude Oil prices due to these supply cuts may be constrained, considering the ample spare capacity in global energy demand. OPEC has indicated that these additional production caps will extend through the first quarter of 2024. Despite the overall strength of the Canadian Dollar, it has only shown a marginal increase of 0.05% against the US Dollar. Attention now turns to Canadian labor data, particularly the Canadian Unemployment Rate, which is forecasted to see a slight uptick from 5.7% to 5.8% in November.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

In October, Swiss retail sales recorded a decrease of -0.10%, falling short of the expected 0.20% increase. The Swiss Q3 GDP is slated for release today. Following the release of the retail sales data yesterday, the Swiss Franc strengthened against its counterparts.The USDCHF pair faces downward pressure as the US Dollar weakens, driven by the likelihood of the US Federal Reserve ending its interest rate hike. The US Dollar Index encounters challenges as US Bond yields react modestly, offsetting recent gains. The DXY is currently trading lower at 103.30. Mixed US data may have contributed to the Greenback’s recent resilience. Additionally, the US Core Personal Consumption Expenditures Price Index reported a year-on-year easing to 3.5% in October from the previous reading of 3.7%.

The month-on-month Core PCE Price Index saw a decline of 0.2% compared to the previous 0.3%. Furthermore, Initial Jobless Claims for the week ending November 24 totaled 218K, slightly below the expected 220K. Investors are eagerly awaiting the release of the US ISM Manufacturing PMI for November, and they are also keeping a close eye on the speech by US Federal Reserve Chairman Jerome Powell scheduled for Friday. These events are poised to influence market dynamics and impact the trajectory of the US Dollar.

GBPCHF Analysis:

GBPCHF is moving in the Box pattern and the market has rebounded from the support area of the pattern

Swiss Real Retail Sales, reported on Thursday, saw a decline of 0.1% in October, falling short of the expected 0.2% growth. This decrease in Swiss consumer demand may have contributed to the pressure on the Swiss Franc. Furthermore, market attention turns to Gross Domestic Product data scheduled for today. Despite this, Swiss National Bank Chairman Thomas Jordan has previously acknowledged the potential for future interest rate hikes, providing support to bolster the CHF.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

Governor Bailey of the Bank of England affirmed a commitment to implementing the necessary measures to address inflation in the economy. It is anticipated that inflation may reach 2% in the second half of 2024.The British pound has been significantly impacted by the US dollar, as investors adopt a less hawkish stance towards the Federal Reserve’s interest rate trajectory.

This shift in outlook is attributed to recent weaker economic data in the United States, coupled with some dovish commentary from the Fed. Despite an unexpected positive surprise in the second estimate of US GDP during yesterday’s trading session, the market continued to hold a bearish stance on the USD. This persistent sentiment follows the Fed Beige Book’s revelation of slowing economic growth and indications of softened prices, trends expected to extend through the year 2024.

GBPJPY Analysis:

GBPJPY has broken the Descending channel in upside

BoJ Member Seii Adachi stated that rate hikes would not be feasible until wage growth adequately offsets the inflation rate. The Japanese Yen is strengthening in the market, partly attributed to other central banks maintaining their rates at this time. While inflation is decreasing in other countries, Japan is experiencing an increase in inflation. On Thursday, the Japanese Yen experienced a slight decline against the United States Dollar, as the potential for a tighter Japanese monetary policy was undermined by recent statements from a Bank of Japan official. Since mid-November, the foreign exchange market had cautiously favored the outlook for both currencies. The anticipation of lower US interest rates in the first half of the following year had eroded support for the Dollar, not only against the Yen but across the board. Conversely, the belief that rising domestic Japanese inflation might prompt the Bank of Japan to ease its loose monetary policy had strengthened the Yen.

However, Bank of Japan monetary policy board member Seiji Adachi explicitly stated on Wednesday that Japan’s economy had not reached a stage where a departure from current policy settings could be considered. He emphasized the need to patiently continue with monetary easing for the time being. Despite global inflation trends, the lasting impact on Japan’s economy has left markets uncertain about the BoJ’s intentions. Japan has grappled with a lack of locally generated pricing power for years, and Adachi noted that it would likely take more than a few months of stronger inflation data to convince policymakers of a sustainable recovery. While the belief in the foreign exchange market that the BoJ will eventually roll back some accommodation remains strong, Adachi’s recent comments have given traders and investors reason to pause. If there is a perception that they have outpaced the BoJ’s thinking, the Yen may face stronger headwinds. However, the modest weakness observed on Thursday could also be attributed to calendar-based position squaring as the month comes to a close. Caution is advised as the next monetary policy decisions from the Federal Reserve and the Bank of Japan are approaching on the 13th and 19th of December, respectively.

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

In November, the Australian Manufacturing Purchasing Managers’ Index experienced its ninth consecutive monthly decline, dropping to 47.7 from October’s official reading of 48.2. Both orderbook volumes and manufacturing production levels faced a twelfth consecutive month of decline, and a lack of capacity pressure resulted in sector employment decreasing for the first time in three years. According to Warren Hogan, Chief Economic Advisor at Judo Bank, the Australian Manufacturing PMI recorded its lowest reading in the survey’s 8-year history outside of lockdown periods. The PMI fell below 48, indicative of an index level broadly associated with a soft landing for the manufacturing sector and the wider economy.

NZDUSD Analysis:

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

RBNZ Deputy Governor Christian Hawkesby mentioned that inflation has yet to align with the set goal. With increasing inflation expectations, there is a need to exercise control over spending, and borrowers should manage debt levels given the current interest rate environment.

On Friday, Deputy Governor Christian Hawkesby of the Reserve Bank of New Zealand emphasized the challenges posed by high and persistent core inflation, underscoring the limited margin for error. He highlighted the significance of taking seriously the uptick in certain inflation expectation measures. Hawkesby emphasized the necessity for New Zealand to undergo a period of highly restrained spending. He also noted that the vast majority of borrowers are currently capable of servicing their debt at the prevailing interest rate levels.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/