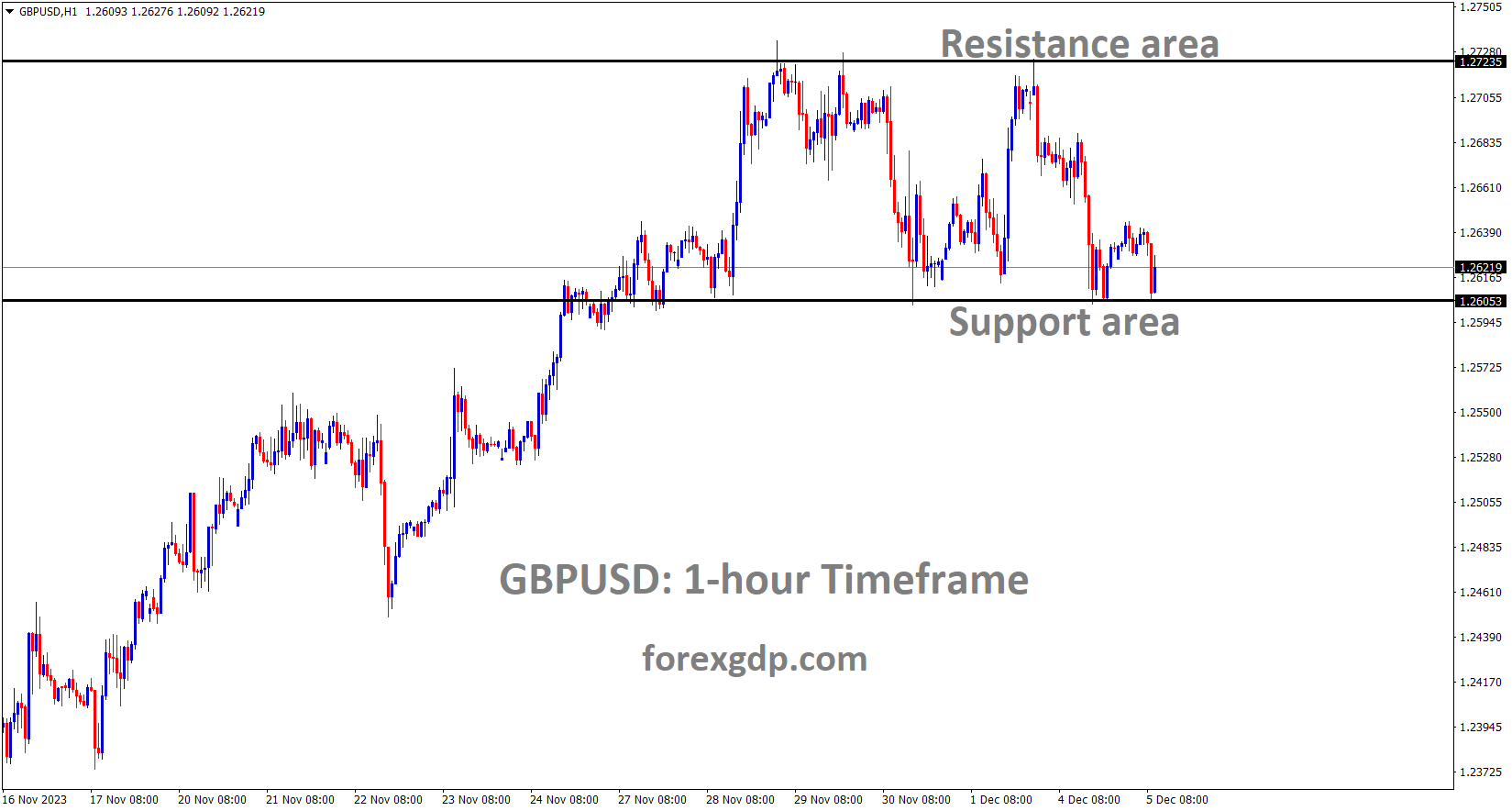

GBPUSD Analysis:

GBPUSD is moving in the Box pattern and the market has reached the support area of the pattern

The GBP retained its strength on indications that the Bank of England is not currently inclined to implement an immediate rate cut in the market. Inflation in the UK is stabilizing, and any further increase in inflation numbers will be taken into consideration for potential rate hikes.

The US Dollar is facing challenges in extending its recent strong performance, reaching a one-week high, as market expectations lean towards the Federal Reserve refraining from further interest rate hikes and potentially initiating policy easing as early as March 2024. This has led to a decline in US Treasury bond yields, placing USD bulls on the defensive and providing support to the GBPUSD pair. Conversely, the British Pound is buoyed by diminishing probabilities of an early rate cut by the Bank of England. BoE Governor Andrew Bailey’s recent caution against prematurely declaring victory over inflation and his projection that monetary policy will need to remain restrictive for an extended period contribute to the GBPUSD pair’s upward movement.

Despite this, a more cautious market sentiment is providing some support to the safe-haven US Dollar, limiting aggressive directional bets by traders. Investors appear hesitant, opting to wait on the sidelines, especially in anticipation of crucial US macroeconomic data scheduled for release later during the early North American session, starting with the ISM Services PMI. The focal point, however, will be the highly anticipated US NFP report scheduled for Friday.

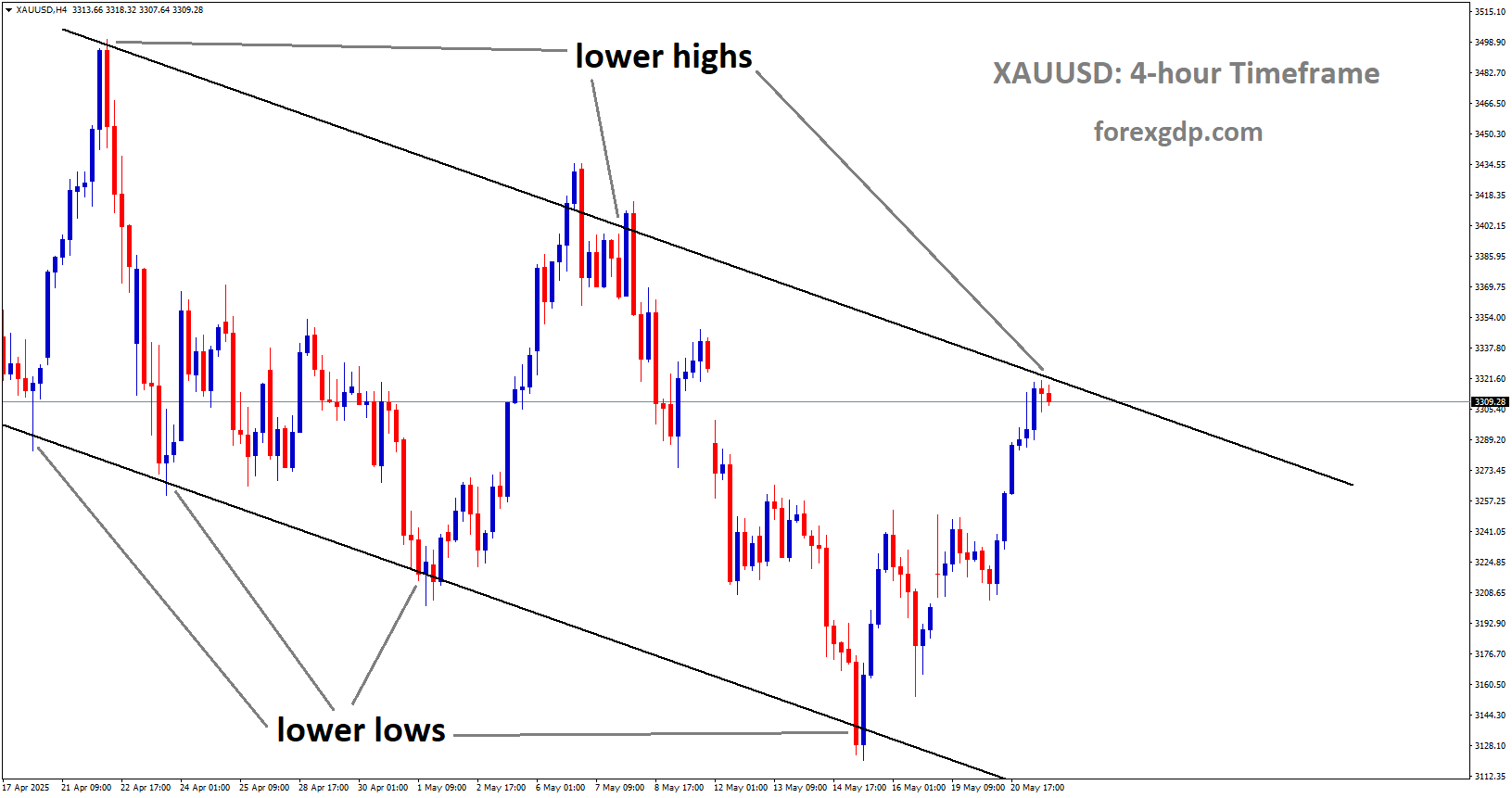

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

Gold prices are experiencing a decline against the USD following a significant upward movement triggered by the Red Sea attack carried out by rebels from Yemen. The ongoing Israel-Gaza war has not concluded, and concerns escalate as the conflict extends to the Red Sea from the city.

Gold prices reached new all-time highs at the market opening due to escalating geopolitical tensions as Israel and Hamas resumed fighting following the ceasefire that concluded last week. The initial surge was supported by the safe haven appeal of the yellow metal; however, it has since retraced below the $2100 mark, despite a stronger US dollar. According to my latest weekly gold forecast, the implied path of Fed funds futures aligns with expectations of approximately 125 basis points in cumulative interest rate cuts by December 2024.

US real yields are trending higher in line with US Treasury yields, technically diminishing gold’s attractiveness due to a rising opportunity cost. Nevertheless, the dominating factor for now is the demand for a safe haven. The trajectory of gold prices is likely to be influenced by updates from Gaza and expectations surrounding the upcoming ISM services PMI and Non-Farm Payrolls (NFP). Analysts foresee the possibility of upside surprises in these economic indicators, and if realized, this could negatively impact gold prices.

SILVER Analysis:

XAGUSD Silver price is moving in an Ascending channel and the market has reached the higher low area of the channel

The US Dollar experienced a slight decline within a narrow range following the increase in US Treasury yields on Monday. The ongoing conflict between Israel and Hamas persists. US dollars are often considered a safe haven during times of war and natural disasters. Today, we await the release of US JOLTS job openings and ISM’s Services PMI data.

The US Dollar demonstrated strength at the beginning of the week, benefiting from safe-haven flows and increasing US Treasury bond yields. After a nearly 0.5% gain on Monday, the USD Index stabilized above 103.50 early Tuesday. Investors are now turning their attention to key economic indicators, including JOLTS Job Openings data for October and the ISM’s Services PMI survey for November.

On Wall Street, major indexes opened significantly lower on the first trading day of the week, reflecting a risk-off sentiment as market participants moved away from risky assets. Concerns over the Israel-Hamas crisis escalating into a broader conflict in the Middle East contributed to the negative market mood.

US stock index futures also showed no signs of improvement, being down between 0.2% and 0.4%. Addressing the situation in Gaza, Martin Griffiths, the top UN emergency relief official, stated on Monday, “Every time we think things cannot get any more apocalyptic in Gaza, they do.” He highlighted the challenges faced by people being ordered to move again with little to survive on, forced to make difficult choices.

Following the December policy meeting, the Reserve Bank of Australia announced that it had left the policy rate unchanged at 4.35%, in line with expectations. The RBA reiterated in its policy statement that the decision on whether further tightening of monetary policy is necessary to bring inflation back to target will depend on evolving data and risk assessments.

USDCAD Analysis:

USDCAD is moving in the Descending channel and the market has reached the lower high area of the channel

The Canadian Dollar exhibits weakness against its counterparts, with the upcoming Bank of Canada monetary policy meeting tomorrow and last week’s OPEC+ supply cuts falling short of expectations.

The upward momentum of the Canadian dollar appears to be waning as we approach a crucial week featuring significant economic data releases for both Canada and the US. The USD has gained strength due to safe-haven demand amid the escalating conflict between Israel and Hamas. Additionally, the recent OPEC+ decision contributed to a negative market reaction, leading to a decline in crude oil prices and further impacting the Canadian dollar.

Looking ahead to the Bank of Canada’s interest rate decision later this week, money markets are indicating an 88% probability of a rate pause. Considering recent Canadian economic indicators, such as subdued growth, slightly higher unemployment, and weaker manufacturing PMI, the domestic outlook for the Canadian dollar is not favorable.

The upcoming week is expected to be predominantly influenced by US factors, with a short-term focus on the ISM service PMI. This is a significant data point for the US, given its predominantly service-driven economy. Close attention will also be paid to JOLTs data in anticipation of Friday’s Non-Farm Payroll report. Improved outcomes in both sets of data could limit support for the Canadian dollar.

USDCHF Analysis:

USDCHF is moving in the Descending channel and the market has reached the lower high area of the channel

The Swiss Consumer Price Index (CPI) for November registered at 1.4%, falling short of the expected 1.6% and decreasing from the October figure of 1.7%.

The US Dollar is advancing across various currencies, driven by widespread risk-off sentiment, while the Swiss Franc faces downward pressure following a disappointing Swiss Consumer Price Index (CPI) inflation reading.

The global market’s risk appetite is further dampened by a more significant-than-expected decline in US Factory Orders for October, registering a decrease of 3.6%, compared to the market’s median forecast of -2.6%. September’s Factory Orders have also been revised downward from 2.8% to 2.3%.

EURCHF Analysis:

EURCHF is moving in the Descending channel and the market has reached the lower high area of the channel

Investors are becoming increasingly apprehensive about the state of the global economy, observing a decline in economic indicators across the board and a shaky growth outlook in major markets. In Switzerland, the November CPI fell short of expectations, with the annualized CPI for November coming in at 1.4%, below the anticipated 1.6% and further dropping from October’s year-on-year figure of 1.7%. The decrease in Swiss CPI seems to be accelerating, particularly in the short term, as November’s month-on-month CPI slips by -0.2%, contrasting with October’s 0.1% reading.

EURUSD Analysis:

EURUSD is moving in the Descending channel and the market has reached the lower low area of the channel

Isabel Schnabel, a member of the ECB Governing Council, expressed doubt regarding additional rate hikes, noting that inflation is indeed calming down as anticipated. Despite this, she highlighted that the trajectory of inflation is expected to stabilize around the target of 2% by 2025.

On Tuesday, Isabel Schnabel, a member of the Executive Board of the European Central Bank, remarked that additional rate hikes are unlikely following the latest inflation data. She expressed encouragement about the inflation developments, highlighting the notable decline in core prices. Schnabel emphasized the need for caution in guiding policy over an extended period and stated that the current level of restriction is deemed sufficient. This, in turn, has bolstered confidence that the 2% target will be achieved by 2025.

The executive board member reiterated the unlikelihood of further rate hikes post the November inflation data but cautioned against prematurely declaring victory. While acknowledging that inflation is moving in the right direction, Schnabel emphasized the necessity for further progress. Despite the positive trajectory, she assured that no prolonged recession is anticipated, and there are indications that the economy may be reaching a bottoming-out phase.

GBPJPY Analysis:

GBPJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

The November Tokyo Consumer Price Index (CPI) for Japan revealed a figure of 2.6%, falling short of the expected 3.3%. This data is considered favorable for the Yen, given the stability in the current rates maintained by the Bank of Japan.

Global risk sentiment took a hit after an attack on US vessels in the Red Sea over the weekend raised concerns about a broader conflict in the Middle East. Additionally, a darkening global outlook and worsening economic conditions in China are dampening investors’ interest in riskier assets. This is evident in the generally weaker tone around equity markets, benefiting traditional safe-haven currencies like the JPY

for Japan revealed a figure of 2.6%, falling short of the expected 3.3%")

Despite speculation about a potential shift in policy stance by the Bank of Japan, its board members downplayed such expectations last week, affirming the continuation of the negative interest rate regime. Furthermore, data released this Tuesday revealed a more significant easing of consumer inflation in Tokyo, Japan’s capital city, for November than initially anticipated. While this may temper bullish sentiments for the JPY

The recently released data for Tokyo CPI showed a deceleration in the headline inflation rate from 3.3% to 2.6% YoY in November. Although this figure remains above the Bank of Japan’s 2% target for the 18th consecutive month, the Core CPI, excluding volatile items, remained flat month-on-month, with the yearly rate easing more than expected. Another core gauge, excluding both fresh food and fuel prices, used as an indicator of underlying inflation by the BoJ, fell from the previous month’s 3.8% YoY rate to 3.6%. Investors, however, are still pricing in the possibility of the BoJ exiting its negative interest rate policy in 2024, providing some support to the Japanese Yen amidst a softer risk tone. The final au Jibun Bank Service PMI for November came in at 50.8, below the flash reading of 51.7, indicating a slower pace of growth in the services sector and a loss of momentum.

AUDUSD Analysis:

AUDUSD has broken the Ascending channel in downside

The RBA decided to maintain the current interest rates at 4.35% today. RBA Governor Bullock noted that inflation in the market is stabilizing, and the labor market is showing signs of cooling. The governor emphasized that any future rate hikes will be contingent on data indicating an increase in inflation coupled with a tightened labor market.

In November, China’s Purchasing Managers’ Index (PMI) rose to 51.5, up from the October reading of 50.4. Business and order conditions in China are rapidly improving, accompanied by a decrease in inflationary pressures within the Chinese economy.

Following its December monetary policy meeting on Tuesday, the board members of the Reserve Bank of Australia opted to keep the Official Cash Rate unchanged at 4.35%, aligning with market expectations. This decision followed a 25-basis-point interest rate hike in November. Governor Michele Bullock presented the monetary policy statement, outlining key points. The need for further tightening of monetary policy to bring inflation back to target within a reasonable timeframe will be contingent on evolving data and risk assessments. The board remains steadfast in its commitment to restoring inflation to the target range.

The limited information received on the domestic economy since the November meeting has generally met expectations. The outlook for household consumption remains uncertain, and the October monthly CPI indicator indicates a continuing moderation in inflation, primarily driven by the goods sector. However, the update did not offer significant insights into services inflation. Measures of inflation expectations align with the inflation target. While conditions in the labor market are gradually easing, they remain tight. There are domestic uncertainties regarding the time lags in the impact of monetary policy. The higher interest rates are actively working to establish a more sustainable balance between aggregate supply and demand in the economy. Maintaining the cash rate at this meeting allows time to evaluate the impact of the recent interest rate increases on demand, inflation, and the labor market.

According to the latest data released by Caixin on Tuesday, China’s Services Purchasing Managers’ Index surged to 51.5 in November, surpassing the October reading of 50.4. This exceeded market expectations, which had anticipated a print of 50.8. The report indicates that business activity and new orders experienced the fastest growth in three months.

Furthermore, there is an improvement in confidence regarding the year ahead, while inflationary pressures have weakened. Dr. Wang Zhe, Senior Economist at Caixin Insight Group, commented on the China General Services PMI data, stating that both services supply and demand expanded, contributing to the ongoing recovery of the market. The gauges for business activity and total new orders have remained above 50 for the 11th consecutive month, reaching three-month highs.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has reached the lower high area of the channel

A multitude of individuals congregated on the streets of New Zealand to voice their opposition to the policies of the current government, particularly those affecting minority communities. The government has implemented measures such as replacing Maori languages with English in various settings and workplaces.

In New Zealand, numerous demonstrators have taken to the streets to voice their opposition to the policies of the newly elected government concerning Indigenous people. Protests unfolded in front of the parliament and on motorways on Tuesday, following a call for nationwide demonstrations by the Te Pati Maori party against the recently elected right-leaning government. These protests coincided with the commencement of New Zealand’s 54th parliament session, marking the end of six years of governance by the centre-left Labour Party after October’s elections. In a departure from tradition, the Te Pati Maori, holding six seats in parliament, took oaths of allegiance to the upcoming generation and the Treaty of Waitangi, a colonial-era pact between the British and the Maori people, before pledging allegiance to King Charles.

The new National Party-led coalition has committed to reviewing affirmative action policies, altering department names from Maori to English, and removing references to the Treaty of Waitangi’s principles from legislation. Te Pati Maori co-leader Rawiri Waititi addressed protesters in Wellington, emphasizing that this was not merely a protest but an activation of their voices. He urged the crowd to make their voices heard and be proud of their identity. New Zealand police reported two arrests in connection with the demonstrations, leading to traffic disruptions in several cities, including Auckland.

National Party leader Christopher Luxon, part of a coalition with the libertarian ACT New Zealand and populist New Zealand First, defended his government against the protesters’ criticism, describing it as pretty unfair. Luxon asserted that his government, in power for just a week, is dedicated to achieving positive outcomes for both Maori and non-Maori. David Seymour, the leader of ACT New Zealand, accused Te Pati Maori of prioritizing divisive theatrics over providing solutions for Indigenous people. Seymour emphasized that New Zealanders elected a government committed to treating all individuals equally, regardless of their race.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/