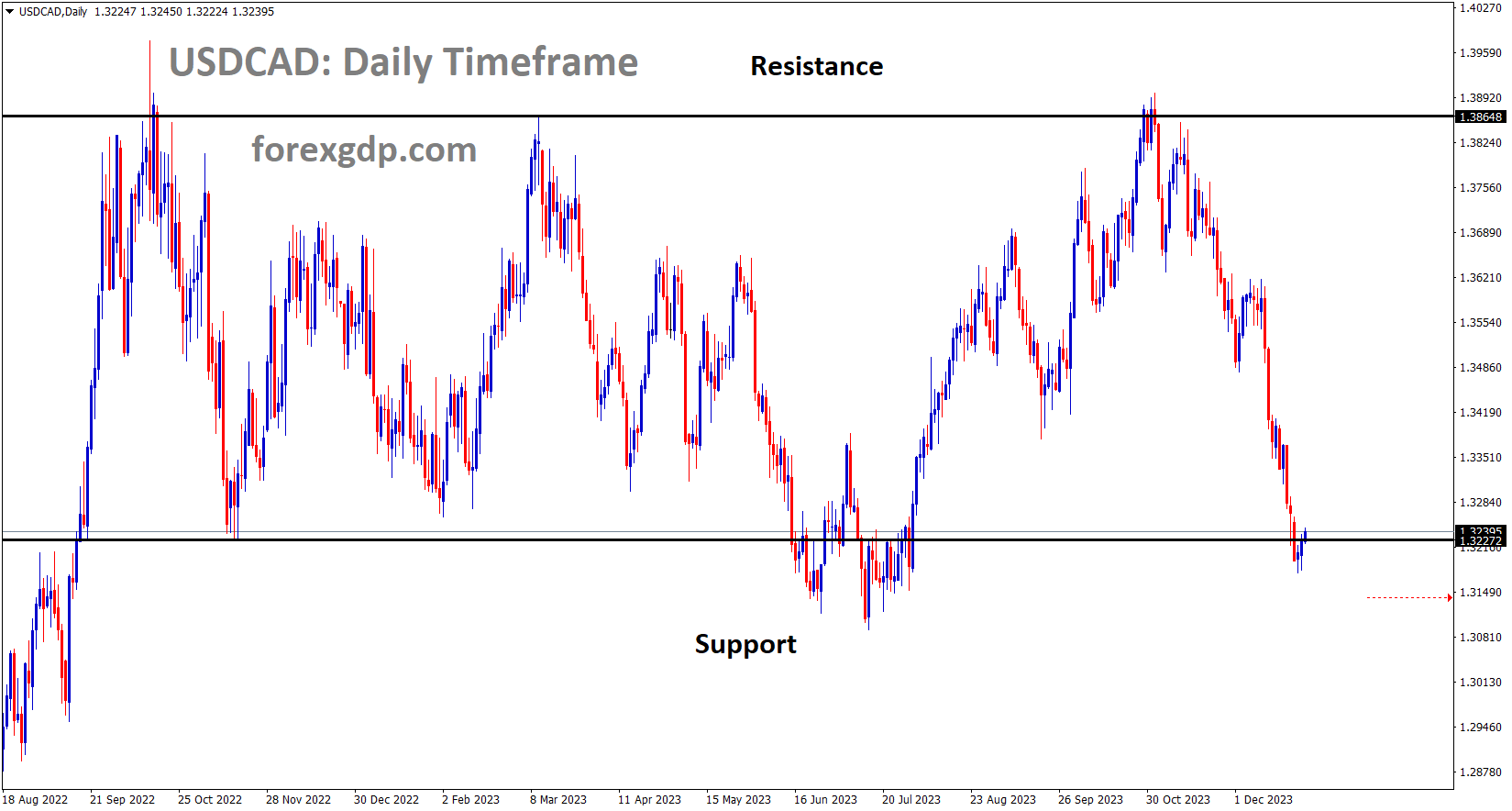

USDCAD Analysis:

USDCAD is moving in the Box pattern and the market has rebounded from the support area of the pattern

The Bank of Canada has indicated that inflation has moderated, making it possible for the next round of rate hikes. This forecast for rate hikes is supported by November’s inflation data, which came in higher than anticipated. Consequently, any plans for rate cuts are expected to be postponed, thanks to robust retail sales data in Canada over the past few months.

On Friday, oil prices continued their descent, driven by concerns of potential supply disruptions. This downward trend has put some selling pressure on the Canadian Dollar, which is closely linked to commodity prices. In its December meeting statement, the Bank of Canada expressed increased optimism regarding the nation’s inflation outlook and hinted at the possibility of further interest rate hikes.

However, the November Consumer Price Index did not show signs of slowing down, raising questions about the likelihood of additional rate hikes. In contrast, investors are anticipating interest rate cuts in the United States in the coming year. During its last meeting of the year, the Federal Reserve opted to keep rates unchanged at 5.25%-5.50%. Fed Chair Jerome Powell mentioned that the timing of rate cuts would be the next question for the Fed. The shift towards a dovish stance by the Fed has led to a broad decline in the US Dollar and a drop in bond yields.

On Thursday, the US Department of Labor reported that the weekly Initial Jobless Claims figure came in at 218K for the week ending December 23, falling short of expectations. This figure was higher than the previous week’s 206K and below the projected 210K. Additionally, Pending Home Sales in the United States remained stagnant at 0%, failing to meet the expected 1.0% increase. Later on Friday, the Chicago Purchasing Managers’ Index for December is set to be released, with expectations pointing to a decline from 55.8 to 51.0. As the year comes to a close, the market is experiencing a relatively quiet session, with traders entering holiday mode as they prepare for the transition into 2024.

GOLD Analysis:

XAUUSD Gold price is moving in an Ascending channel and the market has reached the higher low area of the channel

Gold is maintaining its position with elevated prices at $2080, primarily driven by ongoing tensions in the Red Sea, attributed to Houthi rebels. In parallel, the US Dollar has experienced a decline, largely influenced by the Federal Reserve’s dovish stance regarding potential rate hikes in 2024.

Geopolitical tensions have ratcheted up safe haven appeal from market participants with US data ahead of the Christmas break doing little to offer the US Dollar support. The lack of volume and liquidity this week could be a saving grace for Gold bears as it may limit the upside move. The renewed US Dollar weakness came about following a host of misses but US data in the week before Christmas. This has led to market participants remaining dovish on US rates in 2024 and thus weighed on the US Dollar.

Looking ahead and there is obviously a lack of catalysts this week and with muted volume expected the chance of rangebound trade looms large. The surprise following the Christmas break has come in the form of US Equities continuing their rally which is in contrast to the safe haven demand being experienced by Gold. However, this shouldn’t come as a complete surprise as US Equities for a while now have been disconnected from the consensus view by market participants. This was most evident in 2023, where with a host of downside risks, US Equities surprised and continued their advance. US Treasury Yields continue to tick lower as you can see on the chart below. The 2Y and 10Y yields continuing their downward trajectory as rate cut bets ramp up.

SILVER Analysis:

XAGUSD Silver price is moving in the Descending channel and the market has reached the lower low area of the channel

As we approach the year-end in the market this week, the US Dollar experienced a reversal yesterday. After a significant downward movement, the US Dollar saw an upward surge. This shift was primarily driven by the US Initial Jobless Claims data for December, which unexpectedly rose to 218K, surpassing the expected 210K.

On Thursday, data from the United States showed that Initial Jobless Claims increased by 12,000 in the week ending December 23, reaching 218,000, which exceeded the market’s consensus of 210,000. Continuing claims also rose to 1.875 million, marking the highest level in four weeks. Meanwhile, Pending Home Sales remained unchanged in November, failing to meet expectations of a 1% increase. Looking ahead, Friday will see the release of the Chicago PMI, but the primary focus is on next week’s employment reports.

The US Dollar Index hit its lowest point since July before making a sharp rebound, thanks in part to higher US Treasury yields, which climbed to 3.85% following the auction of the 7-year note. This boost in yields helped bolster the Greenback, allowing it to recover some of its losses for the week. This correction occurred alongside a continued rally on Wall Street, with the Dow Jones poised for another record-high close. While the overall trend for the USD remains downward, there is potential for further correction.

USDCHF Analysis:

USDCHF is moving in the Box pattern and the market has reached the support area of the pattern

The Swiss National Bank has stated that it may continue to intervene in the foreign exchange market to bolster the Swiss Franc’s position. Consequently, USDCHF reached its lowest level since 2015. Additionally, today’s agenda includes the release of the KOF Leading Indicator, with expectations of it rising from its previous reading of 96.7 to 97.0.

The US Dollar Index is currently trading near 101.10, with the yields on 2-year and 10-year US Treasury notes at 4.26% and 3.84%, respectively, at the moment. Furthermore, weaker economic data from the United States may have contributed to the Greenback’s decline, reinforcing market expectations of a dovish stance from the Federal Reserve in upcoming policy meetings. Notably, US Initial Jobless Claims for the week ending December 23 increased to 218K, surpassing the market’s projection of 210K. Additionally, November’s Pending Home Sales remained flat at 0.0%, missing the expected 1.0% growth following a previous decline of 1.2%. The upcoming release of the Chicago Purchasing Managers’ Index for December is anticipated to show a reading of 51, down from the previous figure of 55.8.

Heightened risk aversion, driven by the ongoing geopolitical conflict in the Middle East, has led to increased demand for the safe-haven Swiss Franc . Concerns persist regarding the potential closure of the Gibraltar Strait by Iran, adding an element of caution to the overall situation. However, the return of major shipping companies to the Red Sea suggests a tentative step towards normalization.

In terms of economic indicators, the ZEW Survey Expectations decreased by 23.7 points in December, compared to a decline of 29.6 in November. The KOF Leading Indicator, scheduled for release on Friday, is expected to improve from 96.7 to 97.0. The Swiss National Bank appears ready to take a proactive approach, as indicated in its recent Quarterly Bulletin, expressing its willingness to actively intervene in the foreign exchange market to support the Swiss Franc.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

ANZ Bank predicts that EURUSD will reach the 1.1500 level by the end of 2024. This forecast is based on the expectation that the ECB will initiate rate cuts before the Fed in 2024. The narrowing interest rate differential is anticipated to drive the Euro’s upward momentum against the US Dollar in 2024.

The European Central Bank is expected to initiate easing measures in March 2024. It’s important to note that interest rate cuts may not necessarily have a negative impact on the Euro. As the gap in real yield between the United States and the Eurozone tightens, we believe this could help bolster the upside potential of the EURUSD exchange rate.

And According to analysts at Natixis, the importance of the US Dollar remains strong as a reserve currency and as the preferred currency for trade and financial transactions. This enduring relevance of the Dollar persists despite the United States’ decreasing significance in the global economy. To illustrate this, in 1986, the US accounted for 35% of global GDP, and this figure declined to 26% in 1990, 29% in 2000, 24% in 2010, and 25% in 2022, indicating a consistent reduction in the US’s share of the global economy.

However, what’s noteworthy is that the Dollar’s dominance in areas such as trade invoicing, foreign exchange reserves, international bond issuance, and foreign exchange transactions has not diminished. This resilience of the Dollar’s economic and financial influence, despite the US’s diminishing economic and financial clout, highlights the effectiveness of having a single reserve currency in the international monetary system.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has reached the higher high area of the channel

The Bank of England has opted to keep its tight monetary policy stance in place for England because the country’s inflation rate exceeds that of the G10 nations. As a result, any rate cuts are likely to be postponed, with the possibility of the next decision coming from the Federal Reserve.

US Treasury yields have experienced a decline following gains in Thursday’s trading session, a significant development that has put downward pressure on the US Dollar. Investors are anticipating forthcoming interest rate cuts. In the previous session, the 2-year and 10-year yields closed higher at 4.28% and 3.84%, respectively. However, as of the current press time on Friday, both yields have retreated slightly to 4.27% and 3.83%, respectively. Furthermore, discouraging US economic data, which includes a higher-than-expected increase in Initial Jobless Claims and flat Pending Home Sales for November, may have curtailed the Greenback’s advance.

This data further supports the likelihood of the US Federal Reserve adopting a more accommodative monetary policy stance in upcoming meetings. Specifically, US Initial Jobless Claims for the week ending December 23 surged to 218K, surpassing the market’s projection of 210K, while Pending Home Sales remained unchanged at 0.0% in November, falling short of the expected 1.0% growth. The Chicago Purchasing Managers’ Index for December will be closely watched on Friday, providing additional insights into economic conditions in the Chicago area and contributing to the overall assessment of the US economy.

On the other hand, the Pound Sterling appears to be staging a recovery, driven by market expectations that the Bank of England may maintain its restrictive monetary policy stance. In the United Kingdom, inflation currently stands as the highest among the Group of Seven economies. However, BoE policymakers face a challenging decision-making process, as they grapple with addressing high price pressures while simultaneously navigating the risk of the domestic market entering a technical recession due to deteriorating demand. These intricate economic dynamics add to the volatility and uncertainty in currency markets, impacting the performance of the British Pound. Market participants will likely closely monitor seasonally adjusted UK Nationwide Housing Prices data for December. The month-over-month report is expected to show no change with a reading of 0.0%, compared to November’s 0.2% increase. Yearly figures could indicate a 1.4% decline, a slight improvement from the previous decline of 2.0%.

AUDUSD Analysis:

AUDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The Australian Dollar is on a consistent upward trajectory in anticipation of this week’s release of China’s NBS Manufacturing and Non-Manufacturing PMI data. Given that China is Australia’s largest trading partner, the market eagerly awaits the potential impact of this data on the currency.

The Australian dollar has recently reached its highest value in several months, mainly due to the weakening of the US dollar. This trend is driven by market expectations of the Federal Reserve implementing more lenient monetary policies. Investors are holding onto the belief that the Fed will cut interest rates by approximately 155 basis points throughout 2024, which is contributing to the positive momentum of the Australian dollar, a currency known for its pro-growth characteristics. Looking ahead, the Reserve Bank of Australia is anticipated to commence rate cuts around May or June 2024. However, the timing and overall direction of this shift towards a more accommodating stance will greatly depend on incoming economic data.

AUDCHF Analysis:

AUDCHF is moving in the Box pattern and the market has rebounded from the support area of the pattern

China, being a significant trade partner for Australia, particularly in commodities, is currently in the spotlight. This is due to the impending release of the NBS manufacturing and non-manufacturing PMI report on December 31, 2023. China has been implementing stimulus measures to revive its economy following the lifting of COVID restrictions. A positive surprise in this data could set the stage for a strong start to the new year for the Australian dollar. Meanwhile, today’s focus is on US data, primarily initial jobless claims, which has been consistently monitored. The strong US labor market remains a topic of debate, especially in light of declining inflation. As we move into the first week of 2024, Non-Farm Payrolls will take center stage as a critical economic indicator.

AUDJPY Analysis:

AUDJPY is moving in an Ascending channel and the market has reached the higher low area of the channel

MUFG suggests that the Bank of Japan is poised to raise interest rates in the first half of 2024, although the exact month of the hike remains undisclosed. The essential requirement for the Bank of Japan is to see wage increases for workers that align with the 2% inflation target. When this alignment occurs, it is expected that the Bank of Japan will proceed with an interest rate hike.

The most significant mover in the foreign exchange market today is the Japanese Yen. MUFG Bank’s economists are assessing the outlook for USDJPY. While the exact timing of the first interest rate hike remains uncertain, the overall direction is becoming clearer. Our expectation persists that the Bank of Japan will move away from its negative rate policy during the first half of the upcoming year, which should further support the Yen’s recovery from its previously undervalued levels.

The recent resurgence of the Yen can largely be attributed to the anticipation that major central banks outside of Japan, including the Federal Reserve , will initiate interest rate cuts earlier and more significantly in the coming year. This expectation is likely to help narrow the policy disparities between these central banks and the BoJ.

NZDUSD Analysis:

NZDUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

The RBNZ is anticipated to postpone its policy easing in 2024, leading to a surge in the New Zealand Dollar against the US Dollar. Despite the contraction in GDP in the third quarter due to the RBNZ rate hike, the New Zealand Dollar is demonstrating strong performance against the US Dollar, GBP, and EURO.

The New Zealand Dollar is displaying strength, driven by the expectation that the Reserve Bank of New Zealand may potentially delay policy easing. This sentiment is further bolstered by the release of improved Consumer Confidence and Business Confidence data for November. Despite New Zealand’s Gross Domestic Product data showing a contraction in the third quarter, reflecting the impact of the RBNZ’s higher policy rates, Governor Adrian Orr’s cautious approach and recognition of forthcoming challenges, particularly regarding high inflation, highlight the complexities of navigating the economic landscape.

Additionally, ANZ analysts foresee that a global resurgence in risk appetite, combined with the favorable interest rate differential of the NZD, will provide upward momentum into 2024. Meanwhile, the US Dollar faces headwinds against the Kiwi Dollar as softer economic data from the United States increases the likelihood of the US Federal Reserve adopting a more accommodative stance in its monetary policy decisions early in 2024.

The Greenback may encounter resistance as Initial Jobless Claims unexpectedly rose higher than anticipated, reaching 218K for the week ending December 23, surpassing the market’s expectation of 210K. Furthermore, Pending Home Sales for November remained stagnant at 0.0%, falling short of the expected 1.0% increase. Looking ahead, the upcoming release of the Chicago Purchasing Managers’ Index for December, scheduled for Friday, will provide additional insights into economic conditions in the Chicago region, contributing valuable information to the broader assessment of the US economy. With no significant data events on the Kiwi’s calendar for the next week, traders will shift their focus to China’s Caixin Manufacturing PMI for December on Tuesday, recognizing the importance of China as New Zealand’s close trade partner.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/