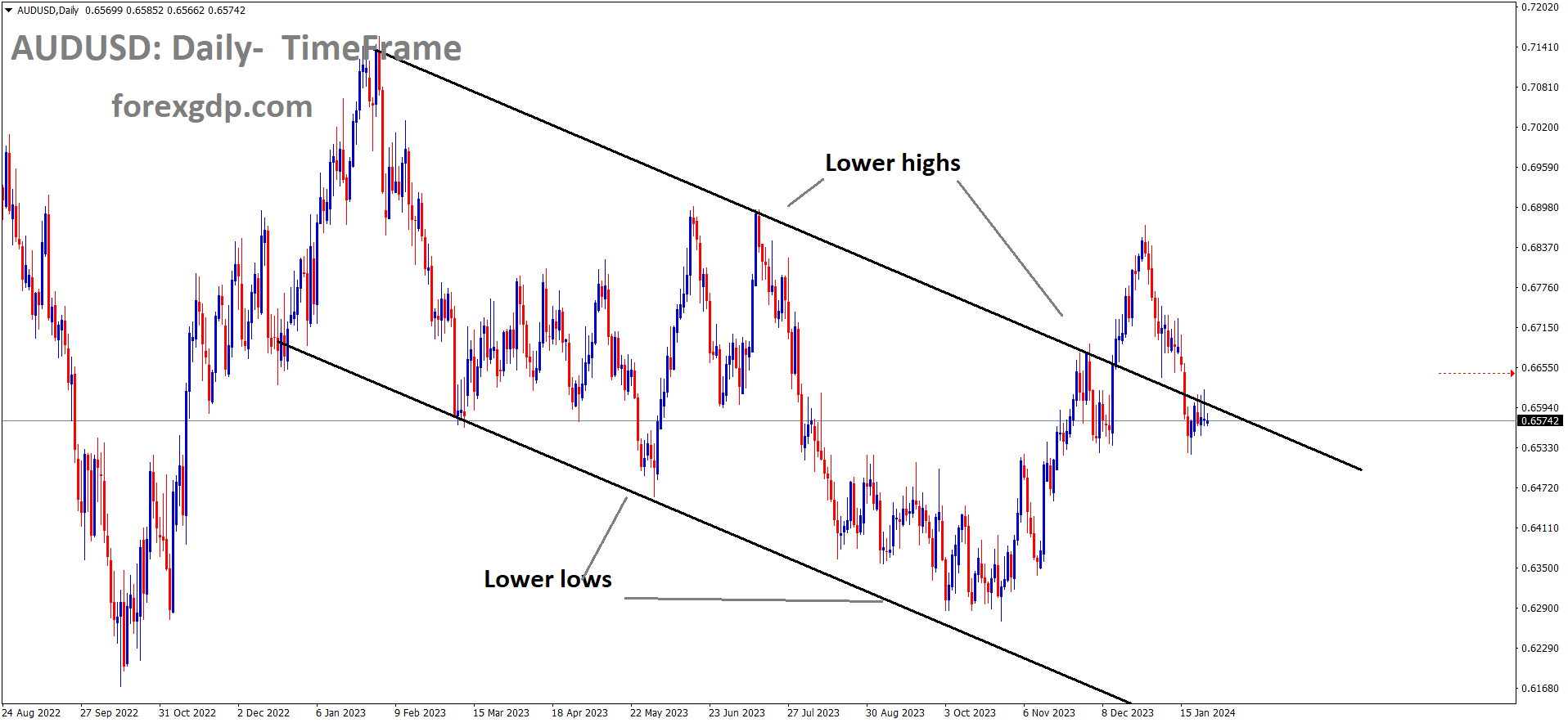

AUDUSD Analysis:

AUDUSD is moving in the Descending channel and the market has fallen from the lower high area of the channel

China’s economic stimulus measures and support initiatives for private enterprises and businesses are poised to counteract the economic slowdown. China is currently grappling with deflationary pressures, prompting various government interventions aimed at enhancing employment, wage growth, and the real estate sector. Consequently, the Australian Dollar experienced a decline due to China’s economic deceleration.

The People’s Bank of China has announced its intention to release bank capital that was being held with the central bank in February. This move is part of the latest initiative to bolster credit markets and the broader economy. In its first full year after the Covid-19 lockdowns, the Chinese economy failed to make a significant impression, facing challenges such as increasing protectionism and a global economic slowdown, despite being the world’s second-largest economy.

While much of the world is still grappling with persistent inflationary pressures, China has been wrestling with deflation, marked by year-on-year price declines. To counter this, China is now implementing another round of stimulus measures to reignite its sluggish economy. The central bank plans to reduce reserve requirement ratios for banks by 50 basis points (0.5%), building upon the 25 basis point reductions made in March and September of the previous year.

Although this move is a step in the right direction, its impact on investor sentiment remains uncertain, particularly as concerns persist about the immense Chinese property sector. While the Australian dollar initially responded positively, it has only seen a modest increase against the dollar thus far.

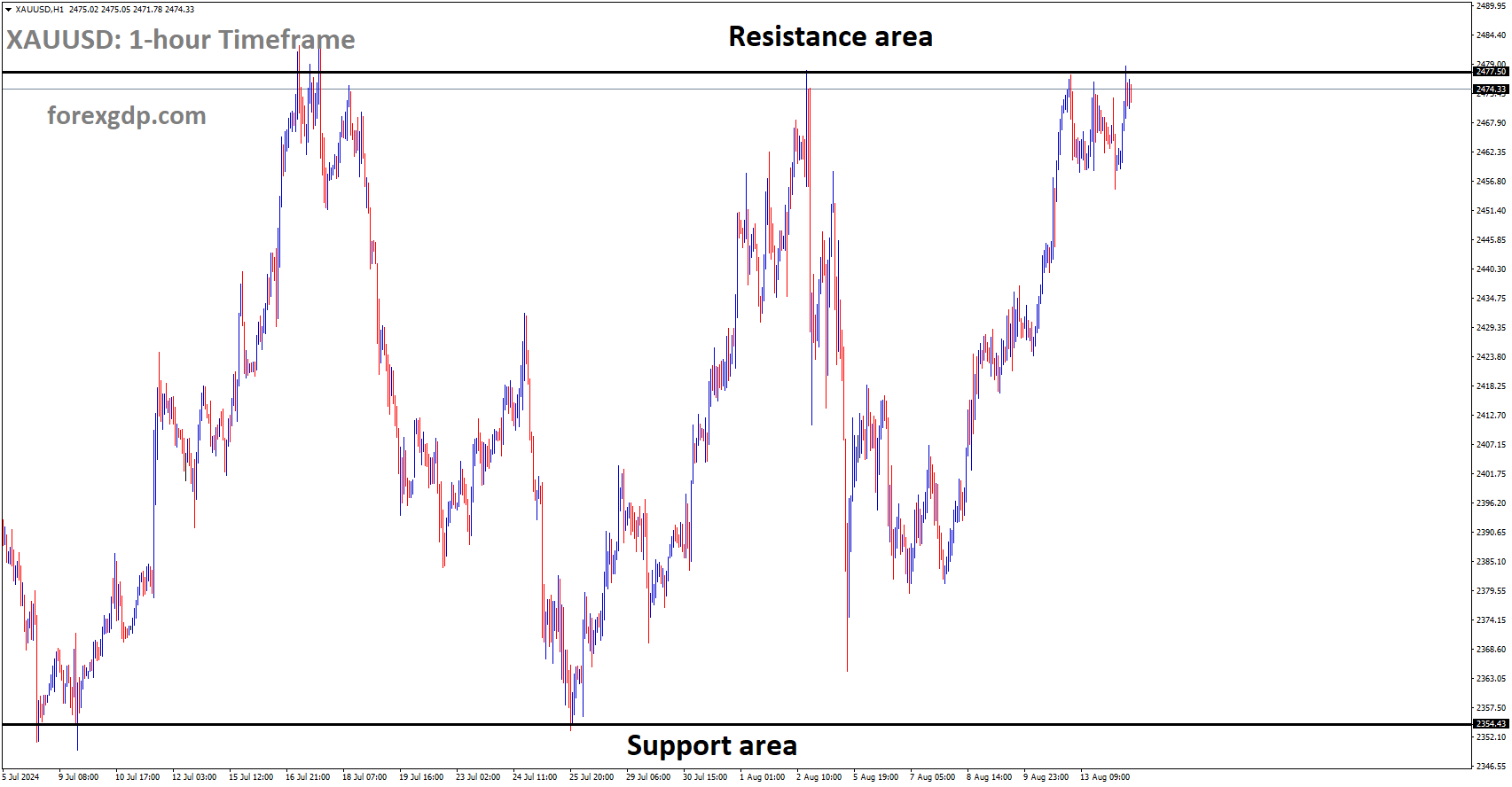

GOLD Analysis:

XAUUSD Gold price is moving in the Descending channel and the market has fallen from the lower high area of the channel

Gold prices saw a decline against the US Dollar following the release of positive US PMI data yesterday.

Gold prices have been exhibiting a slight positive bias during the early European trading session on Thursday, but this momentum has lacked follow-through, leaving the precious metal near the weekly low reached the previous day. Market participants are exercising caution, opting to stay on the sidelines and await the release of the Advance US Q4 GDP growth figures. These figures will offer insights into the Federal Reserve’s potential timeline for interest rate adjustments, which, in turn, will influence the direction of gold in the near term.

The US Dollar is facing challenges in attracting significant buying interest, remaining below its highest level since December 13, which was reached earlier this week. This subdued performance by the US Dollar is providing some support to gold. Furthermore, there is a looming risk of further escalation in geopolitical tensions in the Middle East, adding to the appeal of the safe-haven gold.

However, it’s important to note that reduced expectations for an aggressive policy easing by the Federal Reserve and the prospect of an early interest rate hike are contributing to elevated US Treasury bond yields. This, in turn, acts as a headwind for gold. Therefore, it would be wise to await stronger follow-through buying before considering any substantial upside positions, especially in anticipation of the US Personal Consumption Expenditures Price Index report scheduled for Friday.

The US Dollar remains under pressure, and geopolitical tensions in the Middle East are supporting gold’s safe-haven status. Notably, Iran-backed Houthi rebels in Yemen targeted two US-owned commercial ships near the Gulf of Aden, following multiple rounds of US military airstrikes. This incident follows preemptive US military strikes against the Houthis to prevent an alleged imminent attack on shipping lanes in the crucial Red Sea trade route.

On the economic front, the S&P Global flash US Composite PMI Output Index has shown strength, reaching 52.3 this month, the highest level since June, indicating a robust start to 2024 for the US economy. The flash US Manufacturing PMI also rebounded, reaching a 15-month high of 50.3 in January, while the services sector gauge climbed to 52.9, its highest reading since last June. These data points suggest the US economy’s resilience and have caused investors to revise down their expectations for a more aggressive Federal Reserve monetary policy easing in 2024.

Furthermore, the yield on the 10-year US government bond remains near its monthly peak, providing tailwinds for the US Dollar and restraining gains for gold. Keep an eye out for the Advance US Q4 GDP release scheduled for Thursday, as it is expected to show a slowdown in the world’s largest economy. Additionally, Thursday’s economic calendar includes Durable Goods Orders and Weekly Initial Jobless Claims, which could impact both the US Dollar and the XAU/USD pair.

Moreover, the highly-anticipated European Central Bank meeting could introduce market volatility and trading opportunities. However, the primary focus will remain on the US Personal Consumption Expenditures Price Index data, which serves as the Federal Reserve’s preferred inflation indicator, set to be released on Friday.

SILVER Analysis:

XAGUSD Silver price is moving in the Box pattern and the market has rebounded from the support area of the pattern

The US Dollar depreciated following the release of January’s PMI data for Services, Composite, and Manufacturing, which exceeded expectations. Manufacturing PMI surged to 50.3 from a previous reading of 47.9, while Services PMI rose to 52.9 from its previous reading of 51.4.

On Wednesday, despite better-than-expected PMI results, the U.S. dollar, as indicated by the DXY index, experienced a decline in its value. According to S&P Global, both the manufacturing and service sectors exhibited increased business activity at the beginning of the year, with manufacturing even entering expansionary territory and the service sector reaching its highest level in seven months. Both of these indicators pleasantly surprised by a significant margin.

The accompanying image illustrates how the January Flash PMI figures compare to initial expectations. Despite positive macroeconomic data prompting yields to recover from their initial session decline, the U.S. dollar continued to remain in negative territory. It’s worth noting that this reaction might be temporary. As reality sets in and traders recognize that the Federal Reserve may not be able to implement substantial interest rate cuts as anticipated by financial markets, we may witness the U.S. dollar regaining strength.

Looking ahead, the focus will shift to the release of the U.S. fourth-quarter GDP report on Thursday and the December personal consumption expenditures data scheduled for Friday. If incoming information confirms that the U.S. economy is maintaining its momentum and inflationary pressures persist, there is potential for the U.S. dollar to stage a modest recovery heading into the weekend.

USDCHF Analysis:

USDCHF is moving in an Ascending channel and the market has rebounded from the higher low area of the channel

UBS has officially announced the appointment of Aleksander Ivanovic as the Head of Asset Management overseeing a portfolio valued at $1.6 trillion. Mr. Ivanovic, who has been with UBS since 1992, boasts extensive experience in managing various financial assets. UBS CEO Sergio Ermotti delivered a welcoming address on this occasion.

UBS has appointed Aleksandar Ivanovic, an internal candidate, as the new head of its $1.6 trillion asset management business as part of the bank’s efforts to integrate Credit Suisse. UBS acquired Credit Suisse for approximately 3 billion Swiss francs ($3.46 billion) in a rescue deal last year, marking a multi-year integration process involving significant job cuts. This consolidation will result in a financial institution with a balance sheet roughly double the size of the Swiss economy.

Ivanovic, who will assume his new role in March, succeeding Suni Harford upon her retirement, will oversee a vital UBS division. However, it is notably smaller than UBS’s wealth management business, which contributed 50% of the bank’s revenues in the third quarter of 2023. In the same quarter, Asset Management accounted for 6.5% of UBS’s revenues.

Analysts have highlighted the challenge for Ivanovic, who has been with UBS since 1992 and has worked at Credit Suisse and Morgan Stanley as well. He will need to position asset management more prominently within the larger organization, particularly as the growth of passive investing puts pressure on fee income. UBS CEO Sergio Ermotti praised Ivanovic’s extensive experience and network across the bank, deeming him the ideal candidate to build on their strong foundation and advance integration plans.

While wealth management and the universal bank have been strong performers, asset management has struggled to define its role within the organization. Analyst Michael Klien at Zuercher Kantonalbank noted that Ivanovic would need to decide whether to retain all of the unit’s businesses. Despite the challenges, Ivanovic enjoys a solid reputation within the bank.

GBPCHF Analysis:

GBPCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

UBS is also preparing to identify a successor to Ermotti, who announced his intention to remain at the helm until the end of 2026. Iqbal Khan, head of wealth management, is widely considered the top internal candidate for the CEO role, according to media speculation. However, competition for the position is expected to be fierce, given asset management’s relatively minor role within the group.

UBS Chairman Colm Kelleher has expressed his desire to consider a shortlist of three internal candidates within the next few years, aiming for a seamless transition, as was the case at his former employer, Morgan Stanley. Additionally, UBS has announced that Beatriz Martin Jimenez will assume the role of Lead for Sustainability and Impact on the global executive board, in addition to her current responsibilities. Jimenez, who joined UBS in 2012, has held various key roles within the organization, including Investment Bank Chief of Staff, Chief Operating Officer, Group Treasurer, and Group Head of Transformation. These changes will become effective on March 1.

GBPUSD Analysis:

GBPUSD is moving in an Ascending channel and the market has fallen from the higher high area of the channel

The UK witnessed a notable increase in its Services, Composite, and Manufacturing PMI, reaching a reading of 52.5, surpassing the seven-month average and exceeding expectations. Consequently, the GBP gained strength against its counterparts in response to this news. Additionally, disruptions in the Red Sea contributed to higher inflation readings in the UK, subsequently affecting the manufacturing sector.

According to the most recent S&P Global PMI data, the UK’s services sector has reached an eight-month high, and the composite index has reached a fresh seven-month peak. However, the manufacturing sector has experienced a drop to a three-month low. Chris Williamson, the Chief Business Economist at S&P Global, reported that UK business activity has shown consistent growth in January for the third consecutive month, signaling a promising start to the year. These survey results suggest that the economy is on track for a quarterly growth rate of 0.2% after a stagnant fourth quarter, avoiding recession and indicating a renewed sense of momentum.

Furthermore, businesses in the UK have become more optimistic about the year ahead, with confidence reaching its highest level since last May. This optimism is partly attributed to hopes of faster economic growth in 2024, which is linked to the expectation of declining inflation and subsequently lower interest rates.

However, Mr. Williamson cautioned that “supply disruptions in the Red Sea are reigniting inflation in the manufacturing sector.” Supply delays have increased due to shipping routes being redirected around the Cape of Good Hope. Consequently, expectations for rate cuts in the UK have been revised downward. The market is now anticipating approximately 88 basis points of rate cuts this year, a significant reduction from the more than 125 basis points of cuts that were priced in at the end of last year.

EURUSD Analysis:

EURUSD is moving in an Ascending channel and the market has reached the higher low area of the channel

Yesterday, the Eurozone experienced disappointing figures in its Composite, Services, and Manufacturing PMI, falling below expectations. This marks the sixth consecutive month of economic contraction within the Eurozone. Despite rate hikes implemented by the ECB over the past year, this sluggish performance has persisted since June 2023.

The initial or ‘flash’ Purchasing Managers Index (PMI) data for the Eurozone in January has indicated that both the manufacturing and service sectors are performing below the critical fifty-point threshold, which distinguishes expansion from contraction. The composite index, which combines both sectors, recorded a value of 47.9. This fell short of the market’s expectations of 48 but was slightly higher than December’s reading of 47.6. Notably, the composite measure has now remained below fifty for eight consecutive months. Germany’s PMI data, released just before the Eurozone data, also displayed disappointing results.

The Eurozone’s start to 2024 has been sluggish, making the Euro’s resilience to this data somewhat surprising. One positive aspect is that the rate of contraction in overall business activity in January was the slowest in six months. Additionally, the decline in new orders reported by purchasing managers was the smallest since June 2023. There were also indications of a return in pricing power, with inflation rates having accelerated for three consecutive months since hitting a 32-month low in October.

However, a more plausible explanation for the Euro’s sustained strength on Wednesday could be that these data are unlikely to significantly influence the European Central Bank (ECB). The ECB is set to make its first monetary policy decision of the year on Thursday and is expected to keep interest rates unchanged, despite clear signs of economic weakness. The ECB may argue that it needs more time to ensure that overall inflation remains under control. Although Eurozone inflation has eased considerably from its peak of 10.6% in 2022, it still remains above the ECB’s 2% target.

CADCHF Analysis:

CADCHF is moving in the Descending channel and the market has fallen from the lower high area of the channel

The Bank of Canada kept its interest rates steady at 5.00% yesterday, which had a negative impact on the Canadian Dollar’s value against the USD. BoC Governor Tiff Mackhelm stated that their current focus is on addressing the increasing shelter and rent expenses, along with promoting wage growth accordingly. He also emphasized that there won’t be any rate cuts until inflation reaches the targeted 2% level.

The Canadian Dollar, often referred to as the Loonie, is facing challenges due to the cautious stance of the Bank of Canada (BoC), which remains hesitant about implementing rate cuts. Canadian inflation is not expected to reach the BoC’s 2% target until 2025, which has weighed down the Loonie. Money markets in Canada have reduced their expectations of a BoC rate cut in April from 65% to 40% following the release of the BoC’s monetary policy statement on Wednesday.

During a press conference following the policy statement, BoC Governor Tiff Macklem emphasized the BoC’s commitment to seeing a decrease in inflation before considering rate cuts. The BoC maintains that its current monetary policy framework is effective, but there is still a considerable distance to go in addressing inflation. Macklem stressed that discussions within the bank should focus on how long to maintain the 5% interest rate, rather than rushing into rate cuts.

The BoC hopes that Canadian economic growth will gradually accelerate in the second half of 2024, with inflation expected to fall below 2% in early 2025. The central bank is particularly concerned about rising rents, shelter costs, and high wage growth as areas of concern in the economy.

On another note, Wednesday’s US Purchasing Managers’ Index (PMI) data had the opposite effect, driving investors towards safe-haven assets. US figures exceeded market expectations, reducing hopes for broad-market rate cuts. The S&P Global Manufacturing PMI for the US reached a 15-month high at 50.3 in January, surpassing the anticipated reading of 47.9. This continued strong performance of the US economy has contradicted market forecasts, which were anticipating a slowdown that might trigger a cycle of rate cuts. Similarly, the US S&P Global Services PMI component also exceeded expectations, reaching a seven-month high of 52.9, compared to the forecasted decline from 51.4 to 51.0.

AUDJPY Analysis:

AUDJPY is moving in an Ascending triangle pattern and the market has reached the higher low area of the pattern

During this week’s monetary policy meeting, Bank of Japan Governor Ueda stated that the 2% inflation target is a short-term objective. The policy settings will be adjusted once wage growth and inflation start converging. Following the BoJ meeting, the 10-year bond yield rate increased yesterday.

The key takeaway from the recent Bank of Japan meeting is that Ueda remains focused on a potential exit from negative interest rates, even though inflation is displaying signs of deceleration. Ueda expressed optimism about the likelihood of achieving the 2% inflation target, and he even suggested the possibility of exiting negative rates if the current sub-optimal output gap is addressed.

Market sentiment points to the April meeting as an important event for the BoJ, with a full 10 basis points already factored in by the June meeting. The central bank’s primary objective is to sustain what it calls the virtuous cycle between inflation and wages. As wage negotiations are expected to conclude in March, market attention naturally turns to the April meeting for potential interest rate developments.

In the wake of the BoJ meeting, Japanese Government bond yields have continued to rise. This increase comes after a period of declining yields following the November peak, when inflation pressures began to wane, and market expectations for imminent rate adjustments cooled. The higher yields enhance the yen’s appeal and typically lead to a strengthening of the local currency.

NZDUSD Analysis:

NZDUSD is moving in the Descending channel and the market has rebounded from the lower low area of the channel

In anticipation of the release of the US Q4 GDP data today, the New Zealand Dollar experienced a decline against the US Dollar. Additionally, the New Zealand CPI data, which decreased from 5.6% to 4.7% yesterday, provides support for the Reserve Bank of New Zealand (RBNZ) to keep its cash rates unchanged.

The US Composite PMI for January exceeded expectations, registering a reading of 52.3 compared to the previous figure of 50.9. The Services PMI saw improvement, rising from 51.4 in the previous reading to 52.9, surpassing the expected value of 51.0. Meanwhile, the Manufacturing PMI for January climbed to 50.3, marking the first time it has crossed the 50 threshold in three months, improving from December’s reading of 47.9.

In New Zealand, the Consumer Price Index (CPI) for the fourth quarter eased from 5.6% to 4.7% year-on-year, aligning with expectations. The Core CPI, which excludes food, fuel, and energy, also declined to 4.1% year-on-year, down from the previous reading of 5.2%. Although inflation in New Zealand slowed during the final quarter of 2023, it is not significant enough to prompt the Reserve Bank of New Zealand to seriously consider an interest rate cut in the near future.

")

Furthermore, the People’s Bank of China made a significant announcement late Wednesday, reducing bank reserves substantially. This move is expected to inject approximately $140 billion into the banking system, signaling strong support for the struggling stock market and the fragile Chinese economy. The prospect of additional stimulus measures in China may have a positive impact on the New Zealand Dollar, often considered a China-proxy currency.

Looking ahead, Thursday will bring the release of the flash Gross Domestic Product (GDP) Annualized figure for the fourth quarter, with an estimated expansion of 2.0%. Additionally, the day will feature the release of the weekly Initial Jobless Claims and Durable Goods Orders data.

Don’t trade all the time, trade forex only at the confirmed trade setups.

Get more confirmed trade setups here: forexgdp.com/buy/